Starting with Mystonks: Unveiling the "U.S. Compliance" Marketing Trap of Crypto Platforms

TechFlow Selected TechFlow Selected

Starting with Mystonks: Unveiling the "U.S. Compliance" Marketing Trap of Crypto Platforms

What is the truth behind these so-called "compliant" qualifications?

Recently, a so-called "U.S. stock tokenization" platform named Mystonks has sparked widespread controversy by freezing user funds. It is reported that the platform withheld substantial assets on the grounds of "non-compliant fund sources."

From a financial compliance perspective, this approach is highly unusual. When a legitimate financial institution identifies suspicious funds, the standard procedure is to reject the transaction and return the funds along their original path, while simultaneously filing a report with regulators. The platform's direct "withholding" of assets casts serious doubt on its claimed "compliance."

Mystonks has consistently promoted itself around two key points: holding a U.S. MSB license and conducting compliant STO offerings. But what is the truth behind these so-called "compliant" credentials? I conducted an investigation.

1. The Truth Behind "Compliant STO": Filing Does Not Equal Authorization, Private Placement Does Not Equal Public Offering

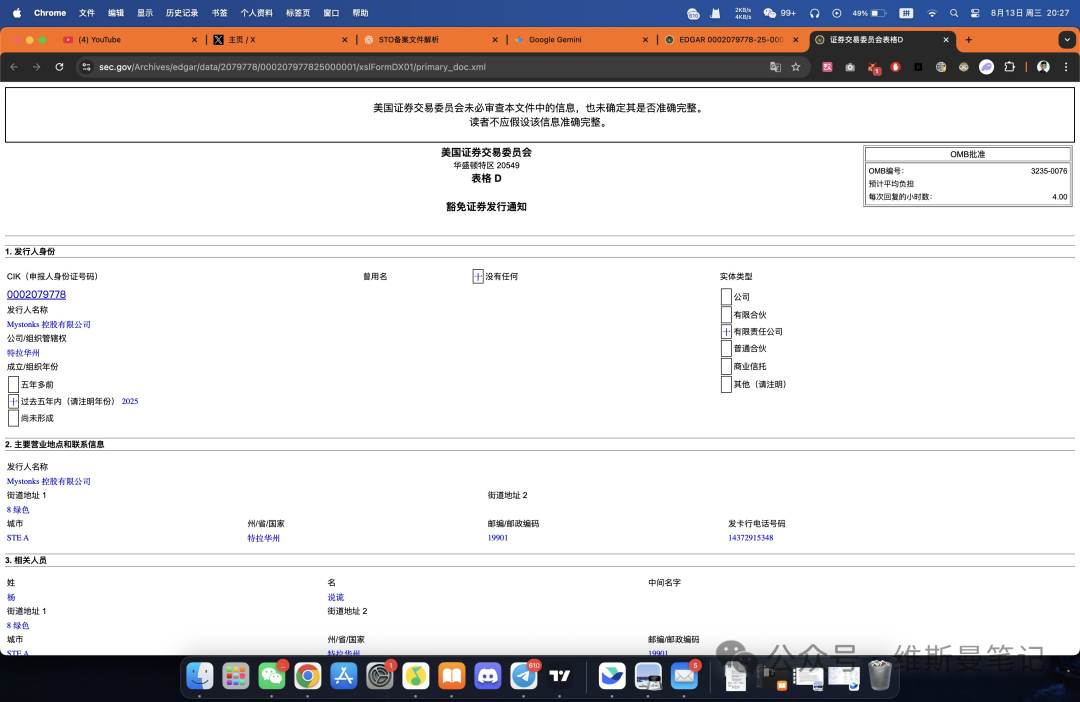

In my research, I found that Mystonks' claims are not entirely baseless. In the public database of the U.S. Securities and Exchange Commission (SEC), registration information for Mystonks Holding LLC can indeed be found.

