Bitget UEX Daily Report | Markets Await Fed’s FOMC Rate Decision; Earnings from the “Big Four” Tech Giants Arrive, Putting AI Trading to the Test

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Markets Await Fed’s FOMC Rate Decision; Earnings from the “Big Four” Tech Giants Arrive, Putting AI Trading to the Test

Overall, the current environment is testing AI-driven trading logic and the ability to price geopolitical risks. Investors are advised to monitor the market volatility window following the Federal Reserve’s meeting and accumulate high-quality assets on dips.

I. Top News

Federal Reserve Updates

The Fed is expected to hold rates steady this week; Powell’s term may be briefly extended

- The FOMC meeting on April 28–29 will release its decision today. Markets widely expect the federal funds rate to remain unchanged. The key focus will be whether the statement’s wording signals that the path toward rate cuts has effectively stalled.

- Republican Senator Tillis stated that after Powell’s chairmanship ends on May 15, he may remain temporarily on the Federal Reserve Board to await outcomes of building project reviews and related appeals.

- This comment aligns with expectations of a “final dance,” meaning policy continuity is highly likely in the near term. However, if the statement proves hawkish, market pricing for future easing will likely be further delayed.

Market impact: Continued uncertainty around the rate path may continue weighing on risk-asset valuations. Precious metals and cryptocurrencies face short-term pressure—but a dovish signal could boost safe-haven demand.

International Commodities

UAE officially exits OPEC on May 1; short-term oil price volatility expected to be limited

- The UAE has formally exited OPEC. Major Wall Street investment banks assess that Brent crude is unlikely to experience significant near-term volatility, primarily because the Strait of Hormuz remains the current bottleneck for energy exports.

- Looking ahead, if a U.S.-Iran peace agreement is reached and shipping through the Strait normalizes, the UAE would be freed from production quotas and able to expand output freely—increasing global supply pressure and raising downside risks for oil prices.

- Trump previously portrayed Iran as being in a “state of collapse.” Meanwhile, the U.S. has prohibited domestic entities from paying transit fees to Iran for passage through the Strait—further escalating geopolitical tensions.

Market impact: Oil prices are supported by near-term geopolitical risk, but medium-term expectations of looser supply may weaken OPEC+’s ability to underpin prices. Energy-driven inflation remains a critical variable influencing Fed decisions.

Macroeconomic Policy

Trump’s approval rating hits new low amid rising cost-of-living pressures and Iran tensions

- The latest Reuters/Ipsos poll shows Trump’s approval rating has fallen to 34%, down from mid-April levels—driven mainly by rising living costs and heightened energy prices stemming from Iran-related developments.

- Public confidence in economic performance remains weak, with only 22% approving of his handling of cost-of-living issues.

Market impact: Declining polling numbers may heighten policy uncertainty. Combined with energy-price pass-through effects, short-term inflation expectations are likely to rise—weighing on risk-asset valuations.

II. Market Recap

Commodities & FX Performance

- Spot gold: +0.18%, at $4,600/oz—two consecutive days of pullback.

- Spot silver: +~0.3%, at $73/oz.

- WTI crude: −~0.73%, at ~$99/bbl.

- Brent crude: −~0.57%, at $103/bbl.

- U.S. Dollar Index: currently at 98.58, slightly lower.

Cryptocurrency Performance

- BTC: −~1.3% over 24 hours, currently at ~$76,300—slight pullback following recent consolidation, awaiting FOMC decision catalyst.

- ETH: −~0.77% over 24 hours, currently at ~$2,280.

- Total crypto market cap: −~1% over 24 hours, now at ~$2.64 trillion.

- Liquidations: ~$189 million liquidated in 24 hours, including ~$127 million in long positions.

