Counting the Evolution of GameFi Models: Is the Future Still Promising?

TechFlow Selected TechFlow Selected

Counting the Evolution of GameFi Models: Is the Future Still Promising?

GameFi has also gone through one full cycle of boom and bust. This article uses extensive charts to burst the bubble of GameFi's original sins and explores which models can achieve sustainable development in the future.

This article contains approximately 5,200 words and takes about 7 minutes to read.

Article Summary: GameFi has already gone through one full cycle of boom and bust. This article uses extensive charts to burst the bubble of GameFi's inherent flaws and explores what models might enable sustainable long-term development.

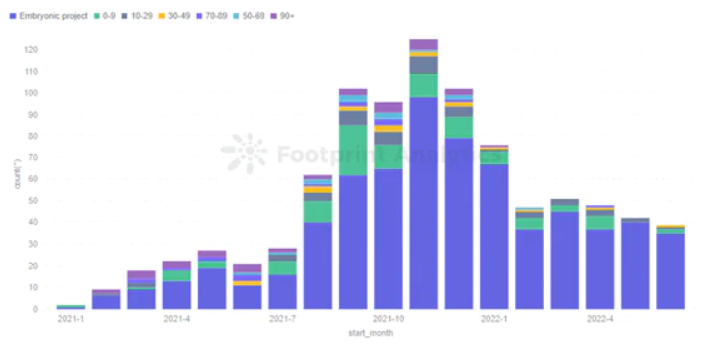

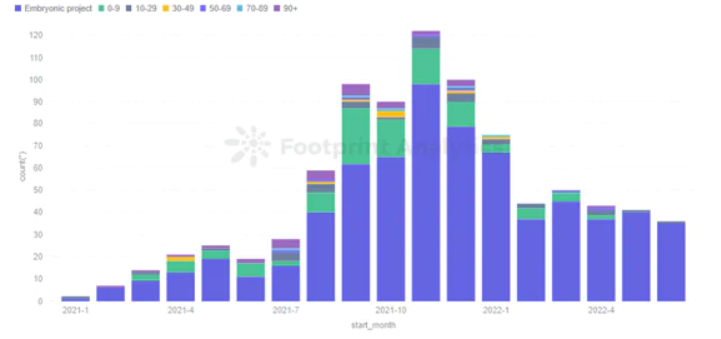

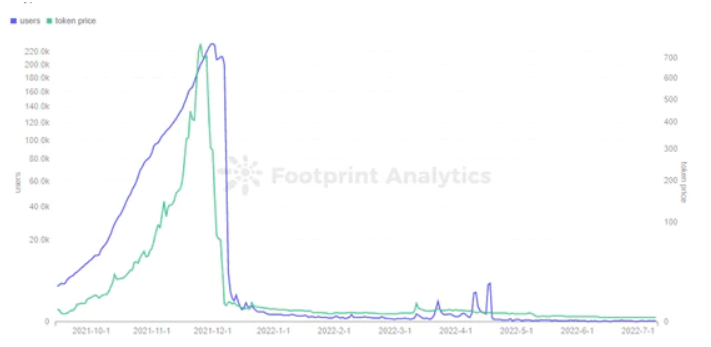

GameFi has been around for over a year—rapid user growth in the final quarter of 2021 gave way to stagnation by early 2022, with a clear downturn emerging in February.

In March 2022, fueled by the popularity of projects like StarSharks and Crabada, GameFi seemed to regain momentum. However, by April and May, both games inevitably fell into death spirals. StepN, which introduced the eye-catching Move-to-Earn model, also collapsed after announcing it would ban users from mainland China.

Within just one year, GameFi rapidly cycled through rise and decline. Despite the global base of three billion gamers, Web3 failed to attract many new players—most participants still came from existing crypto circles such as DeFi or NFTs. Looking at the landscape, the vast majority of GameFi projects have short active lifespans, but their developmental paths offer valuable insights:

1. Rapid Growth Leads to Fewer High-Quality Projects

The GameFi space is a mix of quality and low-effort fork projects chasing quick profits. About 70% to 80% of GameFi projects fail to maintain an average daily active user count of 200 for five consecutive days. Among projects launched in 2022, over 80% reached peak activity within 30 days—but how long did they last?

