Bitget UEX Daily Report | Trump Advances U.S.-Iran Agreement Signing; U.S. Semiconductor Stocks Lead Gains on Wall Street; SpaceX Goes Public Today

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Trump Advances U.S.-Iran Agreement Signing; U.S. Semiconductor Stocks Lead Gains on Wall Street; SpaceX Goes Public Today

Institutional consensus emphasizes attention to protocol implementation details, inflation data, and Fed signals, advising investors to seek structural opportunities amid volatility and avoid excessive leverage.

I. Top News Highlights

Federal Reserve Updates

No new Fed actions announced; markets monitor geopolitical developments’ impact on monetary policy

- The Federal Reserve has not issued any major policy statements recently, but markets continue closely tracking inflation and employment data.

- Trump announced cancellation of U.S. military strikes against Iran and stated that a U.S.-Iran agreement could be signed this weekend—potentially in Europe.

- Analysis: Easing geopolitical risks may reduce safe-haven demand, offering short-term support to risk assets. However, if agreement details fall short of expectations, volatility in the U.S. dollar and oil prices could increase uncertainty around Fed decision-making.

International Commodities

CME plans 24/7 trading for oil and gold; geopolitical easing weighs on oil prices

- CME plans to launch round-the-clock trading for smaller-sized crude oil and gold futures contracts. The new crude contract size will be one-tenth that of the existing Micro WTI contract; the 1-ounce gold contract will launch in July.

- Spot gold briefly recovered prior highs, buoyed by progress on the agreement.

- Analysis: 24/7 trading enhances liquidity and enables real-time management of geopolitical risk exposure. Reduced uncertainty related to the Strait of Hormuz is exerting near-term downward pressure on oil prices, though long-term supply-demand fundamentals remain key watchpoints.

Market Dynamics

Strong demand for advanced process nodes prompts TSMC to consider price hikes

- TSMC’s 3nm capacity has increased but remains insufficient to meet explosive AI chip demand. Price increases of up to 15% for its most constrained advanced nodes are possible in H2.

- Google’s TPU reportedly introduced Samsung as a foundry partner for the first time, alleviating some capacity pressure on TSMC.

- Analysis: AI-driven chip demand remains robust, prompting supply-chain adjustments that benefit equipment and materials suppliers—but also highlights potential bottlenecks constraining industry growth.

II. Market Recap

Commodities & FX Performance (Real-Time Update)

- Spot Gold: ~$4,200/oz, -0.23%.

- Spot Silver: ~$67/oz, -0.06%.

- WTI Crude: ~$86/bbl, -1.43%.

- Brent Crude: ~$89/bbl, -1.45%.

- U.S. Dollar Index (DXY): ~99.7, -0.1%.

Key Drivers: Progress on the U.S.-Iran agreement significantly eased geopolitical tensions. Trump confirmed all parties had approved the text and canceled planned military action—directly stabilizing safe-haven assets like gold in the near term while pressuring crude oil prices (both WTI and Brent declined). The slight DXY dip reflects improving risk sentiment. Institutional views hold that although near-term supply-demand dynamics have eased, long-term geopolitical uncertainty and global demand continue to underpin commodities; CME’s 24/7 trading initiative will further bolster market resilience. Overall, inter-asset correlations suggest risk assets gained, while precious metals retained appeal at elevated levels.

Cryptocurrency Performance

- BTC: ~$63,670, +2.88%.

- ETH: ~$1,670, +2.74%.

- Total Crypto Market Cap: ~$2.26 trillion, +2.5%.

- 24h Liquidations: $270 million total, with $197 million on shorts.

