How did AI put the entire world into a bubble?

TechFlow Selected TechFlow Selected

How did AI put the entire world into a bubble?

Some profound, irreversible structural changes have quietly taken place amid this clamor.

By: Sleepy.txt

"The only winning move is not to play."

In October, Michael Burry wrote these words on social media. The quote comes from the 1983 film *WarGames*, in which a supercomputer arrives at this conclusion after simulating nuclear war scenarios.

A few days later, Burry disclosed his Q3 holdings. The investor, famous for correctly shorting the 2008 subprime mortgage crisis, had placed nearly 80% of the fund he manages—around $1 billion—in a single direction: shorting Nvidia and Palantir.

In his view, the strongest way to refuse participation in this irrational "long" frenzy was to short it directly.

Burry’s bet is not merely against a few overvalued companies, but against the most powerful consensus of our era. Because within this consensus, AI is not just a technological revolution—it is capital’s new faith.

But how did this consensus form? How was it elevated to its current peak? And as this machine of belief continues to run, what price are we paying for it?

Gospel

Behind every financial mania lies a story that is repeatedly told and widely believed.

In this wave of AI, the narrative has been crafted with textbook precision, co-written by three forces: tech leaders who authored the "myth," Wall Street which provided the "rationality," and the media which carried out the "evangelism."

The first storytellers were prophets of the singularity. Tech leaders like OpenAI CEO Sam Altman and Google DeepMind co-founder Demis Hassabis successfully transformed artificial general intelligence (AGI)—a distant concept once confined to science fiction and academia—into a near-term, tangible "new god" capable of solving humanity’s greatest challenges.

Altman repeats across global speaking tours that AGI will be “the greatest technological leap in human history,” bringing prosperity “far beyond anything we can imagine.” Hassabis frames it in more philosophical terms, describing it as a tool to unlock the universe’s deepest mysteries.

Their language radiates religious fervor toward “future” and “intelligence,” endowing this technological surge with a meaning that transcends commerce—a nearly sacred significance.

If tech leaders provided the myth’s script, then Wall Street and economists offered its “rational” validation.

Against a backdrop of slowing global growth and frequent geopolitical conflicts, AI was quickly anointed as the “growth remedy” that could restore capital’s belief in the future.

In late 2024, Goldman Sachs released a report predicting generative AI would boost global GDP by 7%—about $7 trillion—within a decade. Almost simultaneously, Morgan Stanley labeled AI the “core of the Fourth Industrial Revolution,” with productivity impacts comparable to steam power and electricity.

The real function of such figures and analogies is to transform imagination into assets and belief into valuation.

Investors began to believe that assigning Nvidia a 60x P/E ratio wasn’t irrational—they weren’t buying a chip company, but the engine of the global economy’s future.

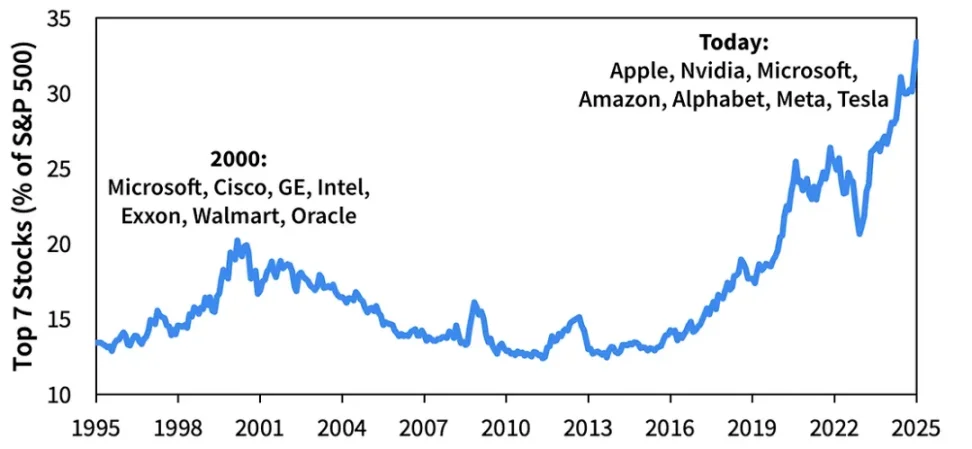

Since ChatGPT’s debut in November 2022, AI-related stocks have contributed 75% of the S&P 500’s returns, 80% of its profit growth, and 90% of capital expenditure growth. This technological narrative has become almost the sole pillar supporting the entire U.S. stock market.

