Bullish, emerging from EOS, officially moves toward listing on the New York Stock Exchange

TechFlow Selected TechFlow Selected

Bullish, emerging from EOS, officially moves toward listing on the New York Stock Exchange

The pioneer of Bitcoin treasury reserves, earned $14 billion.

By: Peggy, Jaleel Jia Liu

On July 19, 2025, according to CNBC, Bullish has officially filed IPO documents with the U.S. Securities and Exchange Commission (SEC), planning to list on the New York Stock Exchange under the ticker symbol "BLSH." This marks another crypto company entering the U.S. stock market following Circle and Coinbase.

According to its prospectus, as of the first quarter of 2025, Bullish's cumulative trading volume reached $1.25 trillion, with an average daily trading volume exceeding $2.5 billion in Q1. Bitcoin trading volume amounted to $108.6 billion, a 36% year-on-year increase.

Bullish is not a well-known name in the highly profitable CEX sector of the crypto industry, but in fact, its origins are extremely prestigious.

In 2018, EOS emerged out of nowhere, claiming to be the "Ethereum killer." Its parent company, Block.one, rode this wave to conduct the longest and highest-funded ICO (Initial Coin Offering) in history, raising a staggering $4.2 billion.

Years later, after the EOS hype faded, Block.one pivoted to launch a new venture focused on compliance and targeting traditional financial markets—a cryptocurrency exchange called Bullish—prompting backlash from the EOS community, which effectively expelled Block.one.

Bullish officially launched in July 2021. Initial funding included $100 million in cash, 164,000 bitcoins (worth about $9.7 billion at the time), and 20 million EOS tokens from Block.one. External investors added $300 million, including PayPal co-founder Peter Thiel, hedge fund magnate Alan Howard, and prominent crypto investor Mike Novogratz.

Pro-Circle, Anti-Tether: Bullish’s Commitment to Compliance

Bullish’s positioning has always been clear: scale isn’t critical, but compliance is.

This is because Bullish’s ultimate goal isn’t maximizing profits within the crypto world, but becoming a legitimate, publicly listed financial platform.

Prior to full operations, Bullish entered into an agreement with public company Far Peak, investing $840 million to acquire a 9% stake and pursuing a $2.5 billion merger to achieve a backdoor listing, thereby lowering the barriers of a traditional IPO.

At the time, media reports valued Bullish at $9 billion.

Thomas, the former CEO of Far Peak—the company being acquired—is now Bullish’s current CEO, bringing strong compliance credentials: previously Chief Operating Officer and President of the New York Stock Exchange, where he excelled; built deep relationships with Wall Street giants, CEOs, and institutional investors; and holds extensive resources in regulatory and capital circles.

Notably, while Farley hasn't made many external investments or acquisitions through Bullish, several high-profile ones stand out in the crypto space: Babylon (a Bitcoin staking protocol), ether.fi (a restaking protocol), and blockchain media outlet CoinDesk.

In short, Bullish is perhaps the crypto exchange most eager to become a "legitimate Wall Street player."

But ideals are lofty, reality is harsh. Compliance proved far more difficult than anticipated.

With increasingly tough U.S. regulatory scrutiny, Bullish’s original merger-based listing plan was terminated in 2022, ending an 18-month effort. Bullish also considered acquiring FTX for rapid expansion, but the deal never materialized. As a result, Bullish had to seek alternative compliance pathways—such as expanding into Asia and Europe.

Bullish at Hong Kong Consensus Conference

Earlier this year, Bullish obtained Type 1 (dealing in securities) and Type 7 (providing automated trading services) licenses from the Hong Kong Securities and Futures Commission, along with a virtual asset trading platform license. Additionally, Bullish secured licenses from Germany’s Federal Financial Supervisory Authority (BaFin) for crypto asset trading and custody.

Bullish has approximately 260 employees globally, with over half based in Hong Kong, and the rest distributed across Singapore, the United States, and Gibraltar.

Another clear sign of Bullish’s “commitment to compliance” is its alignment with “Circle” and distance from “Tether.”

On the Bullish platform, the top stablecoin trading pairs by volume are all USDC, rather than USDT, which has a larger circulation and longer history. This reflects a clear stance on regulatory alignment.

