BackPack Token-to-Equity Swap: A Harsh Self-Rescue Amid the Crypto Winter

TechFlow Selected TechFlow Selected

BackPack Token-to-Equity Swap: A Harsh Self-Rescue Amid the Crypto Winter

BTC halved, IPOs underperformed—crypto exchanges need a new value narrative.

By David, TechFlow

The crypto market has entered winter—BTC’s peak price has been cut in half.

Beyond token prices, another set of figures looks equally bleak: the wave of crypto companies slated for IPOs in 2025 has almost entirely collapsed.

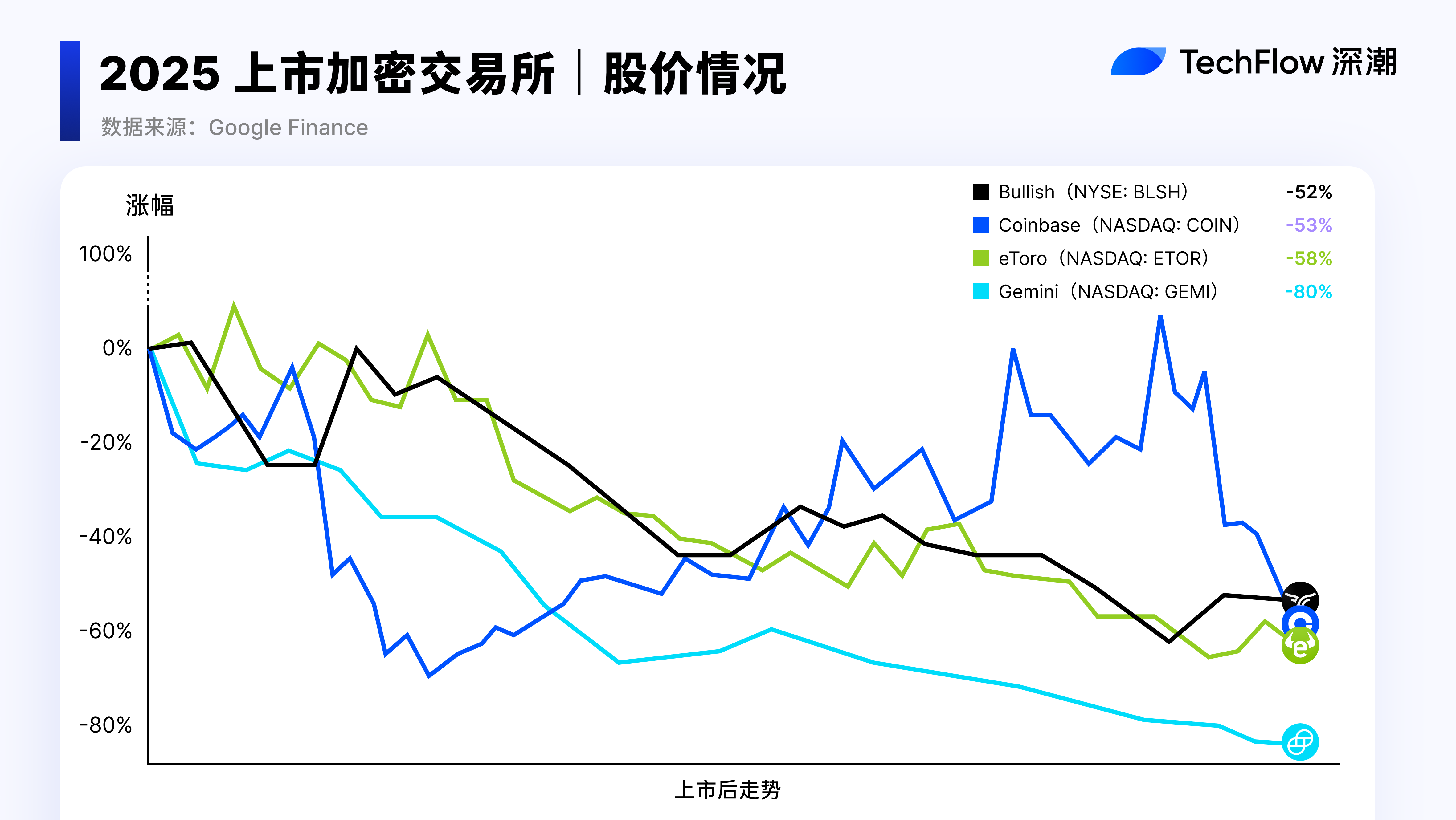

Gemini is down nearly 80% from its IPO price; Bullish, over 52%; eToro, 58%; Circle, 11%. Kraken has already filed its IPO application, with a valuation estimated between $15 billion and $20 billion, and now waits in line.

