Mining each bitcoin results in a $19,000 loss; Bitcoin mining firms collectively pivot to AI

TechFlow Selected TechFlow Selected

Mining each bitcoin results in a $19,000 loss; Bitcoin mining firms collectively pivot to AI

Listed Bitcoin mining companies, facing inverted mining costs, are accelerating their transformation into AI data center operators through debt financing and Bitcoin sales—a growing tension between network hash rate security and structural industry reshaping.

Author: Shaurya Malwa

Translated by: TechFlow

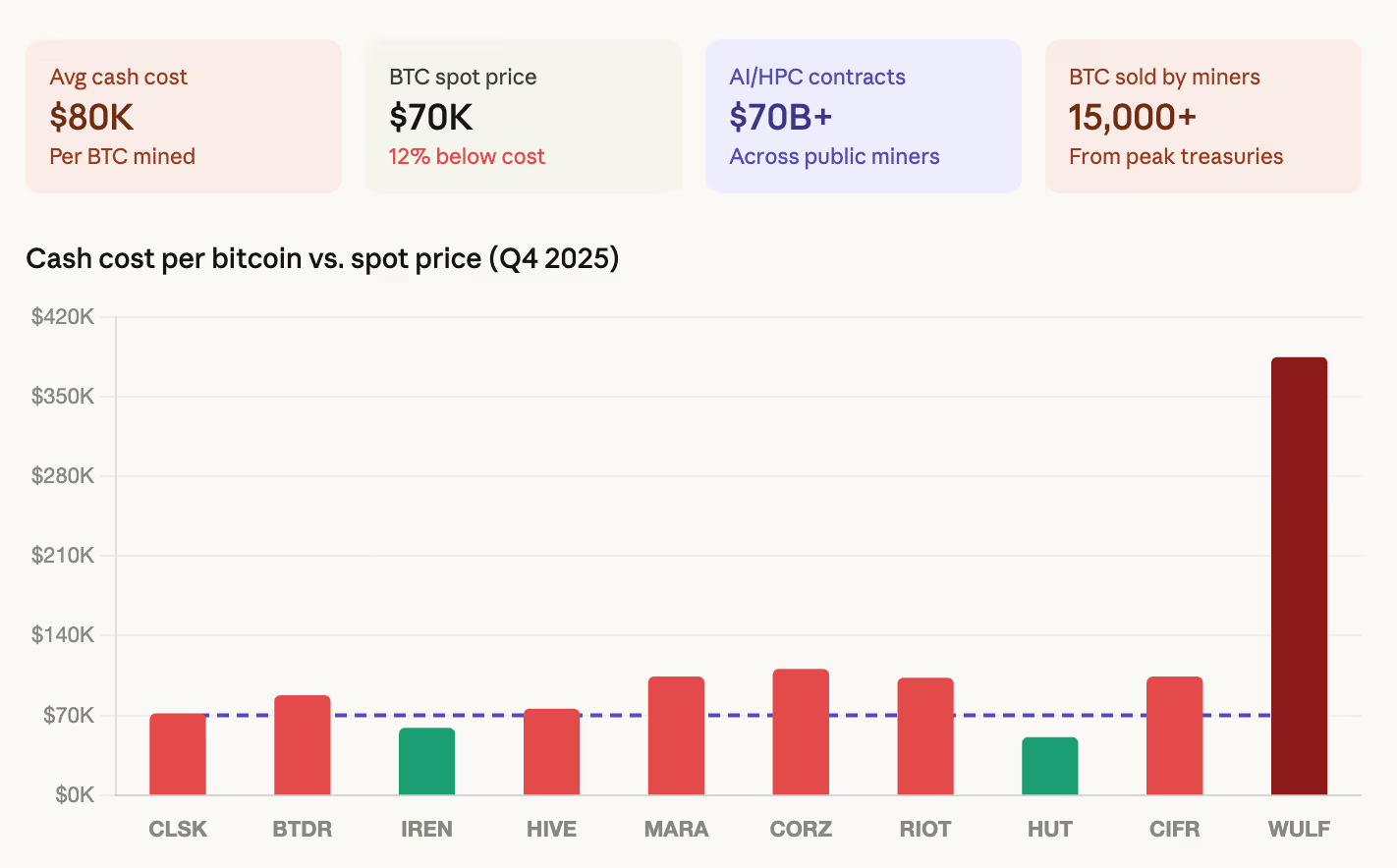

TechFlow Insight: According to CoinShares’ latest mining report, the weighted average cash cost for publicly listed mining companies to mine one bitcoin has risen to approximately $80,000—while BTC is currently trading between $68,000 and $70,000, meaning each mined bitcoin incurs a loss of roughly $19,000.

The industry is undergoing its most fundamental transformation since inception: over $70 billion in AI/HPC contracts have already been signed; publicly listed miners have collectively sold more than 15,000 BTC; companies such as IREN and TeraWulf now carry several billion dollars in debt. By end-2026, AI-related revenue could account for up to 70% of some miners’ total income. These firms are evolving from bitcoin miners into data center operators who happen to still mine bitcoin. The core contradiction lies in the fact that the very companies securing Bitcoin’s network security are selling their BTC to fund AI expansion—while network hash rate has fallen from a peak of 1,160 EH/s to roughly 920 EH/s.

