Pilot Programs Outweigh Demand: The Future Path of Tokenization in U.S. Stocks

TechFlow Selected TechFlow Selected

Pilot Programs Outweigh Demand: The Future Path of Tokenization in U.S. Stocks

A deep deconstruction of the two mainstream paradigms represented by xStocks (Backed Finance) and Robinhood, analyzing their structural barriers and exploring their two potential evolutionary paths.

Author: Keji Kokii

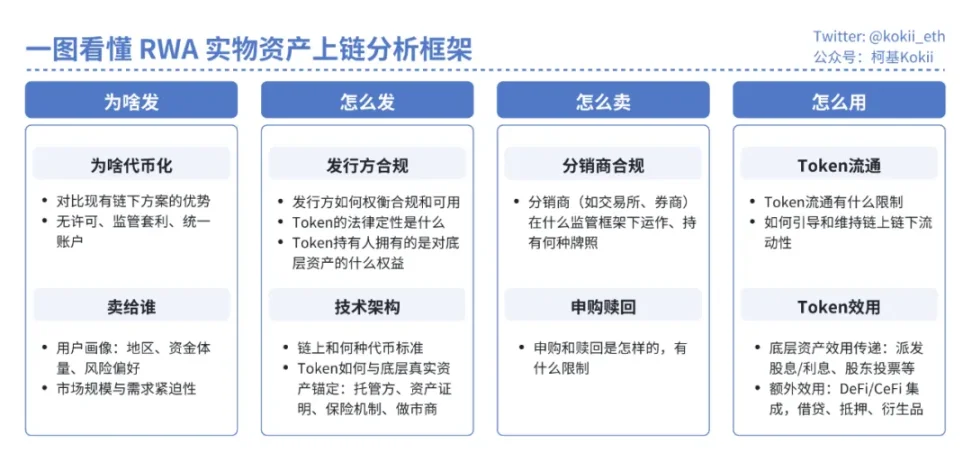

Why Stock Tokenization Struggles to Gain Traction

To understand the challenges of stock tokenization, one must first recognize the key to RWA (real-world asset) onboarding success. Whether it's government bonds, funds, stocks, private credit, or even intellectual property, the essence is simple: a real-world entity holds the physical asset off-chain and issues a corresponding set of tokens on-chain—technically as straightforward as launching a memecoin.

However, every project must confront four fundamental questions: Why issue? How to issue? How to sell? And how to use? Without addressing these effectively, RWAs will end up like most memecoins—lacking real demand and liquidity.

Take the most successful category of RWA products today—tokenized U.S. Treasuries and money market funds—as an example. As a standardized debt instrument with clear rights and predictable cash flows, its tokenization succeeded by following a three-step process: identifying genuine demand, establishing a compliant issuance framework, and building token utility:

-

Why issue: Institutional investors [Crypto VCs/Funds] hold large amounts of idle stablecoins on-chain and require risk-free yield opportunities

-

How to issue: Fund–fund manager structure, where tokens legally represent fund shares. The fund issues tokens and holds assets; the fund manager makes investment decisions. Both entities must be licensed and compliant, supported by custodians, auditors, and institutional-grade reporting

-

How to sell: Only KYC/AML-verified qualified investors can purchase, available 7*24

-

How to use: Token derivative utilities are widely supported across major DeFi platforms—usable as collateral for borrowing stablecoins, and some centralized exchanges are beginning to accept them as margin collateral

In contrast, stocks—as complex ownership instruments entailing governance rights and uncertain cash flows—face significant operational and regulatory hurdles in their path to tokenization.

Why Issue?

Early RWA attempts were often vague about the "why." Focusing on alternative assets such as private loans, private equity funds, and real estate, they hoped blockchain’s efficient settlement would enhance liquidity. Yet, the illiquidity of these assets stems not from technological limitations but deeper structural issues—information asymmetry, lack of fungibility, pricing difficulties, and issuer resistance to secondary markets. These problems exist off-chain and cannot be solved merely by putting assets on-chain.

