Grayscale: Ethereum’s Staking Model Needs an Overhaul

TechFlow Selected TechFlow Selected

Grayscale: Ethereum’s Staking Model Needs an Overhaul

The community is discussing implementing a staking reward cap curve, and Grayscale believes this is beneficial for ETH’s long-term price.

Author: Zach Pandl, Head of Research at Grayscale

Translation & Editing: TechFlow

TechFlow Intro: Zach Pandl, Head of Research at Grayscale, argues that Ethereum’s current staking reward model faces two structural challenges: (1) L2 offloading has reduced token burns and increased net issuance; and (2) the staking threshold is approaching zero, potentially locking nearly all ETH into staking. The community is discussing implementing a staking reward cap curve; Grayscale believes this would be beneficial for ETH’s long-term price.

The Ethereum community is considering modifying the network’s staking reward model—specifically, incentivizing staking only up to a certain threshold, with no additional rewards beyond that point. If implemented, nominal returns for stakers would decline. Yet Grayscale contends this would be positive for ETH’s long-term price for two reasons: first, it would curb ETH inflation; second, it would strengthen ETH’s narrative as a store of value.

This reform discussion is driven by two compounding issues.

Weakening Token Burns and Rising Net Issuance

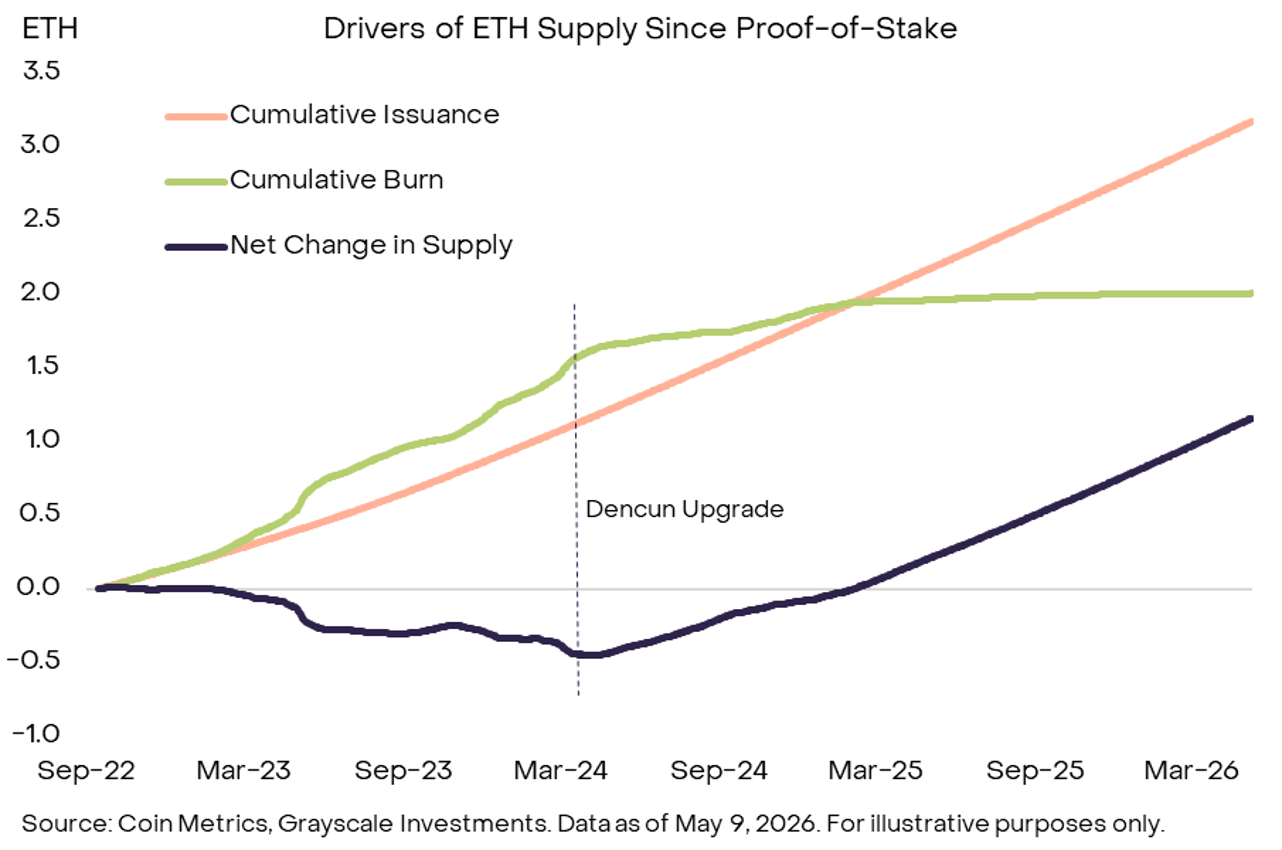

ETH supply is determined by the difference between new issuance and token burns. Currently, Ethereum’s Layer 1 (L1) burns all base transaction fees; high fees mean more ETH is burned, thereby constraining supply growth.

Recent developments over the past few years have disrupted this balance. As more activity migrates to Layer 2 (L2) networks, L1 transaction fees—and thus token burns—have declined, causing net issuance to rise.

Caption: Exhibit 1 — Drivers of ETH supply changes since Proof-of-Stake (PoS). Following the Dencun upgrade, cumulative burns (green line) have flattened, while cumulative issuance (orange line) continues rising, shifting ETH’s net supply change (dark line) from negative to positive. Source: Coin Metrics, Grayscale Investments; data as of May 9, 2026.

Compounding matters, Ethereum’s L1 is now actively pursuing scaling to compete with high-throughput chains like Solana. Pandl states candidly: L1 transaction fees are likely to remain low for the foreseeable future, token burns will continue declining, and net supply growth will further accelerate.

