Dialogue with Blockworks Co-founder: 27 Predictions for 2026—Ethereum Revival, Solana Silence, Bitcoin Faces Quantum Shadow

TechFlow Selected TechFlow Selected

Dialogue with Blockworks Co-founder: 27 Predictions for 2026—Ethereum Revival, Solana Silence, Bitcoin Faces Quantum Shadow

2026 will be a very good year for DeFi.

Organized & Compiled: TechFlow

Guest: Mike Ippolito, Co-founder of Blockworks

Host: David Hoffman

Podcast Source: Bankless

Original Title: 27 Crypto Predictions for 2026 (Ethereum Renaissance, BlackRock Chain & More)

Release Date: December 31, 2026

Key Takeaways

David Hoffman sat down with Mike Ippolito to discuss why 2025, despite reaching new all-time highs, felt exceptionally difficult, and why this tension is crucial for 2026. They believe the crypto industry is entering a phase akin to the "2002 internet" – a period where speculation fades, fundamentals become important, and industry consolidation accelerates.

The conversation covered the reasons why Ethereum might see a renaissance, why Bitcoin sentiment could face challenges, how prediction markets and equity perps are actually performing, and what builders and investors should focus on as the crypto industry moves from hype to genuine value creation.

(This video content is based on 27 predictions proposed by Mike, but does not cover all of them, focusing only on selected key points for in-depth discussion.)

Highlights Summary

- I hope crypto can have a greater positive impact on the world; I'm tired of the industry being labeled as the "Wild West" and a "scam."

- Bitcoin will underperform gold in 2026.

- 2026 will be a very good year for DeFi.

- 2026 will be the year of Ethereum, while Bitcoin might have a bad year, Solana will be a relatively quiet year, and Hyperliquid will face challenges.

- 2025 was the best and worst year; we didn't get the price bull market everyone expected.

- The crypto market is gradually moving from its past wild, irrational state to becoming more rational and fundamentals-based.

- If you can identify projects with compounding growth potential and choose the right protocols, there will be good opportunities in 2026 and beyond.