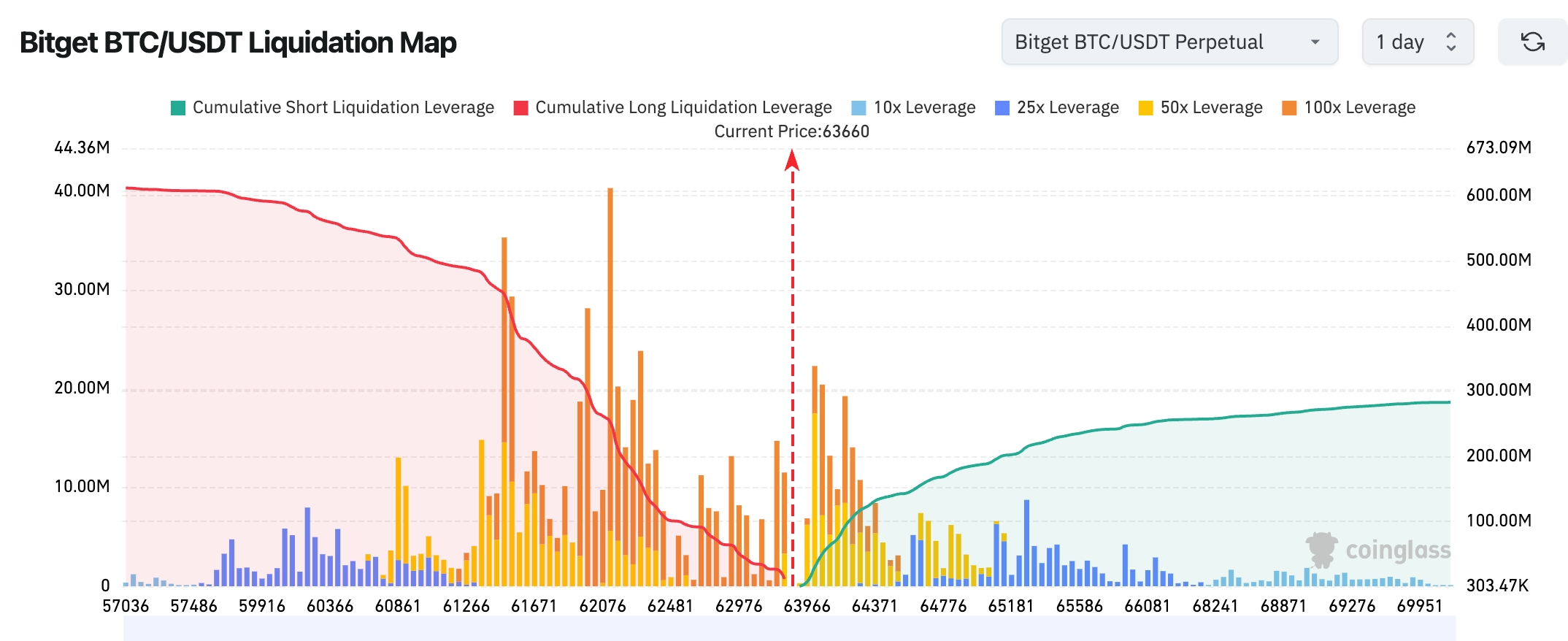

- Bitget BTC/USDT Liquidation Map: BTC has broken above the dense short zone above $63,000; a significant short liquidation band remains between $64,000–$64,500. Further upside could trigger renewed short squeezes. The large long liquidation zone between $61,500–$62,500 has been largely cleared, resulting in healthier near-term positioning. Market focus now centers on whether BTC can sustain above $64,000 and test $65,000.

- Spot ETF Net Inflows/Outflows: BTC spot ETFs saw $214 million net outflow yesterday.

Key Drivers: Easing geopolitical risk combined with a rebound in U.S. tech stocks provided macro-level support for crypto markets, driving synchronized gains in BTC and ETH. ETF flows showed modest volatility; leverage-related liquidations remained manageable; technicals are consolidating within key ranges. SpaceX’s upcoming IPO and strong semiconductor performance indirectly boosted sentiment. Consensus among institutions holds that improving macro conditions and institutional interest will support medium-term trends—but final implementation of the geopolitical agreement warrants close monitoring for its effect on risk appetite.

U.S. Equity Index Performance

- Dow Jones: Closed at ~50,848.75 (+1.86%), continuing its rally.

- S&P 500: Closed at ~7,394.30 (+1.75%), nearing all-time highs.

- Nasdaq: Closed at ~25,809.66 (+2.54%), driven notably by technology and semiconductors.

Tech Giants’ Updates

- NVDA: $204.87 (+2.22%).

- AAPL: $295.63 (+1.39%).

- MSFT: $390.34 (-1.77%).