Finally, media and social networks became the ultimate amplifiers of this myth.

From the stunning debut of text-to-video model Sora to every model update from giants like Google and Meta, each event was magnified, recycled, and amplified again—algorithms pushing this faith into every user’s timeline.

Meanwhile, discussions about “AI replacing humans” spread like shadows—from engineers to teachers, designers to journalists—no one could be certain they belonged to the next era.

When fear and awe spread together, a grand, nearly unquestionable creation myth was written—clearing the path for one of the largest capital mobilizations in human history.

Machine

As the “gospel” spreads across the world, a group of financial engineers skilled in structural design began to act.

Their goal: turn this abstract belief into a functioning machine—an intricate, self-reinforcing capital system. It’s less a bubble than a precisely engineered financial engine, far more complex than the derivatives of 2008.

This machine’s core is built by a handful of tech giants. They weave capital, computing power, and revenue into a closed loop—where funds circulate, amplify, and recirculate like an algorithm-driven perpetual motion system.

First, tech giants like Microsoft funnel massive investments into AI research labs such as OpenAI. A company long accustomed to betting on infrastructure during the cloud era, Microsoft has invested over $13 billion into OpenAI. Within a few years, OpenAI’s valuation surged from billions to nearly $100 billion, becoming a new myth in capital markets.

The immediate consequence of this massive funding? More expensive training. To build GPT-4, OpenAI deployed over 25,000 Nvidia A100 GPUs, with next-generation models demanding exponentially more compute. These orders naturally flow to the market’s sole dominant supplier: Nvidia.

Nvidia’s data center revenue jumped from $4 billion in 2022 to $20 billion in 2025, with profit margins exceeding 70%. Its stock soared, making it the world’s most valuable company.

And who holds large stakes in Nvidia? Precisely the same tech giants and institutional investors—including Microsoft. Rising Nvidia shares make their balance sheets even stronger.

The story doesn’t end there. Training is just the beginning; deployment is where the real spending happens.

OpenAI must host its models in the cloud—and its biggest partner is Microsoft. Billions in annual cloud service fees flow into Microsoft’s books, fueling Azure’s growth curve.

A perfect closed loop is born. Microsoft invests in OpenAI; OpenAI buys Nvidia GPUs and Microsoft cloud services; rising revenues at Nvidia and Microsoft push up their stock prices; higher valuations validate Microsoft’s investment success.

Within this cycle, money simply flows between a few giants, yet generates enormous “revenue” and “profit” out of thin air. Booked growth mutually reinforces itself, valuations lift each other. The machine begins to feed itself. It doesn’t need real demand from the real economy to achieve “perpetual motion.”

This core engine quickly expands into every industry.

Fintech and payments were among the first sectors integrated.

Stripe is the most typical example. The payment company, valued at over $100 billion, processed $1.4 trillion in total payments in 2024—equivalent to 1.3% of global GDP. A year later, it announced a partnership with OpenAI to launch a “one-click checkout” feature within ChatGPT, embedding payment systems directly into language model interactions for the first time.

Stripe’s role in this wave is subtle. It is both a buyer of AI infrastructure—constantly purchasing computing power to train anti-fraud systems and recommendation algorithms—and a direct beneficiary of AI commercialization, creating new transaction entry points via integration with language models, thereby boosting its own valuation.

PayPal followed closely. In October 2025, the legacy payment giant became the first wallet system fully integrated into ChatGPT.

But the ripple effect didn’t stop at finance. Manufacturing was among the first traditional industries to feel the shock. Once reliant on automated hardware, it now pays for algorithms.

