How to build a banking system in the crypto world?

TechFlow Selected TechFlow Selected

How to build a banking system in the crypto world?

We have never been closer to a powerful cryptocurrency banking system.

Author: Seb

Translated by: TechFlow intern

This article explores the foundations required to build a financial system on top of decentralized finance (DeFi). While DeFi has experienced an explosion of innovation, much of it is used for circular speculation. Our focus here is on creating a useful financial system that funds the real economy.

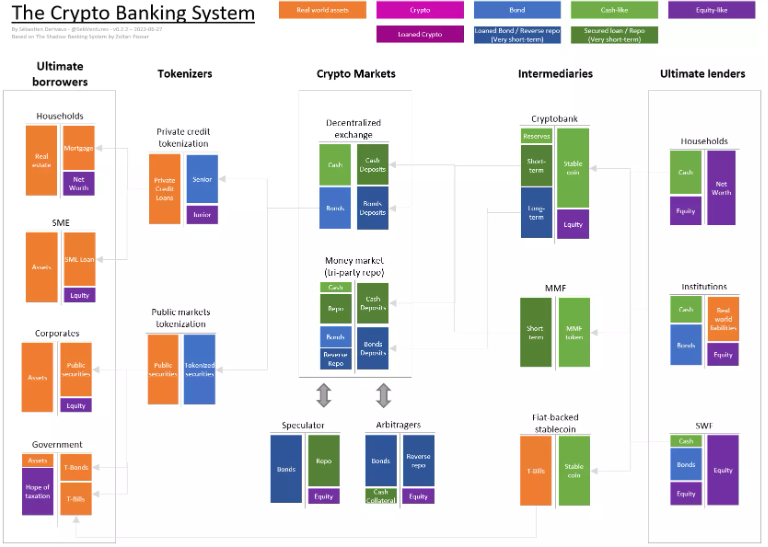

The diagram below, based on Zoltan's Shadow Banking System, provides a high-level overview of a crypto banking system. It also extends the discussions in “Crypto Banking 101” and “Crypto-banking Vs Shadow Bank.”

On the right are ultimate lenders (households with excess savings, financial institutions, sovereign wealth funds…), entities with surplus cash who can fund, at a cost or interest rate, ultimate borrowers on the left (households with mortgages, SMEs, large corporations, governments).

As you can see in the chart, native crypto assets (ETH, BTC, etc.) do not appear. This means it’s not a complete picture—the further work will analyze where crypto assets fit. You could also view cash as a cryptocurrency and assume real-world assets use the same unit of account; the mechanics remain the same.

As we’ll see, the key components of a crypto banking system are:

-

Creation of highly liquid tokenized bonds representing real-world credit (private credit and public markets).

-

A core infrastructure of market economies with decentralized exchanges and repo markets—i.e., crypto markets.

-

Crypto banking savings and lending intermediaries with mature maturity transformation operations.

The Need for New Primitives

DeFi is built on a trustless foundation, and most lending requires collateral. A key characteristic of good collateral is deep liquidity. People should be able to liquidate large positions quickly without significantly affecting price.

Currently, the main collateral used in DeFi is ETH and WBTC—both highly volatile (hence large loan discounts), with very limited supply and speculative in nature. They may be future collateral, but currently they are inconvenient.

Therefore, we need to introduce a new type of collateral. Gold is one example, already tokenized (as PAXG), but hasn't gained significant traction. If we look at TradFi, preferred collateral shifts from commercial paper to government bonds.