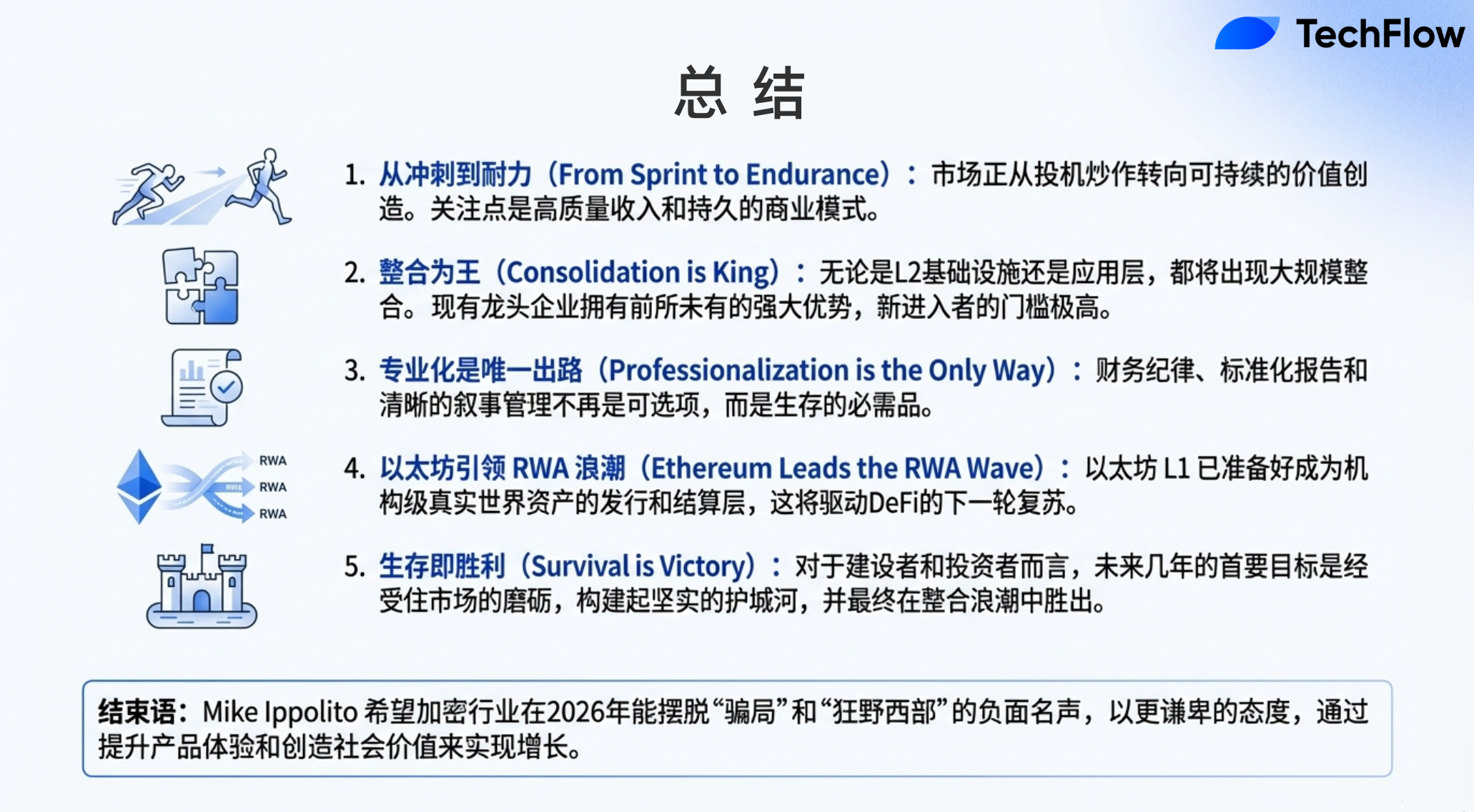

- In 2026, we may continue to see consolidation trends across multiple key categories. In the next three years, "survival is victory" will be the industry's theme.

- Builders need to prepare, be as creative as possible, think big picture, and strive to achieve their goals. They will either be acquired or win in their domain and achieve consolidation.

- 2025 and 2026 are setup years, with no mania; no one is going to get suddenly very rich from crypto.

- In cycles, when people feel bored, tired, or worn out by the market, it's actually the best time to persevere.

- 2026 will be a year of consolidation across multiple key categories; another theme is the convergence of stocks and crypto.

- If there's a DATS worth watching, it might be Tom Lee's.

- For traders, the hope is to be able to complete all trading for crypto and stocks on the same platform.

- Ethereum is more like the chain for asset issuance, while Solana is more like the on-chain price discovery venue for DEXs.

- Quantum computing is not just a crypto problem; it will impact the entire society.

- Centralized exchanges will scale down or up depending on how their strategies are built. We will see more acquisitions in the future, with these launchpads and CEXs actively participating.

Looking Back at 2025: The Best and Worst Year

David Hoffman: Looking ahead to 2026, how would you evaluate or summarize the state of the crypto industry in 2025?

Mike Ippolito:

In my view, 2025 was the best and worst year. The main reason is that we didn't get the price bull market everyone expected. While Bitcoin and some major coins hit new all-time highs, the overall performance fell short of expectations, especially for investors in fringe altcoins. Unless one was very lucky to pick the few coins that performed well, most people suffered significant losses.

Ethereum and Solana broke their all-time highs at different points, but the moves were very small and overall confusing. This might have been the toughest year for crypto investing, especially for those higher on the risk curve. From a price perspective, the year was full of confusion and challenges.

I think the crypto industry makes more sense now than ever before. An important theme this year was "cognitive dissonance." Many felt this situation was irrational: US regulatory sentiment towards crypto seemed to turn into a "bear hug," we saw many brilliant projects emerge, and direction became clearer. Logically, these should have driven asset prices up, but the market didn't comply.

The reason behind this is that the crypto market is gradually moving from its past wild, irrational state to becoming more rational and fundamentals-based. This change was predicted before but is now truly manifesting. Many excellent projects in the market are constantly improving, yet prices keep falling. This phenomenon might become a theme for 2026, as the market shifts from speculative valuation towards fundamental valuation.

While many projects in the market are excellent, their pricing has been consistently poor. I think this will continue to trouble investors into 2026. However, if you can identify projects with compounding growth potential and choose the right protocols, there will be good opportunities in 2026 and beyond.

