Interview with Robinhood Co-Founder: Why Don't We Build Our Own Blockchain?

TechFlow Selected TechFlow Selected

Interview with Robinhood Co-Founder: Why Don't We Build Our Own Blockchain?

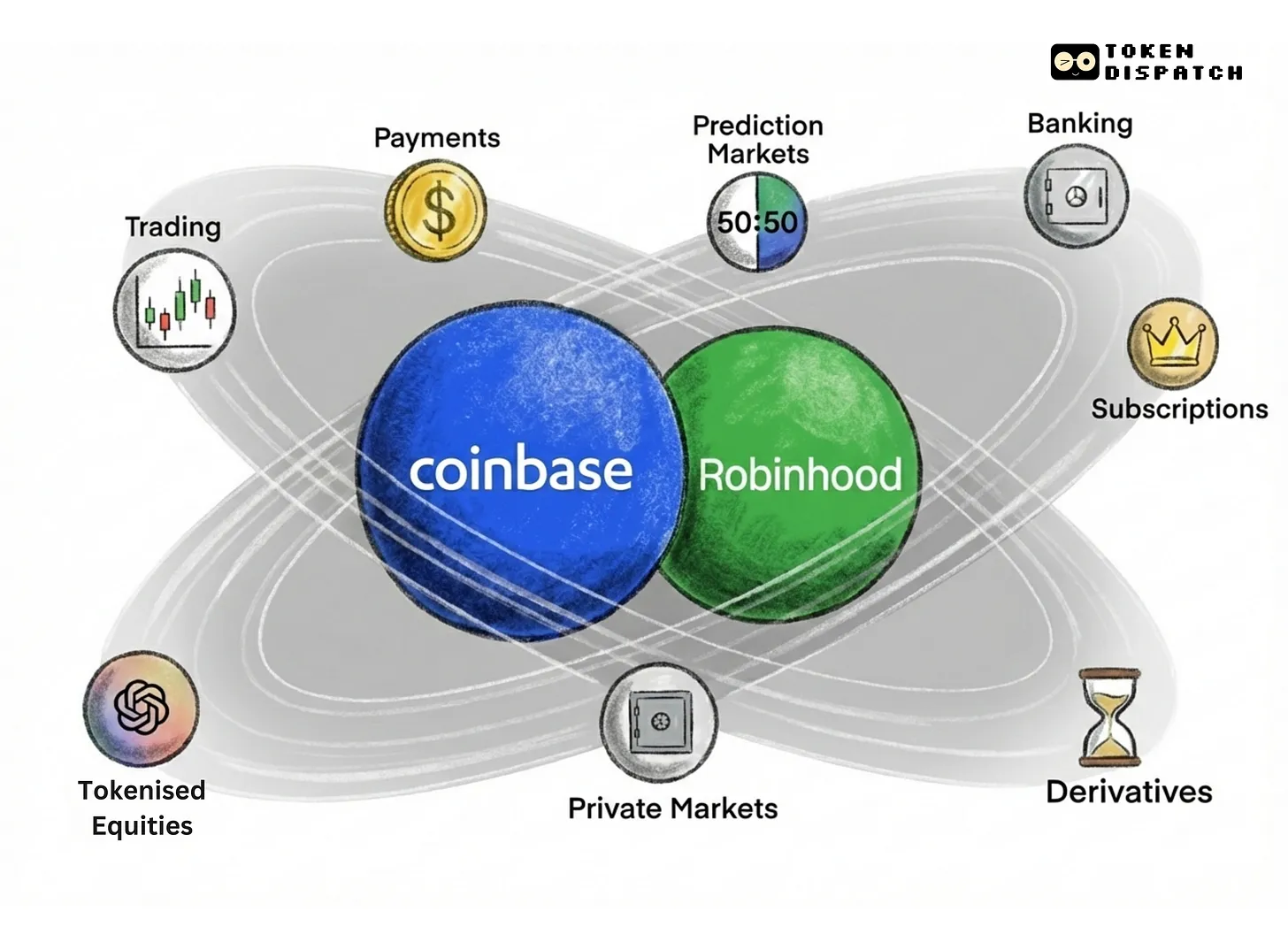

Dissecting Robinhood's product lines and revenue model.

Video source: Bankless

Translation: kkk, BlockBeats

Editor's note: On June 30, Robinhood co-founder Vlad Tenev announced on X that the company will release a major update related to its crypto business at 11 PM Beijing time. This move aligns perfectly with Robinhood’s current aggressive expansion into the realms of cryptocurrency and fintech.

As fintech evolves toward "platformization" and "intelligence," Robinhood now stands at the intersection of traditional brokerage and the emerging crypto order, reshaping the future of personal finance through a series of product restructurings.