These crypto exchange companies chose the traditional path: scale revenue, then go public and let the public markets price them—but the public markets’ verdict has been brutally harsh.

Meanwhile, the alternative path hasn’t fared much better.

BNB holds no legal equity stake in Binance; FTT went straight to zero; Coinbase issues no token, yet offers no bridge between its equity and crypto users.

The category of exchange tokens still lacks a satisfactory value anchor.

Last week, Backpack Exchange unveiled a new answer: users who stake its token for one year can redeem it for a fixed percentage of the company’s equity—20% of total equity is reserved for this purpose. This marks the first such initiative in the crypto industry.

What, exactly, does your exchange token anchor to? A discount coupon that shrinks with trading volume—or a share of the company’s intrinsic value?

After the collective IPO failures of crypto firms in 2025, this question has become more urgent than ever.

When Tokens Lead to Equity

Backpack Exchange’s token utility plan, announced on February 23, centers on a single, clear mechanism:

Users who stake the token for one full year may redeem it for company equity at a fixed ratio; currently, 20% of the company’s total equity is allocated to this pool.

CEO Armani Ferrante explained the rationale on X:

“The utility of most tokens is merely a promise. Unless a protocol becomes so decentralized that the team can all retire to the Bahamas sipping coconut water while operations continue uninterrupted, the so-called ‘token value’ is just empty talk.”

That’s blunt—but not exaggerated.

Most exchange tokens derive their value solely from ongoing team operations, yet holders receive no ownership rights. Backpack chose to break that implicit barrier—and grant equity directly.

This scheme hinges on Backpack’s upcoming platform token.

Yet even the token’s official name remains unannounced, and its token generation event (TGE) date is still unconfirmed. Ferrante hinted in the community that it could launch as early as late March. Still, the tokenomics framework has already been published.

Total supply: 1 billion tokens. On day one, 25%—roughly 250 million tokens—will be unlocked, distributed exclusively to points program users and Mad Lads NFT holders.

This initial unlock ratio exceeds the industry norm of 7%–15%. Backpack states its aim is to empower early users to sell freely—not trap them in mandatory lockups.

The remaining 75% is split evenly: 37.5% allocated to users, released gradually across milestones like product launch and regulatory approvals; the other 37.5% goes to the company treasury, locked until after a U.S. IPO—and then locked for an additional year.

The team receives no direct token allocation; instead, they hold company equity, which only becomes liquid post-IPO.

This design carries added significance in a bear market.

Pure utility tokens rise with trading volume in bull markets—and shrink with it in bear markets. BNB’s buyback strength depends on Binance’s profits, which depend on trading volume, which in turn depends on market conditions.

That chain is long—and every link suffers heavy discounting in a bear market.

The equity-linking model attempts to sever that chain.

If tokens can be redeemed for company equity, their value anchor extends beyond platform trading volume to include the company’s overall valuation.

According to Axios, Backpack is currently negotiating a new funding round at a $1 billion pre-money valuation. The 20% equity pool thus implies a theoretical value of $200 million.

Of course, that $200 million is purely paper value. The redemption ratio remains undisclosed; legal documentation is pending; and no IPO timeline has been set. Yet, at least in intent, Backpack has anchored its token to a value source less volatile than token price alone.

This also explains why the plan was unveiled during a bear market.

In bull markets, tokens ride sentiment and trading volume—no one questions what they’re anchored to. In bear markets, the critical question emerges: “My token price has fallen—what is this thing actually worth?”

What It Means for Holders

Token-for-equity conversion—what does the holder actually receive? As of publication, Backpack has outlined the direction but not the details.

Will it be direct equity, stock options, or some form of rights certificate? Will holders have voting rights, dividend rights, or rights to financial disclosures? Backpack says these will be rolled out over the coming weeks—but for now, there’s only one certainty:

You must stake the token for one year.

