The Battle for On-Chain Finance: Who Will Design the New Order?

TechFlow Selected TechFlow Selected

The Battle for On-Chain Finance: Who Will Design the New Order?

From traditional financial institutions such as JPMorgan Chase to crypto-native companies like Circle, participants from diverse backgrounds are actively building out the on-chain financial ecosystem.

Author: Tiger Research

Translation: AididiaoJP, Foresight News

Executive Summary

-

JPMorgan begins issuing deposit tokens on public blockchains, layering blockchain technology onto the existing financial order

-

Circle applies for a trust bank charter, aiming to build a new financial system from the ground up on technological foundations

-

These two types of institutions are attacking traditional finance from opposite directions, creating a "converging duality" trend

-

Unclear value positioning may weaken their respective competitive advantages; core strengths must be clarified and balanced effectively

A New Competitive Landscape in On-Chain Financial Infrastructure

Blockchain technology is reshaping the fundamental architecture of global financial infrastructure. According to the latest report by the Bank for International Settlements (BIS), as of Q2 2025, the global scale of on-chain financial assets has exceeded $4.8 trillion, with an annual growth rate consistently above 65%. In this transformative wave, traditional financial institutions and crypto-native enterprises are pursuing distinctly different development paths:

JPMorgan – Representative of Traditional Financial Institutions

Adopts a “blockchain+” incremental reform strategy, embedding distributed ledger technology into the existing financial system. Its blockchain division, Onyx, now serves over 280 institutional clients, processing $600 billion in transactions annually. The recently launched JPM Coin has surpassed $12 billion in daily settlement volume.

Circle – Representative of Crypto-Native Enterprises

Has built a fully blockchain-based financial network through its USDC stablecoin. USDC currently has a circulating supply of $54 billion, supports 16 major public blockchains, and processes over 3 million transactions per day.

Compared to the fintech revolution of the 2010s, today’s competition features three key differences:

The focus has shifted from user experience to infrastructure reconstruction

Technical depth has moved from the application layer down to the protocol layer

Participants have evolved from complementary partners to direct competitors

JPMorgan: Technological Innovation Within the Framework of Traditional Finance

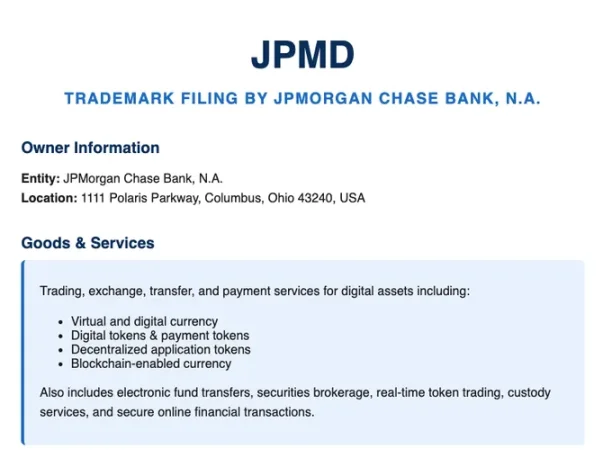

JPMorgan has filed a trademark for its deposit token "JPMD"

In June 2025, JPMorgan’s blockchain unit Kinex began piloting its deposit token JPMD on the public chain Base. Previously, JPMorgan primarily used private chains to apply blockchain technology. Now, by directly issuing and enabling circulation of assets on open networks, it marks a pivotal moment—traditional financial institutions are beginning to operate financial services directly on public blockchains.