David Hoffman:

Yes, if you told people at the beginning of 2025 that both Ethereum and Solana would hit new all-time highs, everyone would have thought a bull market was here, but these breakouts didn't have a real impact. Ethereum barely touched its ATH and then quickly fell back, which was disappointing. Solana's performance lasted a bit longer but wasn't particularly significant either. The only coin consistently above its ATH was Bitcoin, but even then, it's currently 30% to 40% off its ATH.

So in a sense, while we did see all-time highs, the market didn't truly feel the bull market atmosphere. Furthermore, 2025 didn't attract new crypto cohorts. In fact, all crypto investors have been in this space for at least three years, with the median now probably five years. This means market participants have formed expectations for the industry, but these expectations were shattered this year.

As you said, we are becoming more mature. Things are no longer the Wild West, and the market's expectation for the Wild West wasn't met, which I think led to subdued market activity.

Mike Ippolito:

I agree, and I'd like to give listeners an analogy; everyone likes to compare with the internet industry. I think we are now in a stage similar to late 2001/early 2002 Web 2.0. During the dot-com bubble, there were many bold ideas, everything seemed possible. People envisioned building a complete internet world. Although this vision ultimately proved correct, the path dependencies and timing were clearly off, leading to massive overbuilding of infrastructure.

Recently, I've heard a lot about AI-driven discussions, especially related to GPU usage. The situation with dark fiber in 2001-2002 is the opposite of today's GPU situation. Back then, the scale of building undersea cables and bandwidth was enormous. Investors were enthusiastic about telecom companies, believing they would own the internet's infrastructure. But the problem was severe overbuilding, which ultimately led to a massive bear market. At that time, people even thought the internet was dead, and it took years to rebuild confidence.

Meanwhile, a new generation of builders entered the market. They recognized the existing infrastructure and built upon it, finding new creative opportunities to establish businesses that could last for generations. This illustrates an important theme – consolidation. In 2026, we may continue to see consolidation trends across multiple key categories. In the next three years, "survival is victory" will be the industry's theme.

My advice is that builders need to prepare, be as creative as possible, think big picture, and strive to achieve their goals. Frankly, as a builder, there are basically two strategic choices: either get acquired, or win in your domain and achieve consolidation. These are the two most viable strategic paths right now.

Looking Ahead to 2026

David Hoffman: I think 2025 and 2026 are very important setup years, especially on Ethereum. I believe this view also applies to other areas. For Ethereum, I feel the Ethereum L1 protocol performed quite well this year, like zk EVM. Everyone is talking about Ethereum things, and its development is moving faster than we expected.

Maybe we are 1-2 years ahead on zk EVM, allowing us to significantly reduce block generation time in 2026. The Ethereum protocol also has a series of technical improvements that need to be built, delivered, and released, which I think will happen in 2026. By the end of 2026, I expect Ethereum's L1 protocol to be better positioned to capture growth opportunities in tokenization, Wall Street, etc. Whatever gets put on-chain in the future, Ethereum will become a more suitable technical protocol.

Also, I think we can talk about the Clarity Act. Hopefully, the Clarity Act passes in 2026, which would better position the entire crypto industry to capture the potential of tokenization. Even Solana is worth mentioning. Solana finally integrated Firedancer technology. This technology needs time to be fully integrated and accepted by the market.

I think 2025 and 2026 are quiet setup years, with no mania; no one is going to get suddenly very rich from crypto. If someone does get rich, it's an individual exception. We are collectively working to put all the pieces on the table correctly, preparing for potential value capture in the coming years. I think this is characteristic of a post-bubble era; it's about realigning and building infrastructure the right way to prepare for future growth.

Mike Ippolito:

I completely agree, and I think this is a positive sign. Usually when people talk about these things, there's an atmosphere: yes, these things will eventually happen, it's inevitable. But at the same time, people feel frustrated because they can't get 100x returns on altcoins.

However, I'd like to say that from a long-term perspective, building real wealth might be easier now than in 1995. In the past five years, almost no one has made money in crypto, although they might publicly claim they have. The reason is that this is a very difficult investment environment, with almost no assets providing stable returns.

Aside from Bitcoin, Ethereum, and Solana, almost all other assets are more like trading instruments than investments. I know there are exceptions, but overall, I remain very optimistic. I think we have finally entered an environment where we can build something truly sustainable, and the winners that can achieve compounding growth will achieve massive success.