Negligible Friction Costs for Staking

When staking was first introduced on Ethereum, users could not withdraw their assets—their staked ETH remained locked and illiquid, warranting a risk premium. Today, withdrawals are enabled, liquidity has improved significantly, and the risk premium has evaporated.

More critically, liquid staking tokens (LSTs), exchange-traded products (ETPs), and corporate ETH treasuries have all entered the staking ecosystem. The marginal cost of staking ETH is now effectively zero. As long as the network continues offering marginal returns to stakers, nearly all ETH may eventually be staked.

Staking is essential for Ethereum’s protocol to function properly—but an excessively high staking ratio could backfire.

Two risks arise. First, unnecessary dilution: rising net issuance without commensurate gains in network security resembles a country overspending on defense with no tangible improvement in national security. Second, centralization tail risk: a small number of institutions could dominate staking activity. Given network effects among service providers, this scenario is plausible.

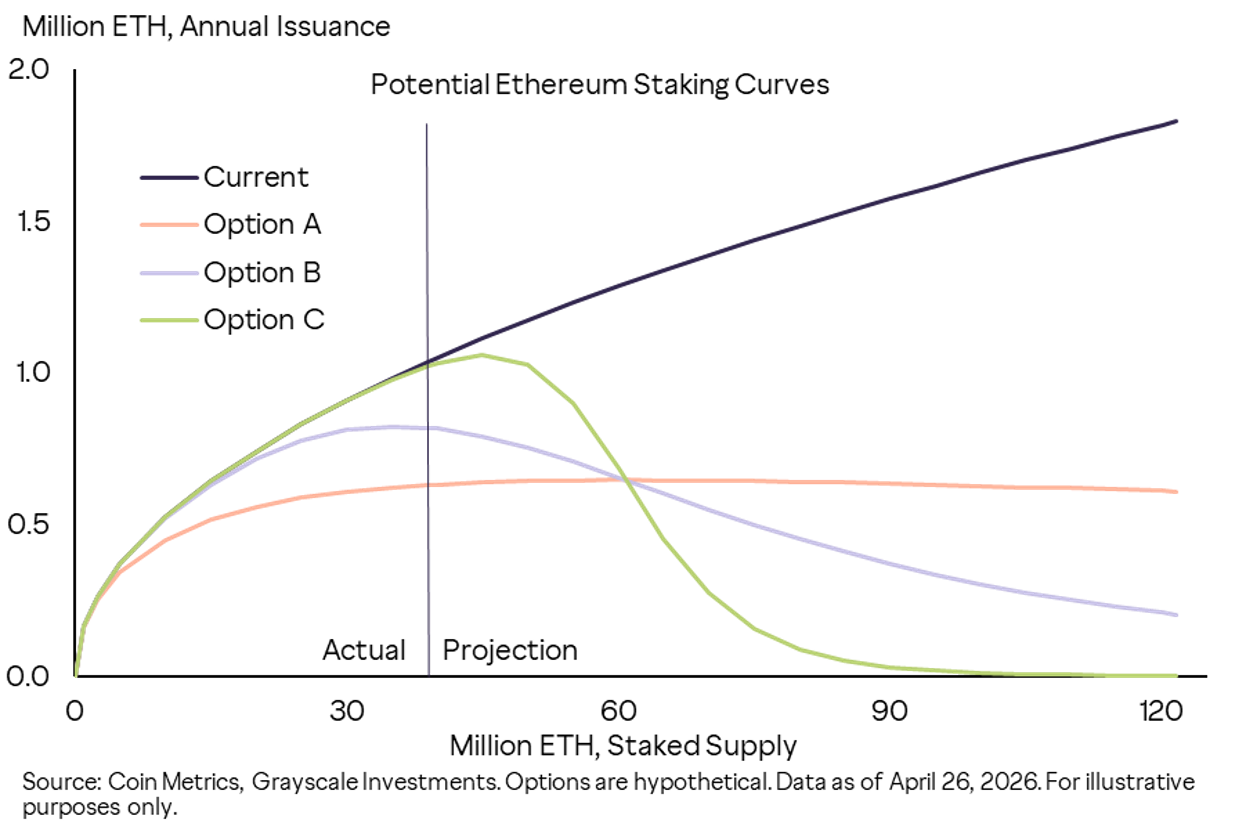

Implementing a Staking Reward Cap Curve

One solution is to shift toward a reward model that incentivizes staking only up to a certain level.

Caption: Exhibit 2 — Alternative staking reward curves Ethereum may consider. Under the current model (dark line), annualized issuance grows linearly with staked ETH; Options A/B/C introduce caps or inflection points at different staking levels, flattening—or even reducing—issuance once the staking ratio exceeds a given threshold. Source: Coin Metrics, Grayscale Investments; data as of April 26, 2026. All options are hypothetical.

Grayscale believes such a change would benefit ETH’s long-term market value. ETH is a functional commodity—not a financial claim like stocks or bonds—and should not be priced solely based on cash flows. Updating the staking reward model would reduce supply growth and enhance ETH’s scarcity. For commodities, production cuts are price-positive; ETH follows the same logic.

Reducing network tail risk and controlling long-term inflation would also increase demand for unstaked ETH as a digital store of value.

Another often-overlooked perspective: ETH’s price volatility impacts investment returns far more than staking yields do. The current ~3% annualized staking yield is roughly equivalent to ETH’s daily price movement (its 360-day annualized volatility is ~60%, translating to ~3% daily volatility).

Conclusion: Ethereum may revise its staking reward model to constrain long-term supply growth and mitigate specific tail risks. If implemented, Grayscale views this as bullish for ETH’s price.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News