Emotion Market Makers: KOLs Generate Toxic Order Flow

TechFlow Selected TechFlow Selected

Emotion Market Makers: KOLs Generate Toxic Order Flow

Information market maker.

Author: Zuoye Web3

The wave of media personalities launching accounts to promote altcoins has subsided; the “saintly fathers and mothers” of the crypto community have also returned their attention to their own “biological sons.”

It appears as if nothing ever happened—media personalities bear no responsibility for the mass dumping of altcoins, nor do exchanges need to answer for the industry’s thoroughly tarnished reputation.

In the public opinion market, KOLs display widespread extremism and clannishness. Behind Kaito’s graceful exit and agencies’ quiet harvesting, “BNB-cheating” participants engage in all-out firefights with everyone else—culminating in an absurd internal war.

Only Noise Remains

Outside information asymmetry and consensus, there remains only noise.

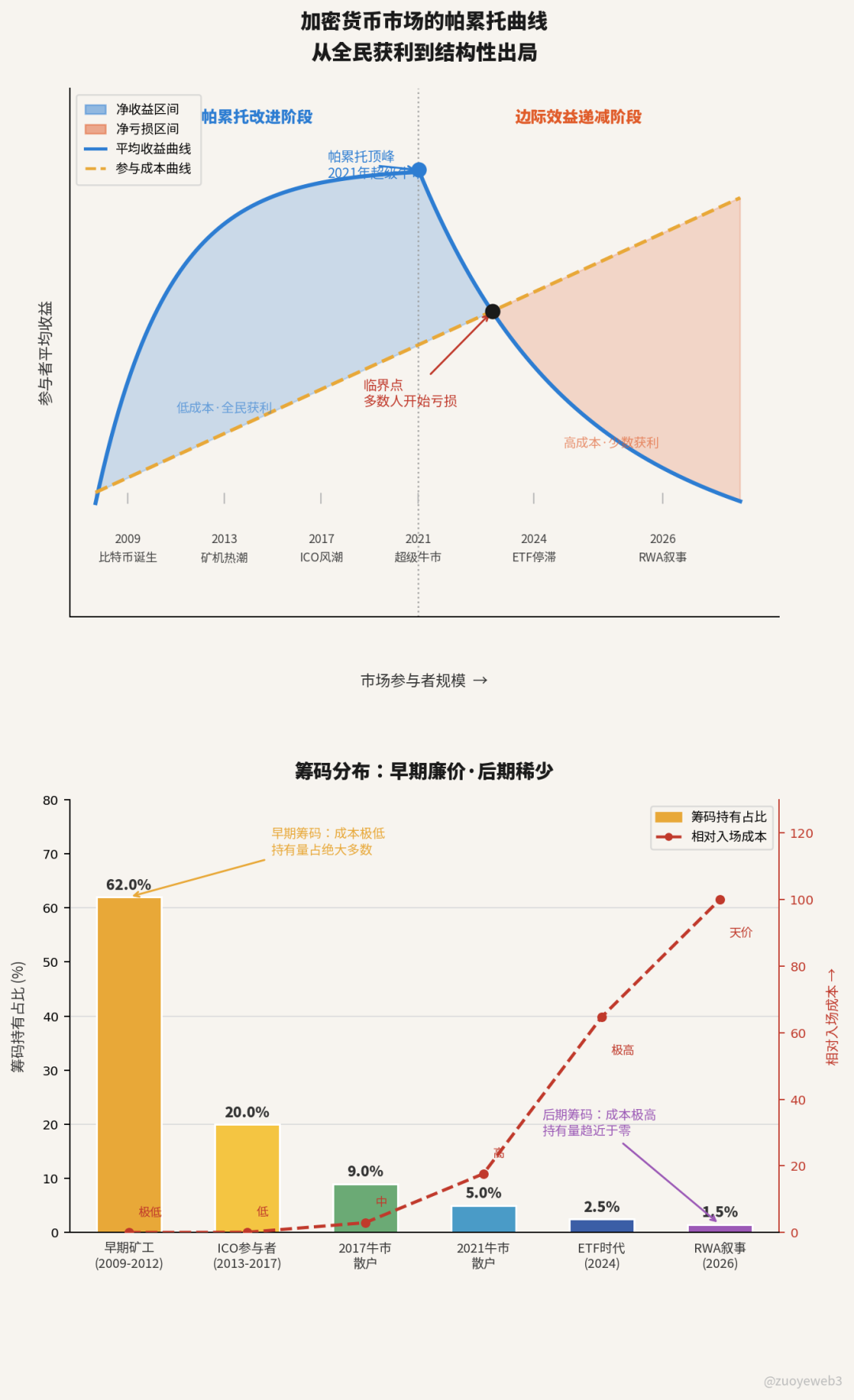

Since Bitcoin’s launch in 2009, cryptocurrency history traces a perfect Pareto curve: early beneficiaries amassed incalculable wealth, while all subsequent actors merely orbit them in cyclical motion.

Caption: The bull-bear cycle has definitively ended.