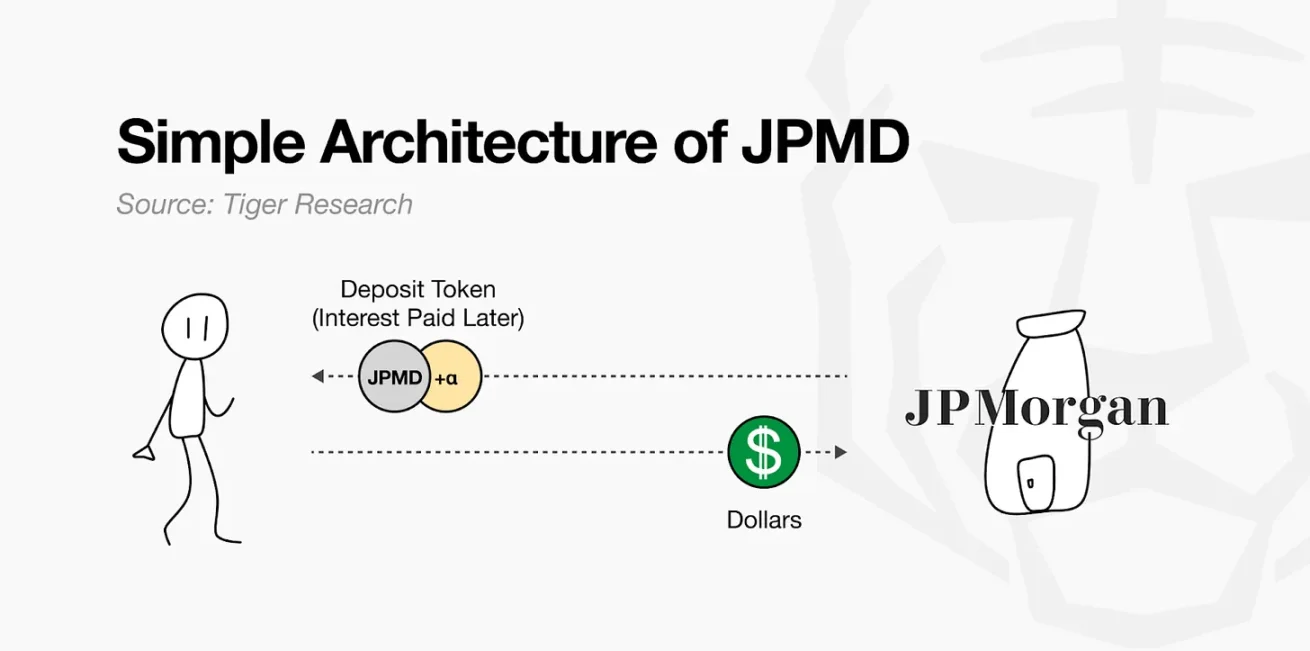

JPMD combines characteristics of digital assets with traditional deposit functionality. When customers deposit U.S. dollars, the bank records the deposit on its balance sheet while simultaneously issuing an equivalent amount of JPMD on the public blockchain. This token can circulate freely and retains legal claim rights to the underlying bank deposit. Holders can redeem JPMD 1:1 for USD and may also benefit from deposit insurance and interest income. Unlike existing stablecoins whose profits are concentrated in the issuer, JPMD differentiates itself by granting users substantive financial rights.

These features offer highly attractive utility value for asset managers and investors—so much so that some legal risks may be overlooked. For example, if on-chain assets such as BlackRock's BUIDL fund use JPMD as the redemption payment instrument, 24/7 redemption becomes possible. Compared to current stablecoins that require separate fiat conversion, JPMD enables instant cash settlement while offering deposit protection and potential interest earnings, giving it significant potential within the on-chain asset management ecosystem.

JPMorgan's launch of a deposit token responds to the new capital flows and revenue structures created by stablecoins. Tether generates around $13 billion in annual revenue, and Circle earns substantial returns by managing safe assets like Treasury bonds. Although these models differ from traditional interest spreads, their mechanism of generating income from customer funds resembles certain banking functions.

However, JPMD has limitations: its design strictly adheres to existing financial regulations, making full decentralization and openness difficult to achieve. Currently, it is only available to institutional clients. Nevertheless, JPMD represents a pragmatic strategy by traditional financial institutions to enter public blockchain financial services while maintaining stability and compliance. It stands as a representative case of traditional finance expanding connectivity with the on-chain ecosystem.

