Celo: A Stablecoin Ecosystem for Real-World DeFi

TechFlow Selected TechFlow Selected

Celo: A Stablecoin Ecosystem for Real-World DeFi

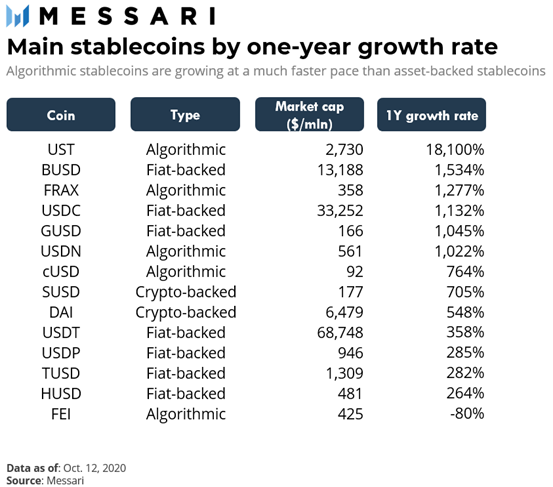

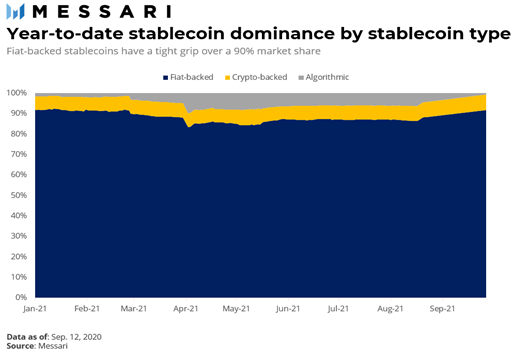

Stablecoins can be categorized into three types: fiat-backed, crypto-backed, and algorithm-backed. Among these, fiat-backed stablecoins are the most popular and show no signs of losing their dominant position. On the other hand, algorithmic stablecoins exhibit a much steeper growth curve.

Original: "Celo: a Stablecoin Ecosystem for the Real-World DeFi"

Author: Cristiano Ventricelli

Translated by: AlexZhang

Stablecoins are like snowflakes: they all look similar, but no two are exactly alike. Despite sharing the common goal of price stability, each achieves it through different mechanisms.

These differences in mechanism matter. The infamous algorithmic stablecoin project Iron Finance recently collapsed to nearly zero due to low-quality reserve assets and poorly designed stabilization mechanisms. Stablecoin design is more important than ever, and conducting proper due diligence on what lies behind a one-dollar token is becoming increasingly challenging.

The majority of stablecoin trading volume is tied to trading activity.

However, some projects like Celo primarily create stablecoins for peer-to-peer payments. Celo aims to make stablecoins a reliable alternative to cash, especially in emerging countries with limited banking access. In terms of stablecoin design, Celo’s stabilization mechanism relies on a combination of algorithmic methods and over-collateralized on-chain and cross-chain reserves.

We need to examine the key features of each type of stablecoin more closely to understand the differences between these mechanisms.

The Stablecoin Market

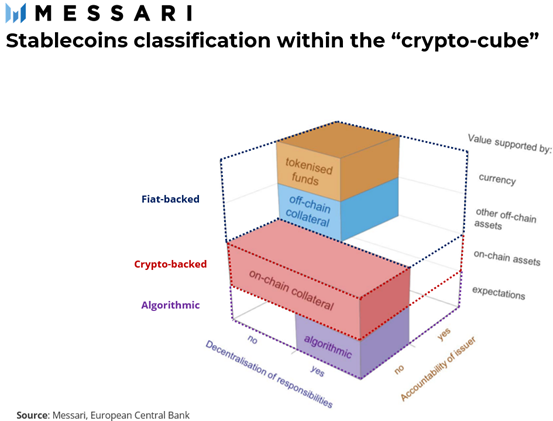

Stablecoins can be categorized into three types: fiat-backed, crypto-backed, and algorithmic.

