Storage is still rising, but smart money is beginning to position itself on this “flash memory chain.”

TechFlow Selected TechFlow Selected

Storage is still rising, but smart money is beginning to position itself on this “flash memory chain.”

AI Is Paying “Taxes” on Memory—And the Companies Helping It Save Money Are Profiting: A Full-Chain Dissection of Flash Memory Substitution

By David, TideFlow Research

TideFlow Summary: SanDisk surged nearly 40-fold in 16 months after its IPO; Longsys’ Q1 2026 net profit jumped 26-fold year-on-year… Memory is the hottest sector in 2026—no contest. Yet since June, three tech giants—AMD, NVIDIA, and SanDisk—have quietly taken the same action almost simultaneously:

Reducing reliance on expensive DRAM memory and shifting workloads to cheaper NAND flash. This “flash substitution” undercurrent has already lifted leading stocks—but the truly undervalued opportunities may lie upstream and downstream of this trend.

Understanding AI’s “Memory Tax” Constraint

How explosive has this memory cycle been so far? A few numbers tell the story.

SanDisk (SNDK) spun off from Western Digital and went public in February 2025 at ~$38 per share; by mid-June 2026, its price had reached ~$2,000—a near 40-fold surge in just 16 months—and its P/E ratio stood at ~69x. Micron’s performance is even more staggering.

In China’s A-share market, Longsys posted Q1 2026 net profit of RMB 3.862 billion, up 2,644% YoY; GigaDevice reported Q1 net profit growth of 522%, hitting an all-time high with a trading halt on June 17. The market consensus before this rally boiled down to one sentence:

“AI desperately needs memory—shortages will persist through 2028. Buy memory stocks blindly—they’ll rise.”

Yet while investors celebrated “shortages,” several of the industry’s most influential players have quietly planted landmines beneath that narrative.

