Will Web3 Replace Web2 as the New Paradigm for the Creator Economy?

TechFlow Selected TechFlow Selected

Will Web3 Replace Web2 as the New Paradigm for the Creator Economy?

Web3.0 will be realized in the coming years—if we had to set a timeline, five or ten years—but the Web3.0 movement has already begun.

Authors: Zoe & FL Research Team

Will the emergence of Web3 mark a disruption to the Web2 creator economy model, which is centered on platforms and driven by advertising revenue? In this article, we focus on the creator economy market—first briefly outlining the current business models and core pain points of mainstream Web2 platform creators—and then argue that Web3 could shift the balance in favor of creators. We believe Web3 technologies may soon unlock new business models and economic opportunities, ushering in a new golden age of creation.

1 Tracing the Evolution of the Web

1.1 The Iteration from Web1 to Web3

For most of human history, people have been engaged in farming or production. In the 21st century, the two most important outputs are code and content. Code creates powerful tools that, among other things, help distribute content. Content supports powerful narratives that, in turn, help bring more economic activity under the control of software tools. Both aim to make abstract ideas actionable.

Based on the characteristics of different stages in internet development, we can divide its history into the eras of Web 1.0, 2.0, and 3.0. The rise of mobile internet shifted control over content creation and distribution—from traditional gatekeepers like publishers, record labels, and film studios in Web1—to creators who capture consumer attention within Web2 platforms. During Web2's golden decade (approximately 2005–2015), we lived in an era where ownership was concentrated in a few centralized tech platforms that controlled data ownership, user relationships, content distribution, and monetization.

1.2 Why the Creator Economy & Creators?

The digital media landscape has undergone massive changes over the past decade. For example, in China, time spent watching live streams now exceeds TV viewing time. In the U.S., users under the age of 25 spend more time on Twitch and YouTube Live than on television. Streamers, influencers, and other core content creators of the Web2 era are capturing attention previously allocated to traditional media, creating new consumption models such as content-driven e-commerce and livestream shopping. As of 2021, the creator economy had become a multi-billion-dollar market with over 50 million creators and attracted over $1.3 billion in funding. According to mediakix, the market size of the creator economy is projected to reach between $5 billion and $10 billion in the next five years.

2 Monetization Models of Mainstream Web2 Platforms and Their Core Pain Points

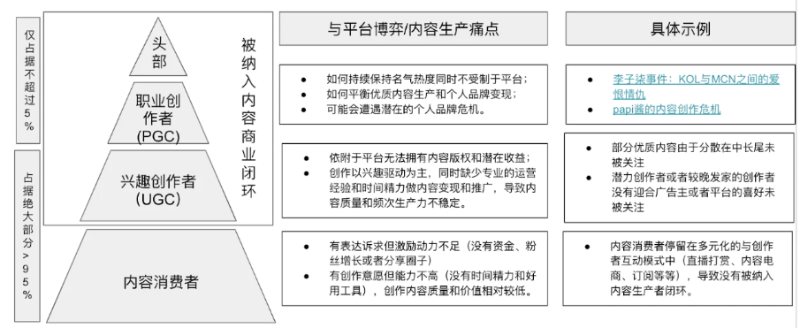

According to SignalFire’s map of the creator economy market, out of an estimated 50 million creators, around 2 million are full-time creators (less than 5%), while approximately 46.7 million are part-time creators. It’s important to emphasize that the Web2-focused creators are those who rely on mainstream social media platforms to distribute their content, build audiences, and profit primarily through sponsorships or ads—rather than direct transactions with their audience (users).

We broadly categorize existing Web2 content creators into the following groups:

Content Consumers: Refers generally to the majority of content-consuming audiences—the people who consume content daily or engage via likes, comments, and shares. They show lower willingness to produce content compared to interacting, though they possess conversion potential.

Hobbyists: Individuals who create content based on interest or as a side activity. With multimedia tools lowering barriers to entry, anyone can publish spontaneous creations on centralized platforms.

Professional Creators: Those with professional skills in content creation who work full-time and sustain themselves financially. These creators typically operate across multiple mainstream platforms, building followings through consistent output. Their monetization methods include ad revenue, platform subsidies, content-based e-commerce, user payments, and IP licensing. They tend to have higher production quality, and platforms often boost their visibility to retain more content consumers.

Top-Tier Creators: A subset of professional creators with deep influence in specific niches or broad appeal. They often wield more power than platforms, establish companies based on personal brands, and form partnerships with external platforms or brands—such as media companies, record labels, or MCNs.

