Market Share Exceeds 61%: After Becoming the Undisputed Leader in Tokenized Stocks, Does Ondo Have New Highlights?

TechFlow Selected TechFlow Selected

Market Share Exceeds 61%: After Becoming the Undisputed Leader in Tokenized Stocks, Does Ondo Have New Highlights?

On the Eve of Tokenizing $150 Trillion in Equities: How Is Ondo Sustaining Its Market Dominance?

Author: TechFlow

Introduction

On March 16, 2026, NVIDIA’s GTC 2026 conference officially opened, and Jensen Huang’s keynote speech once again ignited market enthusiasm.

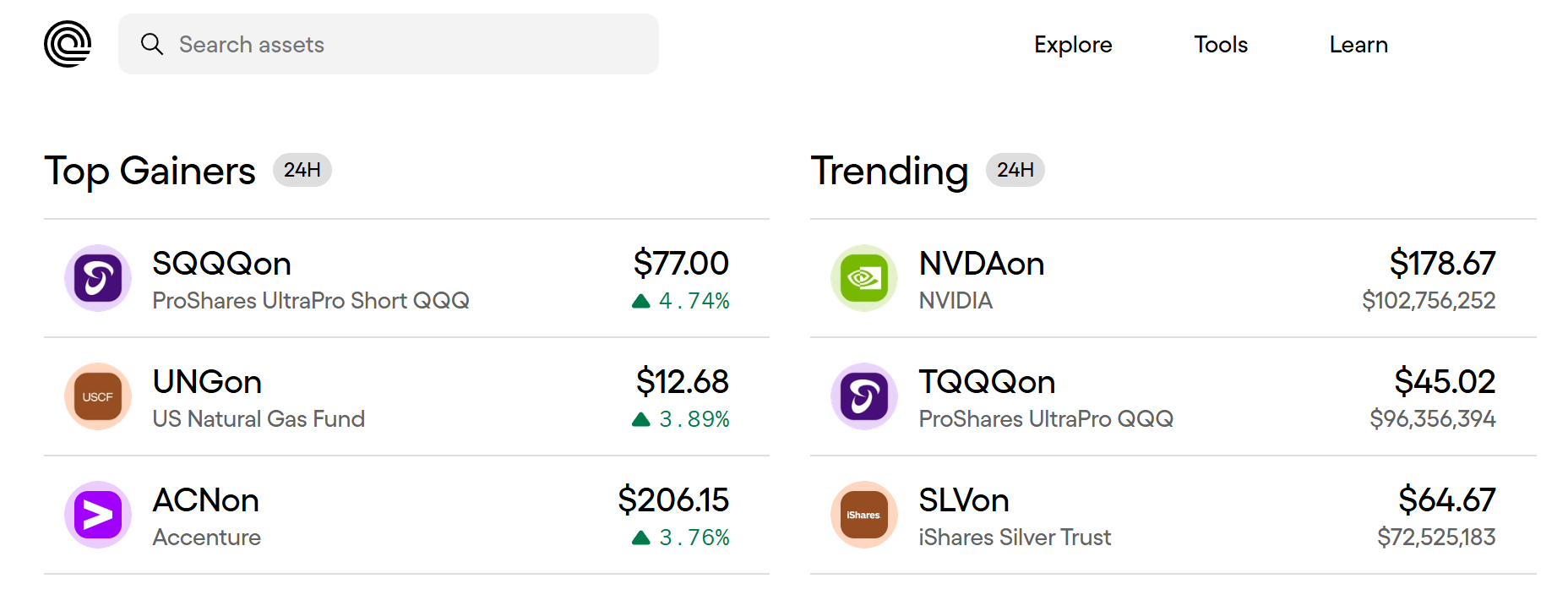

After listening to the speech, you’re convinced that NVIDIA will be a core beneficiary of the global AI wave—so you immediately invested in NVIDIA stock.