Robinhood is moving beyond its identity as a simple trading tool, shifting toward an “operating system” model centered around the user’s full lifecycle. From tokenizing private equity, integrating CFTC-compliant prediction markets, launching Cortex and Strategies—covering AI-powered advisory and options strategy building—to introducing “cash-on-demand” Robinhood Banking and a unified multi-chain wallet architecture, the pace of its financial expansion far exceeds conventional expectations for a fintech firm.

In this in-depth interview with Bankless, Tenev outlines for the first time Robinhood’s comprehensive vision for expanding into crypto, AI, private banking services, and open private equity. He emphasizes that Robinhood isn’t the “antithesis of centralized finance,” but rather a bridge connecting TradFi and DeFi—offering more efficient and equitable financial access without relying on bank charters. He also addresses the debate over whether Robinhood is truly “bankless,” clarifying that Robinhood acts as a conduit service in crypto, not a sovereign issuer.

Today’s Robinhood is no longer just a gateway for retail U.S. stock investors—it aims to become a shared entry point for crypto-native users, AI-assisted investors, and global asset holders alike.

This interview was originally published on March 31. Below is the translated transcript:

Bankless: Welcome to Bankless, a show exploring the frontier of internet finance. Today I’m speaking with Vlad Tenev, CEO of Robinhood. With growing user numbers and assets under management, Robinhood is accelerating its position as a leading player in the cryptocurrency space. They’ve been involved early: not only offering crypto trading within the Robinhood app, but also launching Robinhood Wallet—a true non-custodial crypto wallet.

However, due to the former U.S. Securities and Exchange Commission (SEC)'s aggressive enforcement stance toward crypto, Robinhood’s further expansion in the sector was temporarily paused. Now that phase has passed. I want to understand—now that they’ve finally received clearance from the SEC—how Robinhood plans to advance its crypto product roadmap. Coincidentally, during the week I spoke with Vlad, Robinhood announced several major new product lines: including Robinhood Banking and Cortex. I took the opportunity to dive deep into these new offerings with him.

But for me, the most interesting part of the entire conversation—the part I enjoyed most—was our discussion about how “the bar for private companies to go public in traditional markets is rising ever higher,” and how this trend intersects with the tokenization movement. Companies like SpaceX, OpenAI, and Anthropic—some of today’s most promising ventures—remain private. While their shares circulate informally in private markets, there is no real public market for them.

Vlad believes tokenization can play a transformative role here—not only providing liquidity for these private firms, but also giving investors access to cutting-edge technology companies. It’s a perfect match. And if one platform were best positioned to host such tokenized markets, Robinhood would be among the top contenders.

All in all, I thoroughly enjoyed this conversation with Vlad. While Robinhood may not yet be a fully “bankless” platform, it continues to challenge the traditional financial system and force old institutions to evolve—which is good for the entire industry. So let’s begin today’s episode. But first, thanks to the sponsors who make this show possible—your support makes it feasible to explore what some call the “Wild West” of DeFi. That’s why you should check out FRAC’s Finance—an innovative protocol redefining stablecoins.

Welcome to Bankless Nation. Today we’re joined by Robinhood CEO Vlad Tenev. This is Vlad’s third appearance on the show. Every time he visits, there’s always big news from Robinhood—and each visit marks another step deeper into crypto. This time is no different. Vlad, great to have you back, welcome to Bankless.

Vlad Tenev: Thanks for having me. Always a pleasure to be here.

Bankless: You recently launched a series of major product updates: Robinhood Strategies, Robinhood Banking, and Robinhood Cortex. We’re airing this episode at just the right moment—though that’s mostly coincidence. We’ll get to those products soon. First, I’d like to start with topics closer to crypto natives, especially recent shifts in the U.S. regulatory environment for crypto.

Under this new administration, the U.S. crypto industry has seen many new opportunities—especially for institutional investors previously held back by regulatory uncertainty. Now that the new government is in place, which doors have opened? What can Robinhood do now that wasn’t possible before? And which door will you walk through first?

Shift in SEC Regulatory Stance

Vlad Tenev: I think the most direct change is that the U.S. has stopped using “enforcement as regulation.” In simple terms, we no longer need to operate under constant threat of legal action across every aspect of our business. This shift brings enormous relief. For example, the SEC announced it would terminate investigations into Robinhood’s crypto operations, as well as those of several other companies in the industry. At that moment, we felt immediate reassurance—we could finally move forward as a company and as an industry, no longer fighting endless battles.

The previous administration had a clear stance on crypto: they didn’t believe it should exist, nor should it integrate deeply with traditional finance. So this policy reversal is a massive win. Additionally, two important legislative directions are now advancing. Let me emphasize: ending “regulation by enforcement” alone is already a significant turning point.

Another notable development is clearer regulatory guidance on meme coins. You may have seen the SEC released a memo explicitly stating that meme coins are not securities. There really shouldn’t be much controversy here. Legally speaking, meme coins simply don’t meet the definition of a security—that’s relatively clear. But previously, every project had to conduct its own individual analysis to determine whether it qualified as a security.