Source: @zuoyeweb3

Catering to Binance or complaining about OKX’s unfair lottery draws are mere tantrums. Exchanges represent the ceiling for KOL reach; project teams and whales symbolize the sparse population—only briefly bending down to learn during trending moments or executing one-off paid marketing campaigns before token launches.

There is no long-term partnership akin to those between late-stage tech media and major tech firms, nor fertile ground for cultivating industry-level KOLs—you must pick a side.

More seriously, blockchains and stablecoins like USDC/USDT no longer require crypto-media relations; lobbying, capital operations, and political connections outweigh KOL influence.

Mr. Beast is entering FinTech; crypto KOLs can only clumsily study U.S. equities.

Why?

Because information—as a commodity—holds economic value only where information asymmetry and consensus overlap.

- Early miners faced highly controllable input and holding costs relative to buying/selling Bitcoin or Ethereum—akin to early MLM participants who always exit just in time. CZ had already mastered this art during the philatelic and numismatic era.

- Latecomers believe everything in traditional finance will migrate on-chain—but without The Merge or the BTC spot ETF, there’s no mass anticipation; full positions in altcoins await capital spillover that never arrives.

Either you entered early as a miner—the producer—or arrived late as a whale—the rentier. Those who entered mid-cycle can only shout bullish mantras endlessly. As more become KOLs, fewer depart gracefully.

Even Binance-aligned KOLs widely recognized by the market have been turned against by Binance itself—just as Binance discarded its “girlfriend tokens,” token-launch editors, and listing brokers. Giants have begun shedding their periphery, sustaining only mechanical existentialism.

Moreover, AI’s introduction into the crypto opinion market spells disaster.

Interpreting SEC policy, vetting stablecoin issuers’ qualifications, or conducting due diligence on projects demands analytical rigor approaching that of traditional consulting, auditing, or legal professions.

Yet these very industries are themselves undergoing AI-driven displacement—so why not just learn AI directly?

The problem is that AI excels as a professional assistant: skilled programmers treat it as a productivity multiplier, while most others merely build flashy UI tools.

In reality, AI has never enhanced KOLs’ ability to interpret or disseminate expertise—for instance, we see many independent developer KOLs, yet rarely use their products; we consume countless crypto KOL micro-posts, yet our perception of their personal brands continues declining.

Selling information asymmetry has collapsed—from Solana/Aptos’ successive technical advantages as “Ethereum killers” down to the repetitive mantra: “Agents need stablecoins”—as if repeating it proves crypto still has springtime ahead.

Stablecoins, RWAs—these are merely tools within crypto’s utility layer. Without intrinsic asset-sale value, their ultimate valuation converges on SaaS metrics.

By contrast, native crypto assets evoke profound disorientation: everyone knows MegaETH will follow Monad/Scroll into oblivion—but licensed gamblers demand collective performance until the final curtain falls.

In the post-truth era, the crisis isn’t KOLs and media using AI to fabricate falsehoods, nor recommendation algorithms flooding feeds with “digital swill.” Rather, ordinary people’s suffering index runs so high they seek fleeting calm in emotional K-line charts.

There is no “post-truth era”—only garbage time when truth is refused.

Does Du Jun not know BTCFi is a joke? Yet he persists in offloading BTC/ETH L2 projects, retreating into Bitcoin’s inner sanctum.

Superfluidity of Opinion

Who is our enemy? Who is our friend?

Crypto inevitably enters the latter half of the Pareto curve. Time’s arrow cannot reverse; diminishing marginal returns make zero-sum games (“I win, you lose”) unavoidable—abandon all illusions.

For the crypto industry, the free market of opinions holds value only in identifying the next asset possessing “upward-phase” attributes. Studying whether Google is a long-hold investment or whether Bitcoin will dip to $50,000 is meaningless—these assets have already proven themselves across macro timeframes.

