The subtle signs of a bull market's end: "the fattest part of the bull's tail" and universal bullish sentiment

TechFlow Selected TechFlow Selected

The subtle signs of a bull market's end: "the fattest part of the bull's tail" and universal bullish sentiment

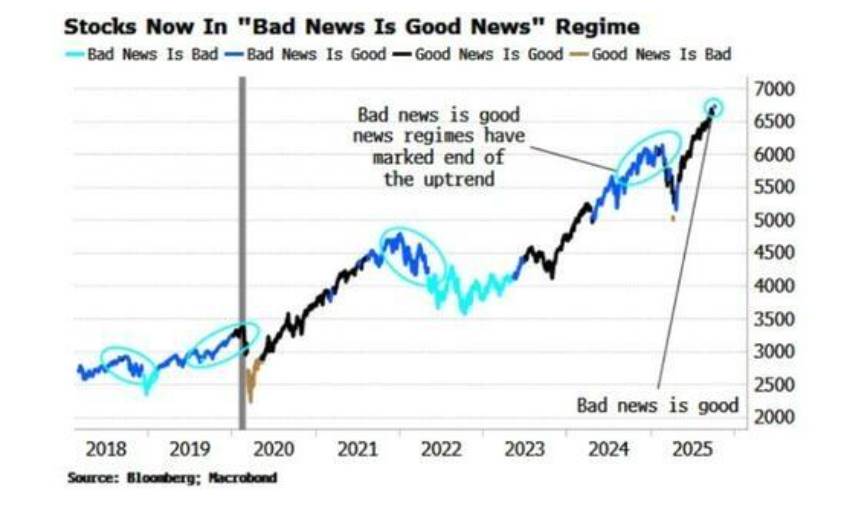

The danger signal of "bad news is good news."

By Long Yue

This Friday, U.S. stocks crashed across the board, with the Nasdaq plunging over 3%—its worst drop in six months—sending alarm bells through the market.

Is the bull run nearing its end? Legendary Wall Street investor Paul Tudor Jones recently warned that while markets may still see a strong rally, they are now entering the final stage of the bull cycle. He believes gains will be front-loaded, followed by a sharp reversal.

This pattern is the common fate of all speculative market phases and "melt-ups." The "melt-up" phase typically brings the highest returns alongside extreme volatility, signaling that risks are rapidly accumulating.

Market psychology may already be growing fragile. Veteran investor Leon Cooperman, citing warnings from Warren Buffett, noted that when markets reach a point where every strategy generates profits, behavior shifts from rational investing to "fear of missing out" (FOMO). In his view, the current rally has detached from fundamental supports like earnings or interest rates and is driven purely by price momentum itself.

More alarmingly, according to Bloomberg analyst Simon White, markets have entered a dangerous mode where "bad news is good news." In this phase, weak economic data actually fuels stock market gains, as investors bet the Fed will ease monetary policy in response. This anomaly has appeared before each of the past major market peaks.

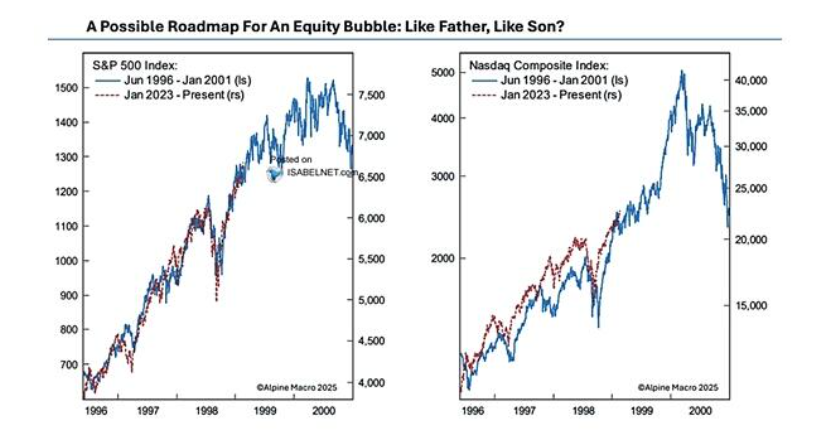

The final狂欢? History eerily echoes 1999

The current market environment bears striking similarities to the dot-com bubble of 1999. Paul Tudor Jones points out that the final year of a bull market often delivers the most impressive returns, but also comes with heightened volatility.