2. Project Lifespan Is Concerningly Short

Over 60% of projects become inactive within less than 30 days. Since November of last year, very few projects have managed to stay active for more than three months.

Most on-chain GameFi projects ramp up quickly from launch to peak activity, but struggle to sustain engagement over time.

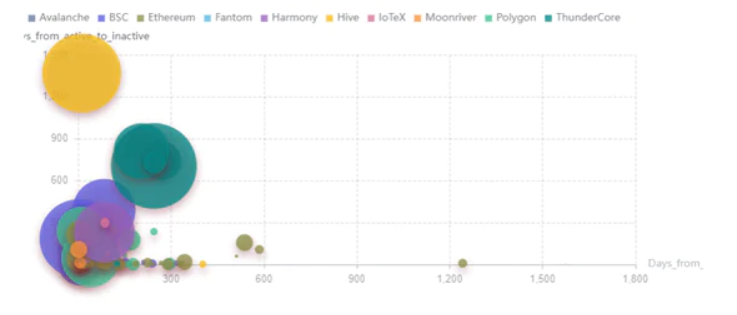

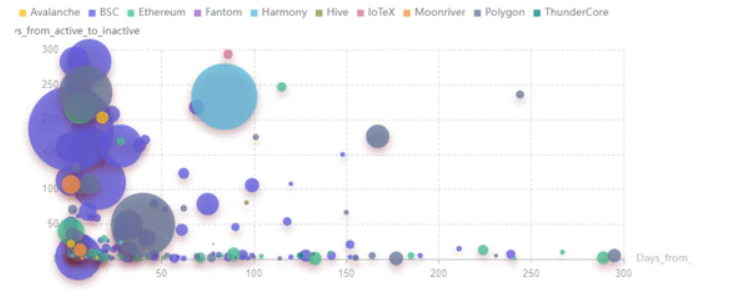

3. Different Blockchains Follow Divergent Development Paths

By analyzing the lifecycle of GameFi projects—from launch to active phase and eventual decline—we set the x-axis as the number of days required to reach active status, the y-axis as duration spent in active state, and bubble size representing total user count.

Projects further left rose to activity faster after launch; those higher up remained active longer. Therefore, projects located in the upper-left quadrant perform better overall.

HIVE stands out among all platforms thanks to Splinterlands. It entered its active phase shortly after launch and remains active today, appearing as a large yellow bubble in the upper-left corner.

Ethereum’s high gas fees and slow transaction speeds make it less suitable for GameFi. Most projects on Ethereum experience long initial ramp-up periods, brief active phases, and relatively small user bases. Nevertheless, given its strong foundation, solving these issues could allow Ethereum to capture greater market share once higher-quality games emerge.

In contrast, BSC tends to produce viral hits more easily, with moderate longevity and decent user scale.

Polygon performs reasonably well, while ThunderCore shows unexpectedly sustained activity duration.

Beyond bear market pressures, GameFi’s current state stems largely from its own structural flaws. This report aims to uncover the root causes behind these problems and explore possible futures for GameFi.

I. The Original Sin of GameFi 1.0 Models

1. The Wild West First Half

The era of GameFi 1.0, led by Axie Infinity, was centered around Play-to-Earn (P2E).