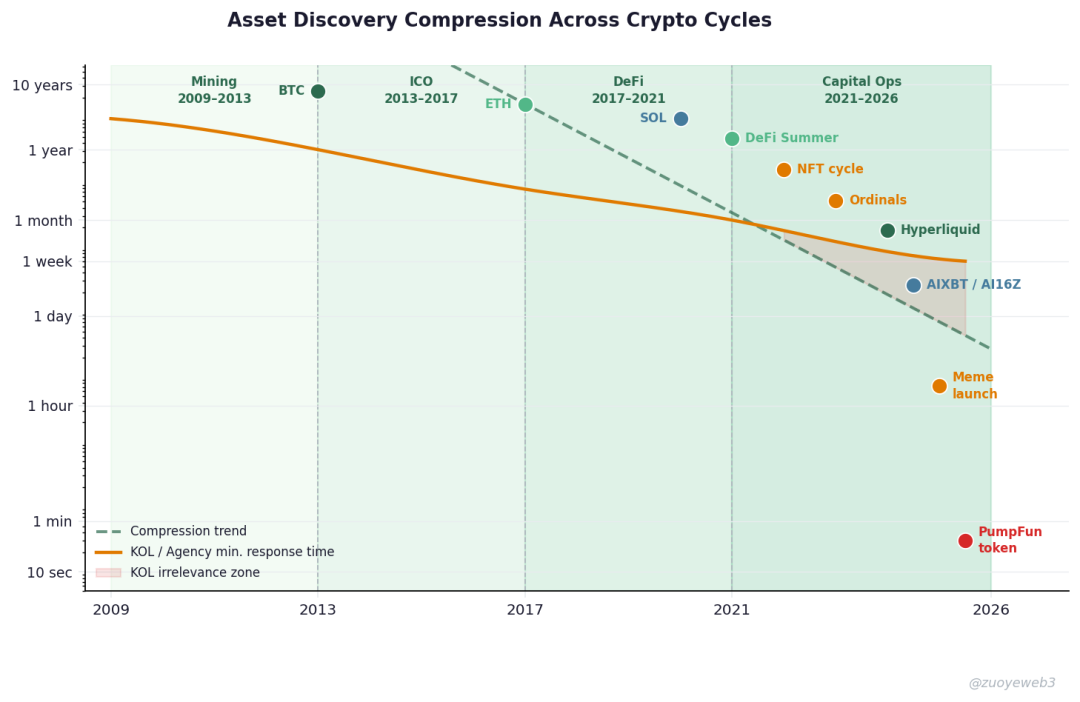

A rigid market structure requires the opinion market to discard the imported concept of “KOL”; “information market makers” is the most fitting designation.

Caption: Asset discovery and information expression cycles

Source: @zuoyeweb3

After technical narratives end, asset narratives fracture from retail purchasing power. U.S. equities and Treasuries must pass through stablecoins and Ondo to enter on-chain narratives. Existing opinion LPs cannot explain such complexity—we must introduce AMM- or CLOB-based opinion markets.

Hyperliquid conducts no marketing, yet traditional platforms (X/Twitter, WeChat, Xiaohongshu) impose algorithmic barriers; PumpFun treats tokens as arcade tokens, ultimately generating extreme-probability ticker movements.

All past paradigms fade: compared with these token issuance models, the opinion market has only evolved to Agency—a manual cooperative—incapable of supporting the next phase of asset discovery: not merely crypto or AI assets, but assets for the next era and the next generation.

If one observes exchange behavior closely, a trend toward “Central Depository” (Zhongdeng)-style institutionalization is already unavoidable.

Their aim is arbitrage across project teams and exchange roles—not entrepreneurship for massive wealth, but executive infighting. Externally, they fail to grasp AI’s industry impact; internally, they neglect user experience enhancement.

Zhongdeng: A creature whose structural superiority—conferred by age and organizational hierarchy—fuels fantasies of commanding others to execute ideas.

Asset holders grow “Lao-deng-ized”; opinion disseminators “Zhong-deng-ize”; only “Xiao-deng” remain bewildered in the wind.

If Perp DEXs are already supplanting CEXs, then replacing today’s information market demands information market makers who understand precisely where to exert effort.

- Retire the old guard: Binance’s “parent-child clique” and Xu Mingxing must step aside, moving to passive holdings to earn industry beta returns.

- Bring in fresh talent: leverage overseas RWA adoption as an opening—finance professionals urgently needed to broker information and capital.

- Reform mechanisms: “Easy Mode” group distribution of project info yields no incremental gains—either discover new assets, or descend into offline MLM.

Our helplessness before AI and confusion about the industry demand founders’ mission—merely brokering exchange-project commercial deals adds zero trading volume.

“Altcoin friends” (crypto media personnel) possess no superior information analysis capability—they rely on media brand inertia. Early-rich “Lao-deng” hold absolute capital advantage but not necessarily superior capital operation skills; scale masks their ineptitude.

Behind Yi Lihua’s collapse, whales liquidated positions; Peter Thiel exited during DAT’s trough—all proving early-mover advantage reigns supreme. You may err repeatedly, yet low-cost early accumulation rescues you again and again.

Under the information market maker framework, any content revolving around current hot topics or figures is merely a clue; submerged currents constitute media’s true excavation zone. If media lacks this discovery capacity, better open Douyin to watch influencers.

Following DeFi’s great path forward, professional market makers must first be AMM-ized before evolving into sophisticated CLOB-based Perp DEXs.

In other words, every individual should treat media as their complementary venture—not KOLs pursuing CPA certification, but CPAs becoming KOLs. The next frontier of information brokering is capital brokering.

Conclusion

Crypto is economic history on a light-year scale.

From universal profit to universal extremism—within just over a decade, money remains unearned while professional shame intensifies daily.

When money becomes engineered stablecoins and AI engineered compute, information must transcend handcrafted labor—only mass participation can trigger capital participation.

The hierarchical structure of few top-tier KOLs and many small retail investors fails to deliver the new-user growth exchanges crave. Hope springs for a super information market maker in 2026.

“Mom and Dad, Love Me Once More” is profoundly abstract—not the child, who merely imitates, but the parents, who bear primary responsibility.

Do not become Wang Lin or Jeffrey Epstein—become the new-era Peter Thiel or Lü Buwei: always hoard the next era’s rare commodity.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News