Fiat-backed stablecoins are the most popular among the three categories, showing no signs of losing their dominance. On the other hand, algorithmic stablecoins have a much steeper growth curve.

The three types of stablecoins differ significantly in many aspects:

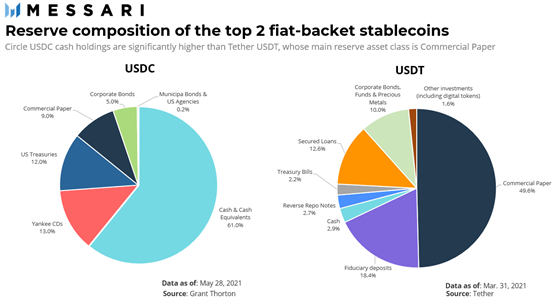

Fiat-backed stablecoins: The value of these tokens is pegged to a specific fiat currency. Most of these tokens come with a promise from the issuer that one fiat-backed stablecoin can be redeemed for one unit of fiat currency when needed. This requires the issuer to hold sufficient cash and cash equivalents on its balance sheet—something difficult (and impossible in real time) to verify, thus requiring trust. From a design perspective, fiat-backed stablecoins are relatively easy to understand. However, monitoring and managing the peg requires intervention by a centralized entity (e.g., the issuing company or protocol treasury), which adjusts reserve balances based on market demand for the token. Additionally, fiat-backed stablecoins require third-party audits to ensure they are fully backed by high-quality reserves at all times. The quality of non-cash reserves is determined by how easily they can be liquidated during market turmoil.

Crypto-backed stablecoins: These operate similarly to fiat-backed stablecoins, except that instead of using fiat-denominated assets as collateral, cryptocurrencies are locked up as collateral. Crypto-backed tokens typically rely on over-collateralization to offset the volatility of the underlying crypto assets. This means that each $1 token is usually backed by more than $1 worth of collateral. MakerDAO's stablecoin DAI is the largest crypto-backed stablecoin by market cap, with over $6.5 billion in circulation. Initially, DAI was minted using ETH as the sole collateral, but now it supports around 20 different types of collateral.

Due to their on-chain nature, crypto-backed stablecoins do not require custodians or external auditors, as reserve values can be publicly verified in real time. However, achieving price stability is more complex than with fiat-backed stablecoins, because the price volatility of the locked-up crypto collateral is wider and harder to predict.

Algorithmic stablecoins: Algorithmic stablecoins aim for higher capital efficiency compared to collateralized models. Instead of setting aside collateral, these protocols manage the peg by dynamically controlling the supply and demand of the stablecoin. The protocol acts as a “central bank,” increasing supply when demand rises and reducing it when demand weakens. Typically, adjustments in stablecoin supply and demand are facilitated through a second token, enabling arbitrage when the stablecoin’s price deviates from parity. Take Terra’s UST—the largest algorithmic stablecoin by market cap—as an example: the LUNA token can be exchanged directly within the protocol for an equivalent amount of UST. This allows arbitrageurs to buy (sell) $1 worth of LUNA when UST trades above (below) parity, exchange it for one UST, and then sell (buy) UST on the open market. These rules are embedded in smart contracts and can only be changed via social consensus or formal governance votes related to the governance/minting fee token.

The main advantages of algorithmic stablecoins are the lack of collateral requirements and transparency; when smart contracts are open-source, they are easy to audit. Compared to asset-backed stablecoins, the higher degree of decentralization comes at the cost of requiring market participants to trust that the protocol will maintain peg stability over time. Without collateral reserves, algorithmic stablecoins rely on the community as the lender of last resort. However, some projects have adopted hybrid designs that combine algorithmic stabilization mechanisms with collateralized reserves. This hybrid approach reduces reliance on market expectations for maintaining peg stability.