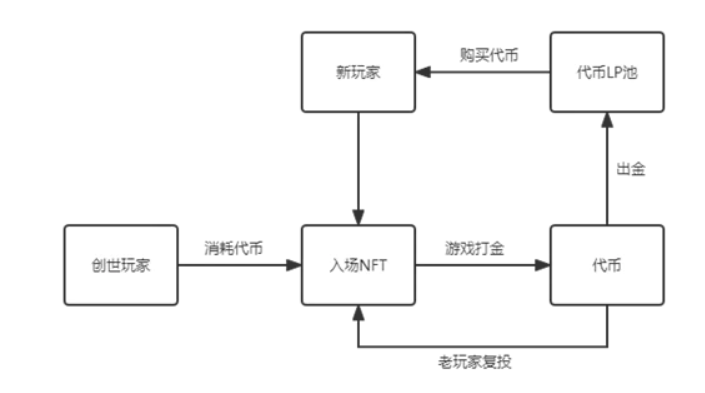

Regardless of gameplay mechanics—be it simple staking, PvE tower climbing, or card-based PvP—or economic designs (single-token, dual-token, Token + NFT, USD-pegged, crypto-pegged, etc.)—the core framework remained fundamentally Ponzi-like, relying excessively on continuous inflows of new capital—a so-called “external cycle” model.

An external cycle refers to a system where early players reinvest funds from new entrants, who continuously pay returns and interest to earlier participants, creating an illusion of profitability. Thus, all tokens earned internally by players must be consumed or purchased by new players. Otherwise, constant selling without sufficient buying pressure leads to token pools having only sell orders, triggering a death spiral in token prices.

According to data from Footprint Analytics on GameFi token market caps, after steady growth between July and September 2021 and explosive expansion from October to November, incoming capital began slowing due to broader macro conditions and individual project failures. Under such circumstances, the external-cycle mechanism of GameFi 1.0 quickly unraveled—external funding could no longer meet internal compounding demands—leading to a shift from positive feedback loops to negative death spirals.

As a result, most GameFi 1.0 projects follow a single life cycle. Once they enter a death spiral, recovery becomes extremely difficult. Various factors—including different models, teams, backgrounds, operations, and environments—influence each project’s trajectory, resulting in diverse lifecycle patterns.

- Blue-Chip Project Pattern

As the pioneer of Play-to-Earn, Axie Infinity had unmatched advantages in background, resources, and player consensus compared to other blockchain games at the time.

Even with just a basic dual-token model and breeding system, it maintained growth for several months before gradually declining, retaining a loyal user base to this day.

- Strong-Backed Project Pattern

BinaryX, another dual-token model project, leveraged community consensus to attract large holders’ locked stakes and created a powerful wealth-generation effect, drawing massive early adoption. However, it faced infinite inflation risks in its secondary token—if gold-farming incentives weakened, it immediately entered a downward spiral, leading to rapid user decline.

Still, thanks to tight control over BNX by exchanges and the team itself, the token price saw some rebound, though actual game users remain minimal.

- Pure Fund-Raising Scheme Pattern

CryptoMines, using a single-token model, was essentially a pure fund-raising scheme—the lifecycle pattern typical of most "shitcoin" projects.

Initially, it attracted significant capital via extremely short payback periods, causing both user numbers and market cap to surge dramatically in a short time. When the bubble reached the critical point of available capital and sentiment, it burst instantly—the higher it climbed, the faster it crashed. Almost every hot project at the time collapsed abruptly into a death spiral.

Despite differences in economic design, operational strategy, and lifecycle shape, whether established leaders like Axie Infinity, top-tier meme coins like CryptoMines, or metaverse concepts like The Sandbox—all hit roadblocks in December 2021.

The entire GameFi sector entered a winter. While macroeconomic factors played a role, the deeper cause lay in GameFi’s intrinsic Ponzi nature. After months of FOMO-driven euphoria, the rate of capital expansion could no longer keep pace with internal yield demands—making a bubble burst inevitable.

2. The Second Half: Gradual Innovation

After a round of market cleansing and consolidation, a few credible projects—with minor economic innovations and strong operations—managed to spark renewed interest in GameFi during Q1 of this year.

Among them, Crabada on Avalanche and StarSharks on BSC stood out.

StarSharks generated buzz early by leveraging associations with “Tianmei” (Tencent Games) and “Binance,” allowing its genesis blind boxes to trade at significant premiums even before the game launched.

Unfortunately, it launched right into the GameFi winter when player enthusiasm for earning rewards plummeted.

As a result, StarSharks never achieved high player counts initially and was mockingly dubbed “peaked at launch.”

However, compared to earlier wild-west-era projects, StarSharks had advantages in team credibility, economic design, and game quality.