Robinhood has always been one of the more compliant companies—we conduct rigorous reviews and compliance analyses for every single coin, assessing whether it constitutes a security. This process is expensive and cumbersome. So official guidance and exemptions are extremely valuable—they significantly reduce operational burdens for us and the entire industry.

Similarly, the question of whether staking constitutes a security now has clearer boundaries. This is very positive. Think about it: staking fundamentally involves users contributing their computational resources to support blockchain networks. Staking providers exist to simplify this process.

Overall, this means users can earn higher yields—more crypto flowing into their wallets. The lack of clarity before was actually harming American consumers, depriving them of rightful returns on better-regulated platforms.

So clear guidance is welcome. Currently, two key pieces of legislation are advancing in the U.S.: one on stablecoins, the other on market structure. The stablecoin bill is expected to pass first, which is great for the industry. But what excites us most is the “market structure” legislation.

We believe this is critical—it will provide a clear path for integrating crypto technology with real-world traditional financial assets. Things like securitized assets, yield-bearing stablecoins, and even prediction markets. It will allow us to clearly define:

-

Which assets qualify as crypto asset securities,

-

Which qualify as crypto asset commodities,

-

What compliance steps platforms must take to list crypto asset securities,

-

And what conditions issuers must meet to offer such assets to the U.S. public.

I believe these are the core issues. Legislation will help answer them one by one—that’s the prerequisite for unlocking crypto’s true potential. We’re genuinely excited about this.

You mentioned earlier that some companies are exploring using stablecoins to build banking services—where users’ stablecoins can be staked or deposited into pools to generate yield. I believe the actual deployment of such innovative products requires alignment with “crypto market structure legislation.” This would bring more competition into banking.

Current stablecoin legislation doesn’t fully cover “yield-bearing stablecoins,” so it can’t yet provide a solid legal foundation for such models. We still need greater regulatory clarity to make these products compliant and safe for mass adoption. But we remain optimistic and are actively participating in relevant legislative efforts in Washington. The current trajectory is positive, and we’re confident.

Bankless: From what you’re saying, it sounds like there are already many products that could theoretically be launched—but we’re still in the exploration or conceptual stage. To truly enter implementation and construction, Congress needs to pass these bills quickly. Is my understanding correct?

Vlad Tenev: Exactly. Take, for instance, a stablecoin that pays interest directly to holders. In essence, it’s very similar to a money market fund. In fact, many stablecoins already hold U.S. Treasuries—so functionally, they’re not that different from money market funds. Regulators have historically treated stablecoins differently, but we believe this is precisely where regulatory clarity is needed.

Tokenization of Private Equity

Bankless: Let’s talk about “asset tokenization”—a hot topic, especially in traditional finance. It’s essentially a bridge between TradFi and crypto: can we bring more assets on-chain and truly leverage the advantages of public, permissionless blockchains? Where does Robinhood fit in this trend? I assume you’re bullish. Will you act as an issuer? A platform? Will Robinhood issue its own tokenized products, or will you focus on being a marketplace for such products? Where do you sit in this tokenization tech stack?

Vlad Tenev: For us, “asset tokenization” means creating an on-chain representation of a non-native crypto asset so it can be freely traded. We already have examples—like stablecoins. A stablecoin is effectively a tokenized U.S. Treasury asset. Another interesting case is Paxos’ tokenized gold product. We’ve also partnered with Paxos and others on USDG—the Dollar Global Network project—with the goal of creating a globally accessible stablecoin that offers attractive yields to holders.

The next natural step is tokenized securities—a direction we’re very excited about. It would allow global users to own shares in U.S. companies as easily as they use stablecoins. Just as stablecoin legislation is seen as a tool to maintain the dollar’s global dominance, tokenized securities could help U.S. companies retain leadership in global markets.

Vlad Tenev: Right now, it’s extremely difficult for overseas investors to invest in U.S. companies. Just as stablecoins made accessing dollars easy, tokenized securities could let global users easily invest in U.S. equities. This benefits corporations, international investors seeking exposure to high-quality assets as a hedge against depreciating local currencies, and American entrepreneurs and capital markets. If we can raise capital more easily via global crypto markets, we’ll see more innovative and promising companies emerge. In fact, we published an op-ed in The Washington Post months ago advocating for the tokenization of private securities.

Think about how hard it is today to invest in private giants like OpenAI or SpaceX. Crypto technology offers a solution. If we can tokenize shares of private companies, it benefits both the companies and investors. It’s absurd that we now have clear regulatory definitions for meme coins—allowing people to freely invest in projects with zero fundamentals—but cannot invest in exceptional private firms like OpenAI or SpaceX.

Bankless: If I piece this together, there’s already a kind of “market” for SpaceX equity—but it exists only in private markets. Many people have acquired SpaceX shares through various channels. Are you suggesting we could tokenize these shares, standardize and formalize this market using crypto, turning it into a truly structured, deep market?