No cumbersome account-opening process. No waiting for U.S. market hours. Just a few simple mouse clicks—and tokenized NVIDIA stock is already sitting in your onchain wallet, with fees so low they’re nearly negligible.

A few years ago, this would have been almost unimaginable. Today, the tokenized stock market has surpassed $1.07 billion in size.

And if one name stands out as the primary force dismantling the wall between ordinary investors and high-quality global assets, it is unquestionably Ondo.

In September 2025, RWA leader Ondo Finance launched Ondo Global Markets, opening trading for over 100 stocks and ETFs simultaneously—marking the transition of tokenized stocks from fragmented experiments to large-scale expansion. Just over six months later, Ondo alone commands over 60% of the tokenized stock market share, making it the undisputed leader in this sector.

Perhaps this is what truly warrants attention:

In a market brimming with potential—and no shortage of competitors—a near-inescapable center has already emerged in its very first explosive phase.

Now that “onchain, freely tradable stocks” is no longer just an appealing story, deeper curiosity is naturally stirred by this “cliff-edge lead”:

In a space where opportunity is visible to all, what enables Ondo to convert that opportunity into its own territory first?

Deep-Dive Data on Ondo: From Surface to Substance—A Structural Lead

Before answering “Why Ondo?”, let’s first examine just how far ahead Ondo stands relative to its competitors.

Assessing competitive dynamics in any market is most directly done through data.

This holds especially true in the tokenized stock space—an early-stage, rapidly accelerating sector—where who leads and who follows is often more honestly revealed by numbers than by narratives.