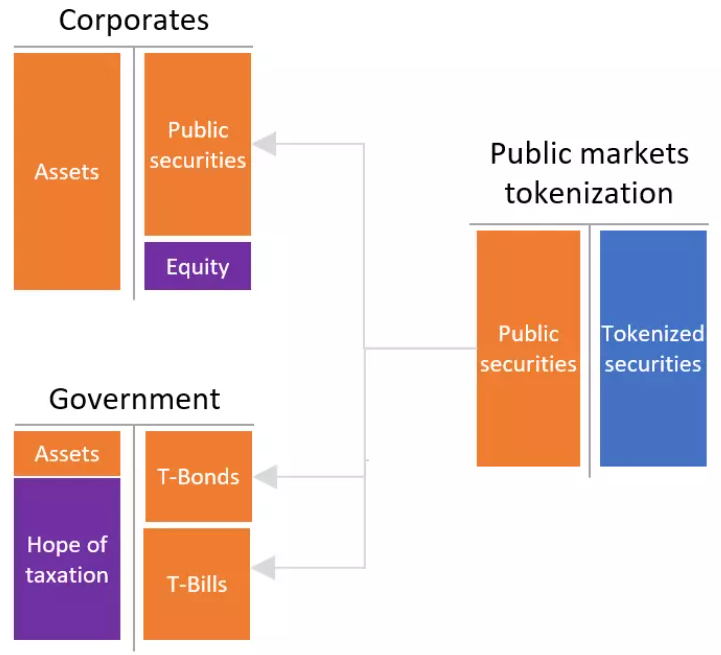

Tokenization of Public Credit

The first area for finding liquid collateral lies in on-chain public markets. Corporations issue bonds that are traded and rated by credit rating agencies. Government-issued bonds are also highly liquid and rated. Unlike crypto assets, these are more stable, meaning higher collateral efficiency. In TradFi, such instruments are considered safe and liquid enough to qualify as high-quality liquid assets.

Public market tokenization simply involves holding public securities on the asset side and issuing tokens (likely on a 1:1 basis). To achieve greater liquidity, similar securities can be pooled together, or ETFs can be brought directly on-chain.

An example is Backed Finance, which partnered with MakerDAO to tokenize the iShares USD Treasury Bond 1-3 Year UCITS ETF.

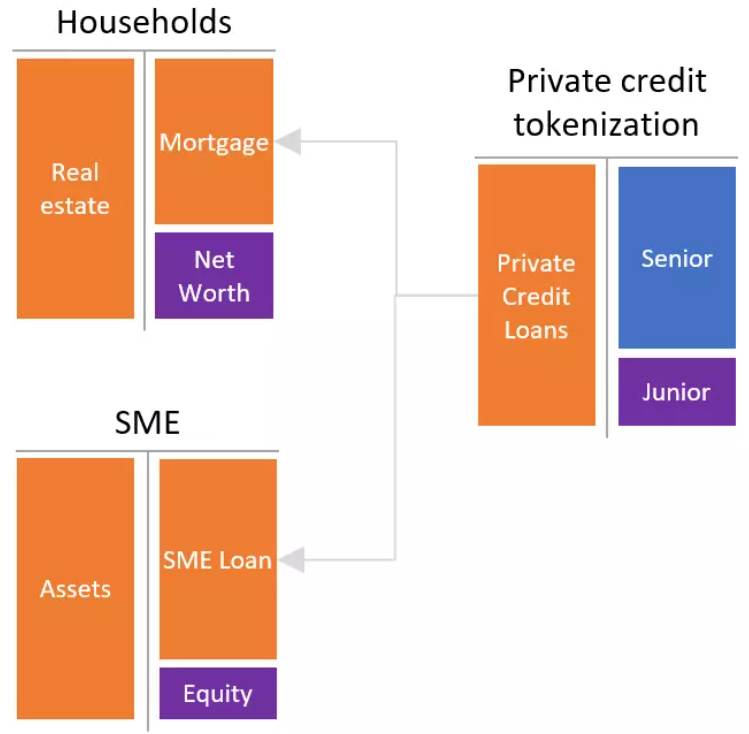

Tokenization of Private Credit

If we remain only at the public credit stage, many things could serve as collateral for years, but this does not create a better system, as it excludes households and small and medium enterprises (SMEs) from funding access.

The solution lies in securitization, where intermediaries pool these illiquid assets (loans are non-tradable) and issue two classes of tokens: senior and junior. The junior tranche provides credit enhancement to the senior tranche, offering security and easier price discovery, while forcing the intermediary to have "skin in the game." Ideally, the senior tranche should be rated by a credit rating agency.

This pool should also be large and transparent enough to encourage strong liquidity in the senior tranche market.