Peg Stability During Market Turmoil

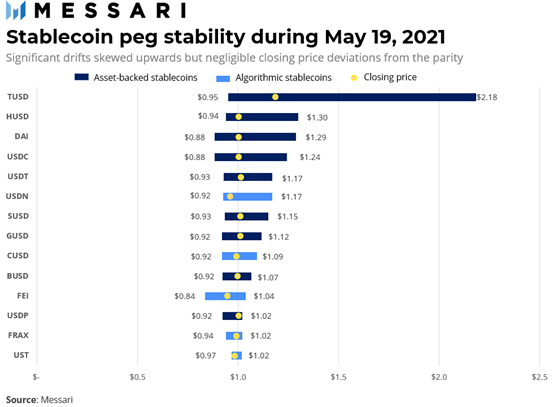

Stablecoin price fluctuations remain within a certain range during normal market conditions. When volatility spikes and prices fall sharply, many traders voluntarily close positions to limit losses, or loans are automatically liquidated by lending protocols when collateral falls below a threshold. In either case, funds rapidly shift from volatile assets into stablecoins. Deviations from the peg during market crashes serve as a strong stress test to evaluate whether the stabilization mechanism works under extreme conditions. For nearly all stablecoins, “peg” refers to a soft peg against a fiat anchor currency, meaning the stablecoin’s value may temporarily deviate from the anchor within a certain range. To measure peg deviation in distress scenarios, we collected daily high, low, and closing prices on May 19, 2021—a day when the cryptocurrency market lost $7 billion in market cap. We then calculated two metrics:

1. Difference between the daily high and low prices (high-low spread)

2. Deviation of the closing price from one dollar

These charts show that neither asset-backed nor algorithmic stablecoins are immune to fluctuations around parity. The former exhibit relatively wide price ranges, while the latter close slightly further from parity.

Celo: DeFi Without Banks Is a Mission

Celo is a platform designed to enable anyone to make global payments using cryptocurrencies via mobile phones. Given the ambitious scope of this goal, Celo relies on decentralized application (dApp) developers leveraging smart contract compatibility to build solutions on its foundation. Use cases of dApps built on Celo range from traditional remittances to contributing to universal basic income initiatives in extremely impoverished communities.

The primary pillars for Celo’s global adoption in financially excluded communities are stablecoins as a medium of exchange and mobile wallets as a payment method. To optimize for mobile use, Celo has adapted its proof-of-stake blockchain to streamline block header synchronization for mobile devices. Additionally, gas fees can be paid in multiple currencies, accommodating users who hold diverse assets.

Celo Stablecoins and Their Stabilization Mechanism

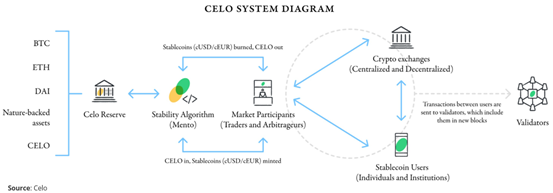

Celo’s stabilization mechanism relies on two distinct types of tokens. The first are elastic-supply stablecoins pegged to fiat currencies, such as the Celo Dollar (cUSD) and Celo Euro (cEUR). The second is CELO, a fixed-supply governance and utility token with a floating value. This dual-token system enables Celo stablecoins to maintain their peg to fiat currencies by adjusting the supply and demand dynamics of the CELO token.

To provide an additional safety buffer, Celo also uses a diversified basket of cryptocurrencies as reserves to support the peg. Thus, this stabilization mechanism can be defined as a hybrid crypto-collateralized/seigniorage-style model. The reserve currently stands at eight times the amount of outstanding stablecoins issued by Celo, with 76% composed of CELO tokens and the remainder consisting of BTC, ETH, other stablecoins (such as DAI), and nature-based assets (like tokenized cMCO2 carbon credits). By allocating part of the reserve to natural capital, the system creates incentives aligning stablecoin demand with environmental protection, effectively acting as a large-scale carbon sink.

Market participants help maintain the Celo Dollar (or cEUR) price at parity by profiting from deviations. This mechanism, called Mento, allows CELO token holders to exchange $1 worth of CELO for one Celo Dollar. When demand for the Celo Dollar rises and the market price exceeds the target, arbitrage profits can be made by exchanging $1 worth of CELO for one Celo Dollar and selling it at the higher market price.