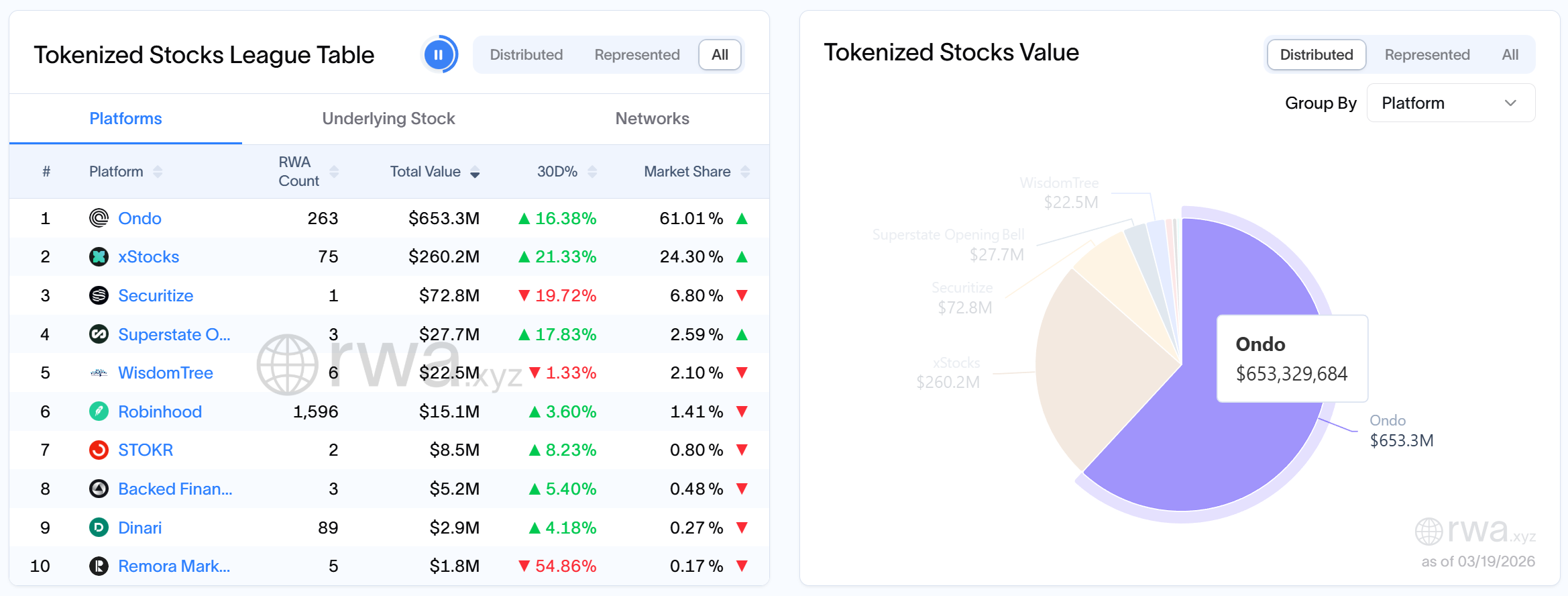

When discussing the competitive landscape of tokenized stocks, many like to describe it as a “duopoly” between Ondo and xStocks. Yet capital volume tells a different story.

According to RWA.xyz, the total onchain value of tokenized stocks has now surpassed $1.07 billion, with Ondo alone accounting for approximately $653 million. Looking back further, we see that as early as January 2026, Ondo’s onchain value of tokenized stocks had already exceeded the combined total of all other platforms—and today, that gap isn’t narrowing; it’s widening.

In terms of market share, Ondo commands over 61% of the tokenized stock market, while second-place xStocks holds 24.65%.

Compared to a “duopoly,” Ondo’s market share—more than 2.47 times larger than its nearest rival—has already established a conspicuously dominant position.

Transaction volume and user metrics offer even sharper contrasts.

Per official data, Ondo’s cumulative trading volume has surpassed $12.7 billion, with peak daily volume reaching $170 million and monthly volume hitting $2.18 billion.

Meanwhile, according to RWA.xyz, among the current ~199,000 token holders across the tokenized stock sector, Ondo hosts 82,900 holders—about 41.7%. While slightly lower than xStocks’ 121,800, Ondo’s 48,600 monthly active addresses exceed xStocks’ 35,200.

These two figures reflect higher-frequency trading and more engaged users—powerfully illustrating that Ondo’s leadership is not merely about “money pooling here,” but about “making the stock market actually happen onchain.”

Even more noteworthy is that this market’s growth remains ongoing:

Per RWA.xyz, Ondo’s user count grew 11.03% over the past 30 days. Maintaining double-digit monthly user growth—even at a 61% market share—means Ondo’s current lead is not a static, completed outcome, but a dynamically accelerating process.

No matter which dimension we examine, the data consistently points in one direction: Ondo is the leader of the tokenized stock market.

Yet data only tells us “how far ahead”—not “why ahead.”

The only certainty is that this multi-dimensional, structural lead is no accidental result of a single product decision; rather, it reflects a complete, coherent strategy.

And that strategy is precisely what deserves unpacking.

Behind the Absolute Center Stage: The “Triple Play” of Asset Coverage, Trading Experience, and Ecosystem Entry Points

Doing tokenized stocks well requires far more than simply moving equities onto the blockchain.

265 Tokenized Stocks Supported—Filling the Onchain Stock Market’s “Shelf”

265—that’s the number of tokenized stocks supported by Ondo, more than any other platform.

These 265 tokenized assets span U.S.-listed companies, Chinese ADRs, energy and commodity-related assets, bonds, index ETFs, and leveraged/inverse ETFs—covering multiple asset classes.

The fuller the shelf, the richer the selection—and the more users can be served, the stronger the reasons to stay.

Faster, Better, Cheaper—Maximizing the Onchain Stock Trading Experience

Of course, once more stocks are brought onchain, the competition shifts to “Why trade stocks here, onchain?”

This is a battle of user experience.

Compared to other platforms, Ondo supports 24/5 trading—meaning users don’t need to stay up late waiting for U.S. market open. Moreover, Ondo offers superior liquidity, tighter spreads, and lower fees: slippage for large trades typically stays below 0.03%, prices closely track Nasdaq in real time, and there are zero minting, redemption, or management fees.

