A Company “Destined to Be Eliminated”—Why Is Its Return Outperforming Solana, the S&P 500, and the Nasdaq?

TechFlow Selected TechFlow Selected

A Company “Destined to Be Eliminated”—Why Is Its Return Outperforming Solana, the S&P 500, and the Nasdaq?

I’m betting that Western Union will outperform Solana—the narrative shift has depressed its valuation, while distribution channels are the real moat.

Author: Santiago Roel Santos

Translated by: TechFlow

TechFlow Intro: The central thesis of this article is a counterintuitive claim: the biggest beneficiaries of stablecoins are not the startups building them—but rather established institutions with distribution channels.

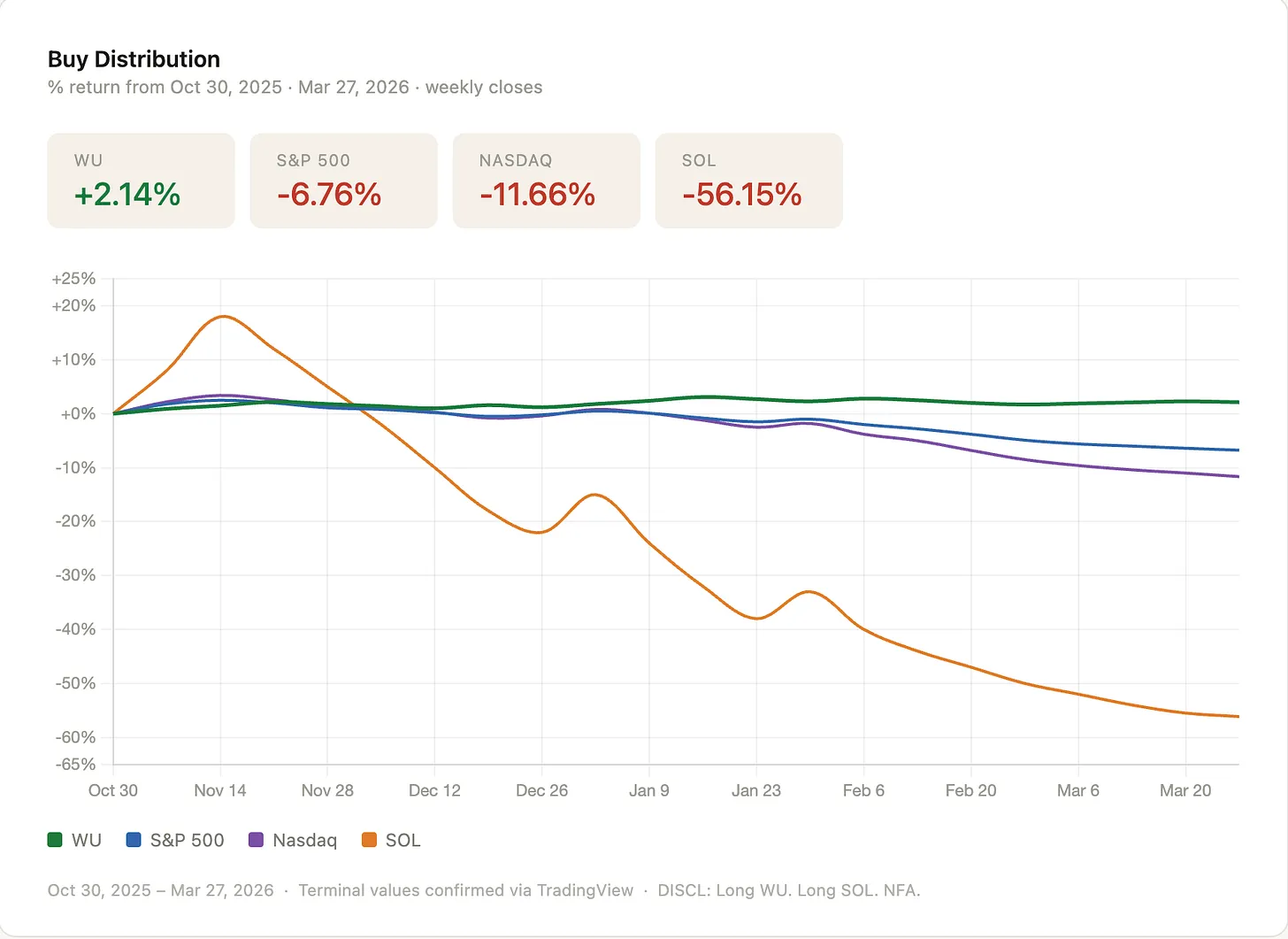

In November 2025, the author bet that Western Union (WU) would outperform Solana—and it did, decisively. It also outperformed both the S&P 500 and the Nasdaq.

What’s worth reading isn’t just the conclusion, but how the author identifies opportunities using the framework of “disruption narratives depressing valuations” and “distribution channels priced at zero.”

Full Text Below:

I began researching Western Union because I believed stablecoins would disrupt its business. Why pay WU fees when you can send money anywhere in the world via stablecoins at near-zero cost? Later, I realized WU’s business is far stronger than that framing suggests—and better positioned than almost anyone to embrace stablecoins. It has brand recognition and an extensive distribution network. The key risk lies in whether management will act.

They hadn’t acted before. Until recently, they appeared dismissive. When I placed my bet in November 2025, I wagered they would eventually act—or someone would force them to. I’m not an activist investor, but I sensed mounting pressure.

This week, I spoke at the Digital Assets Summit—and so did WU’s CEO. I saw a markedly different CEO, one who clearly articulated how stablecoins will compress the cost of global fund flows.

I accepted the risk that this shift might happen—and I liked my odds. At the time, WU traded at a 3x P/E ratio amid slowing growth. Many companies trade at such valuations—and then go bankrupt. Betting on distressed enterprises is tempting: some transform; others go to zero.