The massive scale effect brought by the internet has made Web2 an era dominated by a few centralized giants. This business model heavily relies on closed networks, where each platform exclusively owns its accumulated user data. As dominant players controlling traffic and revenue distribution, large platforms are the biggest beneficiaries of the current creator economy boom—followed only by top-tier creators.

We summarize the core pain points of the Web2 creator economy as follows:

Existing pie distribution could be fairer: saturation in the creator market leads to unfair allocation of interests among stakeholders

Platforms own all user preference data and control content ownership and distribution—not the creators themselves—creating a vicious cycle of inequitable benefit extraction;

Early-mover KOLs benefit from initial growth momentum, capturing stable audience attention and crowding out newer high-quality creators in terms of visibility and disproportionate earnings. Despite their content being replaceable or improvable, due to limited user attention and reliance on algorithmic inertia, advertisers and platform algorithms favor already-popular creators—resulting in only a small number achieving sustainable livelihoods.

Mid-to-long-tail creators struggle to survive. On YouTube, for instance, most small channels aren’t truly active and are overshadowed by larger YouTubers. Researcher Mathias Bärtl demonstrated that in 2016, the top 3% of channels received 90% of views—meaning 90% of YouTube creators were competing for the remaining 10%.

Where is the new pie? Sustained growth in both quantity and quality of content requires fresh blood of new creators

Untapped potential creators (latent consumers and beginner creators) remain unengaged and excluded from the creator ecosystem;

Innovative forms of creation lack viable business models. Influenced by advertisers and recommendation algorithms, creators are pressured to seek broad audiences, producing content tailored to ad and brand appeal. As a result, genuinely novel content remains unproduced due to lack of monetization pathways.

Unfair distribution of data rights:

Opacity in big data collection, sharing, and circulation has led to frequent privacy breaches and data misuse. The fundamental issue of data ownership directly impacts usage rights and downstream profit distribution.

Although the proportion of users sensitive to data rights remains insufficient (“revolutionary” momentum is weak), public, governmental, and even platform-level awareness of rights and privacy management is gradually increasing. The centralized, closed approach to user data management urgently needs reform.

Overall, leading Web2 platforms have recognized these pain points and attempted reforms through innovative measures. For example:

Facebook CEO Zuckerberg recently announced that Instagram will launch a suite of influencer tools—including creator stores, local affiliate links, and a marketplace connecting influencers with brands—to capitalize on these opportunities.

Twitter introduced a Super Follows feature, allowing dedicated users to pay for exclusive tweets and access paid audio chat rooms.

TikTok established a native marketplace linking advertisers with creators and launched a $200 million fund to invest in top creators.

Beyond ad revenue sharing, YouTube has adopted a creator fund model, allocating $100 million to Shorts, its TikTok clone, to support creators.

Notably, in the mature phase of Web2, we’ve seen new platforms emerge aiming to displace giants by offering more direct subscription models and higher incentives to creators:

Substack, the breakout subscription newsletter platform, allows writers to keep 90% of subscription revenue;

Twitch streamers receive 50% of subscription fees;

Patreon creators earn 88%–95% of subscription income;

OnlyFans creators retain 80% of their earnings.

Whether it's the rise of third-party monetization platforms or major platforms launching incentives for mid-to-long-tail and emerging creators, the overarching trend is clear: sustained demand from consumers for “fresh and delicious cakes” necessitates richer and healthier content monetization paths—enabling creators to produce “more and tastier cakes.” The traditional, single-ad-revenue model must be broken. We see opportunities for creators beyond ads—through selling premium content, merchandise, coaching, consulting, etc.—allowing them to focus on delighting their most passionate fans and producing unique niche content instead of chasing mass appeal and broad audiences.

One might question whether the existing Web2 content ecosystem can achieve self-evolution through mild "decentralization"—does it require Web3 empowerment to foster a better creator environment? Can the two coexist rather than compete zero-sum?

Let us speculate. Self-revolution by Web2 tech giants isn't as simple as it seems. User behavior and preference data are a platform’s most valuable assets. Thus, big tech firms close off their ecosystems, locking users into network effects to accumulate proprietary data corpora. Since executives are accountable to shareholders and stock prices, partially opening up data access is already the maximum compromise they can offer. While most users don’t deeply care about privacy or data rights, the underlying issue is the right to profits derived from data ownership. As technology and user awareness evolve, unfair data ownership will inevitably lead to unequal profit distribution.

In the short term, Web2 and Web3 content ecosystems won’t be zero-sum; they’re more likely to coexist compatibly. After all, crypto user penetration is still far lower than that of Web2. The gradual reforms and innovations by Web2 giants may positively accelerate user awareness of Web3. Moreover, we believe Web3 doesn’t just enable fairer distribution of content power—it brings entirely new creators into the fold.