And in this process, Robinhood could serve as the trading platform. Are you saying this is part of your roadmap? And how far off is Robinhood launching tokenized shares of companies like SpaceX?

Vlad Tenev: Yes, Robinhood sits precisely at the intersection of traditional and crypto finance. We possess all the crypto technology while also maintaining full traditional financial infrastructure—including multiple broker-dealer licenses. This is exactly where we can contribute to the ecosystem.

In the future, this might resemble the ETF creation mechanism. An ETF holds a basket of securities and issues tradable shares. In effect, this is a precursor to tokenized securities. In ETFs, investors can exchange a basket of underlying assets for ETF shares, or redeem shares for the assets. This “create/redeem” mechanism is essentially a traditional finance counterpart to tokenization logic. Crypto technology can make this process more efficient and decentralized.

Bankless: While IPO volumes haven’t collapsed entirely, the overall trend is downward. The reason is simple: IPO costs are too high, making it increasingly difficult for many companies to go public. Could this trend accelerate the development of “private market tokenization” as an alternative? Or, from the perspective of global compliance and traditional finance norms, is this path too complex to implement? What’s your view?

Vlad Tenev: I believe this trend will push “security tokenization” to become a viable alternative to IPOs. This will happen eventually—even if the U.S. doesn’t lead, other countries will experiment. Crypto is inherently global. If you can issue tokenized shares of a company on a blockchain within a compliant jurisdiction, you immediately gain access to a highly liquid, global market with hundreds of millions of participants. For this reason, I believe the U.S. will ultimately embrace this trend.

Tokenization serves two key purposes:

-

First, early-stage startups—this is equivalent to traditional IPOs, i.e., primary market fundraising. Access to “main capital” is crucial. As a founder who raised seed funding myself, I know how consuming and resource-intensive fundraising can be for small companies. Being able to quickly tap into a global pool of capital is highly attractive. It will spawn more new companies and projects, and give investors earlier (albeit riskier) access with potentially higher returns.

-

Second, later-stage private companies like OpenAI or SpaceX—founders here have already raised substantial capital and may even be planning IPOs. Tokenization may not appeal much to founders, but it’s highly valuable for employees. Large companies often have thousands or even tens of thousands of employees, many without clear liquidity events or exit expectations. They want the ability to cash out part of their equity for diversification. This creates strong real-world demand for tokenization.

There are already some “secondary employee equity markets,” like EquityZen or Forge, which proactively contact employees to facilitate share transfers. But the biggest problem with these platforms is fragmented liquidity. They must manually match buyers and sellers—an inefficient process. The advantage of crypto lies in interoperability. Once an asset is on-chain and freely tradable as a token, it instantly connects to global liquidity. This is where tokenization shines as a technological solution.

Bankless: Indeed, many trends are pushing in this direction. Star companies like SpaceX and OpenAI remain private, with little apparent interest in going public. Many AI startups follow suit—they don’t have public equity, nor do they face dilution issues like Meta or Google, making it hard for investors to bet directly on the AI sector.

Vlad Tenev: For average investors, options to bet on AI are extremely limited. You might buy NVIDIA (but it’s already worth over a trillion), Alphabet (also trillion-dollar), or Tesla. These are all massive and already reflect most AI premiums. But you can’t invest in core AI startups like OpenAI, Anthropic, or Perplexity.

Bankless: Exactly. Looking at public market trends today, new investment opportunities are increasingly emerging not in public markets, but in private ones. Part of the reason, as I mentioned, is the rising cost and difficulty of IPOs. Meanwhile, crypto offers a potential solution. I see many favorable winds pushing this trend toward a conclusion: tokenized private equity may eventually evolve into a form of “quasi-public market.”

Alright, I’d also like to discuss prediction markets—I recall Robinhood recently entered this space. Did you ever have a slogan like “everything can be marketized”? Or am I misremembering? Is that an official strategic direction, or just a perception? Can you clarify?

Robinhood’s Entry Into Prediction Markets

Vlad Tenev: Actually, Robinhood has never officially used the slogan “everything can be marketized.”

Bankless: So I imagined it.

Vlad Tenev: However, our parent company is called Robinhood Markets, and you might have heard our mission statement: “Democratizing finance for all.” This means we believe in the power of markets—if a market exists, we believe it should be enabled, and traders should be able to participate. Especially for markets traditionally accessible only to institutions, if retail investors are interested, we believe they should be able to participate fairly. That’s one of our goals in “building markets,” and it naturally extends to prediction markets.

Personally, I think prediction markets offer additional social value: they’re not just trading venues—they can produce more accurate forecasts. We saw this during presidential elections—while mainstream media hesitated, prediction markets gave directional signals hours or even days earlier. I believe this trend will expand into more domains. So I see prediction markets as “truth machines”—an evolution of traditional news, sometimes even letting us “see the news” before events unfold. Fascinating.