- GOOGL: $357.77 (+0.39%).

- AMZN: $241.51 (+1.47%).

- META: $568.43 (-0.45%).

- TSLA: $399.15 (+4.60%).

Summary & Key Drivers: The broader tech sector rallied, with semiconductor indices surging strongly; memory and aerospace services concepts also performed well. Stock performance diverged markedly: Intel and Micron surged amid tight capacity and strong AI demand, while Oracle faced pressure due to unexpectedly high capex. SpaceX’s impending IPO lifted space-related stocks; Google’s use of Samsung foundry capacity signals a broader supply-chain diversification strategy. Geopolitical easing drove capital rotation from defensive to growth-oriented assets—though valuation concerns and company-specific events produced differentiated results. AI remains the dominant thematic driver in the near term.

Crypto Derivatives Trading Data

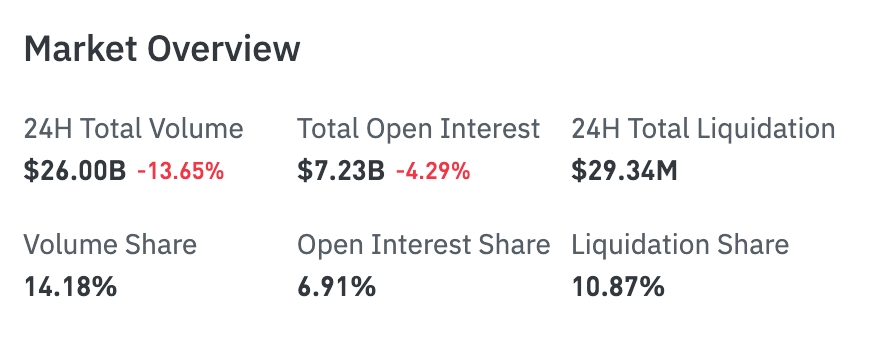

- 24H Total Turnover: $26 billion (-13.65%)

- Open Interest (OI): $7.23 billion (-4.29%)

- 24H Total Liquidations: $29.34 million

- Turnover Share: 14.18%

- OI Share: 6.91%

- Liquidation Share: 10.87%

Market Interpretation:

Both turnover and open interest declined in the stock derivatives market, indicating a cooling of short-term risk appetite. However, liquidation volume remained relatively contained, suggesting active de-risking rather than panic-driven exits.

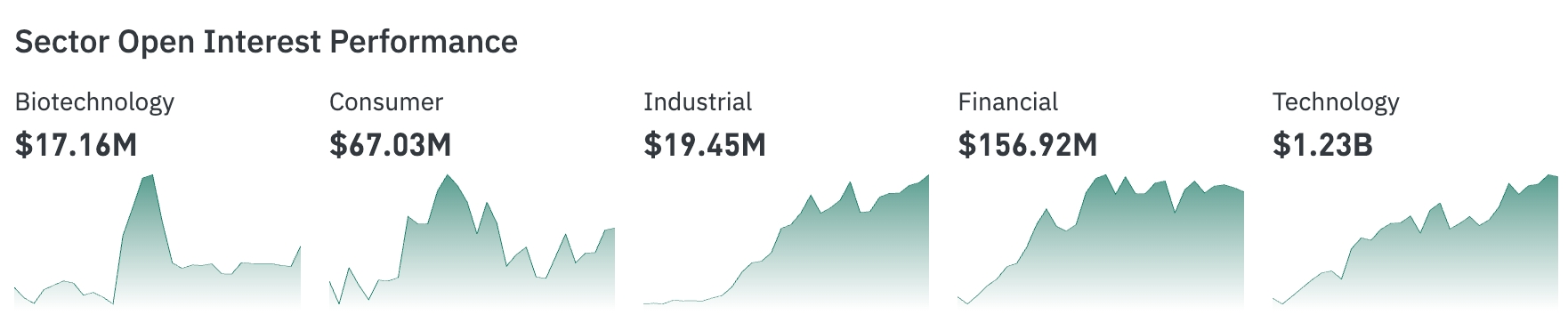

Sector Positioning

- Technology: $1.23 billion (clear leader)

- Financials: $157 million

- Consumer Discretionary: $67.03 million

- Industrials: $19.45 million

- Biotech: $17.16 million

Market Interpretation:

The technology sector continues to dominate positioning, with funds concentrated on AI, semiconductors, and mega-cap tech names. Financials remain solidly in second place, reflecting ongoing investor attention to interest rate and macro-policy expectations.