3 Where Is the Next Intersection Between the Creator Economy and Web3?

In Part 2, we discussed core issues in the Web2 era: privacy and data collection, misaligned incentives between ad-dependent platforms and user needs, and lack of innovation in content creation—all contributing to bottlenecks in content growth and dissemination. One reason Web3 excites many is that it returns power to the people via NFTs, bypassing platforms to connect producers directly with consumers. Ideally, independent creators would no longer depend on corporate or platform control, but could publish original content and earn revenue via decentralized platforms or communities. The creator economy includes not only individual creators and creative teams but also community builders and the financial and software tools designed to help creators earn and grow.

3.1 How Does Web3 Introduce New Rules for Content Creation and Consumption? What Might the New Model Look Like?

By tokenizing works as NFTs, creators establish a verifiable on-chain record of ownership and provenance. This process ultimately mints a unique asset (NFT) traceable back to the creator. Overall, we envision a shift from a world where creators depend on platforms for income, toward one where they—or they together with communities—can generate wealth independently. Two of the most significant changes Web3 brings to the creator economy are:

1. Changed incentive mechanisms (empowering users, redistributing platform profits to creators/users);

Blockchain networks act merely as “galleries” for works. Creators retain copyright and can upload works directly to public chains for commercialization—eliminating intermediaries who take profit cuts. Creators can leverage NFTs to design diverse monetization and fan engagement strategies.

2. Transformed trust mechanisms (breaking down platform/company boundaries, decentralizing control, changing data rights).

In the Web2 era, we relied on intellectual property law—a blunt instrument—for protecting creators and copyrights. In Web3, we aim to use smart contracts. Digital assets gain stronger rights protection from creation to consumption, ensuring fair profit distribution and ownership while avoiding copyright lawsuits and rampant piracy.

For example, creators can issue NFTs with a sense of “exclusivity” and “scarcity.” Owning a creator’s NFT can serve as proof of membership in a DAO—acting as a “badge” to express identity and mutual recognition. Value can be created in scenarios such as:

Owning an NFT issued by a favorite band grants backstage access at concerts;

Receiving an NFT as a receipt when supporting an idol, proving financial contribution;

Buying a rising creator’s NFT early and reselling it at a premium later, capturing investment “dividends” from content.

We imagine a future where two superfans might scan each other’s QR codes (or use another method) before meeting, checking each other’s NFT collections to understand shared interests and contributions—or jointly labor in a shared community: creating, consuming, and investing in content based on identity and values.

3.2 Can the New Model Address Unfair Distribution of Creator Interests and Content Power?

1. We believe Web3 enables fairer power distribution and unlocks greater creative possibilities through community co-building.

a. Content Ownership: Creators’ works exist independently of platforms, free from strong platform constraints.

b. Community Ownership: Creators build direct relationships with fans through new interaction models. Fan bases can come from multiple platforms,不受 centralized distribution.

c. Revenue Ownership: Creators can mint their own creator tokens. Revenue models aren’t dictated by platforms or reliant solely on advertisers/sponsors—they can define diversified income streams independently.

Content is stored in public databases, giving creators and consumers full flexibility in data usage. This means creators no longer have the same level of dependency on specific platforms as in Web2. Decentralized incentive mechanisms can reduce customer acquisition costs. Creators can issue social tokens to loyal fans to increase engagement, or even share copyright revenue with the community, promoting co-creation. Market transparency empowers creators to regulate markets, transitioning from platform-driven copyright monetization to self-directed models. Future works may also serve as social entry points, exhibiting multifunctional attributes across lifecycle stages.

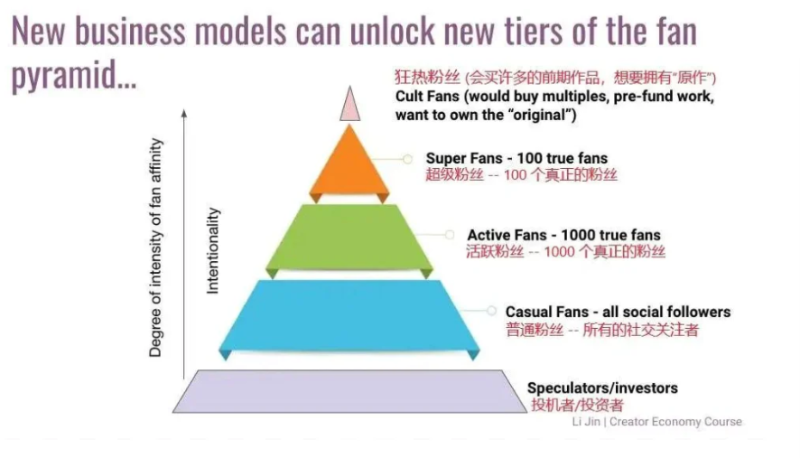

2. Helps rebalance risk and reward in the creator economy. “Lower wealth concentration means reduced risk of top creators being poached by competitors to threaten the entire business.”