Two examples of such tokenization are New Silver and FortunaFi—New Silver focuses on fixed and variable loans (technically not yet suitable for households), while FortunaFi operates in revenue-based finance, aggregating loans from multiple asset originators.

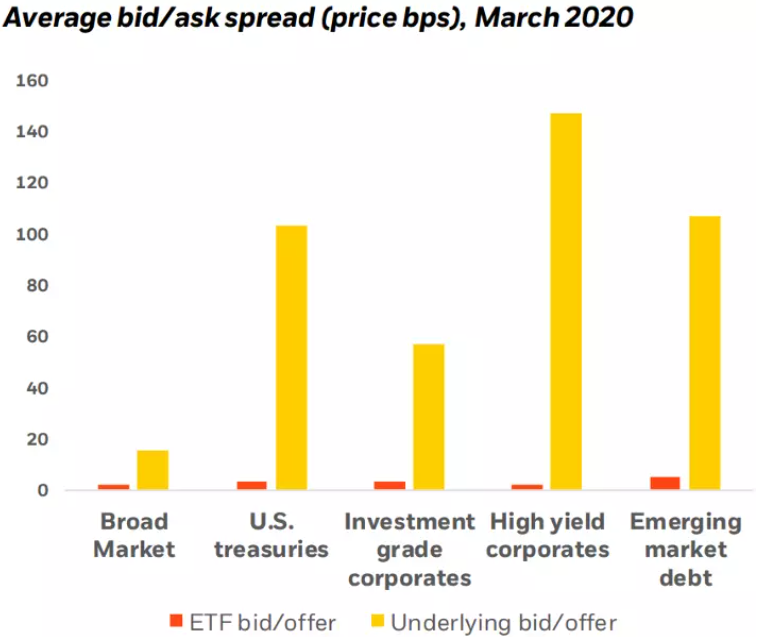

Scale and Liquidity Trump All

A critical point, whether in the public or private sector, is achieving sufficient scale to form a liquid market and avoiding fragmentation of liquidity.

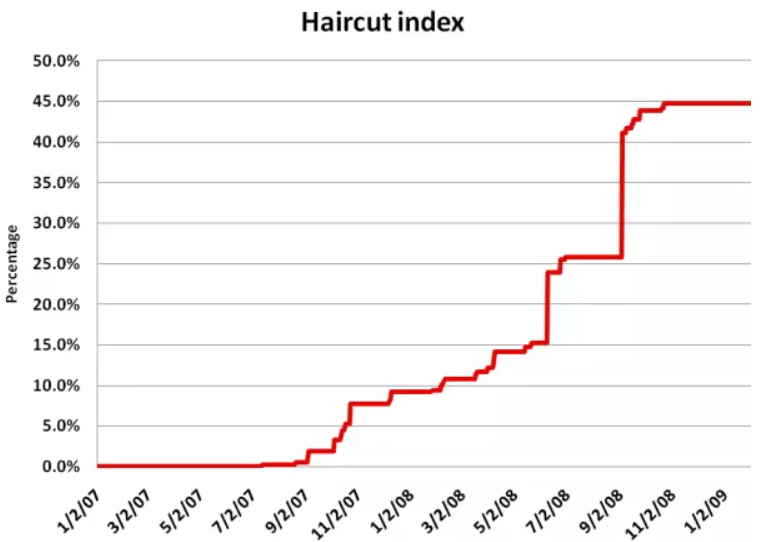

Some data shows that during March 2020, bond ETFs had far higher liquidity than their underlying assets, as shown in the chart below. Research also suggests such pooling reduces dumping impacts.

One issue during the global financial crisis was that illiquid securitized products were used as collateral. When the crisis worsened, higher haircuts were applied, or such collateral was excluded from repo markets.

Therefore, having highly liquid and highly transparent instruments to back the crypto banking system is crucial.

What is not shown in the crypto banking system are bonds issued by on-chain protocols and DAOs, whether backed by crypto collateral or not. Pooling these bonds would indeed allow the creation of another liquid and transparent bond instrument.

With these deep and liquid primitives, we will be able to build a robust crypto market.