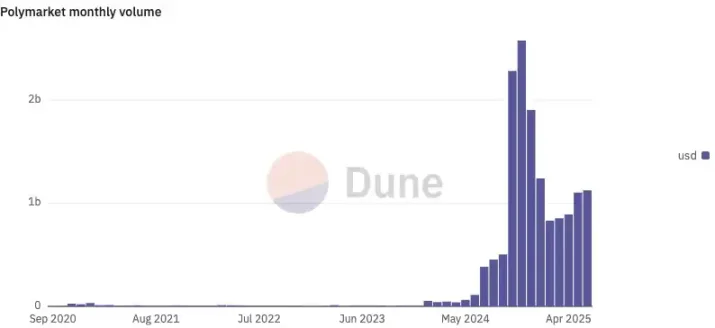

Bankless: Like many others, I hosted a presidential election party. We had mainstream media on TV, but since most of my friends work in crypto, we also opened a Polymarket page on screen. Everyone kept switching between mainstream media and Polymarket—the latter felt more “real-time” and closer to the truth.

Recently, Robinhood made a move in prediction markets. Let me read the press release to introduce the topic: Robinhood recently launched a prediction market section within its app, allowing users to trade outcomes of major global events. At launch, available contracts included the upper bound of the May Federal Funds rate and NCAA men’s and women’s college basketball tournaments—two very different types of markets. So, the first question I already know the answer to—why launch prediction markets? But more importantly, the product is powered by Kalshi. Can you explain Kalshi’s role in this partnership?

Vlad Tenev: Sure. Kalshi is a DCM (Designated Contract Market), playing a role similar to exchanges in the stock market—like NASDAQ or NYSE. Robinhood, as a broker, connects to these exchanges or market makers to match buyers and sellers; trade execution happens on the exchange. In stocks, Robinhood is a broker with introducing and clearing brokers—we route orders to exchanges or market makers. In futures markets—regulated by the CFTC—DCMs serve as exchanges. In this context, Robinhood acts as an FCM (Futures Commission Merchant), interfacing with customers, providing UI and order entry, then routing orders to the DCM for matching.

You can think of Kalshi as NASDAQ, and us as the traditional broker. For presidential election-related contracts, we connect to another DCM called ForecastEx, a subsidiary of Interactive Brokers. We can connect to multiple DCMs, offering users access to different contracts. However, any prediction market contract we offer must be formally listed by a DCM—we can’t launch our own.

Bankless: So Robinhood itself can’t launch its own prediction market—it can only connect via third-party DCMs, correct?

Vlad Tenev: Correct. You mentioned Polymarket earlier—one key reason it can’t operate compliantly in the U.S. is because it’s not a DCM. It uses a fully decentralized, crypto-based model to run prediction markets. But this is exactly what the market structure legislation we discussed earlier aims to address: how should prediction markets like Polymarket be regulated in the U.S.? Should they fall under CFTC commodity contracts, or require a new regulatory framework specifically for “crypto-native” prediction markets? Currently, these questions lack clear answers. Only after legislation advances can such markets legally operate in the U.S.

Bankless: I think our audience would love to legally use Polymarket in the U.S. One final question on prediction markets: Robinhood currently offers Fed Funds rate and college basketball prediction markets. What new prediction products are coming? Can you share Robinhood’s next steps?

Vlad Tenev: With our latest batch of prediction market contracts, we’ve upgraded from launching one contract at a time to supporting hundreds simultaneously. This involves operational complexity in clearing, settlement, and interdependencies between contracts—especially with series like men’s and women’s NCAA tournaments, which greatly tested our systems. Soon, we’ll be capable of launching thousands of contracts at once—unlocking the full diversity and potential of prediction markets.

We’re excited about many areas, especially AI advancements. Prediction markets around AI progress are intriguing and insightful—our users are very interested. More importantly, I believe prediction markets should become a “new kind of newspaper.” It should have a “front page” (what people care about most), plus sections for sports, business, entertainment, and lifestyle. Prediction markets can serve as a microcosm of information—a form of news driven by real trading intent.

Bankless: Yes, “prediction markets as truth machines”—that’s why many crypto users are so fascinated by them. A classic example was the Israel-Iran conflict: when missiles crossed borders, Polymarket provided real-time, credible insights. These aren’t just sensitive geopolitical issues—they’re high-stakes, impactful events. As global tensions rise, ordinary people naturally want better insight into the probabilities of such events. Do you envision Robinhood eventually integrating global macro and geopolitical prediction markets?

Vlad Tenev: I believe it’s socially valuable. Currently, the CFTC has guidelines on “event-based contracts” (i.e., prediction markets), stating that markets “contrary to the public interest should not be listed.” But “contrary to public interest” is vague and broad. I believe we should strive to clearly define this boundary, because I trust that the vast majority of prediction markets are, in fact, aligned with the public interest.