Likewise, when demand drops and the market price falls below the target, users can buy Celo Dollars at the discounted market price, exchange them for $1 worth of CELO via the protocol, and then sell the CELO in the market. This allows market participants to keep the Celo Dollar price near $1 with minimal protocol intervention. Notably, the Mento mechanism includes a variant called Granda Mento, used when the protocol needs to exchange large amounts of CELO for Celo stable tokens without causing excessive slippage.

Coexistence of Multiple Stablecoins on the Celo Ecosystem

Platforms and projects aiming to deliver globally impactful products and services must be flexible enough to meet customer needs from all over the world. Dollar-pegged stablecoins may not be suitable for payments in countries using different fiat currencies. Therefore, Celo allows for the creation of multiple stablecoins. The euro-pegged stablecoin cEUR was launched in early 2021, and others could be added in the future to track currencies like the Japanese yen or Brazilian real.

Each stablecoin’s stability is independently managed through its own Mento mechanism. New stablecoins are introduced via governance processes to ensure platform sustainability. To prevent new assets from negatively impacting the stability of other tokens (e.g., if they are highly volatile), Celo uses a collateralized proof-of-stake model for voting on new introductions. Only when Celo holders believe a new stablecoin can grow sustainably without harming the ecosystem will they vote in favor.

Finally, it’s important to note that the reserve pools for each stablecoin do not need to be identical. Reserves can be tailored based on the specific characteristics of the stablecoin and its intended use case. For instance, in cases where a stablecoin is used locally for remittances, portions of local reserve currencies could be distributed to local residents, allowing them to benefit from adopting the local stablecoin—as a form of social dividend.

Mobile Wallets for a Global Audience

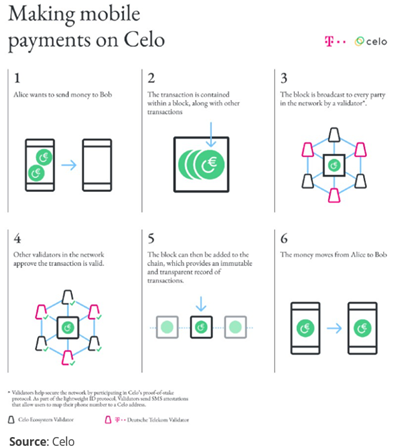

Wallets are essential tools for managing cryptocurrency payments. Most are certainly not as intuitive as smartphones and are not easily accessible to communities without personal computers. Celo aims to expand its user base and improve the user experience of crypto payments by introducing a phone-number-based identity system. This mechanism links phone numbers to Celo addresses, so when sending payments, the phone number serves as the wallet address. This approach does not compromise user privacy, as hashed phone numbers with pseudo-random peppers are stored on the blockchain without revealing actual numbers. Celo public addresses allow users to attach multiple phone numbers to a single address, change linked numbers, and/or revoke them at any time.

Mobile phones are not the only possible tool—any device capable of receiving secure messages can be used, such as IP addresses or bank routing and account numbers. Finally, linking phone numbers to Celo addresses enables reputation tracking (similar to credit scores). Celo adopts EigenTrust, a decentralized algorithm where a phone number’s score is defined by how many other trusted numbers trust it, weighted by their own reputation scores (similar to how PageRank works). While payments among small circles of known individuals pose little trust risk, aggregating trust signals becomes useful when transacting with people outside one’s immediate network.

Regulatory Stance Toward Stablecoins

Stablecoins represent fiat currencies on blockchains. It’s no surprise that financial and monetary regulators are intensifying efforts to understand the potential implications of stablecoin usage for consumer protection and financial stability. The U.S. Treasury recently met with several industry participants to discuss the risks and benefits posed by stablecoins. Two major concerns from regulators include:

"Bank run" scenario: If at any point a large number of customers simultaneously attempt to redeem their stablecoins for underlying fiat currency, the issuer may be unable to serve all clients if reserves are insufficient or illiquid.