As analyzed by RealInvestmentAdvice.com, at the core of every bubble lies a narrative. In 1999, it was the internet; in 2025, it's artificial intelligence—both offering transformative visions for industries and explosive productivity growth.

This similarity extends to investor psychology. Back then, FOMO drove investors into the market, pushing companies like Cisco to price-to-earnings ratios exceeding 100x. Today, the narrative—"if AI will change everything, you must own it"—is driving identical behavior.

Although ample liquidity, large fiscal deficits, and global central bank rate cuts continue to support the bull market, these very factors are also sources of instability. When nearly all asset classes—from large-cap stocks to gold and Bitcoin—hit record highs and become highly correlated, a reversal could trigger a chain reaction.

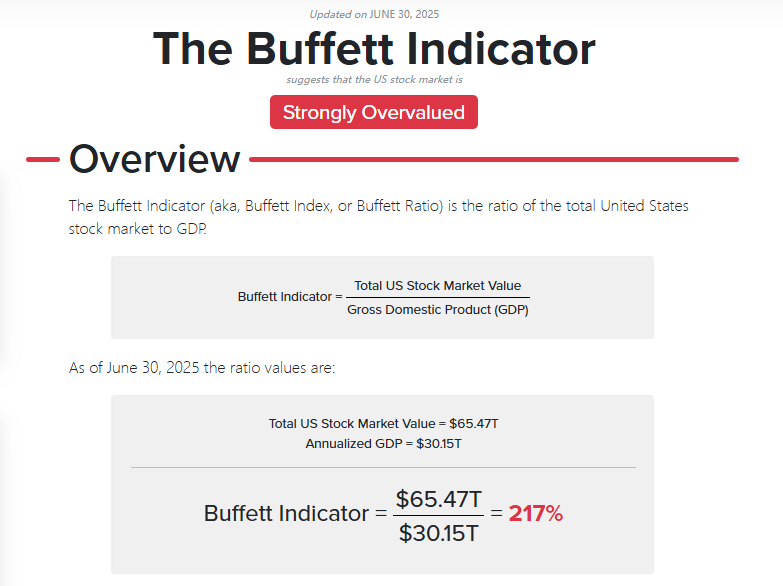

"Buffett Indicator" flashing red and narrative risk

Risks quietly build when markets are driven by narratives rather than fundamentals. Leon Cooperman warns that investors are buying simply because prices are rising—a behavior he says “never ends well.”

The “Buffett Indicator,” which measures total market capitalization relative to GDP, has surpassed 200%, exceeding all previous historical extremes and suggesting a severe disconnect between the stock market and the real economy.

The danger lies in the fact that when everyone constructs a “rationalizing narrative” for their rising assets, consensus becomes dangerously crowded. As investment master Bob Farrell put it: “When all the experts agree, something else is about to happen.”

Currently, nearly all investors expect prices to keep rising. Such one-way positioning makes the market extremely sensitive to even minor negative news, potentially triggering an outsized reaction.

The danger signal of "bad news is good news"

According to Bloomberg’s Simon White, the market’s shift into the "bad news is good news" mode is a key sign that a top is forming. Investors ignore signs of economic slowdown and instead cheer, anticipating Fed intervention. Historical data shows this mechanism preceded each of the last three major market tops, as well as peaks in 2011 and 2015.

However, the analysis offers two caveats. First, this mechanism can persist for months before a true correction occurs.

Second, in the past two decades, such patterns have also emerged during mid-bull market phases.

Yet given the current overinvestment in AI, record-high valuations, and growing speculative bubbles, no one dares to claim this is merely a "mid-game break."

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News