- The bitcoin mining industry is undergoing its most fundamental transformation since inception—not signaled primarily by hash rate or difficulty adjustments, but by balance sheets.

- CoinShares’ Q1 2026 Mining Report, released this week, states that the weighted average cash cost for publicly listed miners to produce one bitcoin rose to approximately $79,995 in Q4 2025.

- Bitcoin has traded within a $68,000–$70,000 range, and a recent CoinDesk report estimated losses of roughly $19,000 per mined BTC.

- This level is unsustainable—and the industry knows it well. The response has been a wholesale pivot toward AI infrastructure—a shift actively reshaping the identity of these companies.

Per the CoinShares report, publicly listed mining firms have announced over $70 billion in AI and high-performance computing (HPC) contracts. CoreWeave’s expanded agreement with Core Scientific is valued at $10.2 billion over 12 years. TeraWulf has secured $12.8 billion in HPC contract revenue. Hut 8 signed a $7 billion, 15-year AI infrastructure lease for its River Bend campus. Cipher Digital entered into a multi-billion-dollar agreement with Fluidstack, a Google-backed firm.

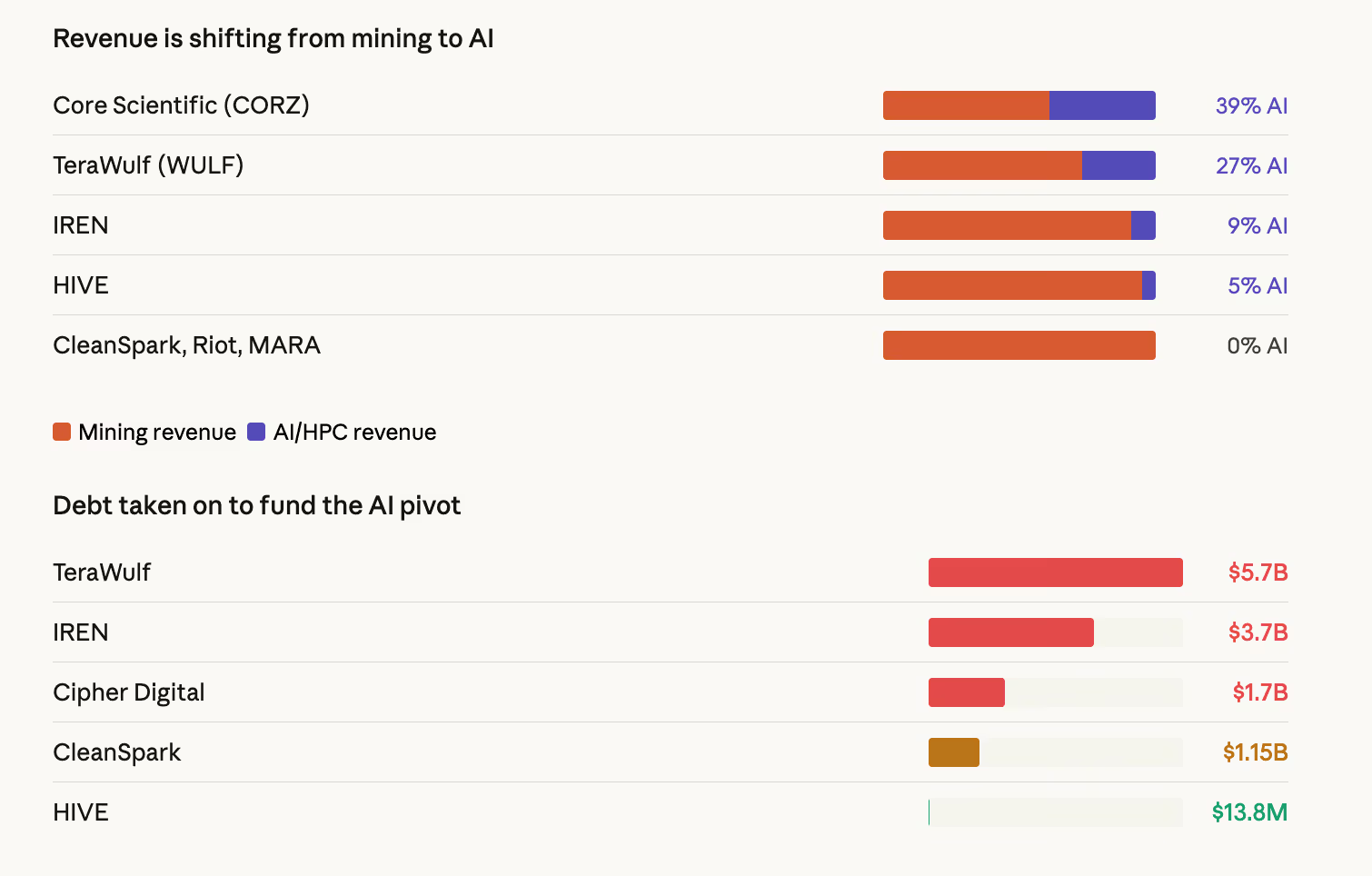

By end-2026, AI-related revenue may constitute up to 70% of total revenue for some listed miners—up from roughly 30% today. Core Scientific’s AI colocation revenue already accounts for 39% of total revenue; TeraWulf’s stands at 27%; IREN currently sits at 9%, but is expanding rapidly, with liquid-cooled GPU capacity under construction totaling up to 200 MW.