Whether faster, better, or cheaper—each incremental UX improvement hits users’ most sensitive pain points.

All this rests on foundational design work, the most critical element being Ondo’s “wrapped tokenization + instant atomic minting and burning” architecture.

The rationale for wrapped tokenization is straightforward: Under native tokenization, tokens represent legal shares and must be directly recorded on the issuer’s cap table—a slow, legally complex process.

In contrast, wrapped tokenization is more pragmatic and scalable: Tokens are pegged to real-world assets and brought onchain via regulated custodians and mature market infrastructure—no issuer involvement required. Tokens represent claims on underlying shares, held securely by custodians.

Regarding custody risk inherent in the wrapped model, Ondo President Ian De Bode offered a vivid analogy: Stablecoins are, at their core, wrapped tokens.

This sparks an intriguing question: If we’ve already widely accepted stablecoins as a successful “first version” of bringing the U.S. dollar onchain, why shouldn’t we accept the same mechanism for bringing equities onchain?

De Bode’s view is unequivocal: A wrapped model built upon robust legal, custody, and verification frameworks is currently the most effective and scalable method for bringing real-world assets (RWAs) onchain.

The market has, to some extent, already validated this: Ondo’s wrapped model commands 60% market share, while platforms attempting stricter or more native-like token structures hold only single-digit shares.