Three Product Lines

Robinhood Banking Product Line

Bankless: Back to Robinhood. You recently held a major launch event—like a Robinhood summit—introducing three new product lines: Robinhood Strategies, Robinhood Banking, and Robinhood Cortex. Let’s go through them one by one. Start with the one I’m most curious about: Robinhood Banking. What’s the motivation behind this product? How did the idea originate?

Vlad Tenev: The core idea behind this Gold event is: we want every user to have access to the same resources and services available to the wealthy. High-net-worth clients typically have private bank advisors, investment managers, research teams helping them find opportunities globally—across public and private markets. Technology now allows us to deliver this “family office-level service” to everyday users at very low cost. That’s our goal—to put a high-net-worth family’s financial team in every user’s pocket. For just $5/month, Gold members can access this service. We don’t just want to offer financial services—we want to build a “financial iPhone”: a premium product everyone can afford and be proud to own.

So the three products launched at the Gold event follow a unified logic: Strategies is your digital investment advisor; Cortex is your intelligent research assistant; Robinhood Banking is your private banker. This is also Robinhood’s first launch of AI-powered products. Going forward, you’ll see more advanced reasoning models and intelligent agents deeply integrated across products, enabling seamless interoperability and truly connected experiences.

“Information flows seamlessly,” delivering intelligent financial services.

Robinhood Cortex Product Line

Bankless: When I first read the announcement about Robinhood Cortex, I thought you’d launched an AI agent. After reading closely, I understood better. Can you give an example of how users actually use Cortex? I assume it’s integrated into the Robinhood mobile app—is it like a finance-specific ChatGPT? Can you elaborate on what kind of product it is?

Vlad Tenev: Within the Robinhood app, Cortex currently has two main use cases. First: explaining “what’s happening with this stock.” We often send push notifications when a stock moves more than 5%. Many users click in to see what’s going on. Cortex then appears on the stock’s detail page, explaining the drivers behind the price movement with clear, concise insights.

Second: options trading. Options are complex for most people, especially multi-leg strategies requiring professional judgment. With the Trade Builder feature, Cortex can automatically construct suitable options strategy combinations based on your forecast for a stock’s future movement—making the experience feel magical. We demonstrated this at the Gold event: users pick a stock, input their prediction, and the system generates executable options strategies, or enters our new parallel options chain view—letting users manage multiple options trades efficiently on one screen.

Bankless: So it’s like this: you express your trading intent in natural language, the AI processes it, and suggests several options combinations—is it translating human language into actionable strategy recommendations? Is that the logic?

Vlad Tenev: Yes, but we don’t just match based on your language input. We also integrate external data—real-time market data, technical indicators, news—and help refine your prediction itself. So we’re not just generating strategies from your existing outlook—we’re also assisting you in forming a more accurate forecast.

Bankless: Can you talk about the underlying LLM (large language model) architecture? I assume you’re not just slapping a ChatGPT wrapper on it, right? Is there anything special about the data or training that makes it a truly Robinhood-centric financial AI?

Vlad Tenev: Exactly. Most general-purpose LLMs lack real-time financial data—their knowledge is outdated. So they can’t tell you a stock’s current price, let alone accurately explain price movements. Worse, they’re prone to hallucinations in finance due to lack of reliable data. Our AI layer solves both the hallucination problem and real-time data gap—two major weaknesses of traditional LLMs.

Bankless: Yes, hallucinations in financial AI could be disastrous.

Vlad Tenev: Absolutely. But finance has an advantage: we have “sources of truth.” Unlike writing a history paper where hallucinations are hard to detect, financial data has clear benchmarks. We can set guardrails to precisely identify and correct hallucinations.

Bankless: That might be Robinhood’s core competitive advantage in building a financial AI assistant: real-time market data, user behavior data, and contextual data across all financial scenarios.

Vlad Tenev: Yes, that’s a major edge. Another is our ability to enable trading actions within the app. If Cortex can be context-aware of user behavior, it becomes far more valuable. We don’t want to just drop a chatbox into the app—that approach is naive, produces verbose outputs, and risks hallucinations. We deliberately avoid that path.