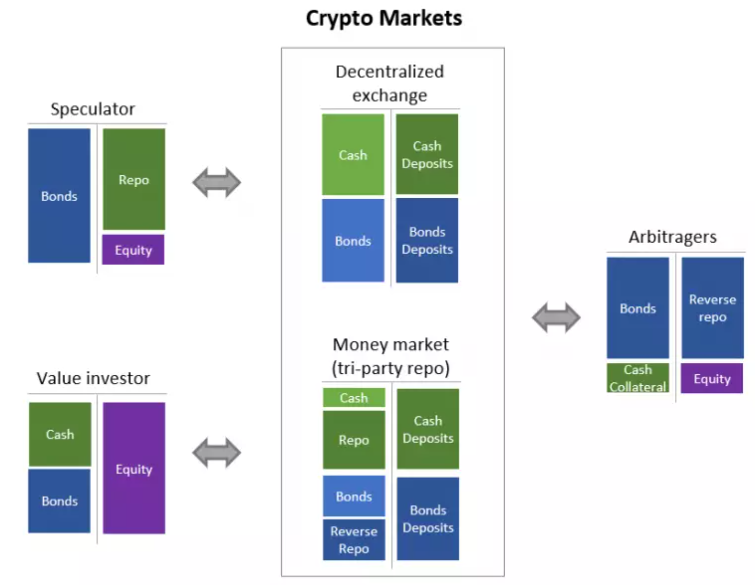

Crypto Markets

The core of the crypto banking system is the crypto market, which provides high liquidity (trading and short-term funding).

The crypto market itself consists of two sub-markets: one for trading (decentralized exchange or Dex), and one for short-term financing (money market). Both markets should be minimally governed and, to the greatest extent possible, immutable contracts. They should be trustless, permissionless, and unregulated.

Participants in the crypto market fall into three categories: value investors, speculators, and arbitrageurs.

The overall stability of the system is provided by value investors. They can be individuals, DeFi institutions (such as crypto banks or insurance protocols), or TradFi investors. For simplicity, assume they follow a predefined asset allocation (e.g., 50% cash, 50% bonds). They deposit some of these assets into decentralized exchanges, passively allowing market arbitrageurs to rebalance their positions to maintain constant exposure. They can also deposit unused liquidity and some bonds into money markets, allowing other participants to borrow them at a fee (again increasing returns for value investors, unlike costly custody in TradFi).

Arbitrageurs provide efficient markets by adding liquidity through small price fluctuations. If investment-grade bond prices fluctuate significantly, they can borrow **some bonds from the money market, swap them for some similarly-tenored Treasuries (to hedge interest rate risk) and some higher-credit-risk bonds (to hedge credit risk)**. These bonds will serve as collateral in the money market to fund their borrowing. These arbitrageurs can also provide liquidity to options protocols and enable orderly markets for on-chain ETFs (by arbitraging between ETF prices and underlying assets).

Finally, when speculative profit opportunities arise from going long one asset and short another, speculators will take on more risk (unhedged) than arbitrageurs. An example is when speculators believe the yield curve is too steep (or flat), going long Treasuries and refinancing these positions via leverage in the money market. Through speculation, they provide a price discovery mechanism.

By concentrating liquidity in crypto markets rather than leaving it idle in wallets, the crypto banking system can achieve greater liquidity than traditional markets at lower cost and complexity.

Bonds are designed to enhance liquidity because they are pools of low-liquidity assets (i.e., corporate bonds and mortgage loans). Crypto markets offer a way to use much of the market cap of these primitives as trading liquidity or funding enablers (and nothing prevents Dexes from using money markets in the background for liquidity).

To increase efficiency further, we need to introduce a new participant: the crypto bank.