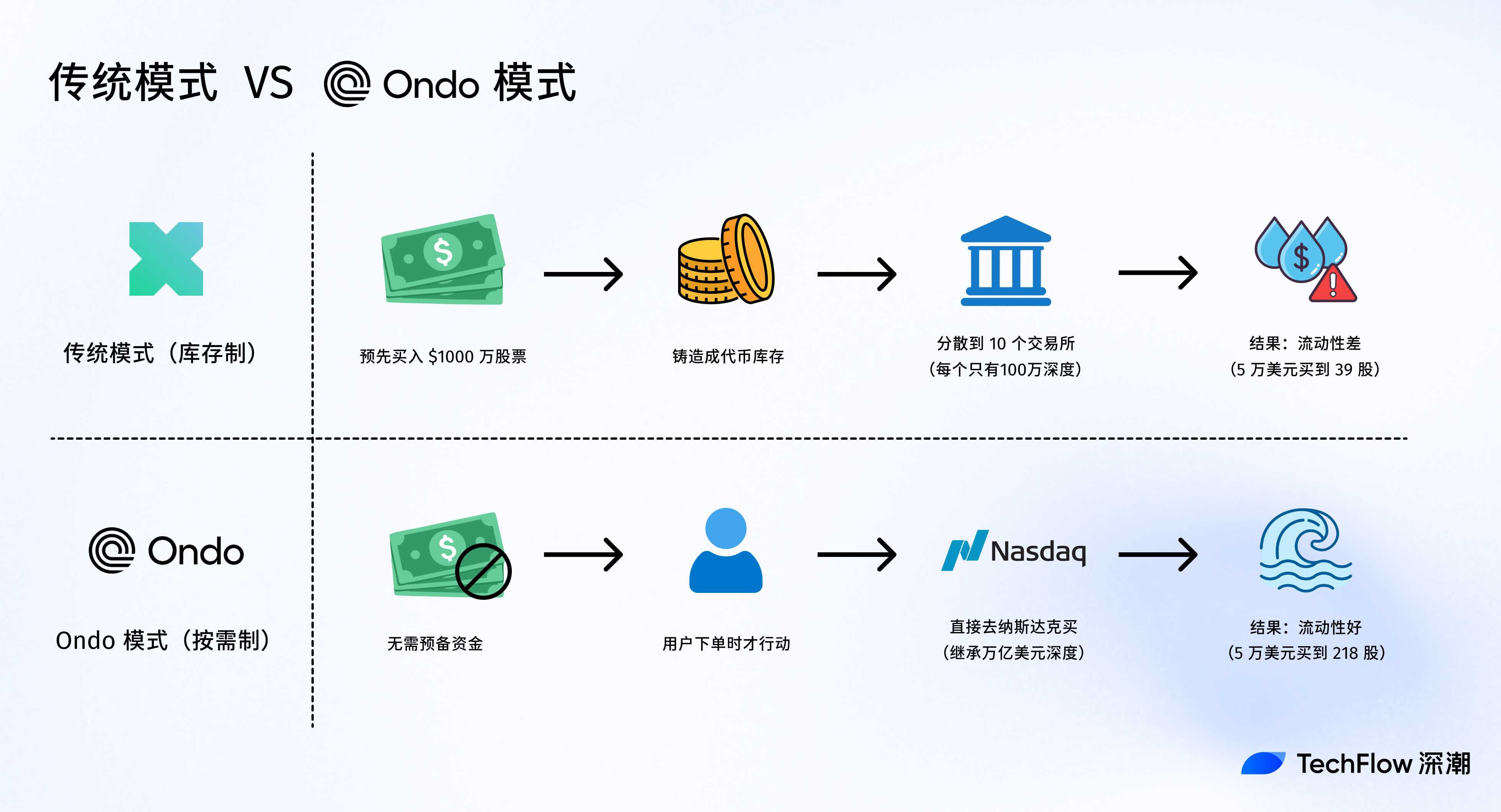

If wrapped tokenization solves “how to bring assets onchain,” then instant atomic minting and burning solves the other critical question: How to enable those assets to trade more efficiently onchain.

Unlike traditional models—which pre-mint inventory and build liquidity themselves—Ondo only purchases the underlying stock and mints its tokenized version when a user places an order.

Once minted, the token is a standard ERC-20, fully transferable 24/7 onchain and composable within onchain finance.

When users sell, Ondo burns the tokens and sells the underlying stock on Nasdaq.

This mechanism elegantly bypasses the clunky “stockpile first, sell later” path of traditional models—giving Ondo two irreplaceable advantages: (1) Stronger liquidity in open markets, directly tapping into trillions of dollars of traditional-market liquidity; and (2) Scalability—since no dedicated capital pool is needed per stock, the platform can easily expand to hundreds or even thousands of equities.

What Matters Even More Than Technology: Securing Entry Points

While “good wine needs no bush,” technology defines a product’s ceiling—distribution determines its growth speed.

Thus, beyond refining technical and product fundamentals, Ondo’s other key move has been forging broad partnerships to embed Ondo tokenized stocks and ETFs deeply into the most frequently used user entry points.

At the wallet layer, Ondo has partnered with leading wallets including MetaMask, Trust Wallet, and Ledger; at the exchange layer, it connects with top-tier platforms like Binance, Bitget, and Gate; in DeFi, it integrates with active protocols such as Morpho, PancakeSwap, and 1inch; and across multichain expansion, Ondo is already live on Ethereum, Solana, and BNB Chain—the user-rich mainstream chains—with future plans to launch Ondo Chain.

The importance of this goes far beyond having an impressive partner list—it fundamentally reshapes user acquisition paths.

When wallets, exchanges, and DeFi protocols all become Ondo distribution channels, users no longer need to seek out Ondo deliberately—they encounter it repeatedly along their existing, familiar usage flows.

Once these entry points are secured, customer acquisition cost, usability barriers, and migration difficulty are all simultaneously rewritten.

Data confirms the strategy’s immediate impact: Whether integrating Solana or partnering with Binance Alpha, each initiative delivered significant uplifts in trading volume and active users. Per official data, since partnering with Ondo in September 2025, 1inch’s aggregated trading volume for tokenized stocks and ETFs has exceeded $2.5 billion.

When breadth of assets, quality of trading experience, and ecosystem-wide accessibility are combined as a strategic “triple play,” Ondo effectively answers users’ three most pressing questions: Is what I want available here? Is it pleasant to buy? And can I use it everywhere?