Creators no longer need millions of followers or platform traffic protection to survive—they can thrive on support from a smaller base of passionate fans. Fans deeply committed to a creator’s work will willingly pay more, enabling creators to better capture their audience’s willingness to pay. For example, the thriving music NFT market demonstrates this effect. On streaming platforms, each play generates the same royalty (e.g., $0.004 per play on Spotify for paid accounts), regardless of how much a fan loves the artist.

3. Platforms no longer bear high costs moderating mid-to-long-tail content (illegal or gray-market material) or incubating long-tail creators—each community becomes responsible for its own content ecosystem.

3.3 Does Web3’s Model Bring New Creators and Hence New Content?

We observe that in the Web3 world, the boundary between fans and creators is blurring, fundamentally transforming the nature of creators. Developers, fan enthusiasts, and others can now be integrated into the commercial loop of content creation, extending works in new ways (e.g., IP remixing, content investment and circulation). This expands the value of existing works while introducing new profit-sharing mechanics for creators and consumers alike.

Imagine a second wave of creator growth fueled by active subscribers from existing channels—using YouTube as an example:

Full-time Creators (~2M+)

YouTube: Of 31 million channels, ~1 million creators have over 10K subscribers

Instagram: Of 1 billion accounts, ~500K have over 100K followers and are considered active influencers

Twitch: Of 3 million streamers, ~300K are partners or affiliates

Others: Musicians, podcasters, writers, illustrators—estimated at ~200K totalPart-time Creators (~46.7M+)

YouTube: Of 31 million channels, ~12 million have 100–10K subscribers

Instagram: Of 1 billion accounts, ~30 million have 50K–100K followers

Twitch: Of 3 million streamers, ~2.7 million are neither partners nor affiliates

Others: Estimated ~2 million musicians, podcasters, writers, illustrators

From this model, we can reasonably anticipate that in the Web3 era:

Existing creators can co-create with fans, generating new content;

Content consumers can be integrated into the production loop, becoming new creators;

Content cycles can be enriched: content not only consumed but also invested in.

If every high-quality creator inspires 10 influential fans to co-create, the growth in creators and content becomes exponential. This can be facilitated through Tokens that align incentives between creators and fans. *One example is Shibuya,* a Web3 video platform that “allows users to participate in, fund, vote on outcomes, and become owners of long-form content.” The idea is that fans can buy NFTs called Producer Passes and use them to vote on plotlines and characters in animated series. By doing so, fans earn $WRAB tokens representing proportional ownership in an NFT series.

The Quibbler’s latest issue How Web3 Affects Creators explains Web3’s impact on creators by comparing traffic acquisition in Web 2.0 and Web 3.0. An excerpt:

“A creator’s main income is no longer ads or platform subsidies, but the ‘money’ mentioned earlier. This ‘money’ is created by the creator, used to incentivize distribution, while the creator retains a portion. But this ‘money’ isn’t fiat currency—it’s more like stock: if you do more for the creator—sharing their work, giving effective suggestions—you earn this ‘stock.’ As the creator’s work gains popularity and the project’s success likelihood increases, more people want this ‘stock,’ driving up its price. This builds a more cohesive fan community. Thus, how this ‘stock’ operates becomes critical, giving rise to Token Economics—a field focused on designing healthy systems for this ‘stock,’ which is key to evaluating a project’s credibility.”

In summary, the new characteristics Web3 brings to the creator economy:

New creator groups:

Power distributed to individuals rather than platforms—reducing or eliminating intermediaries;

Opportunities open to all, regardless of scale of productivity—anyone can earn rewards and attention through passion and skill.

New content creation:

New creators bring new content;

New digital products and virtual services expand creative possibilities.

Optimized business models: powered by smart contracts and DeFi, creators

Gain more direct and diversified monetization options;

Enable more engaging and varied content circulation methods.

4 Controversies Around Web3 Creator Economy Development Are Inevitable

Historically, in 2017, a wave of blockchain social projects briefly emerged (ONO, QunQun, GSC, YeeCall, NRC, SwagChain, Huoxin, TTC Protocol). However, due to limitations in early crypto markets, user base size, and ecosystem models, most have since disappeared. In 2020, yield farming began integrating into various ecosystems. Fueled by DeFi, a new wave of mainstream SocialFi projects emerged—Whale, Chilliz, RALLY, Fyooz, Zora, and others.