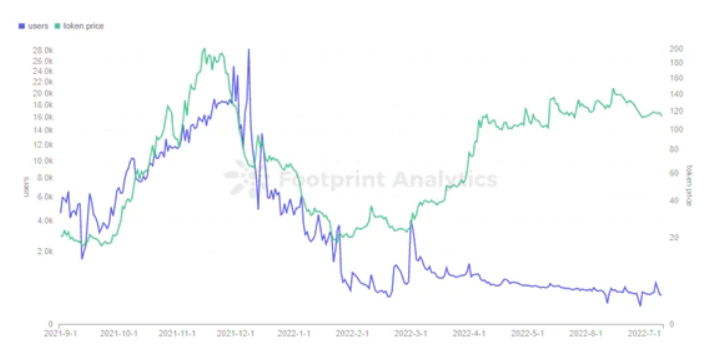

Combined with strong community support, it steadily grew throughout Q1 and peaked in April before gradually declining.

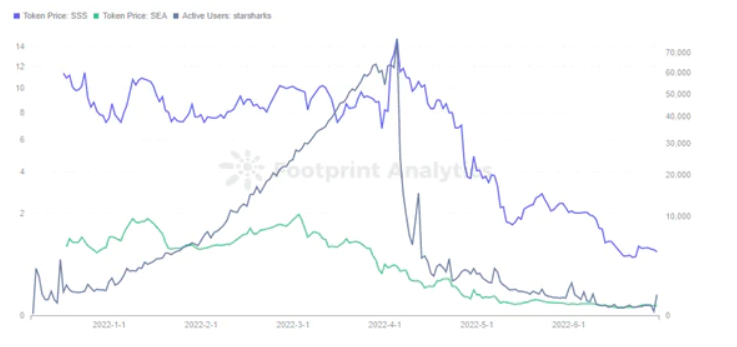

Footprint Analytics - StarSharks Monthly New Users & Active Users

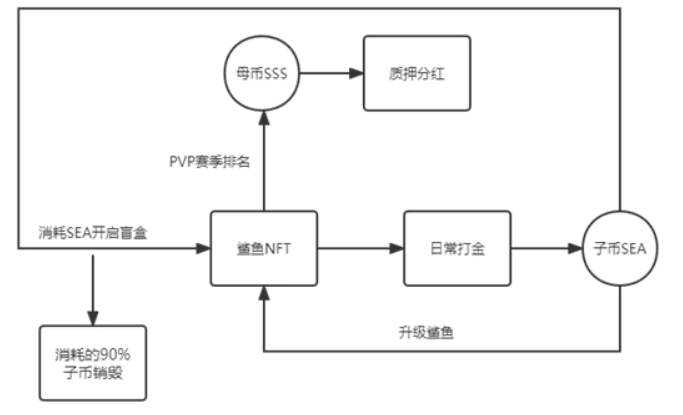

Analyzing its model, StarSharks adopted the classic dual-token structure: SEA as the main utility token and SSS as the governance token.

To prevent unlimited inflation of the secondary token SEA (which often triggers death spirals), StarSharks made entry dependent on spending SEA to buy blind boxes, shifting selling pressure from tokens to NFTs. SEA became central, with 90% of spent tokens directly burned, reducing circulating supply.

Meanwhile, the primary token SSS mainly offered staking rewards, but since its utility was limited, emissions were kept low.

Data from Footprint Analytics shows monthly active users rising steadily from January to March, indicating consistent SEA consumption. Yet starting in early March, SEA’s price began trending downward, signaling that accumulated in-game output was accelerating—supply soon exceeded demand, reflected quickly in falling prices.

Sure enough, in early April, removing daily tasks and the rental marketplace lit the fuse—user counts plunged sharply. For GameFi projects, model analysis and data tracking can effectively signal which stage a project is in.

Although StarSharks swam against the tide during a downturn, it ultimately couldn’t escape the death spiral. Its journey offers important lessons for other GameFi projects:

Advantages:

1. Given the relatively small GameFi capital pool, only a few hundred active users are needed to kickstart a project in the early stages.