Circle: Financial Reconstruction from a Blockchain-Native Perspective

Circle has established a key position in on-chain finance through its stablecoin USDC. Pegged 1:1 to the U.S. dollar, backed by cash and short-term U.S. Treasuries, USDC has become a practical alternative for corporate payments, settlements, and cross-border remittances due to its low fees and instant settlement advantages. Supporting 24/7 real-time transfers without the complex processes of the SWIFT network, USDC enables businesses to break free from the constraints of traditional financial infrastructure.

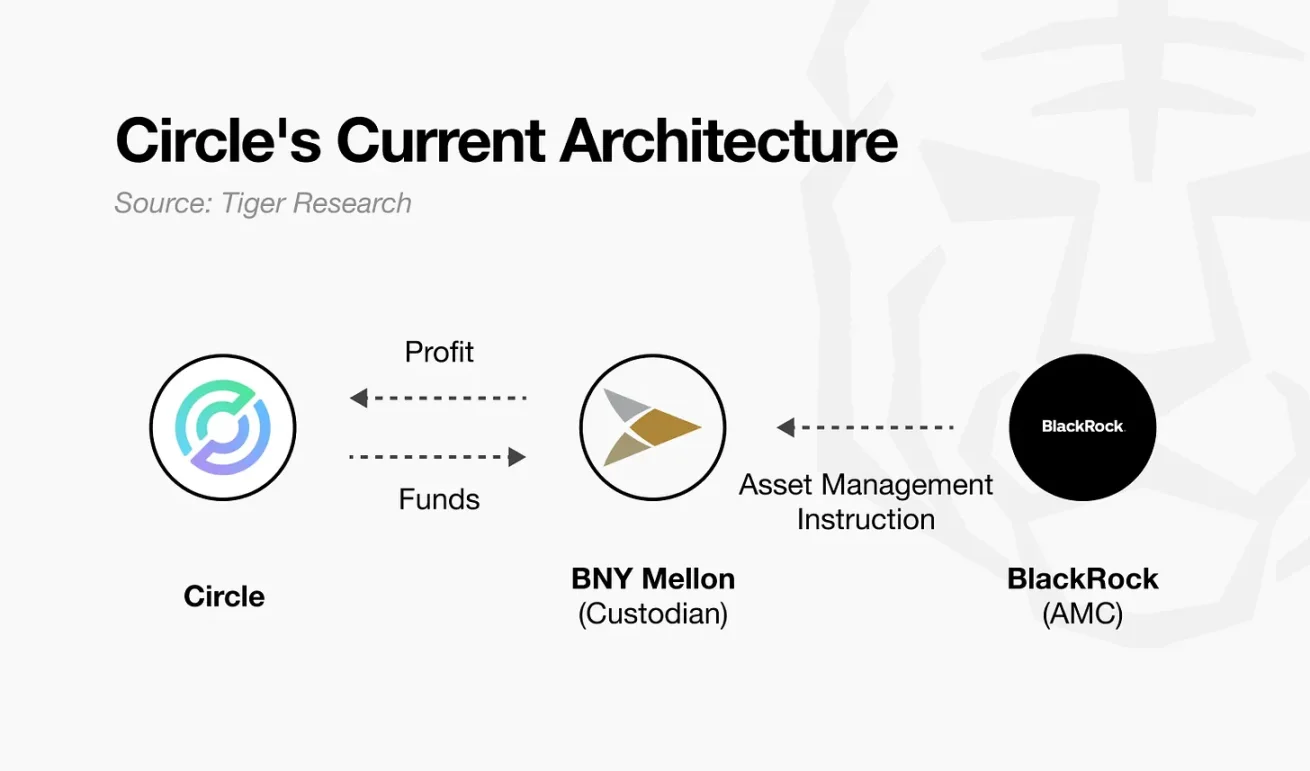

Yet Circle’s current business model faces multiple constraints: BNY Mellon custodies USDC reserves, while BlackRock manages asset operations. This structure outsources core functions to external parties. While Circle receives interest income, it has limited actual control over these assets. Its current profit model is also heavily dependent on high-interest-rate environments. To achieve long-term sustainability and diversified revenue streams, Circle needs more independent infrastructure and operational authority.