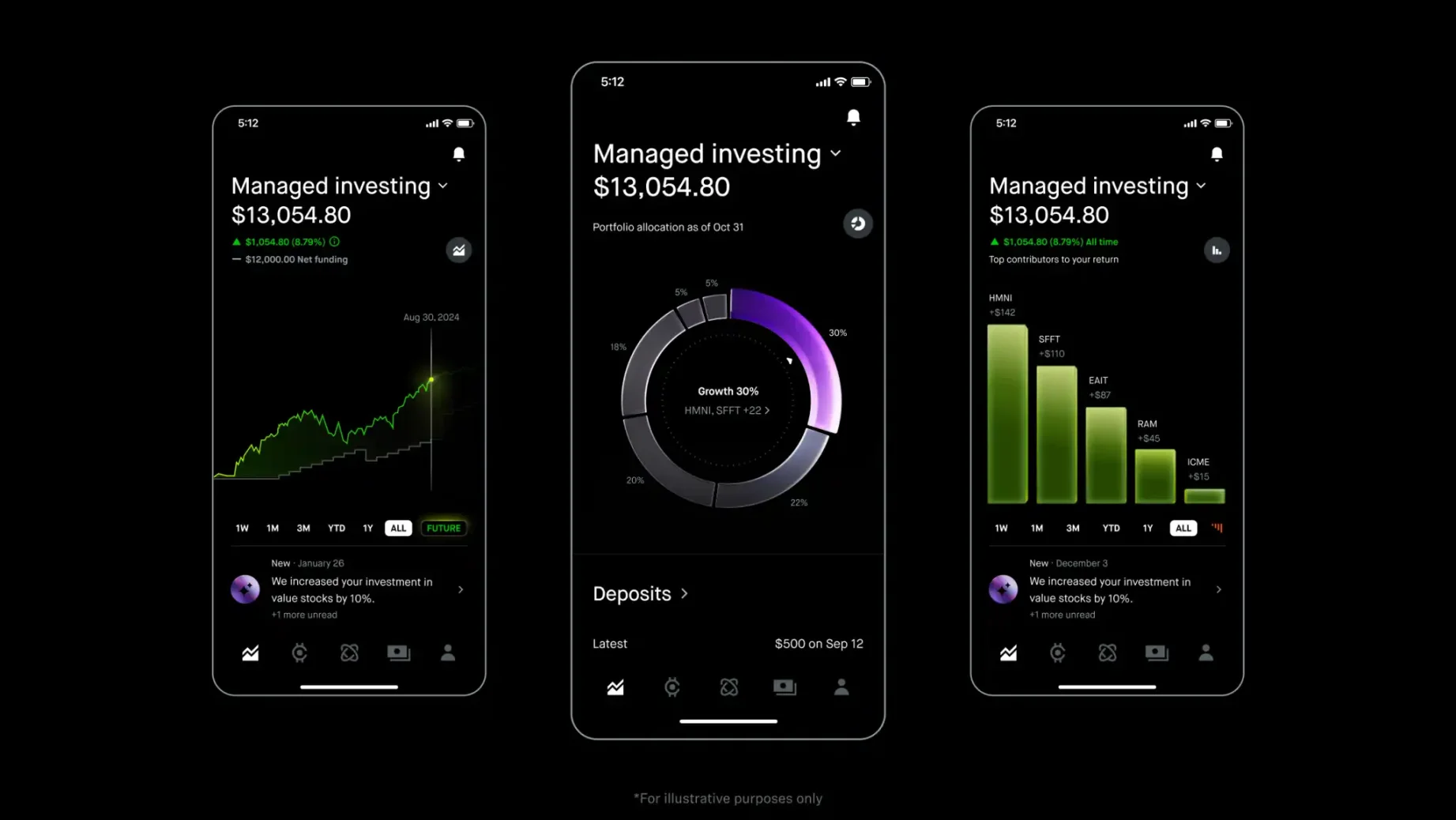

Robinhood Strategies Product Line

Bankless: Let’s circle back to Strategies: do you plan to extend this product to crypto assets? Because every crypto friend gets asked: “How do I buy crypto?” “How should I allocate?”—and few know how to answer. If Strategies could offer smart allocation advice for crypto, wouldn’t that be incredibly valuable? How do you plan to expand into this area?

Vlad Tenev: Technically, no problem. We have a long backlog—dozens or even hundreds of features under consideration. Right now, we prioritize based on user demand. We started with individual stocks because most robo-advisors only support ETFs, while our engine supports both stocks and ETFs in portfolios. We also designed a clean interface—like a ring chart showing asset allocation, with automatic rebalancing for a “set-and-forget” investing experience. Crypto was considered from day one—we’ll gradually integrate it. We’re live now, user feedback is strong, and many are migrating their portfolios over.

Also, Strategies has a key differentiation: we’ve completely reinvented the traditional advisory fee model. Traditional advisors charge a percentage of AUM—about 1%. Robo-advisors charge at least 0.25%. This creates a problem: the more you invest, the more you pay linearly, even though the service complexity doesn’t scale accordingly. For example, managing $1M isn’t 10x harder than $100K, but you pay 10x more. This frustrates high-net-worth users. Our model caps fees at $250. No matter your portfolio size, fees stop increasing. So the wealthier you are, the better the deal—and the happier you’ll be using Robinhood Strategies.

Bankless: Your Strategies cap is $250—not AUM-based. Does this mean Robinhood sees this more as a “user-count-driven” business? How do you benefit from large-scale growth in Strategies?

Vlad Tenev: Yes, this pricing model is a powerful incentive—it attracts users with large external assets to transfer funds to Robinhood. Robinhood benefits through multiple channels: asset management fees, Robinhood Gold subscription revenue.