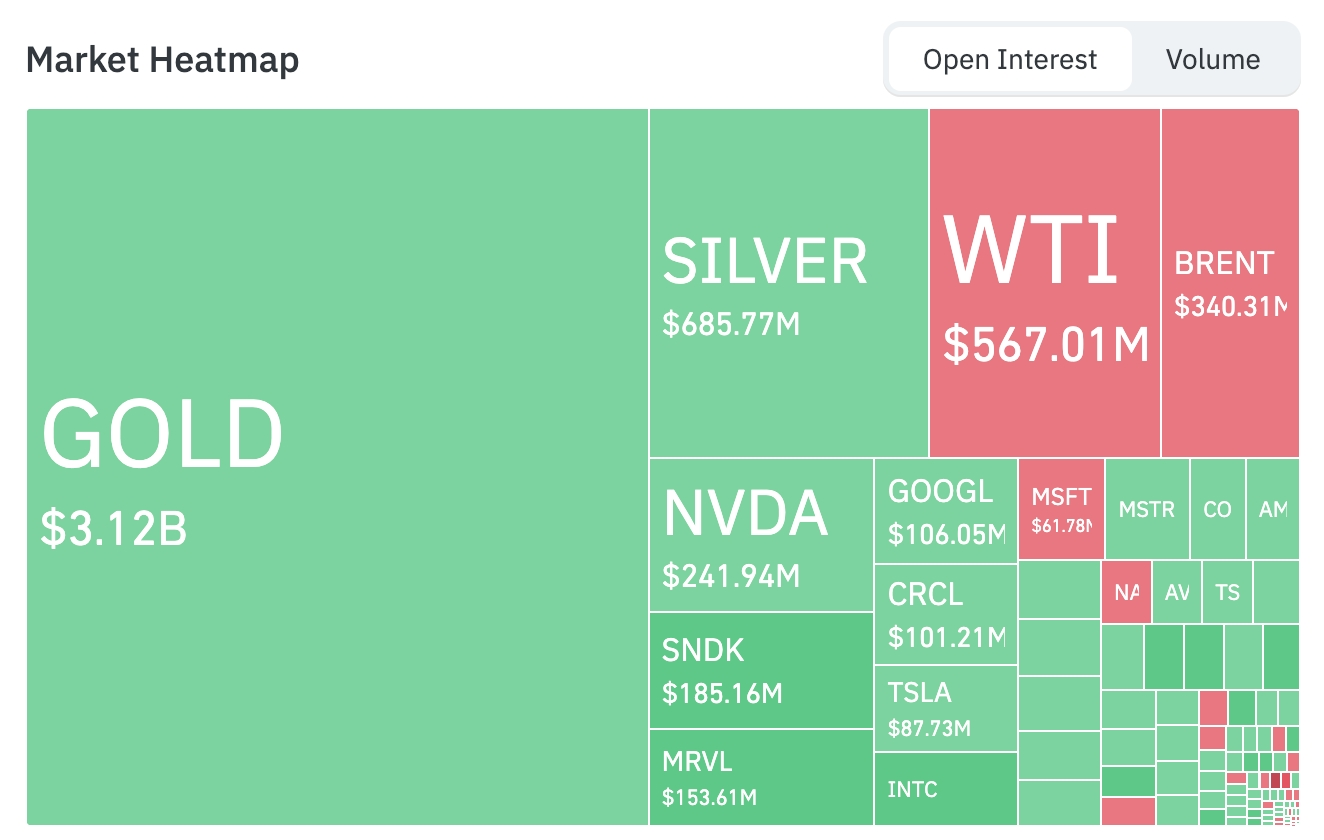

Heatmap Fund Flows (by Open Interest)

Commodities

- Gold (GOLD): $3.12 billion (largest position)