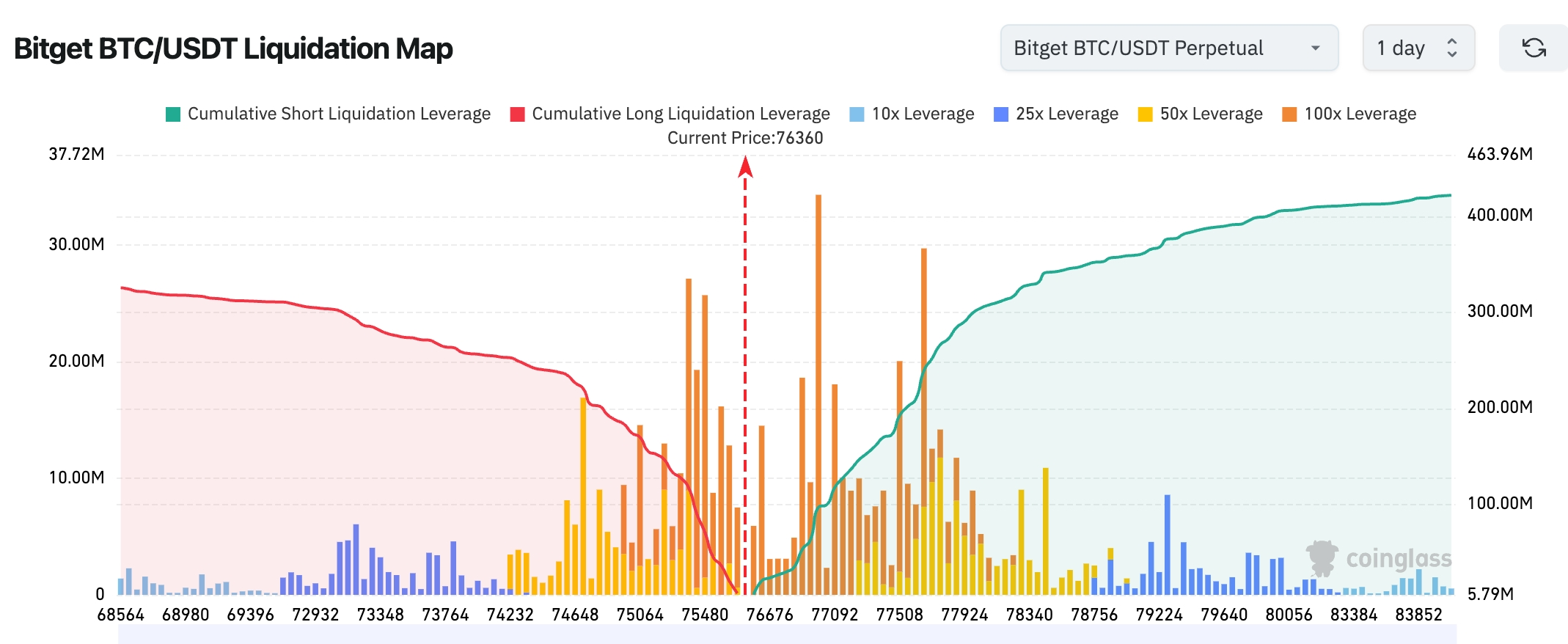

- Bitget BTC/USDT liquidation heatmap: Current price ~$76,300. Heavy short liquidations cluster between $77k–$78k—suggesting potential short squeeze and upward resistance testing in the near term. However, long leverage remains concentrated near $75k; a break below could trigger cascading long liquidations and rapid downside movement.

- Spot ETF net inflows/outflows: BTC spot ETFs saw $22.5 million net inflow yesterday; ETH spot ETFs saw ~$8.6 million net outflow.

- BTC spot flows: $1.726 billion inflow, $1.786 billion outflow—net outflow of $60 million.

U.S. Equity Index Performance

- Dow Jones Industrial Average: −0.05%, at ~49,142—relatively stable trend.

- S&P 500: −0.49%, at ~7,138.8—dragged notably by tech-weighted components.

- Nasdaq Composite: −0.9%, at ~24,663.8—AI-related stocks weighed heavily on the index.

Tech Giants Update

- Apple (AAPL): $270.71 (+1.15%)

- Microsoft (MSFT): $425.10 (+1.04%)

- NVIDIA (NVDA): $213.50 (−1.59%)

- Amazon (AMZN): $261.20 (−0.52%)

- Alphabet (GOOG): $348.80 (−0.29%)

- Meta (META): $675.50 (−1.07%)

- Tesla (TSLA): $378.20 (−0.67%)

Market attention shifts to Q1 earnings reports after market close today from four mega-cap tech firms—Microsoft, Amazon, Alphabet, and Meta. AI-related trading sentiment has cooled somewhat; a Wall Street Journal report highlighting OpenAI’s revenue and user growth falling short of targets further pressured chip stocks—with NVIDIA leading the decline. Apple and Microsoft—stocks with relatively defensive characteristics—held up better, reflecting investor positioning ahead of earnings.

