Whales' Game: Curve Completes Initial Liquidity Mining, 20 Addresses Claim Nearly Half the Rewards

TechFlow Selected TechFlow Selected

Whales' Game: Curve Completes Initial Liquidity Mining, 20 Addresses Claim Nearly Half the Rewards

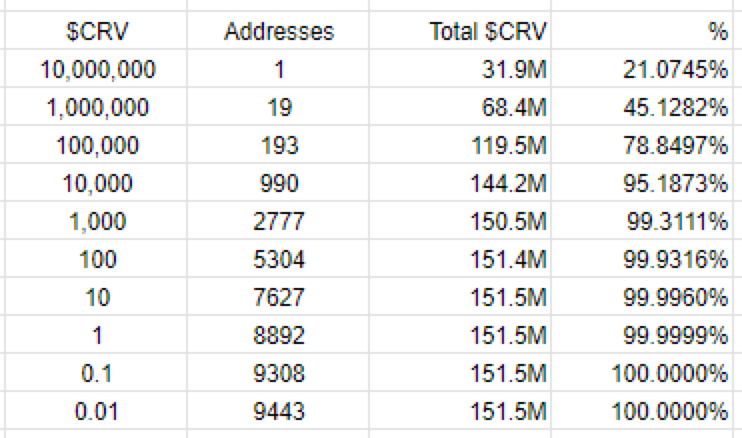

This event attracted over 9,000 addresses participating in the distribution of 151.5 million CRV tokens, with 20 whale addresses accounting for 45% of the rewards, leading some to jokingly call it a game for whales.

On August 10, the much-anticipated DeFi project Curve announced that its initial pre-launch mining event for its governance token has concluded. The event attracted over 9,000 addresses, which collectively claimed 151.5 million CRV tokens (5% of the total supply). Notably, 20 whale addresses received 45% of the rewards, prompting some to jokingly refer to it as "a game for whales."

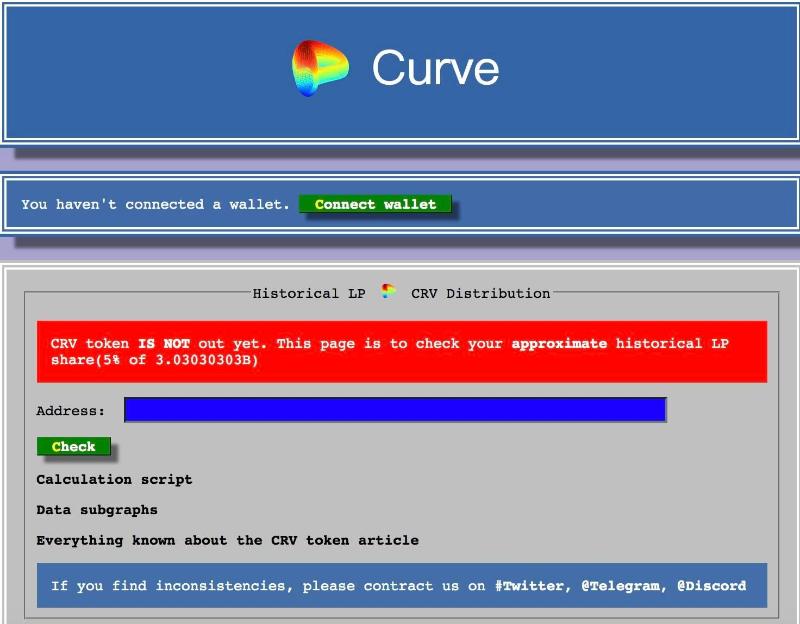

According to Curve's official statement, CRV has not yet officially launched; the current interface only displays earned rewards to participants.

By definition, Curve is a liquidity aggregation protocol—commonly understood as a decentralized exchange (DEX) specializing in stablecoin and Bitcoin-pegged asset swaps.

Since its launch in January 2020, Curve has rapidly become one of the leading players in Ethereum’s decentralized finance (DeFi) ecosystem. According to DefiPulse data, the protocol currently holds $246 million in value locked (TVL), ranking second among DEXs.

Like many other DeFi protocols, Curve was not fully decentralized at launch. It is managed by a team led by Michael Egorov, PhD in Physics and founder of NuCypher.

This means that despite being an innovative concept and well-designed system, the protocol remains susceptible to decisions made by a single entity.

To address this, Curve plans to introduce its governance token “CRV,” transforming the platform into a decentralized autonomous organization (DAO). Before diving deeper, let’s first understand how the Curve platform works.

What Is Curve?

As mentioned, Curve is a protocol designed to provide users with a platform to easily exchange certain Ethereum-based assets. As Michael Egorov, founder of Curve, explained in a recent interview:

“Curve is essentially an exchange built specifically for stablecoins and Bitcoin-pegged tokens on Ethereum.”

You might wonder: apart from focusing on dollar-pegged stablecoins (like USDT, USD Coin, and DAI) and Bitcoin-pegged tokens on Ethereum (such as renBTC and WBTC), what sets Curve apart from order-book-based DEXs?

The answer is complex but ultimately lies in how trading and liquidity provision operate.

Unlike traditional decentralized exchanges, Curve uses an automated market-making algorithm to enhance market liquidity, making it an Automated Market Maker (AMM) protocol.