Fractional Reserve Crypto Banks

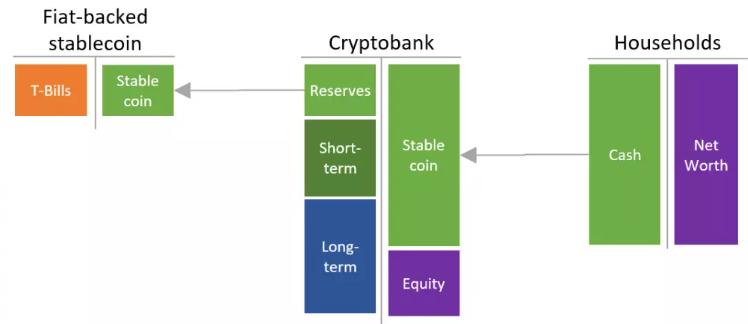

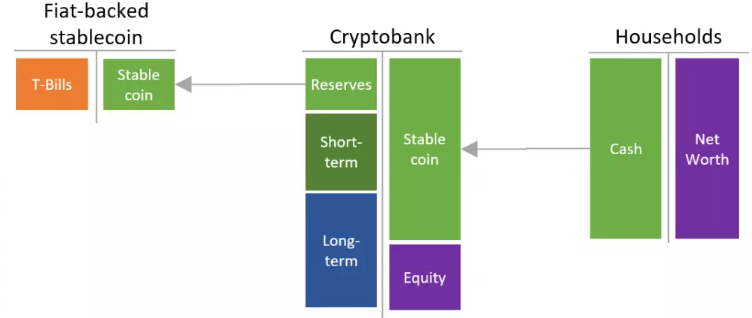

Under current definitions, a crypto bank consists of bonds and cash. We already know bonds are composed of tokenized pools of private credit and public market instruments. But what is cash?

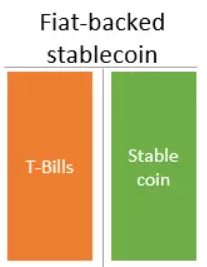

Defining Cash in the Crypto Banking System

Simply put, fiat-backed stablecoins are just $1 on-demand liabilities backed by Treasury bills (or bank deposits). This backing allows stablecoins to be redeemed at any time (on demand) without liquidity issues. Currently, the spread between the two (i.e., T-bill rates) goes entirely to the stablecoin issuer (or distributor), not to the stablecoin holders. This could change, but structurally, any interest paid to stablecoin holders would be capped by T-bill rates.

At scale, such a system may be detrimental to credit intermediation. Indeed, if stablecoins become the new bank deposits, they reduce the size of the latter, limiting traditional banks’ credit creation—this is where crypto banks come in.

Addressing Liquidity Preference and Expanding the Money Supply

There is a fundamental mismatch between ultimate borrowers who need long-term funding and ultimate lenders who have a preference for liquidity. As you can see below, most ultimate lenders hold cash, possibly large amounts. While there may not be a shortage of national deficits, it won’t allow sufficient funding for economic activity and leads to economic constraints.

To solve this, fractional reserve banking is introduced as a way to expand the supply of cash based on long-term lending.

As shown in the diagram below, thanks to intermediaries—crypto banks—a small amount of fiat-backed stablecoins can be expanded into a larger quantity through fractional reserve banking. Crypto banks issue a stablecoin perceived by creditors as money-like because it is redeemable for fiat currency (reserves). However, here lies the problem: there aren’t enough reserves to redeem all stablecoins at once. History shows this can lead to bank runs when trust erodes, yet even during recessions, banking systems can operate for years without collapsing. You can refer to the article “Crypto-banking 101” for more details.

Crypto banks are neither traditional banks (which hold illiquid loans), nor market-based banks (without maturity transformation), nor shadow banks (illusion of market-based maturity transformation). Crypto banks hold highly liquid assets as a defense against bank runs.

Conclusion

As we’ve seen, building a robust crypto financial system requires three components: tokenized real-world credit (bonds), a strong crypto market for trading and lending (providing deep liquidity and price discovery), and crypto banks providing maturity transformation.

At the time of writing, crypto markets are still incomplete but functional. However, we severely lack the bond component—tracks exist, but they’re mostly used for speculation. Crypto banks like MakerDAO are already integrating with money markets using tools like D3M. MakerDAO is also helping create bond primitives, including Centrifuge for private credit and Backed for public markets, and has proposed issuing up to $1 billion in short-term bonds.

We have never been closer to a robust crypto banking system.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News