Sector Movement Observations

Memory-related stocks posted notable declines (broadly weaker)

- Key names: SanDisk −6.34%, Micron Technology −3.86%

- Catalyst: Pre-market sector-wide demand concerns weighed on sentiment—though Seagate’s after-hours earnings beat triggered a rebound (Seagate +>16%).

Semiconductor sector showed divergence

- Key name: NXP Semiconductors (NXPI) surged +15% after hours

- Catalyst: Q1 revenue rose 12% YoY—beating expectations—and guidance for Q2 was raised, signaling accelerating demand recovery.

III. In-Depth U.S. Equity Analysis

1. Seagate Technology (STX) – Third-Quarter Results Strongly Beat Expectations

Event Summary: Seagate reported third-quarter revenue of $3.11 billion—exceeding analyst expectations of $2.95 billion. Adjusted EPS came in at $4.10—well above the $3.50 forecast—and adjusted operating margin reached 37.5% (vs. 34.8% expected). Shares surged >16% after hours. Market Interpretation: Institutions view these results as confirmation of recovering storage demand—especially robust AI-driven demand for high-capacity HDDs—bolstering confidence in the company’s future profitability. Investment Takeaway: Near-term earnings momentum supports valuation uplift, though sustained downstream demand must be monitored against macro headwinds.

2. NXP Semiconductors (NXPI) – Q1 Revenue Beats Expectations; Q2 Guidance Raised

Event Summary: NXPI reported Q1 revenue of $3.181 billion—a 12% YoY increase and above consensus. Non-GAAP EPS was $3.05 (+16% YoY); GAAP EPS reached $4.43, boosted by one-time gains from the sale of its MEMS sensor business. The company also issued an upbeat Q2 outlook. Shares jumped >15% after hours. Market Interpretation: Analysts note broad-based recovery across end markets signals accelerating semiconductor demand revival; the MEMS divestiture gain further enhanced earnings highlights. Investment Takeaway: Clear demand recovery signals present opportunities tied to the bottoming-out and reversal phase of the semiconductor cycle.

3. Robinhood (HOOD) – FY2026 Q1 Revenue Up 15% Year-on-Year

Event Summary: Robinhood reported Q1 revenue of $1.067 billion—up 15% YoY—but shares fell ~9% after hours. Market Interpretation: Revenue growth stemmed largely from platform expansion, yet market focus centers on shifting crypto-trading revenue contribution and evolving regulatory implications. Investment Takeaway: Rising platform user engagement remains a long-term positive; short-term valuation adjustments are likely following earnings release.

IV. Cryptocurrency Project Updates

1. Coinbase Institutional and Glassnode reports indicate markets remain influenced in the near term by macro conditions and Middle East tensions—direction remains unclear—but overall sentiment leans cautiously optimistic. A bottoming and rebound later this quarter is anticipated. Bitcoin sentiment has shifted from fear to optimism, with >70% believing it is undervalued. Ethereum shows declining short-term holdings and rising long-term accumulation—indicating speculative capital has exited and structural improvements are underway.

2. Bloomberg ETF analyst James Seyffart posted on X that market prediction ETFs are expected to launch next week. Roundhill’s filing indicates an effective date of May 5. Initial offerings will center on wagers regarding Democratic or Republican control of the House or Senate. Seyffart expects other issuers—including Bitwise and GraniteShares—to file similar applications shortly and potentially launch on the same or closely aligned dates.

3. CryptoQuant analyst Darkfost notes Bitcoin’s 7-day average realized loss stands at $829 million, while realized profit totals $566 million. Net realized profit briefly turned positive on April 9 but reversed again within two weeks. Darkfost also points out that on-chain data shows 64% of circulating supply is in profit—a level insufficient historically to sustain prolonged upward trends.

4. The U.S. Commodity Futures Trading Commission (CFTC) filed suit in a Wisconsin federal court against Governor Tony Evers, Attorney General Joshua Kaul, and Gaming Division Director John Dillett—the CFTC’s fifth state-level lawsuit in one month, following actions against Illinois, Arizona, Connecticut, and New York.

5. According to Onchain Lens, Bitmine staked 107,992 ETH (~$248 million) hours ago. Its cumulative staked ETH now stands at 3,923,389 ETH (~$8.98 billion).