Because its algorithm is optimized for stablecoins and Bitcoin-pegged assets, Curve offers significantly deeper liquidity than other DEXs. Founder Egorov stated in an interview:

“The key to Curve is its market-making algorithm, which provides 100 to 1,000 times greater market depth than Uniswap or Balancer, given the same amount of total value locked.”

This allows traders—even large ones—to easily swap one supported stablecoin for another with minimal fees and slippage.

According to Curve’s own statistics as of July 21, liquidity providers (LPs) in its Compound pool achieved an annualized yield of 5.51%. While this return may sound attractive—especially in a zero-interest-rate environment with depreciating fiat currencies—it's important to note that providing crypto liquidity carries inherent risks.

Risks of Providing Liquidity to Curve, Balancer, and Other AMM DEXs

The primary risk when using Curve and other AMM protocols is impermanent loss (IL).

Simply put, impermanent loss refers to the potential loss incurred by depositing cryptocurrencies into an automated market maker (e.g., Curve or Balancer) instead of holding them in a wallet. IL occurs when the prices of tokens within a liquidity pool diverge—for example, when Token A surges while Token B remains flat.

However, because Curve focuses on stablecoins and Bitcoin-pegged tokens—assets whose prices move in near-synchrony—the risk of impermanent loss is negligible. This makes Curve more favorable for liquidity provision compared to platforms like Uniswap.

Additionally, since these DEXs rely on smart contracts, participants also face risks related to potential contract vulnerabilities.

What Is CRV?

Now that we’ve covered Curve briefly, let’s explore what CRV actually is.

As previously noted, Curve was relatively centralized at launch. Although users could engage via Twitter, Reddit, or forums, the direction of this Ethereum protocol largely depended on the Curve team.

To resolve this centralization issue, Curve plans to launch the CRV governance token and establish a decentralized autonomous organization called CurveDAO.

Unlike the ICO model widely used in 2017, CRV will be distributed through liquidity mining (also known as yield farming). According to the initial plan, the maximum supply of CRV will reach 3.03 billion, with approximately 61% (1.85 billion) allocated to liquidity providers (LPs). In yesterday’s concluded initial liquidity mining event, 5% of CRV (151.5 million tokens) were distributed to LPs, with these tokens locked for one year.

Another 31% (about 939 million) will go to Curve’s investor institutions—identities not yet disclosed—with lock-up periods ranging from 2 to 4 years.

An additional 3% (around 90 million) will be allocated to Curve employees, subject to a 2-year vesting period.

Finally, 5% (approximately 150 million) will enter a burn reserve, where these backup tokens can only be accessed in emergency situations.

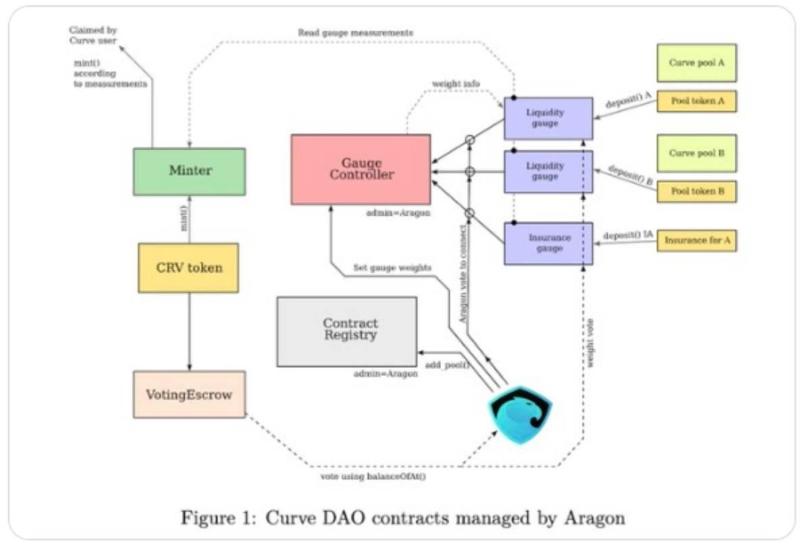

Moreover, CurveDAO is a DAO customized using Aragon, allowing CRV holders to influence the protocol’s development through “time-weighted voting.” This voting mechanism gives greater weight to long-term CRV holders, thereby mitigating the influence of newly wealthy large holders.

The Whales’ Mining Game

According to Charlie, a member of the Curve team, the initial liquidity mining event ended at Ethereum block height 10,627,59. The event drew approximately 9,400 participating addresses, which shared around 151.5 million CRV tokens.

One participant reported investing about $250,000 worth of stablecoins but receiving only around 1,000 CRV tokens in return.

Official data shows that one whale received 31.9 million CRV—21.07% of the total rewards—while 19 other whale addresses each received over 1 million CRV. The majority of addresses split the remaining small portion of CRV tokens.

These results clearly indicate whale dominance in Curve. Furthermore, according to data from qkl123.com, Curve had only 141 active users in the past 24 hours, yet processed over $12.6 million in trading volume—indicating that most users are whale-level participants.

Notably, Curve officials emphasized that CRV has not officially launched yet. The current page merely displays reward balances to participants. Some users have also reported the appearance of counterfeit CRV tokens online.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News