The benefits of bringing real-world assets on-chain have become cliché. To summarize briefly:

-

Permissionless accessibility: [Capital] lowers investment barriers; [Products] removes geographic and financial restrictions such as bank accounts, compliance, and foreign exchange controls; [Time] enables 7*24*365 trading with instant clearing and settlement. Additionally, permissionlessness allows for regulatory arbitrage—crypto-native platforms including wallets and exchanges can expand into traditional finance without requiring licenses

-

DeFi composability: Leverage DeFi protocols for trading, lending, and derivatives to apply transparency and interoperability to traditional assets, unlocking additional yield opportunities

-

Unified accounts: If stablecoins become widely adopted for economic activity via on-chain settlement, integrating real-world assets onto the chain would allow users to manage diverse holdings across brokers within a single account, enabling cross-collateralization

The key lies in identifying the target user base. No matter how compelling the narrative of financial inclusion, one cannot expect unbanked individuals in Africa to buy U.S. Treasuries or equities. Well-functioning markets require sufficient participants—this demand may come from policy-driven mandates, experienced high-net-worth retail investors, or institutions already exploring blockchain.

Most likely, the intended users for RWA projects are actual investors—high-net-worth individuals and institutional players. This leads directly to the next set of questions: how to issue and distribute, and crucially, how to avoid regulatory crackdowns.

Investors need clarity on the legal nature of the tokens they're buying—the issuing entity, risk controls, pegging mechanism, whether the token is backed, redeemable, and legally enforceable. Past attempts at stock tokenization, including DeFi’s Mirror Protocol and Synthetix, and CeFi platforms like Binance and FTX, all failed or shut down due to regulatory pressure or awkward product designs that found no market fit.

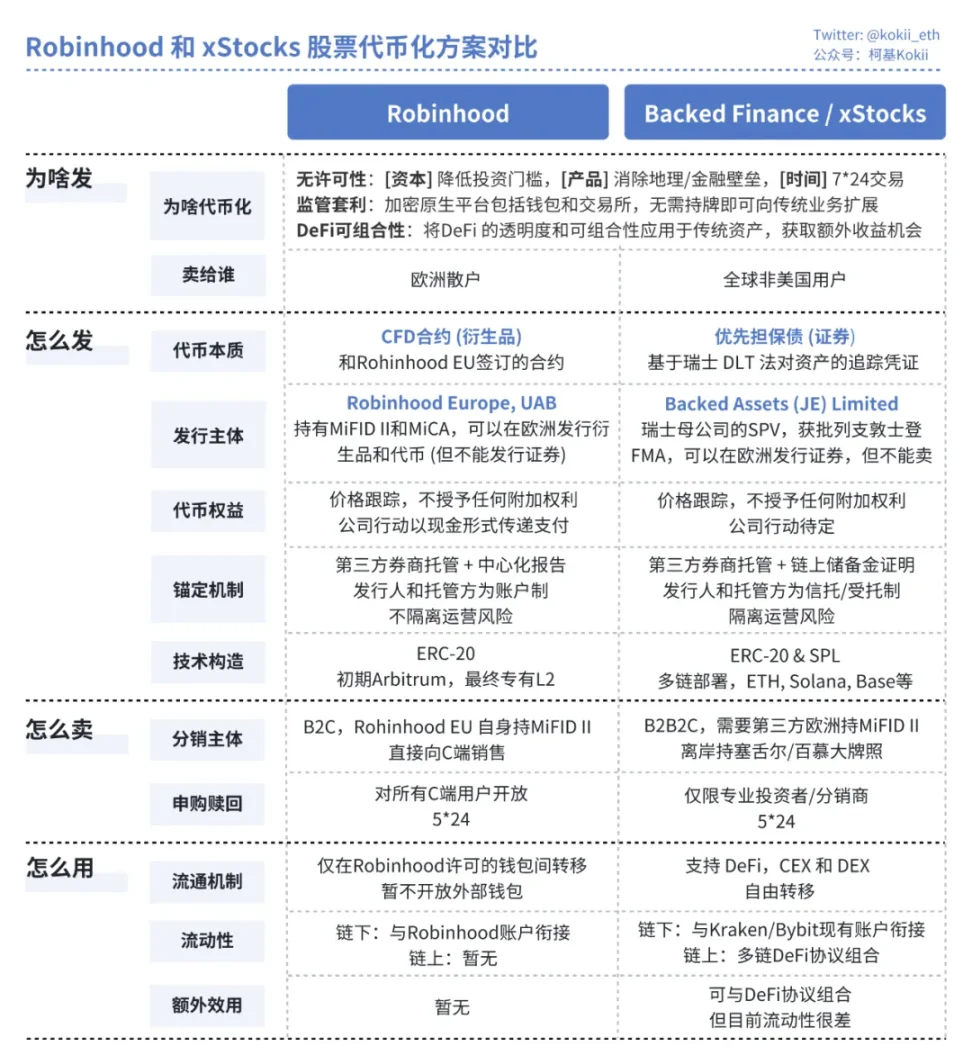

Recently, Robinhood and xStocks have launched tokens under relatively favorable regulatory frameworks—fully backed 1:1 off-chain, centrally registered securities, fully compliant and legal.