2. Strong narrative and backing helped build anticipation and trust in Q1/Q2 GameFi launches, attracting broad interest.

3. The team successfully timed the transition between cycles, shifting from aggressive, fast-return P2E to stable, longer-payback earning models, enabling sustained wealth generation supported by community and whale participation.

Disadvantages:

1. Although lifespan was extended, the fundamental architecture remained unchanged.

2. Failure to roll out timely updates caused profitable users to exit, disrupting ecosystem balance.

II. What Might the Future of GameFi Look Like?

Ultimately, StarSharks failed to avoid the death spiral—but it does reveal a trend: crude, 5–7-day ROI P2E models are being phased out in favor of higher-quality games offering 30–90-day payback periods.

Yet just as optimism returned, GameFi 1.0’s second half failed to deliver standout performance in Q2. Whether measured by number of new games or total game assets, the sector showed signs of gradual decline.

So, what kind of model will enable GameFi to thrive sustainably?

1. AAA Games Prioritizing Content Quality

AAA games refer to titles with high development costs, large scale, and superior quality. There is no objective standard for AAA classification, so in GameFi, projects are generally evaluated based on team strength, vision, and demo quality. Widely recognized AAA candidates include BigTime, Illuvium, StarTerra, Sidus, Shrapnel, and Phantom Galaxies.

These AAA games enjoy clear advantages—generating massive attention upon launch—but still face criticism:

-

Slow development progress

-

Graphics and content only slightly better than typical Web3 games, far below traditional gaming standards

-

Insufficient utility for game assets post-IDO/INO

-

Unclear or unexecuted roadmaps

Even tokenized projects saw their valuations decline in the first half of this year alongside the broader GameFi downturn.

Nonetheless, AAA games remain promising. While Play-to-Earn remains controversial in GameFi, high-quality content is universally desired. Any positive news or events related to these AAA titles can significantly boost player confidence.

Eventually, we may see a golden age of AAA GameFi, with diverse genres—MOBA, RPG, SLG—each tailored to specific audiences and experiences. Games won’t need to obsess over P2E mechanics but instead focus on genuinely fun gameplay and unique blockchain benefits, encouraging real engagement. Players may need to wait—perhaps until Q2 or Q3 next year, or longer—but this path leads toward true gaming excellence.

2. Narrative-Driven X2E Products

StepN was undoubtedly this year’s flagship project, igniting global interest in Move-to-Earn and pioneering the X2E niche—Learn-to-Earn, Sleep-to-Earn, Watch-to-Earn, Sing-to-Earn, etc.

According to Footprint Analytics, while other X2E models remain conceptual, StepN’s M2E variant led a wave of popularity in May, spawning countless imitators.

But beyond Genopets—which follows a Pokémon-style gameplay loop—other X2E projects like StepN, Korean sneaker app SNKRZ, singing platform Melody, and jump rope fitness FitR resemble Web3 products with earning features rather than full-fledged games. Hence, social functionality becomes key to user retention.

As part of the broader metaverse vision, SocialFi remains highly sought after. Features like open-world chat, leaderboards, in-game competitions, and guild battles provide immersive experiences beyond mere earning. Currently, there are few true GameFi projects in this space—casual or card-based games could benefit greatly by integrating social elements.

3. Fi-Centric Transitional Games

No matter what lies ahead, the current mainstream remains rooted in Play-to-Earn. The mindset of earning through gameplay is deeply ingrained in Web3 users, so most developers continue iterating on economic models.