Therefore, when we talk about the future, this potential pull effect is very exciting. This is the best time for the crypto industry in the past eight years.

David Hoffman:

I think we all know that in cycles, when people feel bored, tired, or worn out by the market, it's actually the best time to persevere. If you can endure these difficulties, you'll be in a favorable position. I remember in 2019, the situation was that everyone in the Ethereum ecosystem basically only focused on Bitcoin and Ethereum. While there were Cardano and Ripple communities, the Solana community wasn't that active.

For example, if you persevered and Ethereum positioned itself reasonably, you benefited from DeFi Summer. And you just had to survive the 2017, 2018, and 2019 bear market to get there because everyone else had left. The result was that opportunities in the market became very abundant because not many people were competing. My feeling is that this will happen again because people are being worn down by the market, and the market isn't inspiring investor enthusiasm.

David Hoffman: Your 27 industry predictions cover different ecosystems; we'll try to discuss them one by one. Before we officially start, how do you think we should guide the listeners?

Mike Ippolito:

I think we can first focus on some general themes. For example, we will validate or overturn some long-held beliefs in the industry. In the past, the crypto market was relatively irrational and very early; in most cases, creating real value wasn't necessary, so there was no effective feedback mechanism.

In the past, which beliefs were correct and which were wrong wasn't clear, but I think by 2026, many things will have clear determinations. I also think 2026 will be a year of consolidation across multiple key categories. We've seen similar situations before. My favorite example is the prime brokerage space.

Furthermore, I think another theme is the convergence of stocks and crypto. I mean, we might see something like equity futures in 2026, although I'm skeptical about this model actually landing. But I think crypto will move towards a more fundamentals-based, real-value approach, while the stock market will also borrow some characteristics from crypto. I think this convergence is already starting to happen.

These are my main themes for 2026.

Investor Relations in Crypto

David Hoffman: Let's move to the first topic. This is a current topic – investor relations will become increasingly important. Investors will demand standardized financial disclosures. While investor relations will borrow some aspects from traditional IR, it will also focus more on social media and community, ultimately redefining its performance in the stock market. This is exactly what you mentioned: the community management aspect of investor relations might converge with the traditional stock market, and the traditional market might also realize this and think, we need to do this too.

Mike Ippolito:

Yes, I think people need to build a mental model. When a business doesn't have a publicly traded financial instrument, it only has one product: its business. But once it launches a publicly traded financial instrument, like a token or stock, the CEO or founder of the business effectively has two products: one is the business, the other is the financial instrument. This means you need to constantly tell the market the story of this asset, making everyone aware of it.

You have your business product, and your financial instrument. This means you need to constantly tell the market the story of this asset, tell it to everyone. You need narrative management; a business can't just "build it and they will come." So besides ensuring your product and business make sense to investors, you also need to constantly tell the market the story of this asset. Historically, this narrative management has been comprehensive and systematic.

However, I've also observed how the stock market operates; some aspects are done very well, like standardized financial reporting systems (e.g., GAAP), which provide uniform accounting standards for all US businesses. But at the same time, there are things that seem very outdated, like using old software to get Zoom links, meeting with a bunch of analysts, etc.

A few years ago, CoinShares was a decent-performing company. As a company listed in Europe, they at least used to do quarterly earnings releases via Twitter Spaces. And now, we're starting to see some protocols or companies, like Etherfi, adopting similar approaches. I actually saw Vlad Tenev say a few days ago that they are rethinking Robinhood's investor relations, planning to make it more community-driven while leveraging social media channels, etc. So, I think crypto will borrow certain principles, like standardized processes, inviting analysts. But in the long run, the stock market might realize this and start rethinking their approach.

David Hoffman: We've already seen Coinbase and Robinhood host Apple-style product launch events this year, kind of showcasing their products. This indeed aligns with your point: we need to control our own narrative. This way, they can directly address the audience interested in Robinhood. For Robinhood investors, they can clearly see: "Yes, we did launch new products this year, here are our results." I remember Coinbase held at least a couple of such events, like for Base's launch and recently revealing some new products. They introduced these directly to their audience and explained why these products are worth investing in.

Mike Ippolito:

I think this is a big change this year. I have two related predictions; I think there will be a lot of discussion about GAAP accounting standards this year.