Source: Circle

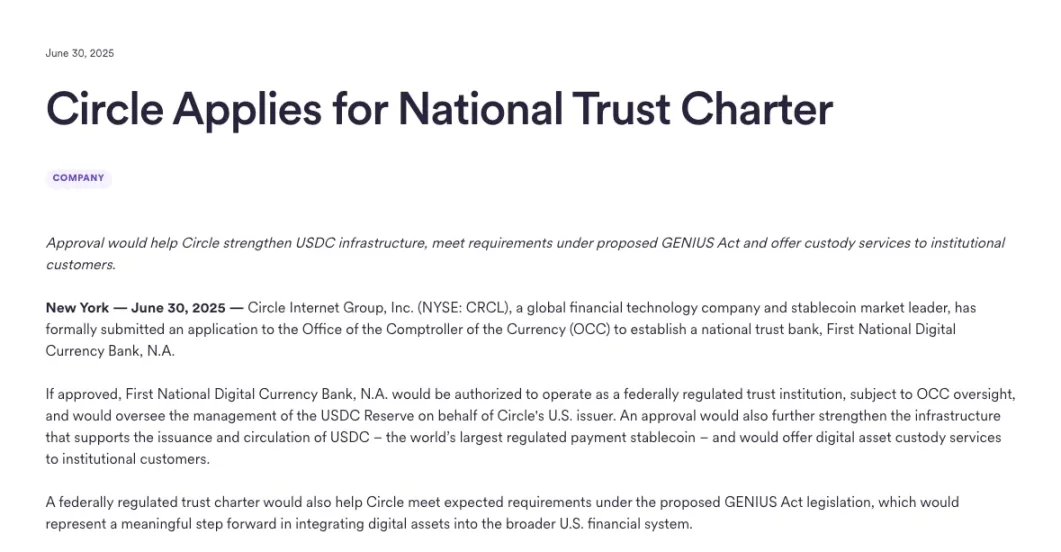

In June 2025, Circle applied to the U.S. Office of the Comptroller of the Currency (OCC) for a national trust bank charter—a strategic move that goes beyond mere compliance. Industry observers interpret this as Circle’s transformation from a stablecoin issuer into an institutionalized financial entity. As a trust bank, Circle would gain direct control over reserve custody and asset management, strengthening internal control over financial infrastructure and opening doors to broader service offerings, including institutional digital asset custody.

As a crypto-native company, Circle is adjusting its strategy to establish a sustainable operating model within the regulatory framework. This transition comes at the cost of reduced flexibility and increased regulatory burden, requiring acceptance of existing financial system rules and roles. The specific permissions granted will ultimately depend on policy developments and regulatory interpretation. Nonetheless, this attempt marks a critical milestone in measuring how deeply on-chain financial structures can be integrated into the established institutional framework.

Who Will Lead On-Chain Finance?

From traditional financial institutions like JPMorgan to crypto-native firms like Circle, participants from diverse backgrounds are actively building out the on-chain financial ecosystem. This echoes past competitive dynamics in the fintech industry: tech companies entered finance by internally replicating core functions like payments and remittances, while financial institutions expanded their user base and improved efficiency through digital transformation.

The crucial difference now is that these boundaries are blurring. A similar phenomenon is emerging in on-chain finance: Circle is directly assuming core functions like reserve management by applying for a trust bank license, while JPMorgan is issuing deposit tokens on public blockchains and expanding into on-chain asset management. Starting from opposite ends, both are gradually adopting each other’s strategies and encroaching on each other’s domains, each seeking a new equilibrium.

This convergence brings both opportunities and risks. If traditional financial institutions blindly imitate the agility of tech firms, they risk clashing with their existing risk control systems. Deutsche Bank, for instance, incurred billions in losses pursuing a “digital-first” strategy due to conflicts with legacy systems. Conversely, if crypto-native firms over-accommodate regulatory frameworks, they may lose the very flexibility that underpins their competitiveness.

The ultimate success or failure in on-chain finance hinges on a clear understanding of one’s foundational strengths. Companies must build upon their “unfair advantages” and achieve organic integration between technology and institutional frameworks. It is this balancing act that will determine who emerges as the winner.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News