In 2025, a German automaker announced plans to invest €5 billion over three years in AI transformation, with most funds going toward cloud services and GPUs to rebuild the nervous system of production lines and supply chains. This is no isolated case. Executives in automotive, steel, electronics, and other industries are pursuing similar efficiency gains, as if computing power were the new fuel.

Retail, logistics, advertising—almost every imaginable sector is undergoing a similar shift.

They purchase AI computing power, sign cooperation agreements with model companies, and repeatedly emphasize their “AI strategy” in earnings calls and investor meetings, as if those three letters alone could generate premium value. Capital markets respond accordingly: valuations rise, fundraising becomes easier, narratives grow stronger.

And all roads lead back to the same few companies. No matter which industry the money originates from, it ultimately flows back to core nodes like Nvidia, Microsoft, and OpenAI—toward GPUs, cloud, and models. Their revenues climb steadily, stock prices keep rising, reinforcing the entire AI narrative in a feedback loop.

Cost

Yet this machine is not built from nothing. Its fuel is drawn from real economic and social resources—slowly extracted, converted, and burned into the roar of growth. These costs are often masked by the noise of capital, but they exist—and are quietly reshaping the skeleton of the global economy.

The first cost is opportunity cost of capital.

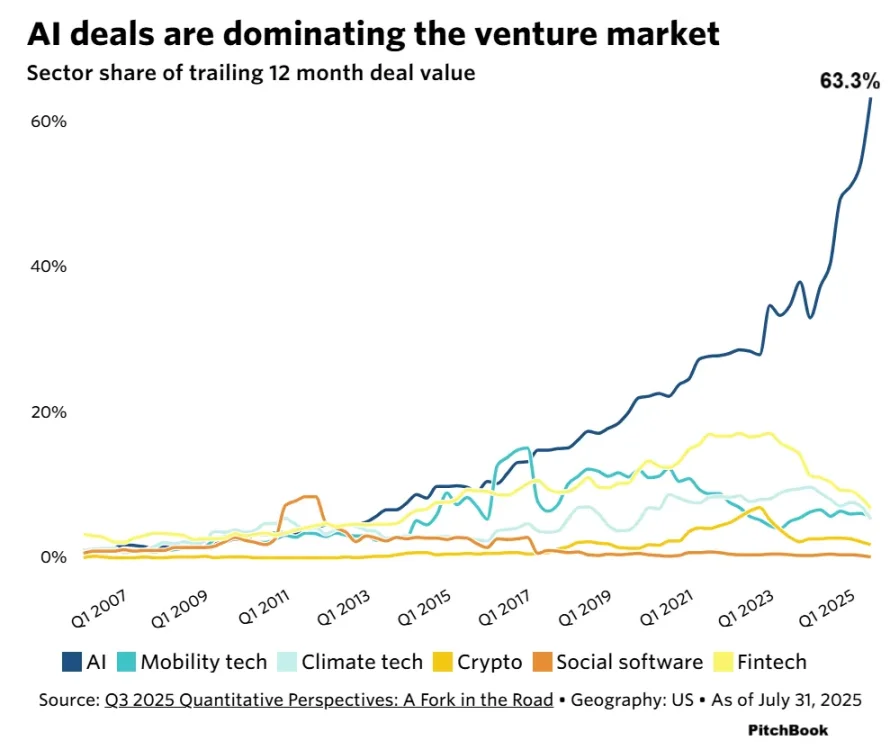

In venture capital, money always chases the highest returns. The AI gold rush has created an unprecedented capital black hole. According to PitchBook, in 2024, about one-third of global venture capital flowed into AI; by the first half of 2025, this share in the U.S. rose to a staggering two-thirds.

This means capital that could have supported climate tech, biotech, clean energy, and other critical fields is being disproportionately siphoned into a single story.

When all the smartest money chases the same narrative, the soil for innovation is hollowed out. Capital concentration does not always mean greater efficiency—it often means the loss of diversity.

In 2024, global VC investment in clean energy totaled only one-fifth of that in AI. Climate change remains humanity’s most urgent threat, yet capital flows instead toward compute and models. Biotech faces the same fate. Multiple founders have said in interviews that investors show little interest in their research because “AI’s story is sexier, with shorter return cycles.”