What I saw in WU—and still see—is distribution. A market-leading brand with deep consumer insights, trusted by users, and intimately familiar with both consumer resistance to new financial primitives like stablecoins and their reliance on familiar tools. People will always pay for convenience. They trust WU. It’s embedded in corner stores, bodegas, and retail service points where less tech-savvy consumers withdraw cash. That won’t vanish overnight.

I’ve read The Innovator’s Dilemma, and I’ve invested in the very technologies claiming to replace WU. But I’ve grown increasingly convinced that distribution is extremely hard to build—and trust is even harder, especially in financial services.

All this is to say: Since I bet WU would outperform Solana, it has—substantially—and also outperformed both the S&P 500 and the Nasdaq. A classic mean reversion.

Starting From the Assumption That Markets Are Right

I always begin by assuming markets are right—and then work backward to uncover why.

For WU, I kept arriving at the same answer: the market prices it as a melting ice cube—a dying business slowly eroded by Remitly, Wise, and some seed-stage stablecoin-native remittance startup launched last week. If management does nothing, perhaps that’s correct. But price is the most important variable—and at this valuation, there’s considerable margin of safety.

WU’s market cap is $2.8 billion. When I first researched it last year, its P/E was nearly 3x; today it’s 6x. $4.1 billion in revenue, $923 million in EBITDA, $500 million in net income, and a 12% net margin. This is not a dying business—it’s a cash-generating machine the market has already written off.

The gap in valuation multiples is real—and so are its underlying causes.

WU’s business is larger than both Remitly and Wise combined, operating across 200+ countries and generating nearly $1 billion in EBITDA annually. A 6x P/E implies you’re paying nothing for any recovery, any technology adoption, or any optionality. The market has priced all upside at zero. That’s where the margin of safety lies.

The Core Thesis

This is the foundational idea behind my founding of Inversion.

Markets often treat certain enterprises as “dead men walking,” assuming disruption is imminent—yet assign zero value to decades of built-up brand equity and distribution infrastructure. Layer in optionality from technology adoption, and asymmetry becomes compelling.