We’ve observed that once users become Gold members and migrate a meaningful amount—say $1,000—they start feeling the platform’s value and are more likely to adopt other services like credit cards or active trading. That’s our goal: to migrate the user’s entire financial relationship to Robinhood, making it easy to manage all their money in one place. As total platform assets grow, so does our revenue.

Cash Delivery Service

Bankless: Got it. One more question about your new product—the cash delivery service. My first reaction was: “Is this the Uber Eats of cash?” Why are you doing this? How does it work?

Vlad Tenev: Yes, we’re entering the “logistics business”—which is personally fascinating to me. First, this is a premium private banking service. Robinhood has no physical branches. So we asked: how can we deliver a full-featured digital banking experience without physical locations? While cash usage is declining, it still accounts for 16% of all payments in the U.S.—many people still need it. But if you use a purely digital bank, you can only withdraw at 7-11 or CVS. Clearly, “going to a convenience store” contradicts the “private banking experience.”

We asked: can we reverse this—can the bank come to you? Logistics platforms today are mature—deliveries in 15 minutes, even iPhones arrive at your door. So we’re applying that model to cash services.

Of course, we won’t build our own logistics network. We’ll partner with specialized providers—we’ll announce the partner soon. It’s complex, but we believe it delivers tremendous value. I used to be a First Republic client—they offered “cash delivery” (via armored vehicles for large amounts). We’re thinking: how can we standardize this “rich people’s service” so more people can afford it?

Bankless: I assume the minimum withdrawal isn’t something like $100?

Vlad Tenev: In our demo, we set it at $200 minimum. But we’re still exploring—final thresholds, user behavior, average withdrawal amounts will depend on post-launch feedback. But we expect averages to fall in the hundreds-of-dollars range.

Robinhood’s Next Chapter: Product Matrix and Ecosystem Strategy

Bankless: Back to crypto. Robinhood currently lists relatively few crypto assets. Do you plan to expand the selection?

Vlad Tenev: Yes, since the regulatory environment improved, we’ve already added several assets—for example, Trump Coin, which we launched on inauguration day and became very popular. Thousands of new tokens emerge weekly. We realize we need to rethink our asset listing strategy. You’ll see Robinhood Wallet—currently somewhat separate from the main app—become more tightly integrated with the main app.

You’ll see: the main app gaining more on-chain capabilities; smoother deposits and withdrawals in Wallet; gradual convergence between Custody and DeFi products. As the industry matures, our strategy will shift from “hand-picking assets” to “efficient backend optimization based on demand,” giving customers more choice. Still, we’ll maintain screening mechanisms to prevent fueling speculative bubbles and protect users from asymmetric risks of low-quality, high-risk meme coins.

Bankless: So you now have Robinhood Wallet, the main Robinhood app, and Robinhood Credit Card—which is now part of Robinhood Banking, right?

Vlad Tenev: Correct, the Robinhood Credit Card is now under Robinhood Banking.

Bankless: Is the separation between these three apps mainly due to compliance/regulatory considerations? Do you have plans to unify them into a “super financial app”?

Vlad Tenev: We initially wanted a unified app, but the problem was—homepage design became too critical. Active traders and banking/credit card users have completely different homepage expectations. Most users mentally separate “trading interface” from “banking interface.”

So I’m open to integration. We can try building a super app, but I’m not fixated on merging. What matters more: unified KYC; frictionless fund transfers between accounts. Beyond that, let the best interface win. Our main app may add more features, or we may keep separate apps—perhaps like Uber and Uber Eats, splitting and merging as needed.

Bankless: Finally, let’s go off-script. You know our show is called Bankless—we advocate “de-banking,” self-custody, and autonomous control. Yet many Robinhood features sound quite “bank-like”—you’re actually launching banking products. Crypto challenges traditional finance—banks like Wells Fargo offer 0.25% savings rates with zero innovation. Robinhood offers better alternatives, yet you’re not fully “Bankless.” So I ask:

Vlad Tenev: “How Bankless am I?” Right?

Bankless: Yes, how Bankless are you? Which direction is Robinhood heading?

Vlad Tenev: Literally speaking, we are Bankless—we don’t have a bank charter. Sometimes people ask: will you apply for a bank license? Since we’re often compared to traditional financial firms with bank charters. Having one brings benefits: direct access to FedWire, Zelle; ability to issue loans, perform settlements.

But our current strategy is to remain a neutral platform partnering with banks. For our credit card product, our partner bank is Coastal Community Bank; other banks support our cash management program. In fact, many DeFi projects inherently need bank interfaces—whenever you convert fiat to on-chain assets, banks are part of the pipeline.

I believe we’ll see more “crypto banks” emerge—entities with certain licenses, under regulation, but less burdened than traditional banks. These institutions could manage key functions like capital pools and reserves, avoiding past collapses like Terra Luna, Anchor, or Celsius—projects that looked like banks but lacked real rules. I’m a market believer—I trust free competition and fair regulation. These two worlds—traditional banking and crypto technology—will ultimately converge, not remain divided.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News