In recent years, as USDT faces increasing regulatory pressure from the U.S. SEC, its market dominance has begun to waver. In contrast, USDC, a stablecoin jointly launched by compliant firms Circle and Coinbase, not only successfully went public on U.S. markets but has also gained favor as the “first stablecoin stock,” delivering strong stock performance. Thanks to its transparency and regulatory compatibility, USDC’s trading volume continues to surge.

According to Kaiko’s latest report, USDC’s trading volume on centralized exchanges (CEX) rose significantly in 2024, reaching $38 billion in March alone—far surpassing the monthly average of $8 billion in 2023. Among these, Bullish and Bybit are the two largest platforms for USDC trading, collectively capturing around 60% of the market share.

The Love-Hate Relationship Between Bullish and EOS

If one sentence could describe the relationship between Bullish and EOS, it would be: the ex and the new partner.

Although the price of A (formerly EOS) surged 17% after rumors surfaced that Bullish had secretly submitted an IPO application, the truth is that relations between the EOS community and Bullish have been poor ever since Block.one abandoned EOS and embraced Bullish instead.

Back in 2017, the public blockchain sector was in its golden era. Block.one released a white paper introducing EOS—a so-called superchain promising “one million TPS and zero fees”—which instantly attracted global investors. Within a year, EOS raised $4.2 billion via ICO, setting an industry record and igniting dreams of an “Ethereum killer.”

But just as quickly as the dream began, it collapsed. After the EOS mainnet launched, users quickly discovered the chain wasn’t as “invincible” as advertised. While transactions didn’t require fees, they required staking CPU and RAM, making the process complex and user-unfriendly. Node elections weren’t the “democratic governance” envisioned but were soon dominated by whales and exchanges, leading to vote-buying and vote-pooling issues.

However, what truly accelerated EOS’s decline wasn’t just technical shortcomings, but internal resource allocation problems at Block.one.

Block.one originally promised to allocate $1 billion to support the EOS ecosystem, but in practice did the opposite: it invested heavily in U.S. Treasury bonds, hoarded 160,000 BTC, poured money into failed ventures like the social app Voice, and used funds for stock trading and domain purchases—leaving almost nothing for actual EOS developers.

Meanwhile, power within the company was highly centralized, with key executives almost entirely composed of Block.one founder BB and his relatives and friends, forming a tight-knit “family business.” In 2020, BM announced his departure from the project, foreshadowing the complete split between Block.one and EOS.

What truly ignited outrage in the EOS community was the emergence of Bullish.

BB, Founder of Block.one

In 2021, Block.one announced the launch of the crypto exchange Bullish, claiming to have already secured $10 billion in funding backed by elite investors such as PayPal co-founder Peter Thiel and Wall Street veteran Mike Novogratz. The new platform emphasized compliance and stability, aiming to serve as a “bridge” for institutional investors into crypto finance.

Yet this Bullish had virtually no connection to EOS—neither using EOS technology nor accepting EOS tokens, denying any association, and offering not even basic gratitude.

To the EOS community, this was nothing short of a public betrayal: Block.one used resources built on EOS to launch a “new love,” leaving EOS completely behind.

Thus, resistance from the EOS community began.

By the end of 2021, the community launched a “fork uprising,” attempting to cut off Block.one’s control. The EOS Foundation stepped forward as a community representative to negotiate with Block.one. Over the course of a month, multiple proposals were discussed, but no agreement was reached. Ultimately, the EOS Foundation teamed up with 17 nodes to revoke Block.one’s authority and remove it from EOS’s management. In 2022, the EOS Network Foundation (ENF) filed a lawsuit accusing Block.one of breaking its ecosystem commitments. In 2023, the community even considered a hard fork to fully isolate Block.one and Bullish assets.

After the split between EOS and Block.one, the EOS community engaged in years-long legal battles over ownership of the raised funds, though Block.one still retains control and usage rights to the funds to this day.

Therefore, in the eyes of many in the EOS community, Bullish is not simply a “new project,” but a symbol of betrayal—one that turned their idealism into cold reality. This Bullish, quietly filing for IPO, remains that shiny yet shameful “new lover.”