GAAP, Generally Accepted Accounting Principles. There's an old joke about accountants: a hiring manager is interviewing accountants. The first one comes in and is asked, "What are these numbers?" He gives an answer and leaves. Then the second one comes in, and the answer is: "This is what I think these numbers should be." Finally, the third one is asked the same question, and he answers: "What do you want these numbers to be?" And he gets hired.

This joke illustrates there's a lot of flexibility in accounting treatment. Even among many data providers in crypto, standards are very inconsistent; different companies report revenue numbers with huge variations. This necessitates an accepted standard to clarify how to treat revenue, how to calculate costs, and how to aggregate this data into cash flow statements.

Of course, there is some flexibility in accounting treatment, but there are also rules dictating what can and cannot be done. These rules constitute the accounting treatment accepted by US publicly traded companies. However, for crypto companies, the burden is still too heavy; reaching such standards is very difficult. While some lightweight solutions might emerge, I think there will be a lot of discussion about GAAP accounting standards this year, but the entire industry is still far from this standard; the difficulty of improvement is simply too high.

There has already been a lot of discussion about dual-token equity structures. My long-term prediction is that in 90% of cases, this structure simply doesn't work. It's just a legacy structure originating from the SEC during the Gary Gensler era, even before the SEC under J. Clayton. Essentially, it's a legacy attempt at some kind of regulatory arbitrage. However, many mental models built on this structure haven't worked.

We've already seen many public disputes, like with Aave. I think such disputes will continue. At the same time, I think Uniswap deserves great credit in this regard. They took a very brave and difficult step; I deeply sympathize. I'm not targeting Aave; this is a very difficult thing because it involves unwinding the results of much completed work, but the market might need some time to push protocol leaders to act. I expect these issues won't all be resolved in 2026. We might start hearing some discussions, with certain protocols – especially those with less organizational or governance burden – potentially quickly following Uniswap's lead. But I think most protocols might procrastinate on this.

However, I do think investors will start publicly questioning these protocols and may develop a negative view of protocols adopting dual equity and token structures.

The Evolution of Revenue Discussions

David Hoffman: Let's continue with the third prediction for 2026. Discussions about revenue will gradually shift towards durability and quality. Companies that can create more predictable revenue will receive market recognition for the first time. Enterprise software will become hot in crypto. Please elaborate.

Mike Ippolito:

I'm glad to see our industry has already started focusing on revenue discussions. If you listen to stock market discussions, you'll find a view I strongly agree with: not all revenue is created equal. In the stock market, certain types of revenue are assigned higher valuation multiples, and this is usually related to the quality of the revenue.

So, how sticky is the revenue? Is the revenue repeatable? Is 80% of revenue from a single customer? Is the revenue highly cyclical? All these different characteristics are dissected and analyzed to assess the business moat investors typically care about and the degree of risk the business faces in its revenue structure.

We haven't even touched on profit margins, but I think there's a similar phenomenon in crypto. We used to make a mistake: when we saw revenue charts climbing, we would annualize the peak revenue or assign excessively high valuations to cyclical revenue peaks. For example, when looking at cyclical stocks, a counterintuitive phenomenon is: cyclical stocks are cheapest when they look most expensive, and most expensive when they look cheapest.

This saying was widely circulated. As an industry, we used to make this mistake, assigning overly high valuations to highly cyclical revenue. I think investors will gradually stop trusting this unreliable revenue, and this is actually the right direction. I think this will push the entire industry to start focusing more on sticky revenue and high-quality revenue. You know, in crypto, this revenue model is actually very scarce. Although some businesses are trying, they haven't fully achieved it.

These on-chain products might have tokens or other revenue sources, but I believe we'll see more efforts to drive sticky and high-quality revenue in the future. Because the fact is, not all revenue is created equal.

The Future of DATS

David Hoffman: Let's move to the fifth prediction: DATS will basically do nothing. Some companies might attempt acquisitions in infrastructure and try to transform into operating companies, but these efforts won't truly succeed. You predict DATS will have a weak year in 2026, which I think fits the current industry development. But will there be exceptions?

Mike Ippolito:

I'm not taking a huge risk on this prediction, but I do think DATS will face considerable challenges in 2026. However, I think the only possible exception is Tom Lee's DATS. I think Tom Lee has done an excellent job in this regard; he has extremely high credibility on Wall Street. I also think this is closely related to the natural recovery of Ethereum's core metrics, which might generate investor interest.