The crypto industry has seen too many “get on board first, fill in the ticket later” designs—where the final “ticket” often bears little resemblance to the original promise. Until the fine print arrives, that 20% equity pool represents an intention—not a binding contract.

Assuming the final terms prove reasonable, stakers face a second challenge: liquidity.

You trade a highly liquid asset—freely tradable on exchanges—for equity in a private company. That’s a shift from high- to low-liquidity assets.

Private equity lacks a 24/7 open market. To monetize equity, you have only two paths: wait for IPO—or find an off-market buyer.

And IPO is the linchpin of the entire design.

The post-IPO performance of crypto firms in 2025 already shows: IPO ≠ valuation realization. The $1 billion valuation assigned in private markets may diverge sharply from the final public-market pricing. What your equity is ultimately worth depends on the latter—not the former.

What if the IPO is delayed—or never happens?

The team’s tokens remain locked, yes—but your equity gains no exit route. Ferrante himself has acknowledged that an IPO could come quickly, take years—or possibly never materialize.

So for holders, the real choice is stark:

Don’t stake: retain your token, endure price volatility—but preserve liquidity. In a bear market, liquidity itself is the scarcest resource.

Stake for one year: forfeit liquidity—and bet on three conditions aligning: fair redemption terms, successful IPO, and post-IPO valuation holding firm. Miss any one, and the expected return plummets.

If Backpack truly achieves IPO—and sustains its valuation—early stakers could become the first in the industry to obtain genuine corporate equity via tokens.

Valuation Reset in the Bear Market

Every bear market forces crypto to confront hard truths.

The 2018 bear market burst the ICO bubble—most utility tokens went to zero, prompting industry-wide reflection on whether tokens were even necessary. After the 2022 FTX collapse, the focus shifted to transparency and proof-of-reserves.

This cycle poses a more direct question:

When token prices halve from peaks and trading volume shrinks, where does the value anchor for exchange tokens lie?

No one cared during bull markets. But in bear markets, shrinking volume ties token value tightly to short-term platform performance—leaving little resilience across cycles.

Backpack’s equity-linking model—regardless of whether it fully materializes—attempts to answer this question, seeking a value anchor less dependent on trading volume.

Yet this response sits within a deeper dilemma: exchange valuations are undergoing a collective reset.

Prior to 2025, exchange valuations relied largely on trading volume multiplied by a multiple. In bull markets, volume surged—and valuations ballooned. Public markets, however, are increasingly skeptical of this logic.

The sharp post-IPO share price declines of listed exchanges signal a clear message: “Your revenue isn’t sustainable—I won’t price you at peak levels.”

This means both tokens and equity carry inherent cyclical risk when anchored to exchange valuations.

Backpack’s token-equity linkage solves the identity problem—“What does the token represent?”—but not the pricing problem—“What is the exchange actually worth?”

The latter hinges on Backpack’s ability to diversify its revenue model—not rely solely on trading fees.

From a broader perspective, tokenomics across most crypto projects is undergoing a generational shift. At least in bear markets, the industry is being forced to confront a question long overdue: Where should token value truly originate?

Trading Future Equity for Today’s Lifeline

For several years, exchange business models may have grown complacent:

Build a venue, issue a platform token, profit from bull-market liquidity via fees, and symbolically allocate a sliver of profits to buybacks and burns. Users held tokens essentially as patrons of platform prosperity.

The crypto winter shattered that logic entirely.

As retail exits, volume collapses, and even IPO—the “ultimate exit path”—is coldly rejected by public markets, exchanges face a brutal survival test.

In this era of zero-sum competition, the exchange that best locks up users’ remaining capital will be the one to survive into the next cycle.

When vague “token utilities”—like fee discounts or token sale access—fail completely, exchanges must offer something truly consequential to keep users’ funds willingly parked through relentless downtrends: their most valuable asset—equity.

This is a defensive battle—trading your strongest card for time.

For one year, as long as users’ tokens remain staked in Backpack’s pool, the platform’s TVL stays floor-supported, key metrics stay presentable, and the $1 billion valuation narrative remains viable.

You can’t call this generosity—it’s a ruthlessly pragmatic survival strategy: exchanging an option on unlisted company equity for the most precious asset in a bear market—stable, non-outflowing capital.

Backpack’s token-to-equity initiative could mark a turning point in exchange token design—or simply become another bear-market narrative that fails to deliver.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News