Because these questions are answered upfront, our analysis of Ondo’s leadership extends beyond deconstructing the present—we also seek clarity on the future.

On the Eve of $150 Trillion in Equities Going Onchain: Ondo’s Narrative of a “New Onchain Asset Infrastructure”

Discussing growth in the tokenized stock market demands looking beyond the chain.

If we focus solely on the present, tokenized stocks are already buzzing: Market size has surpassed $1 billion, discussion热度 is rapidly rising, leading platforms are emerging, and more users are buying familiar U.S. equities and ETFs onchain for the first time.

But consider this: The global equity market’s total market capitalization stands at roughly $150 trillion. Against that backdrop, $1 billion in tokenized stocks looks infinitesimal.

The tokenized stock market is less a fiercely contested arena and more like a superstore whose door has just cracked open.

That, precisely, is where Ondo’s future growth merits dedicated attention.

In a market with less than 0.001% penetration, traditional equity friction—including brokerage commissions, custody fees, foreign exchange losses, T+2 settlement delays, and account-opening hurdles—means as long as onchain stocks consistently outperform traditional pathways across trading hours, cross-border accessibility, settlement efficiency, liquidity orchestration, and usage costs, more users will migrate, and more assets will go onchain.

Here, Ondo’s regulatory progress further accelerates growth: Historically, strict geographic restrictions applied—U.S. citizens and residents were barred from participating. But in November 2025, the SEC concluded its two-year investigation without recommending charges against Ondo. Shortly before that, Ondo announced the acquisition of SEC-registered broker-dealer Oasis Pro Markets—both moves set to accelerate Ondo’s U.S. market development.

Meanwhile, another tailwind stems from Ondo’s undeniable leadership position in the tokenized stock market.

Of course, from a long-term industry health perspective, the community may not welcome prolonged single-platform dominance. Competition is always healthy, and diverse ecosystems foster innovation.

Yet returning to commercial reality and market logic, we must acknowledge: Once a center forms, it rarely yields easily—and Ondo is clearly that center today.

Financial markets have never been arenas of equal traffic or capital distribution—especially in onchain finance, where liquidity depth, brand, trust, and network effects converge, strong “Matthew Effects” inevitably emerge: Users flock to the deepest liquidity pools; capital gravitates toward the most consensus-driven platforms; partners prioritize integration with the player most likely to become foundational infrastructure. Once positive feedback loops take hold, catching up becomes increasingly difficult for newcomers.

Beyond market scale and network effects, a third growth driver deserves special attention: DeFi composability.

In traditional markets, holding a stock grants rights limited to price appreciation, depreciation, and dividends.

But once a stock is tokenized onchain, it ceases to be merely a “tradable asset”—and becomes a “composable asset.”

The difference isn’t one feature—it’s an entire universe of imagination.

You can hold it, trade it, collateralize it, route it through aggregated trading networks, and let it freely seek optimal liquidity and lowest execution costs across platforms. It functions like a building block embedded into the entire financial system—once the underlying interfaces are unlocked, that’s where tokenized stocks may deliver their true, super-leveraged impact.

Ondo’s series of integrations with DeFi projects signals clear recognition of this potential.

For example, via its partnership with 1inch, Ondo tokenized stocks gain enhanced liquidity through aggregation. Similarly, Morpho has confirmed acceptance of Ondo’s stock tokens as collateral—enabling users to borrow against onchain equities in DeFi. This boosts tokenized stocks’ utility, transforming them from isolated assets into interconnected nodes within broader DeFi ecosystems. As more DeFi modules mature, this potential will only amplify.

Any one of these three forces—market scale, network effects, or composability—is sufficient to sustain Ondo’s continued growth.

Should all three materialize concurrently over the coming years, Ondo Global Markets’ narrative may evolve beyond “a tokenized stock platform” into something far more ambitious: the emergence of a new, highly imaginative onchain asset infrastructure.

And that—beyond growth itself—may be the most compelling aspect of Ondo’s future worth watching.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News