Monetary policy effectiveness: There may be a significant disconnect between the return on one dollar in the real economy versus one dollar on the blockchain. In some cases, returns on these fiat-denominated instruments can even be negative. This divergence could lead savers to shift funds away from traditional financial institutions, thereby undermining the effectiveness of monetary policy. The risk became evident when Coinbase announced a Lend feature aimed at providing USDC depositors with a 4% annual yield. Coinbase’s chief legal officer wrote that the SEC threatened to sue the company if it launched such a product. According to Coinbase CEO Brian Armstrong, the SEC informed the company that the lending feature would be considered a security, meaning it would be regulated as an investment product.

What regulatory measures are most likely to address these two issues? A recent paper titled “Taming Wildcat Stablecoins,” published by two Federal Reserve economists, offers a framework for understanding what upcoming stablecoin regulations might entail:

Treating stablecoins as bank deposits: This would force stablecoin issuers to operate within licensed banks. Issuers could either become licensed banks themselves or partner with existing ones to conduct stablecoin activities (as reportedly planned by Facebook for its Diem stablecoin). If stablecoins are sold to retail customers, this would equate to accepting retail deposits, requiring FDIC insurance under current law.

Designating stablecoins as “systemically important payment instruments”: This would allow the Federal Reserve to impose stricter controls and closer oversight on risk management practices of stablecoin issuers. The authors suggest the Fed might require stablecoins to be issued by FDIC-insured banks or mandate that issuers hold one-to-one cash reserves at the Fed (i.e., converting stablecoins into public money).

Replacing stablecoins with public digital currencies in the form of Central Bank Digital Currencies (CBDCs): One of the main purposes of CBDCs is to protect the U.S. dollar from competition posed by private digital currencies.

Forcing full compliance with Federal Reserve regulations would effectively tie stablecoins to U.S. monetary regulation. Retaliation from other countries could be a potential workaround. China, Russia, and the European Union have all taken steps or expressed concerns about moving away from a dollar-dominated financial system. All three are actively regulating cryptocurrencies or developing their own digital currencies. If sovereign-backed stablecoins emerge, these nations may issue their own currency-backed stablecoins to broader crypto markets. CBDCs, privately issued, and public-private stablecoins denominated in various currencies could become countermeasures against U.S.-centric stablecoin regulation.

How Is Celo Prepared to Face Regulatory Challenges?

When assessing how harmful regulatory impacts on stablecoins might be, Celo’s advantageous features can be summarized as follows:

Low dependence on stablecoin reserves: Algorithmic stablecoins are theoretically less affected by regulatory cycles. For example, under the EU’s Markets in Crypto-Assets (MiCA) regulation, algorithmic stablecoins “shall not be considered asset-referenced tokens provided they do not aim to stabilize their value by reference to one or more other assets.” However, the hybrid nature of Celo’s stabilization mechanism may place its stablecoins in a gray area, making regulatory treatment more uncertain. On the other hand, auditing the smart contracts underlying Celo stablecoins is easier and cheaper than assessing the credit risk of reserves held by banks for other stablecoins.

Decentralized governance: Algorithmic stablecoins represent true decentralization, with no central authority to maintain or supervise the system—code manages supply and demand adjustments around the target price. Celo’s decentralized governance structure ensures there is no single accountable entity for regulators to target.

Stablecoin diversification: Exposure to multiple fiat currencies enables Celo to operate in countries with more lenient regulatory approaches toward stablecoins and cryptocurrencies, avoiding over-concentration within U.S. regulatory jurisdiction.

Low reliance on traditional DeFi use cases: Since Celo stablecoins are primarily used for payments, the impact of potential shutdowns of decentralized exchanges or lending platforms would be limited compared to asset-backed stablecoins.

The development of stablecoins can no longer ignore regulators and their attempts to limit their influence to preserve the status quo, nor exclude the possibility of a clear divide between highly centralized and highly decentralized stablecoins. While the latter undoubtedly possess immense innovative potential, they must build trust to gain traction and move beyond being perceived as disguised speculative assets.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News