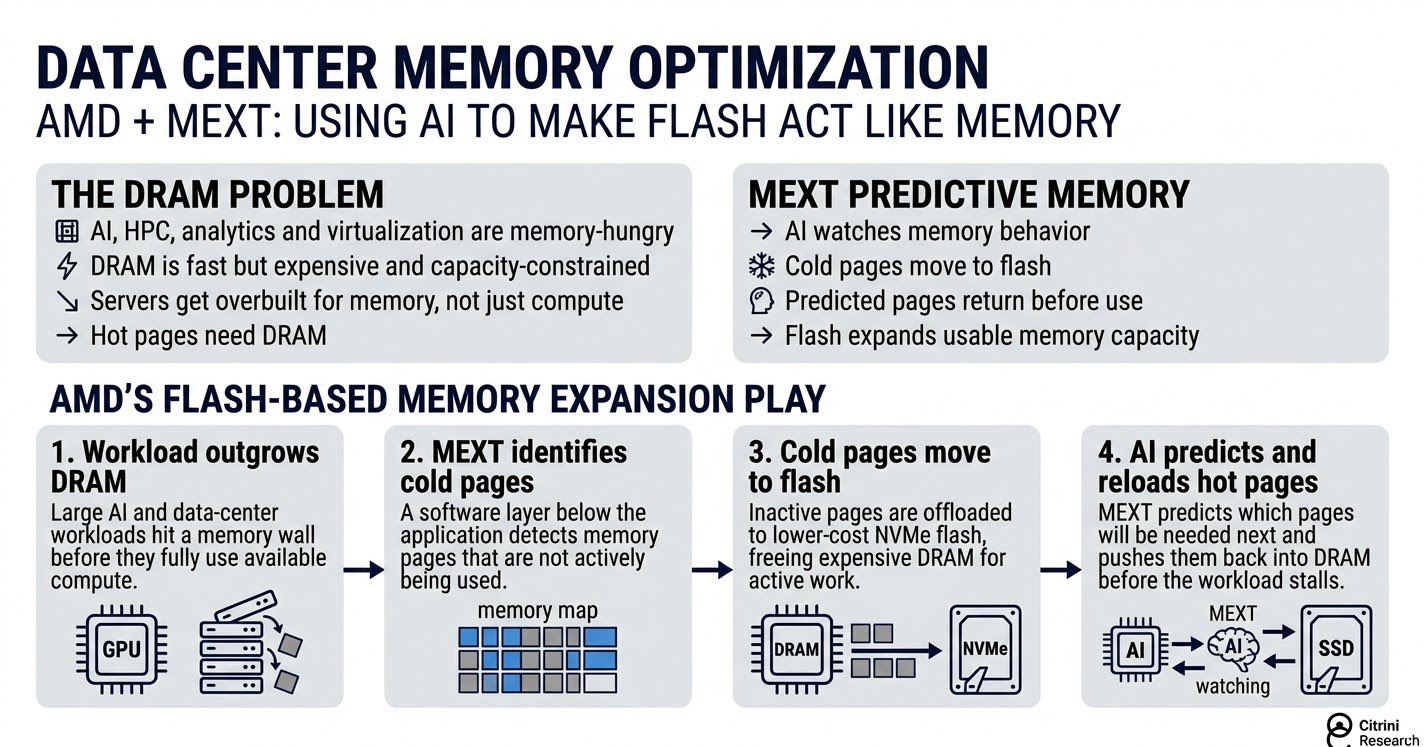

On June 15, AMD announced its acquisition of MEXT, a company whose core technology uses AI to “masquerade” NAND flash as DRAM;

Earlier, NVIDIA unveiled CMX at CES and GTC in early 2026, moving the most memory-intensive portions of AI runtime data to the NAND layer; and prior to that, SanDisk and SK hynix jointly launched HBF—a new standard in February—to embed NAND flash into packages previously reserved for high-end memory (HBM).

Viewed collectively, these three moves point in one unified direction:

Adding a new “memory tier” for AI—one faster than storage but cheaper than DRAM—to reduce spending on costly DRAM. Citrini Research, a U.S.-based thematic investment research firm, has dubbed this phenomenon “The AI Tax.”

To grasp this term—and identify investable themes—you must first distinguish between AI’s two types of “memory.”

One is DRAM—the mainstream memory, and its highest-performance variant HBM (High Bandwidth Memory), designed specifically for GPU integration. It’s fast: GPUs can fetch data instantly. But it’s extremely expensive and capacity-constrained.

The other is NAND flash—the technology behind your SSD. It’s cheap and high-capacity, but slow. A rough but serviceable analogy: DRAM is like documents laid out on your desk—immediately accessible; NAND is like goods stored in a warehouse downstairs—cheap and abundant, but slower to retrieve.

AI’s rapid evolution over the past two years has revealed a clear problem: the “desk” is overflowing—and prohibitively expensive.

TrendForce data shows DRAM contract prices rose over 90% QoQ in Q1 2026; Citigroup forecasts full-year 2026 average DRAM prices up 88% and NAND up 74%. The root cause is AI:

NVIDIA GPUs require massive data feeds, and HBM—fast yet costly—is consuming an ever-larger share of DRAM wafer output.

Citrini cites data showing HBM’s share of total DRAM wafer production climbed from 2% in 2020 to ~21% in 2025 and is projected to reach 25% in 2026… meaning one-quarter of global DRAM capacity is now dedicated to HBM, leaving less—and thus pricier—capacity for everyone else.

This is the origin of the “Memory Tax.”

To run AI efficiently, companies are forced to pay an increasingly steep “tax” on scarce, expensive memory. When the tax becomes too heavy, someone inevitably seeks to avoid it. And the sole viable path is to shift part of the workload originally assigned to DRAM onto cheaper NAND flash.

The three initiatives cited earlier—by AMD, NVIDIA, and SanDisk—are distinct technical approaches to “tax avoidance.” Yet their effect is identical: adding a new “memory tier”—cheaper than DRAM, faster than HDD—for AI.

The investment implication lies precisely in this “shift.” Every workload moved to NAND translates directly into additional demand across the NAND value chain. Memory leaders have already rallied on the “shortage-driven pricing” thesis. “NAND substitution for DRAM” represents a second, additive layer of logic stacked atop that pricing theme.

It doesn’t necessarily point to already sky-high leaders—but rather to segments along the chain not yet priced for this second-order logic. That’s where deeper digging pays off.

Dissecting the NAND Value Chain: Foundries Feast, Controllers Sell Picks

The NAND business—from wafer to end-user SSD—roughly comprises three tiers, with profitability and concentration increasing upstream.

- Upstream: NAND Foundries—those who fabricate wafers themselves:

Samsung, SK hynix (now including Kioxia), Micron, and SanDisk (spun off from Western Digital). They control capacity and reap the largest gains during price-up cycles.

- Middle-tier: Module Manufacturers—who buy NAND die from foundries, package them into SSDs or memory modules, and sell to end users:

They don’t fabricate wafers; instead, they earn margins on assembly and branding. Their earnings leverage can even exceed that of foundries—because when die prices surge, their existing low-cost inventory instantly appreciates.

A-share players include Longsys, Biwin Storage, and Demingli. Longsys posted Q1 2026 net profit of RMB 3.862 billion (+2,644% YoY); Biwin recorded +1,567% growth in the same period.