Markets are structurally long technology—and short anything that looks old. Innovation is accelerating; AI feels like it will replace everything. This isn’t about debating whether creative destruction will occur—it always does. It’s about price—and what you’re paying for it.

WU is acting—and faster than expected.

Western Union CEO Devin McGranahan has recently shifted his stance. This week, at the New York Digital Assets Summit, he explicitly outlined how stablecoins will compress the cost of global fund flows—turning negative float into positive float, and transforming a cost center into a revenue generator. WU has now announced the launch of its own stablecoin, USDPT, on Solana—ironically issued through Anchorage Digital. This pivot was catalyzed by the GENIUS Act.

This is no minor signal. A 175-year-old remittance company shifting from skepticism to launching its own stablecoin on Solana in under a year represents a profound change in management posture. The bear case has always been that they wouldn’t act—and now they are. That alone warrants a re-rating.

Execution risk remains—and always will. Everything will ultimately be disrupted. The key is understanding what you’re paying for that future to unfold. Downside risk is a 20–30% drawdown if revenue decline accelerates—buffered by a 10% dividend yield and $500 million in annual net income. Upside, as noted, is 4–5x if they regain any credible growth trajectory.

By contrast, most high-multiple tech stocks are priced on assumptions of flawless execution—so even a small deviation can unravel the thesis. When something is priced as dead, it takes only the faintest sign of life. WU is showing signs of life.

A Product Vision I Keep Returning To

Though I believe in technology, deploying it—and persuading customers to adopt it—takes time. The more you understand technology, the more you appreciate how well it performs specific tasks—but core human behaviors don’t change. This is especially true with money. When existing solutions work well, most people won’t try something new. Consumers will always pay for convenience.

Users prefer clicking WU over downloading and learning a digital wallet. This isn’t ignorance—it’s lifelong inertia, trust, and familiarity. That inertia carries real economic value. That’s why WU still processes nearly 300 million transactions annually—and why you can buy it at 6x P/E and collect a 10% dividend while you wait.

My core thesis—and position—is this: the greatest beneficiaries of cost-reducing technologies aren’t the startups building them, but the mature enterprises adopting them—those with established distribution channels. Whether it’s stablecoins compressing remittance costs or AI compressing operational costs, incumbent distribution is the fulcrum. Startups commoditize infrastructure; incumbents capture profits.

WU can reduce costs via stablecoin rails while preserving its hallmark convenience. If smart, it will launch a digital wallet to lower payment commissions. Global users could receive and hold dollars in a WU wallet—and spend them via Visa cards. If users don’t cash out, WU avoids needing to source liquidity in destination markets—further compressing costs. Distribution stays intact; infrastructure gets cheaper; margins expand. Cost reduction is controllable—and carries far lower intrinsic risk than underwriting revenue growth.

That’s the optionality the market is pricing at zero.

WU Is Just One Example

I’ve long accepted that I’ll never time the market perfectly. My forecasts of the future aren’t more accurate than anyone else’s sitting beside me. What I believe in is achieving superior returns through disciplined positioning.

That positioning always circles back to the same idea: buying durable businesses with distribution—at the right price. These businesses embed substantial optionality. Not everyone will act in time—and some will die. But those that do will massively outperform the broader market—and those gains will far outweigh losses.

You’re seeing General Catalyst, Thrive, and Bezos alike injecting AI into traditional businesses. The opportunity with stablecoins and blockchain rails is identical.

Inversion’s thesis is simple: buy assets with distribution at the best possible price—while holding the option to reshape the business with technology. Disruption narratives depress valuation multiples—that’s your entry point.

Invert—always invert. The question isn’t whether WU will be disrupted, but whether, at $923 million in EBITDA and a ~6x P/E, you’re being generously compensated for bearing that risk. I believe you are—and that the compensation is generous.

Disclosure: Long WU. Long SOL. This is not investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News