6. Pump.fun announced on X that it has burned all previously repurchased PUMP tokens—valued at ~$370 million, representing ~36% of circulating supply. Additionally, Pump.fun has launched a one-year programmable buyback-and-burn program, allocating 50% of future revenues to purchase PUMP tokens on the open market and immediately burn them.

V. Today’s Market Calendar

Data Release Schedule

Key Event Preview

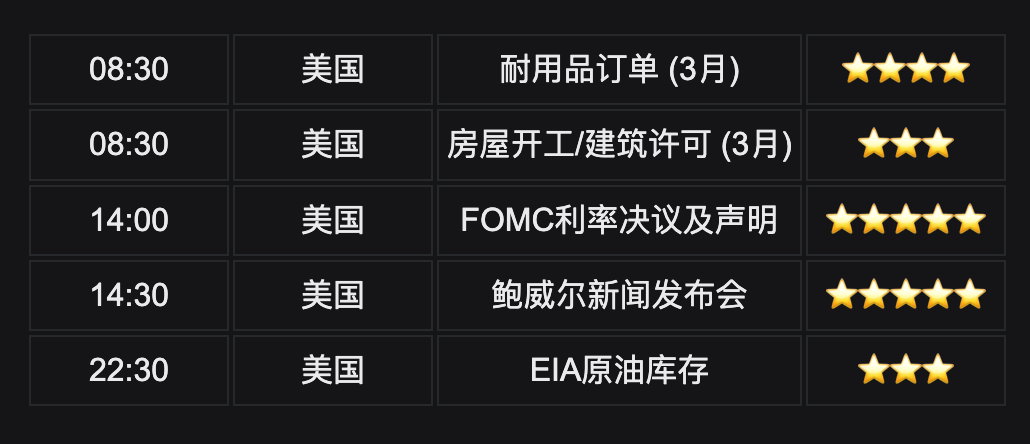

Wednesday (April 29)

- After-market Q1 earnings releases from Alphabet, Amazon, Microsoft, and Meta Platforms ★★★★★ (The true start of earnings season; AI growth and profitability metrics will directly determine whether the market can sustain its rally—extreme volatility expected)

Thursday (April 30)

- Fed FOMC interest-rate decision (UTC+8, 02:00) + Powell press conference (02:30) ★★★★★

(Markets intensely focused on the dot plot and rate-cut path; Powell may deliver his final major statement before term expiry.)

- March PCE price index (the Fed’s preferred inflation gauge) ★★★★★

- Apple’s after-market Q1 earnings release ★★★★★ (The final “Magnificent Seven” member; AI and services performance will be closely watched)

- Others: Eli Lilly and Western Digital pre-market; SanDisk after-market

Friday (May 1)

- U.S. Q1 GDP data (first official readout of actual economic impact from Middle East tensions)

- ISM Manufacturing PMI

- Chevron and ExxonMobil pre-market Q1 results

*Overall trading recommendation: This week features the dual climax of earnings season and the FOMC meeting. The “Magnificent Seven” earnings and PCE data are the primary drivers. If AI-related results exceed expectations, risk appetite may improve; otherwise, hawkish Fed commentary or elevated inflation readings could suppress markets. Focus on structural opportunities within large-cap tech.

Institutional Views:

Leading investment bank analysts broadly agree the FOMC decision this week will serve as the short-term market barometer. JPMorgan and UBS note that although oil prices have surged due to geopolitical tensions, the Fed is highly likely to hold rates steady. Should the statement emphasize “data dependency” without excessive hawkishness, concerns about stagflation would ease—supporting a rebound in risk assets. In the crypto space, Glassnode and CoinShares data show institutional inflows into Bitcoin and Ethereum via ETFs have continued steadily—totaling over $4 billion in the past four weeks—demonstrating long-term capital remains committed despite short-term volatility. Wall Street strategists stress that any dovish signal from Powell could propel BTC back above $78,000; conversely, oil-driven inflation pressure may trigger synchronized corrections in both crypto and U.S. equities. Overall, current conditions are testing the resilience of AI-driven narratives and the market’s ability to price geopolitical risk—investors are advised to monitor post-FOMC volatility windows and accumulate quality assets on dips.

Disclaimer: The above content was compiled using AI-powered search tools and verified manually prior to publication. It does not constitute investment advice. Data herein may contain unavoidable inaccuracies; please rely on real-time market data for decision-making.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News