But leverage cuts both ways: if die prices fall, inventory devaluation hits module makers first—making them the most vulnerable in downturns.

- The often-overlooked third tier: Controller ICs:

Every SSD contains not only NAND die but also a “brain”—the controller chip—that manages data flow in and out. While controllers don’t benefit directly from die price hikes, their demand rises in lockstep with SSD shipment volumes.

Theoretically, this tier is closest to the classic “pick-and-shovel” position in the value chain. The global top two independent SSD controller vendors are Phison (8299.TW) and Silicon Motion (SIMO), both headquartered in Taiwan; A-share player Linkage Technology (688449) ranks third globally.

Currently, among these three tiers, foundries and module makers have been fully priced for the “price-increase” thesis—their valuations reflect current shortage-driven inflation.

“NAND substitution for DRAM” is a second-layer thesis layered atop price increases—it benefits not just pricing, but long-term expansion of SSD/NAND shipment volumes.

This logic most directly benefits volume-driven, non-price-inflationary segments—such as controllers—and the newly created incremental demand spurred by HBF, discussed in the next section.

Truly Undervalued Opportunities: Controller “Valuation Gaps” and HBF’s “New Cake”

Volume-driven segments not yet lifted by the price-inflation rally. Two areas stand out.

First, the valuation gap in controllers.

Linkage Technology (688449) serves as a case study. It ranks third globally among independent SSD controller vendors—behind Taiwan’s Silicon Motion and Phison—and is one of the few Chinese firms capable of mass-producing PCIe 5.0 controllers.

Yet as of April 2026, its market cap remains below its IPO debut level—its stock significantly lagging peers like Longsys and Demingli… likely for a simple reason:

Controllers don’t directly capture die price inflation. During the past six months of surging NAND die prices, capital rushed into the most leveraged module makers—leaving controllers sidelined.

But this highlights precisely the divergence between the “price-increase” and “volume-driven” logics. Price hikes benefit foundries and module makers holding low-cost inventory—controllers gain nothing. Yet NAND-for-DRAM substitution drives long-term expansion in SSD shipment volumes: each additional SSD sold requires one more controller.

If this logic holds, beneficiaries are volume—not price—and controllers represent a purer play.

Three names stand out in this tier:

Silicon Motion (SIMO) (U.S. ADR): Global leader in independent controllers, commanding >30% market share in consumer SSD controllers.

Phison (8299.TW) (Taiwan Stock Exchange): World’s #2 independent controller vendor; supplies custom controllers for Kioxia.

Linkage Technology (688449) (A-share): Global #3 independent controller vendor, China’s most advanced domestic player—and the one with the widest valuation gap.

That said, risks remain clear. Controllers aren’t highly monopolized; numerous domestic entrants compete fiercely, and price wars persist. Public data shows Linkage’s R&D expense ratio runs consistently at 36–38%, continuously pressuring margins—its #3 global share does not equate to high profitability.

Second, the “new cake” created by HBF.

First, what is HBF?

HBM is fast, expensive, and consumes ~25% of DRAM capacity—so SanDisk and SK hynix devised a solution: stacking NAND flash to create an HBM-like interface layer offering 8–16x higher capacity and a fraction of the cost—this is HBF (High Bandwidth Flash).

HBF doesn’t replace HBM. Instead, it functions as a “high-capacity warehouse” adjacent to HBM—specifically storing AI inference data that’s “too large for HBM, yet too valuable to discard into cold storage.”

HBF manufacturing relies on TSV (Through-Silicon Via)—vertical interconnects formed by drilling holes in silicon wafers—followed by multi-layer NAND stacking and bonding. This process shares technological roots with HBM packaging and therefore drives demand for advanced packaging, OSAT (outsourced semiconductor assembly and test), and specialized materials. Relevant listed names include:

JCET Group (600584) and TFME (002156) (A-share): China’s top two OSAT providers—TSV-based stacking and bonding fall squarely within their capabilities.

Huahai Chengke (688535) (A-share): China’s sole producer of GMC—the core material used in HBM packaging—and possesses process extension capability applicable to HBF.

However, this segment remains largely unproven. Several key points warrant attention:

First, HBF is not yet in mass production. SanDisk’s timeline targets samples in H2 2026 and initial equipment shipments in early 2027—meaning all current “benefit” narratives are purely forward-looking, with zero revenue impact on financial statements.

Second, the addressable market is smaller than imagined. Per SK hynix’s cited projections, the HBF market will reach ~$12 billion by 2030—versus ~$117 billion for HBM. HBF is a complementary layer—not a disruptive replacement.