In 2025, EOS rebranded to Vaulta to distance itself from its past, building Web3 banking services atop its blockchain, and simultaneously renamed its token from EOS to A.

Just How Rich Is Block.one?

We know that early on, Block.one raised $4.2 billion, marking the largest fundraising event in crypto history. In theory, this sum could have sustained long-term development of EOS, supported developers, driven technological innovation, and nurtured ecosystem growth. Yet when EOS developers pleaded for funding, Block.one offered only a $50,000 check—less than two months’ salary for a Silicon Valley programmer.

“Where did the $4.2 billion go?” the community asked.

An email from BM to Block.one shareholders dated March 19, 2019, revealed part of the answer: as of February 2019, Block.one’s total assets—including cash and invested funds—amounted to $3 billion. Of this, approximately $2.2 billion was invested in U.S. government bonds.

So where did the $4.2 billion ultimately go? Broadly speaking, three directions: $2.2 billion in U.S. Treasuries—low risk, steady returns, ensuring wealth preservation; 160,000 BTC; and minor stock investments and acquisition attempts, such as the failed Silvergate investment and purchase of the Voice domain.

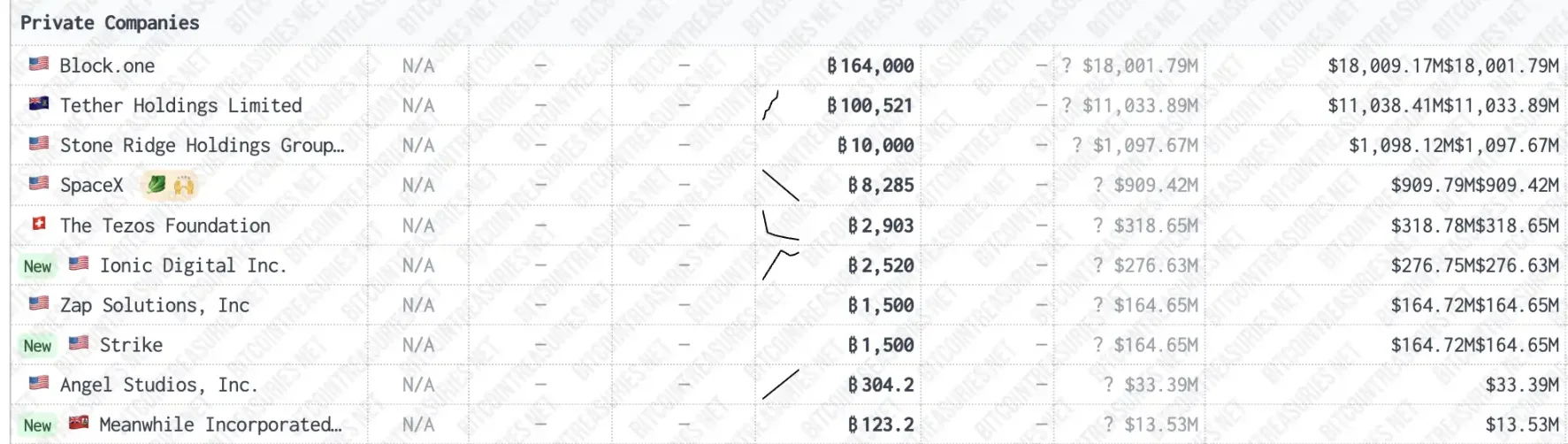

What many don’t realize is that Block.one, the parent company of EOS, is currently the private company holding the largest amount of Bitcoin—160,000 BTC, 40,000 more than stablecoin giant Tether.

Data source: bitcointreasuries

At the current price of $117,200, this 160,000 BTC is worth approximately $18.752 billion. This means Block.one has made over $14.5 billion in paper gains from Bitcoin alone—about 4.47 times its original ICO funding.

From a “cash is king” perspective, Block.one today is undeniably successful—even more “forward-thinking” than MicroStrategy—and stands among the most profitable “project teams” in crypto history. Only, its success didn’t come from “building a great blockchain,” but from “how best to preserve principal, grow assets, and exit gracefully.”

This is another ironic and truthful side of the crypto world: in this space, the one who wins in the end may not be the one with the best technology or brightest ideals, but the one who best understands compliance, reads the room, and knows how to hold onto money.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News