- Silver (SILVER): $686 million

- WTI Crude: $567 million

- Brent Crude (BRENT): $340 million

Tech Stocks

- NVIDIA (NVDA): $242 million

- SanDisk (SNDK): $185 million

- Marvell Technology (MRVL): $154 million

- Google (GOOGL): $106 million

- Circle (CRCL): $101 million

- Tesla (TSLA): $87.73 million

- Intel (INTC): Active positioning

Market Interpretation: Safe-haven funds remain heavily concentrated in gold and silver—gold positions exceed $3.1 billion, far surpassing other assets. Among tech stocks, NVIDIA, SanDisk, and Marvell—key AI infrastructure and compute enablers—continue drawing sustained inflows, reflecting ongoing bets on AI-driven infrastructure and computing demand growth.

Sector Momentum Watch

Semiconductor Sector up >7%

- Key stocks: Micron up nearly 12%, Intel up >9%.

- Drivers: Tight advanced-node supply and robust AI demand.

Memory Concept rallies strongly

- Key stock: SanDisk up >14%.

- Driver: Anticipated NAND technology refresh cycles.

Space Sector surges

- Key stock: Virgin Galactic up nearly 22%.

- Driver: Proximity of SpaceX IPO lifting sector sentiment.

III. Deep Dive: U.S. Equities

1. TSMC (TSM) – Advanced Node Pricing Outlook: TSMC’s monthly 3nm output has risen to 175,000 wafers, yet still falls short of explosive AI chip demand. Supply-chain sources indicate potential price hikes of up to 15% for its most constrained advanced nodes in H2, aimed at offsetting upstream cost pressures. Google’s TPU reportedly began using Samsung’s 2nm foundry for select components—the first such move—signaling deeper supply-chain diversification to reduce overreliance on TSMC, even as Google’s core compute engines remain fabricated on TSMC’s 1.4nm node. Market View: Institutions broadly recognize TSMC’s pricing power and technological moat in advanced nodes—but caution investors to monitor capacity expansion pace, intensifying global competition, and potential geopolitical shocks to the supply chain. Investment Insight: Near-term capacity constraints may support valuation premiums; longer-term sustainability hinges on tracking AI capex cycles and multi-foundry strategies to assess growth durability.

2. Intel (INTC) – BofA Upgrades Rating: Intel shares rose >9% after Bank of America Securities upgraded its rating from “Underperform” to “Buy”, with a $135 target price. Analysts highlighted strong prospects for Intel’s server chips and underestimated potential in its external foundry business, forecasting EPS exceeding $6 by 2030—significantly higher than prior estimates. This upgrade signals renewed confidence in Intel’s long-term competitiveness across AI infrastructure and chip manufacturing. Market View: Multiple institutions view this as the onset of Intel’s valuation recovery cycle—though execution risk and cyclical industry volatility remain key concerns. Investment Insight: Offers an attractive entry point for valuation recovery; investors should prioritize monitoring execution on technology deployment and signals marking a semiconductor cycle inflection.

3. Oracle (ORCL) – Capex Concerns: Oracle shares fell >8% as quarterly capex exceeded consensus expectations, deepening investor concerns about the sustainability of profitability in its AI infrastructure business. With ~$117 billion in debt, Oracle ranks as the largest bond issuer outside financial services. While heavy investment supports cloud and AI ambitions, short-term profit pressure is pronounced. Market View: Analysts focus on return-on-capital and debt management, identifying path-to-profitability as the critical metric; several institutions maintain neutral-to-cautious stances. Investment Insight: Short-term focus should center on cost discipline and cash flow generation; long-term AI cloud positioning retains strategic value—suitable for investors with moderate risk tolerance.

4. SpaceX Developments – IPO Imminence: SpaceX aims to raise $75 billion via IPO, having already attracted over $70 billion in retail orders—including at least $5 billion from BlackRock. The IPO is entering its final stage, with retail investors expected to receive ≥20% of shares. Ark Investment analyst Brett Winton projects its orbital data center business alone could generate $300 billion in annual revenue by decade-end—complemented by Starlink and rocket technologies for a multi-engine growth narrative. Market View: Institutions remain optimistic on the long-term space economy; as industry leader, SpaceX’s IPO pricing and post-listing performance will serve as a critical barometer for the sector. Investment Insight: Monitor final IPO pricing and post-listing liquidity; related space equities may continue benefiting from catalysts—but assess valuation bubble risks carefully.