The key points of this document (Form D) are as follows:

● Type of filing: Private placement exemption under Regulation D Rule 506(c).

● Target investors: Limited exclusively to "Accredited Investors."

● Offering size: $575,000, with a minimum investment threshold of $50,000.

This very document is the crux of the issue—and where the platform’s marketing is most misleading.

First, Form D is a notification filing, not an operating license. It merely indicates that the company has informed the SEC of a private offering; the SEC archives it without reviewing or endorsing the company's qualifications or the legitimacy of the project.

Second, and most importantly, the filing strictly limits the investor pool. Regulation D is a private placement exemption designed for a small number of qualified wealthy individuals or institutional investors ("Accredited Investors"). Yet Mystonks operates as a publicly accessible trading platform whose vast majority of users clearly do not meet this criterion.

Therefore, Mystonks’ conduct amounts to using a filing intended solely for limited fundraising from a small group of wealthy individuals to publicly engage in securities trading activities—which require rigorous licensing.

This practice essentially exploits ordinary investors’ unfamiliarity with U.S. securities regulations through conceptual confusion. To legally offer security token trading services to the public, a platform must hold advanced licenses such as an **ATS (Alternative Trading System)** or **Broker-Dealer** license—credentials that are worlds apart from a simple Form D filing.

2. The Misused MSB License: An "Anti-Money Laundering" Filing With No Connection to Fund Safety

Having discussed the relatively complex STO issue, let’s now turn to the more commonly used marketing tool—the U.S. MSB license.

Investors need to understand one core fact about the MSB license: its value and significance are severely overstated by many projects in the market.

The regulator overseeing MSB (Money Services Business) is FinCEN, a bureau of the U.S. Department of the Treasury, whose primary mission is anti-money laundering (AML). This means FinCEN only cares whether platforms report suspicious transactions to combat financial crime. It does not ensure user fund safety, review business models, or assess technical capabilities.

More importantly, the barrier to obtaining an MSB registration is extremely low. Through third-party agencies, it can be easily completed remotely from overseas—even without establishing a physical office in the U.S. As a result, it has become the go-to instrument for many projects to cheaply and quickly "package" themselves as compliant.

When a platform primarily serving non-U.S. users repeatedly emphasizes its MSB license, investors should realize this is largely a marketing tactic, not proof of strong financial credibility.

Conclusion: Understanding the "Compliance" Playbook Through the Case of Mystonks

The Mystonks case is not isolated. It clearly reveals the common "compliance" packaging tactics used by certain platforms operating in gray areas. Across the market, numerous exchanges and financial platforms are reusing similar scripts, and investors need clear awareness of this reality.

The typical playbook of such platforms can be summarized as follows:

1. Step One: Use the MSB license as a marketing "foot-in-the-door." Leveraging its "official U.S." association and low acquisition cost, they quickly build a superficially credible image.

2. Step Two: Misrepresent securities filings through "concept substitution." They repackage limited filings with strict conditions—such as private placement notifications—as comprehensive operating licenses permitting public service offerings, deeply misleading investors through information asymmetry.

3. Step Three: Conduct "precision marketing" by exploiting jurisdictional and legal differences. Knowing full well their operations cannot legally launch within the U.S., they specifically target overseas users unfamiliar with U.S. regulations, creating a "blooming outside the wall" phenomenon.

As investors, we must learn from these tactics. When assessing whether a platform is truly compliant, remember two fundamental principles:

● Real compliance is expensive and tangible. It involves high licensing fees, capital reserves, physical office leases, and local legal team expenses. Any "compliance" that is easily obtained and intangible is inevitably of little value.

● Real compliance is transparent and specific. It openly discloses the exact license type, number, regulatory scope, and limitations. Vague, generalized claims of "compliance" almost always collapse under scrutiny.

In making investment decisions, strip "compliance" of its marketing veneer and treat it as a legal fact requiring rigorous examination. Upholding this底线, you can best safeguard your assets.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News