Third, A-share markets have already spawned numerous “HBF concept lists”—including Yishitong, Feikai Materials, Chipsource Micro, and Quick Intelligent—frequently cited without substantiation. Most lack actual HBF-related orders or verified process validation, making them classic “concept-chasing” plays.

These differ fundamentally from JCET and Huahai Chengke—whose technologies demonstrably align with HBF process requirements. They must be evaluated separately.

Thus, these two opportunities represent near-term and long-term narratives under the same investment theme.

Controllers represent a “currently shipping, yet undervalued under substitution logic”洼地—with tangible execution; HBF’s incremental demand is a “compelling story awaiting 2027+ realization”—a distant option with high conceptual noise.

One Chart to Map the Entire Market: Where Are the Names—and Are They Priced Fairly?

Consolidating the previously dissected segments into a single map.

Geographically, this chain concentrates across four markets: NAND foundries in the U.S., Japan, and Korea; controllers traded as U.S. ADRs and on Taiwan’s exchange; modules, OSAT, and materials almost exclusively in China’s A-share market. No pure-play NAND stocks exist on Hong Kong Exchanges—so we exclude them here.

When reading this chart, remember one coordinate:

The further upstream (foundries), the higher the monopoly power and upside—but also the most fully priced and expensive valuations. Moving downstream (modules, controllers, OSAT, materials), risk-return profiles vary: some remain unpriced for the “substitution logic.”

Risks & Uncertainties: Near-Term Tailwind vs. Long-Term Sword Hanging Over DRAM

The most common misreading of the “flash substitution” thesis conflates short- and long-term dynamics—which actually point in opposite directions.

In the short term (2026–2027), large-scale substitution hasn’t yet materialized, and the memory supercycle remains intact. NAND contract prices rose over 70% QoQ in Q2, and foundry/module maker earnings continue to explode.

During this phase, the “Memory Tax” acts as a pure tailwind for the NAND chain: the more AI strains DRAM supply, the greater the incentive to shift workloads to NAND—and the stronger the demand pull on NAND.

The immediate risk isn’t the logic—it’s positioning. Leading stocks already price in aggressive optimism: SanDisk trades at 69x P/E; A-share module stocks have doubled; on June 17, Micron, AMD, and SanDisk all corrected 6–7%—a natural reaction by high-positioned capital to “overheated, overextended” valuations.

Chasing these highs bets on sentiment sustainability.

In the medium-to-long term (2027 onward), real uncertainties emerge. If HBF enters mass production and solutions like NVIDIA’s CMX and AMD’s MEXT prove effective, “NAND replacing part of DRAM’s workload” shifts from whitepaper to reality.

At that point, the narrative of “DRAM perpetually scarce, premium pricing eternal” collapses—becoming a sword hanging over pure DRAM bulls.

Note: This sword strikes DRAM’s scarcity premium—not NAND’s fundamentals. In fact, demand diversion could benefit the NAND chain. So the same development poses risk to DRAM bulls but opportunity for NAND players.

To translate vague long-term variables into trackable signals, we recommend monitoring three metrics:

- HBF Sample Progression (H2 2026): Yield rates and cost structure of initial samples will determine whether this technology path is commercially viable—or another overpromised concept.

- NVIDIA CMX Shipment Volume (starting H2 2026): Will cloud providers pay for a “flash memory layer”? CMX shipment volumes provide the clearest vote.

- Samsung/SK hynix NAND Contract Price Inflection: A shift from rising to flat—or falling—contract prices would be the earliest signal of loosening supply-demand fundamentals and the supercycle’s retreat.

Until these signals appear, near-term strength persists; once they do, the narrative must pivot from “pricing tailwind” to “substitution validating DRAM’s eroding scarcity.”

TideFlow View:

Near-term fundamentals remain robust—but valuations have already paid for optimistic expectations. Chasing memory leaders is essentially betting on sentiment continuity. A better asymmetric opportunity lies in volume-driven, substitution-logic-undervalued segments—like controllers (Silicon Motion, Phison, Linkage Technology)—rather than foundries trading at 40x multiples.

HBF’s incremental demand is directionally attractive—but remains a long-dated option pre-2027, rife with concept-chasing noise. It merits tracking—not heavy allocation today.

In one sentence: We endorse the long-term logic of this value chain—but the current best risk-adjusted value lies elsewhere—not with the hottest leaders.

Note: This article compiles publicly available information and presents analytical views. All referenced stocks, ratings, and target prices derive from open sources and reflect time-sensitive data. This does not constitute investment advice. Markets carry risk; decisions are solely the reader’s responsibility.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News