IV. Cryptocurrency Project Updates

1. Asset manager Fidelity Investments selected Uniswap as the liquidity infrastructure for its stablecoin FIDD; the FIDD liquidity pool has gone live on Uniswap.

2. Bloomberg ETF analyst Eric Balchunas posted on X that BlackRock filed Form 8-A for its Bitcoin premium yield ETF BITA. This step typically precedes formal launch within one week; he expects the product to begin trading next Thursday.

3. Galaxy Digital Head of Research Alex Thorn posted on X that the U.S. Securities and Exchange Commission (SEC) has proposed eliminating Rule 611 (the Order Protection Rule) and Rule 610(e) (the Lock-up/Cross-Market Restriction) of Regulation NMS. Thorn noted Rule 611 is one of the biggest barriers to tokenized stock trading in DeFi: automated market makers cannot comply, and any tokenized stock liquidity pool would continuously violate it—effectively operating as an illegal exchange. Replacing Rule 611 with a “best execution” standard applicable at the broker level creates a principles-based framework compatible with AMMs.

4. J.P. Morgan analyst Nikolaos Panigirtzoglou stated that the “fiat depreciation hedge trade”—investors buying Bitcoin and gold amid geopolitical uncertainty, inflation, rising government debt, and USD diversification—is fading. Gold ETFs saw ~$20 billion outflows in the week ending June 5; Bitcoin ETF outflows have gradually increased over the past four weeks.

The depreciation hedge trade has been receding across ETFs, futures markets, and investor positions. Bitcoin’s correlation with 10-year U.S. Treasury real yields recently turned negative; gold’s correlation with the S&P 500 now resembles Bitcoin’s positive correlation with equities—indicating both have recently behaved more like risk assets. Analysts reiterate that a second-half rally requires clarity on treasury dividend policy and passage of the Clarity Act—currently assessed at <50% probability. Yet current market weakness may ultimately serve as a “bullish contrarian signal.”

5. Jack Mallers, founder of Strike and CEO of Twenty One Capital, stated that Bitcoin’s current price reflects the true state of the global liquidity crisis. He pointed out that the University of Michigan Consumer Sentiment Index has hit a historic low—even as the S&P 500 sits at record highs—suggesting central bank intervention has distorted the equity market’s signaling function. Mallers remarked, “Bitcoin is the closest thing we have to monetary truth.”

Mallers believes nations are simultaneously financing war, AI development, and deficit spending, while individuals default on credit cards and rent—putting the world in “cash-raising mode,” selling the most liquid assets. “You sell what you can—not what you want to.” Regarding Strategy’s sale of 32 BTC, Mallers said it reflects the reality that its “never-sell” stance is no longer viable. He questioned Strategy’s perpetual-first instrument, which imposes permanent liquidity obligations—forcing trade-offs among stakeholders each time liquidity is needed.

V. Today’s Market Calendar

Key Events Ahead

June 12 (Friday)

- SpaceX officially lists on Nasdaq (Ticker: SPCX): A landmark IPO event—first trading day, expected to boost market sentiment. ★★★★★

- U.S. Economic Data: Preliminary June University of Michigan Consumer Sentiment Index; preliminary June 1-Year Inflation Expectation.

Institutional Views:

Leading investment banks and analysts adopt a cautiously optimistic stance toward current markets. Easing geopolitical risk—such as progress on the U.S.-Iran agreement—has lifted risk assets; the strong rebound in U.S. equities, especially semiconductors, underscores AI demand resilience, while falling oil prices reflect easing supply concerns. Banks like BofA see long-term potential in stocks like Intel, while maintaining a neutral-to-cautious outlook on gold and crude oil in the near term. Crypto markets benefit from macro improvements; ETF flows show volatility but medium-term trends remain favorable. Consensus emphasizes monitoring agreement implementation details, inflation data, and Fed signals—and recommends seeking structural opportunities amid volatility while avoiding excessive leverage.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute investment advice. Data herein may contain unavoidable inaccuracies; please refer to real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News