Please note, this is absolutely not financial advice; everyone must do their own research. But I think, if there's a DATS worth watching, it might be Tom Lee's. Additionally, I think you'll see some DATS trying to transform into yield-providing operating companies.

However, I think many crypto companies are going through similar situations. Some of the most notable categories once received huge speculative premiums, but when they try to transform into more fundamental, real-value-creating models, unfortunately, they have to be reevaluated based on new metrics. Now it can be said that some of these DATS have already undergone this reevaluation; after all, the performance charts of most DATS in the market don't look optimistic.

But I still think it will take time for the market to start rewarding this structure. Besides "I am Soul plus a lot of extra Beta ETH plus extra Beta," there's a completely different story to tell. I think this will take a long time, but I do believe you'll see some DATS trying to move towards more sustainable structures, like making acquisitions related to staking or yield.

Venture Capital (VC) Investment Trends

David Hoffman:

Your sixth prediction is venture capital (VC) investment will be weak. It's predicted that investment in 2025 will decrease slightly, from an estimated $25 billion in 2025 to $15-20 billion.

Mike Ippolito:

This is indeed a decline. Looking back at 2020, we peaked at around $30 billion in 2021, so I'd say we're now in a downtrend; 2021 was a local maximum. We're still recovering from many past excesses. I need to point out that VC in equity financing and crypto doesn't perform exactly like the traditional model. Typically, investing in the early stages of a company carries greater risk, right?

Because you can think of it as a churn rate. Only a portion of companies go from Series C to Series A, only a portion go from Series A to Series B. So, the traditional view is that when investing in early stages, the risk is greater. But in crypto, this logic doesn't necessarily hold because you can get liquidity quickly, and very few token projects generate real long-term value.

Actually, the situation is the opposite. The earlier you get in, the less risk you actually bear, because you can later flip the tokens at a higher price, sometimes a very high price. But I think the situation now is that there are so many tokens, and investor requirements for projects are much higher than before.

Frankly, I think speculative capital is moving to other areas. The responsibility now lies in truly creating value, and the traditional models of risk existence and pricing will reassert themselves. The winners will continue to win. In major categories, like prediction markets, exchanges, lending protocols, decentralized exchanges (DEXs), the strategy will shift from "Uniswap took off, now there are Uniswap clones on Solana, Avalanche, and Sui, I'm going to fund these projects and flip these tokens" to "I'm going to bet on Uniswap because it has a moat, they will continue to win because competition has become more difficult, barriers to entry have increased." This has already started manifesting on Ethereum and Solana; the barriers to entry on these two platforms are now so high that these victories will continue to compound. You will start to see growth equity gradually entering this space.

Prediction Markets: Victory for Incumbents

David Hoffman:

Speaking of prediction markets, Kalshi and PolyMarket will continue to dominate prediction markets, other DEXs will try to enter, but no new players will make real progress. Exactly consistent with what I just said, I think incumbents will win here, and the number of incumbents even exceeds Kalshi. If you can call Kalshi an incumbent, then Robinhood will capture most of the prediction market share.

Mike Ippolito:

I have another prediction related to prediction markets, which is that prediction markets will continue to succeed in 2026, but I expect sentiment to change. I think there will be a lot of criticism of sports betting as a cultural phenomenon; it might receive negative coverage. Nonetheless, overall trading volume will continue to grow.

I see many VCs predicting 10x market growth, but I think growth closer to 2x is more realistic. Part of the reason, frankly, is purely sentiment. I think prediction markets face real challenges. So I think we're at a local maximum now, but I remain optimistic about the structural trend.

We used to have a wrong mental model, thinking "Hey, we just saw Kalshi and Polymarket define this category and succeed, they have many partners, but I just need to fund a bunch of new protocols with slightly different mechanisms or trading structures." But I don't think this strategy works.

I think this year moats in crypto have become very deep. However, there's one prediction I want to bring up, which is that the concept of "everything apps" will become very powerful. I think Coinbase, Robinhood, Hyper Liquid, and some Asian exchanges are considering this direction. In fact, we've already seen SEC Chairman Paul Atkins mention "everything apps" similar to China's Alipay multiple times. I think this will have a profound impact. For example, we've already

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News