We must critically assess: is the Web3-powered creator economy a fleeting fad or a genuine opportunity? And what conditions or turning points will signal its breakout moment?

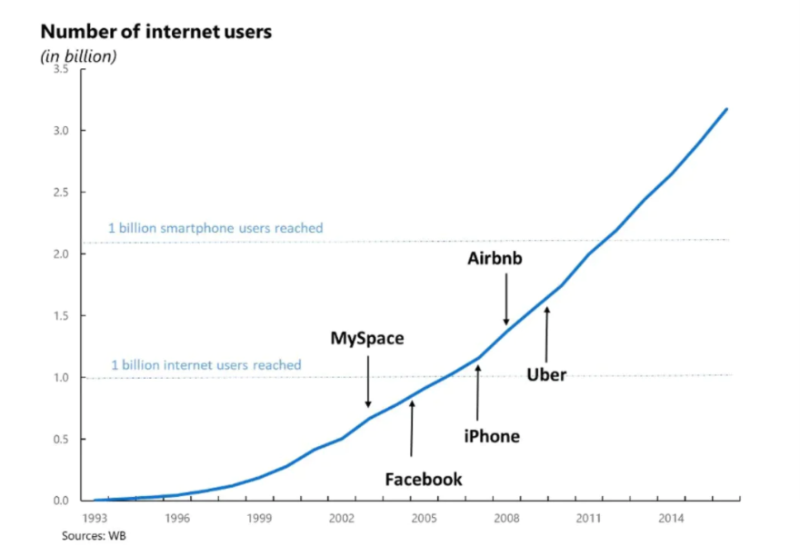

Historical patterns from the exponential growth of the internet and mobile devices (bandwidth + mobile internet + 4G built on accumulated big data and production resources) suggest that once a new technology reaches a user base of 1 billion, large-scale applications begin explosive growth.

In contrast, Ethereum currently has only 180 million addresses. Using this as a proxy for Web3 adoption, at current growth rates, it will take about five more years to reach 1 billion users.

Therefore, we believe the Web3 creator ecosystem hasn’t yet accumulated enough non-financial NFT data, behaviors, and information on-chain to trigger network effects—meaning the critical inflection point for SocialFi hasn’t arrived.

What obstacles exist in implementing Web3-social applications? Could they introduce new problems? Issues like incomplete legal frameworks for content ownership, trade-offs between decentralization and centralized platforms, and others warrant caution.

Currently, SocialFi is in its early stage. Most participants focus on social tokens, exploring conceptual expansions and technical updates. Few platforms are purely categorized under SocialFi, and many projects overlap with NFTs, GameFi, and other concepts.Analyzing the closed-loop chain around creator economy development:

From perspectives of original content and IP development, content storage and distribution infrastructure, community outreach and audience interaction, and commercial monetization, we are particularly bullish on vertical tool-based products—serving as gateways from Web2 to Web3, especially companies enabling creation or monetization.For example, starting a paid blog today involves registering on Substack, writing in Google Docs, designing graphics in Figma, setting up payment via Stripe Atlas, opening a bank account with Mercury, recording and editing podcasts on Descript, publishing via Anchor, and promoting on Twitter. These companies collectively help creators build, grow, manage, and monetize their audiences. Crucially, the essential tools for individual creators to enter the commercial loop are those enabling relationship-building, content distribution, and revenue generation.

CONCLUSION

During the golden decade of mobile internet, we lived in an era where ownership was concentrated in a few centralized tech platforms—controlling data, end-user relationships, and the means to distribute and monetize content. While content creation exploded during this time, it also led to widespread dependency of creators on centralized platforms, filter bubbles, and creative burnout.

The root cause of inequality in the creator space is the excessive control platforms exert over creators and their works through ownership of production means and content distribution. The most direct way to challenge this control is to change who owns the means of production. Fortunately, we see Web3 potentially shifting the balance of power toward creators.

The Web3 creator ecosystem is already taking shape—whether built on blockchain and NFT-based economic infrastructures or in-platform native token systems.Creators can leverage ecosystem tools to produce content and monetize via platforms, marketplaces, and communities. But identifying which innovations truly add value will require prolonged exploration and trial-and-error. We believe Web3 holds immense potential to bring incredible opportunities to everyone contributing and creating online: the true golden age of content creation we’ve always hoped for.

Quoting the founder of the IPFS protocol at the DLD International Conference:

“Web3.0 will happen in the coming years—if I had to set a timeline, five or ten years—but the Web3.0 movement has already begun.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News