This means mining companies are increasingly resembling data center operators—merely coincidentally still engaged in bitcoin mining.

Economics explains why. CoinShares data shows bitcoin mining infrastructure costs approximately $700,000–$1 million per MW, while AI infrastructure costs $8–15 million per MW. The gap is substantial—but AI offers structurally higher and more stable returns.

The “hash price”—a metric measuring miners’ revenue per unit of hash power—fell to a post-halving record low of ~$28–$30 per PH/day in early March.

At that level, miners using mid-generation hardware require electricity priced below $0.05/kWh to maintain cash profitability. In contrast, AI infrastructure contracts promise gross margins exceeding 85%, backed by multi-year revenue visibility.

Where Is the Money Coming From?

CoinShares’ report identifies two clear sources of funding for this transformation—both plainly visible in the data.

First, debt issuance. The industry’s leverage profile has undergone a qualitative shift. IREN now carries $3.7 billion in convertible notes across five series. TeraWulf’s total debt stands at $5.7 billion, composed of convertible bonds and senior secured notes issued by its hashpower subsidiary.

In November, Cipher Digital issued $1.7 billion in senior secured notes, causing its quarterly interest expense to surge from $3.2 million over the prior nine months to $33.4 million in Q4 alone. This is not mining-scale debt—it is infrastructure-scale betting: a wager that AI revenue will arrive quickly enough to cover debt service obligations.

Second, BTC sales. Publicly listed miners have collectively sold over 15,000 BTC from peak holdings. Core Scientific sold ~1,900 BTC ($175 million) in January and plans to liquidate nearly all remaining BTC holdings by Q1 2026. Bitdeer zeroed out its BTC holdings in February. Riot Platforms sold 1,818 BTC ($162 million) in December.

Even Marathon—the largest publicly listed BTC holder (53,822 BTC)—quietly expanded its policy in its March 10-K filing to authorize sales from its entire balance-sheet reserves. Partly driving this decision is pressure on its $350 million BTC-collateralized credit facility—as BTC prices approach $68,000, its loan-to-value (LTV) ratio has climbed to 87%.

Who Will Secure the Bitcoin Network?

The very companies selling BTC to fund AI ventures are those whose mining operations secure Bitcoin’s network. This constitutes the central paradox of the transformation. When mining is unprofitable and AI is lucrative, rational economic behavior dictates reallocating capital away from mining. Yet if enough miners do so, the network’s security budget shrinks.

Hash rate data already reflects this. Network hash rate peaked at ~1,160 EH/s in early October 2025, then declined to ~920 EH/s—accompanied by three consecutive negative difficulty adjustments, the first such occurrence since July 2022.

Valuation Divergence

The market has already priced in this divergence. Miners with signed HPC contracts currently trade at 12.3x forward 12-month revenue, whereas pure-play miners trade at only 5.9x. The market assigns over double the premium for AI exposure—further reinforcing the incentive to transform.

Geographic dynamics are also shifting. The U.S., China, and Russia currently control ~68% of global hash rate. In Q4 alone, the U.S. gained ~2 percentage points of market share. Yet emerging markets are entering the fray—Paraguay and Ethiopia have both entered the top-10 global mining nations, driven respectively by HIVE’s 300 MW and Bitdeer’s 40 MW facilities.

Hash Rate Forecast

CoinShares forecasts network hash rate will reach 1.8 ZH/s by end-2026 and 2 ZH/s by end-March 2027 (one month later than its prior forecast).

However, this forecast assumes BTC returns to $100,000 by year-end. If price remains persistently below $80,000, CoinShares expects hash price to fall further and hash rate to decline further, prompting additional miner exits. Sustained sub-$70,000 pricing could trigger broader capitulation-style liquidations—an irony being that such a collapse would benefit surviving miners through lower difficulty.

New-generation hardware offers a potential lifeline. Bitmain’s S23 series and Bitdeer’s in-house SEALMINER A3 both deliver energy efficiency under 10 J/TH and are expected to ship at scale in H1 2026. Compared to current mid-generation rigs, these machines could cut per-BTC energy costs by roughly half. But deploying them requires capital—and many miners are redirecting funds toward AI instead.

At the start of this cycle, the bitcoin mining industry comprised companies protecting the network and accumulating BTC. It is exiting the cycle in a radically different guise: a cohort of AI data center builders financing their construction by selling BTC.

Is this merely a temporary response to adverse economics—or a permanent structural shift? One variable decides: BTC’s price. If it rebounds to $100,000, mining profitability recovers and AI transition slows. If it stagnates at $70,000 or lower, transformation accelerates—and the mining-centric industry that defined the past decade will continue dissolving into something entirely new.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News