This capital frenzy is approaching a dangerous tipping point.

Capital expenditure growth in the U.S. tech sector now nearly matches the peak of the 1999–2000 dot-com bubble. Back then, everyone talked about the “new paradigm,” companies expanded before turning profits, and investors raced to back visions of “changing the world.” Then the bubble burst, Nasdaq lost two-thirds of its value, and Silicon Valley entered a long winter.

Twenty-five years later, the same sentiment flares again—only this time, the protagonist is AI. Capital expenditure curves are rising sharply once more, as giants pour tens of billions into data centers and compute clusters, as if spending itself could guarantee the future.

The historical parallels are unsettling. The outcome may not repeat exactly, but such extreme capital concentration means that when a turning point comes, the cost will be borne by society as a whole.

The second cost is intellectual cost—the brain drain.

This AI boom is triggering an unprecedented global intellectual siphon. The world’s top engineers, mathematicians, and physicists are being pulled away from solving fundamental human problems and funneled into a single direction.

In Silicon Valley, the scarcest resource today isn’t capital, but elite scientists in large model teams. Companies like Google, Meta, and OpenAI offer salaries that dwarf those in any other scientific or engineering discipline.

Industry data shows an experienced AI research scientist can easily earn over $1 million annually—while a top physics professor in a university lab earns less than a fifth of that.

Behind this pay gap lies a shift in focus. The world’s brightest minds are withdrawing from long-term fields like basic science, energy innovation, and biological research, converging instead on a highly commercialized track. Knowledge has never flowed faster—but the channels it flows through are narrowing.

The third cost is strategic cost to industries.

Caught in the AI wave, nearly every traditional company now suffers from passive anxiety. They’re forced into this costly AI arms race—spending heavily, building AI teams—despite lacking clear ROI roadmaps.

According to Dell’Oro Group, global data center capital expenditure in 2025 is projected to reach $500 billion, most of it AI-related. Amazon, Meta, Google, and Microsoft alone plan to spend over $200 billion. But this investment frenzy has long spilled beyond the tech sector.

A major retail company announced in its earnings call that it would spend tens of millions over the next three years on AI compute to optimize recommendation and inventory systems.

Yet according to MIT research, the vast majority of such projects yield returns insufficient to cover costs. For these firms, AI is not a tool—it’s a statement. Often, such investments stem not from strategic intent, but from fear of being left behind.

Shift

However, viewing this AI wave solely as a financial bubble and misallocation of resources is too narrow. Regardless of whether market tides rise or fall, profound, irreversible structural changes have already taken place amid the noise.

“Intelligence”—and the compute that drives it—is replacing traditional capital and labor as the new foundational factor of production.

Its status is akin to electricity in the 19th century or the internet in the 20th—irreversible and indispensable. It is quietly infiltrating every industry, rewriting cost structures and competitive dynamics.

Total weight of the top 7 stocks in the S&P 500 at each point in time | Source: Sparkline

The race for computing power has become this era’s oil race. Control over advanced semiconductors and data centers is no longer just an industrial competition—it is central to national security.

The U.S. CHIPS Act, EU technology export bans, and policy subsidies across East Asia have formed a new front in geoeconomic warfare. A global race for compute sovereignty is accelerating.

At the same time, AI is setting a new baseline for every industry.

Whether a company has a clear AI strategy has become key to earning capital market trust and surviving future competition. Whether we like it or not, we must learn to speak the language of AI—it is the new business grammar, the new rule of survival.

Michael Burry isn’t always right—he has been wrong many times in the past decades. This bet may prove his foresight once again, or it may cast him as a tragic figure discarded by the times.

But regardless of the outcome, the world has been permanently changed by AI. Compute has become the new oil. AI strategy is now a mandatory question for corporate survival. Global capital, talent, and innovation are all converging in this direction.

Even if the bubble bursts and the tide recedes, these changes won’t disappear. They will continue to shape our world, becoming the irreversible foundation of this era.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News