Current Solutions

a. Robinhood

-

How to issue: Legally structured under the EU's MiFID II framework, issued by Robinhood Europe UAB—a licensed entity based in Lithuania—as a financial derivative contract. Users' tokens are digital representations of this contract, with Robinhood itself acting as the counterparty. The underlying real stocks are held as hedged positions by Robinhood’s U.S.-based brokerage affiliate

-

How to sell: Operates a B2C model, with Robinhood Europe as the sole issuer and seller, targeting European retail users directly through its app. Liquidity is entirely internalized, forming a closed loop

-

How to use: Smart contracts include strict whitelisting mechanisms, preventing free circulation and eliminating any external DeFi composability

b. xStocks

-

How to issue: Under Switzerland’s DLT Act framework, real stocks are held by a bankruptcy-remote SPV established in Liechtenstein. Tokens represent legally recognized, 1:1 asset-backed senior secured debt (tracking certificates). Trust is ensured through independent third-party custody and Chainlink Proof of Reserves (PoR), verifiable in real time by anyone

-

How to sell: Uses a B2B2C model. Issuer Backed Finance handles institutional-level primary market subscriptions and redemptions, while licensed exchanges like Kraken and Bybit act as distributors for secondary market users. Liquidity is provided jointly by professional market makers on centralized exchanges and liquidity pools on decentralized protocols (e.g., Jupiter, Kamino on Solana)

-

How to use: Fully transferable and fully composable within DeFi—can be used as collateral for borrowing

In both cases, tokens legally track only price movements and do not represent direct equity on-chain. Other shareholder rights—such as voting and dividend entitlements—and handling of corporate actions (e.g., splits, mergers, delistings, liquidations)—remain unresolved. Meanwhile, the added utility promised by tokenization remains unrealized: Robinhood’s tokens circulate only internally, while xStocks, despite DeFi compatibility, suffers from extremely poor liquidity—effectively non-existent.

These two models resemble regulatory arbitrage by crypto-native platforms under currently lenient regimes—aimed more at capturing market attention and achieving better capital market valuation than delivering transformative utility. Regardless of the approach, current stock tokenization faces several structural obstacles unlikely to be resolved in the short term:

-

Fuzzy demand: For their primary non-U.S. audience, numerous mature, low-cost, highly liquid channels already exist for trading U.S. stocks (e.g., online brokers like IBKR, CFDs). Stock tokenization offers no clear advantage in user experience or fees

-

Liquidity困境: Price discovery still occurs off-chain. On-chain liquidity is minuscule and fragmented compared to traditional markets, leading to high slippage for large trades

-

Market-making risks: During periods when underlying stock markets are closed (e.g., weekends), market makers cannot hedge exposure, forcing wider spreads or withdrawal of liquidity—undermining the reliability and cost-efficiency of 24/7 trading

-

Incomplete rights: Both models significantly compromise core shareholder rights. Holders receive only economic benefits, while governance rights such as voting are retained and exercised by the issuer (SPV or Robinhood), making them functionally inferior to established instruments like ADRs

The Road Ahead

Despite present shortcomings, the true significance of these “pilot” efforts lies in exploring future possibilities. The future of tokenized stocks depends on their ultimate role within the broader financial ecosystem.

-

Path A: Mainstreaming and Infrastructure Integration. If global regulatory frameworks mature and stabilize, and stablecoins achieve widespread adoption, major financial institutions may eventually place portions of their assets on-chain. Custodians and issuers could evolve into traditional powerhouses like JPMorgan or BNY Mellon. In this scenario, tokenized stocks would become powerful “composable super ADRs.” Blockchain would serve as a unified settlement layer for global equity markets, integrated into DeFi protocols, and companies might conduct IPOs directly via STOs on-chain

-

Path B: Offshoring and Emerging Asset Platforms. If mainstream regulation tightens further, the crypto space may instead evolve into an efficient offshore innovation hub. Rather than competing with NYSE on Apple stock trading, tokenization would shift toward becoming a “launchpad” for novel or illiquid assets—such as Pre-IPO private equity, fractionalized VC fund shares, or securitized future income streams from intellectual property

The current immaturity of stock tokenization is not a sign of failure, but a necessary phase in the development of foundational infrastructure. The metric for success should not be whether it offers a better way to trade Apple stock today, but rather what new markets and financial behaviors it enables tomorrow. For all market participants, recognizing this truth is key to gaining early advantage in the financial revolution now unfolding.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News