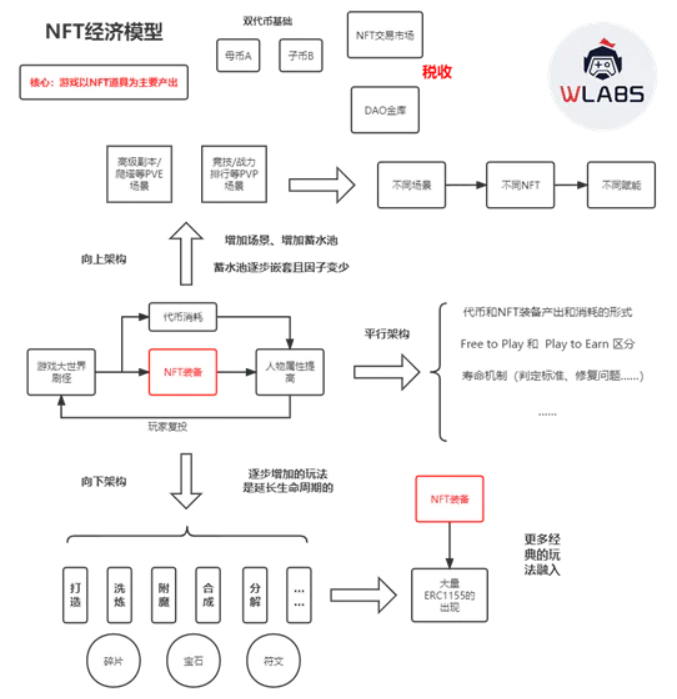

The dual-token model has proven resilient through market testing. Future GameFi designs will likely rely heavily on dual- or multi-token systems, incorporating DAO treasuries and proprietary NFT marketplaces. Innovations across multiple stages and careful numerical tuning will be essential.

Critically, the NFT marketplace must be owned by the project team, ensuring transaction taxes serve as a primary revenue stream—not solely relying on capital from new entrants.

Since NFTs will play a vital role in future GameFi ecosystems, projects should experiment with making NFT items the main in-game output—whether ERC-721, ERC-1155, or newer upgradable protocols like EIP-3664.

More importantly, the foundational game architecture determines sustainability.

Simple loops between token minting and character upgrades—as seen in GameFi 1.0—are too fragile.

This structure resembles a Ponzi scheme—later investors subsidize earlier ones. When the project shifts token sell pressure onto NFTs, once the NFT liquidity pool overflows, a death spiral ensues.

To enrich the ecosystem and extend lifespan, projects must expand horizontally and vertically beyond basic models. A sufficiently robust internal economy generates centrifugal force strong enough to resist gravitational pull into death spirals.

- Horizontal Expansion

Horizontal expansion enriches the base scenario with parallel frameworks. It introduces additional ways to earn and consume tokens and NFTs—such as implementing equipment durability and repair systems—or segmenting free-to-earn and play-to-earn players into distinct gameplay tiers.

- Vertical Expansion

Vertical expansion includes upward and downward dimensions. Upward expansion addresses the lack of meaningful roles beyond mining-and-selling—the dominant mode for 99% of players—by introducing advanced content like elite dungeons, PvE, and PvP modes. These scenarios should differ meaningfully and be enhanced through incentive alignment and shared consensus.

Downward expansion differs from upward—it extends lifespan by massively increasing item variety and gameplay depth. Examples include adding item fragments, gems, crafting, and deconstruction mechanics. The downward layer can borrow extensively from traditional game design principles.

III. Conclusion

GameFi 1.0’s lifecycle has demonstrated a stark difference between Web2 and Web3 gamers—at least for now. While Ponzi-like structures work as short-term acquisition tools, reliance on external cycles alone is unsustainable. Without establishing internal mechanisms to absorb prior bubbles, projects cannot escape death spirals.

Most current GameFi projects still lack engaging gameplay and fail to leverage blockchain’s technical strengths.

Thus, the industry must build transitional GameFi models from the perspective of Web3 users and economics. These transitional models lead to short-lived projects and uneven chain-level development—some chains host many low-quality games, others feature one breakout hit but unbalanced ecosystems.

The future of GameFi lies in innovation around content, gameplay, and visual quality.

Strong backing accelerates success, but maintaining community consensus over time is crucial for extending a game’s lifespan.

Whether through visually superior AAA titles, story-driven X2E initiatives, or economically sophisticated games, any of these directions could mark a turning point for GameFi’s resurgence.

End of article.

Data Source: Footprint × W Labs GameFi Report Dashboard

This article was jointly written by W Labs and Footprint Analytics. Follow us on Twitter @GuaTianGuaTian and @Footprint_Data.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News