Two Paths, One Destination

TechFlow Selected TechFlow Selected

Two Paths, One Destination

Today, they are all moving toward the same vision: becoming a financial super app.

By Prathik Desai

Translated by Block Unicorn

Introduction

Happy Year of the Dragon! Last week, two high-profile emerging financial firms released their earnings reports within 48 hours—and both missed revenue expectations. Immediately, they were lumped into the same narrative: “Crypto markets are weak, trading volumes are soft, and the good times are over.”

But this view completely misses the point.

While Coinbase’s and Robinhood’s stock prices may correlate closely with Bitcoin (BTC) price movements, their future trajectories aren’t dictated by BTC’s Q4 performance. Both are steadily moving beyond the narrow framing of “company fate tied to the crypto cycle.”

Both companies are undergoing major transformations—if you know where to look, you’ll spot these shifts in their financials. Yet focusing only on last quarter’s noisy data could cause you to overlook them entirely.

In fact, things aren’t that ambiguous. A glance at recent quarterly results—paired with the string of product announcements each company has issued over the past 12 months—makes everything clear.

Their long-term trends reveal not just where each is headed, but also how they’re betting on finance’s future—and crucially, when their paths begin to converge.

In today’s analysis, I’ll first unpack each company’s story separately, then explain where they overlap—and what that reveals about the broader competitive landscape they inhabit.

Part I: Coinbase — A Bet on Infrastructure

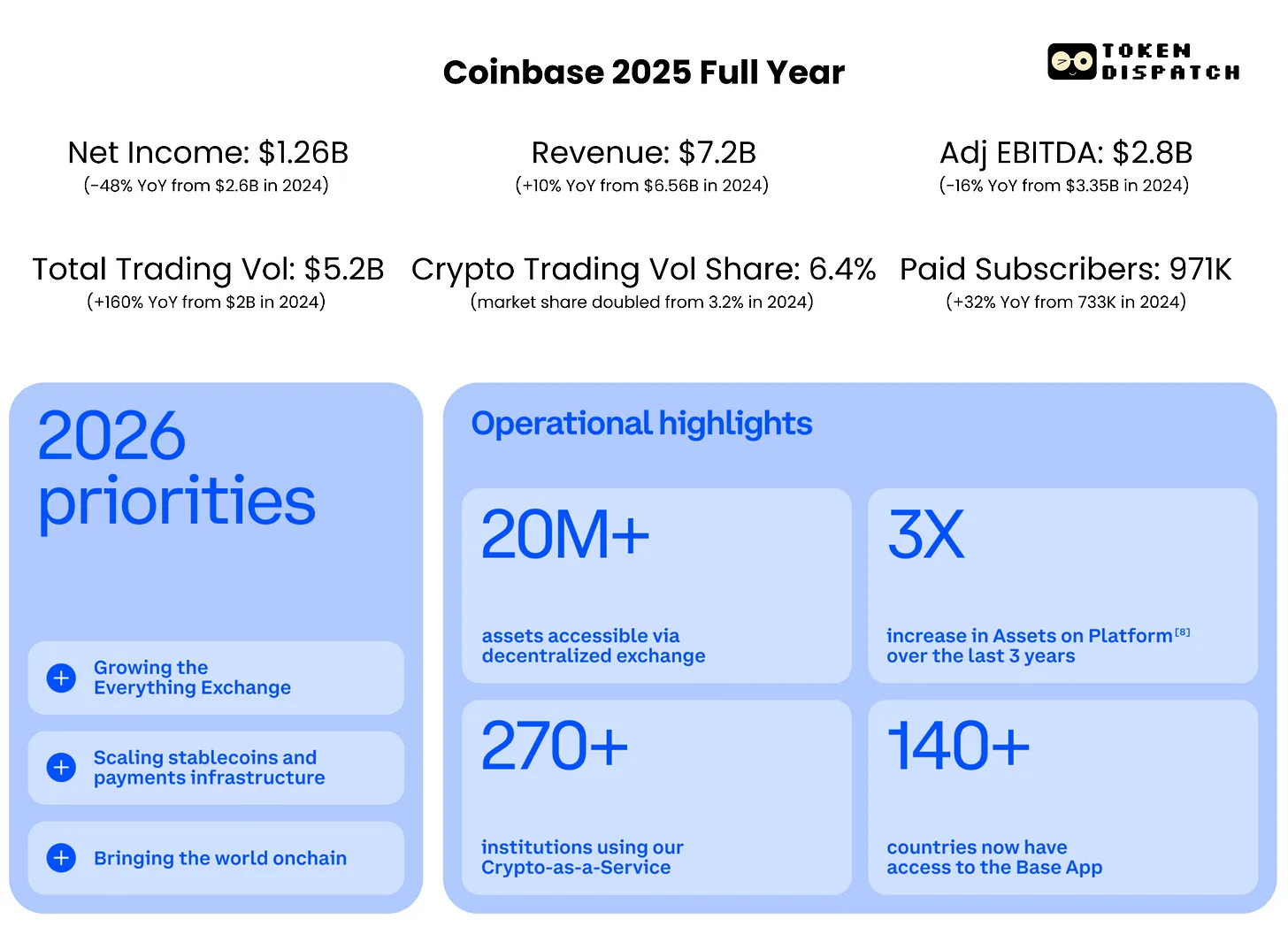

Coinbase reported a $667 million net loss for Q4 2025—a figure that may sound alarming at first glance. But numbers must be interpreted in context. That quarter, Coinbase recorded $718 million in unrealized losses on its crypto holdings and a $395 million impairment charge on its investment in Circle. Strip away those non-cash, mark-to-market losses, and Coinbase remains profitable on an adjusted basis—for 12 consecutive quarters.

The report shows $178 million in adjusted net income and $566 million in adjusted EBITDA.

While reassuring, there’s something else I find even more telling.

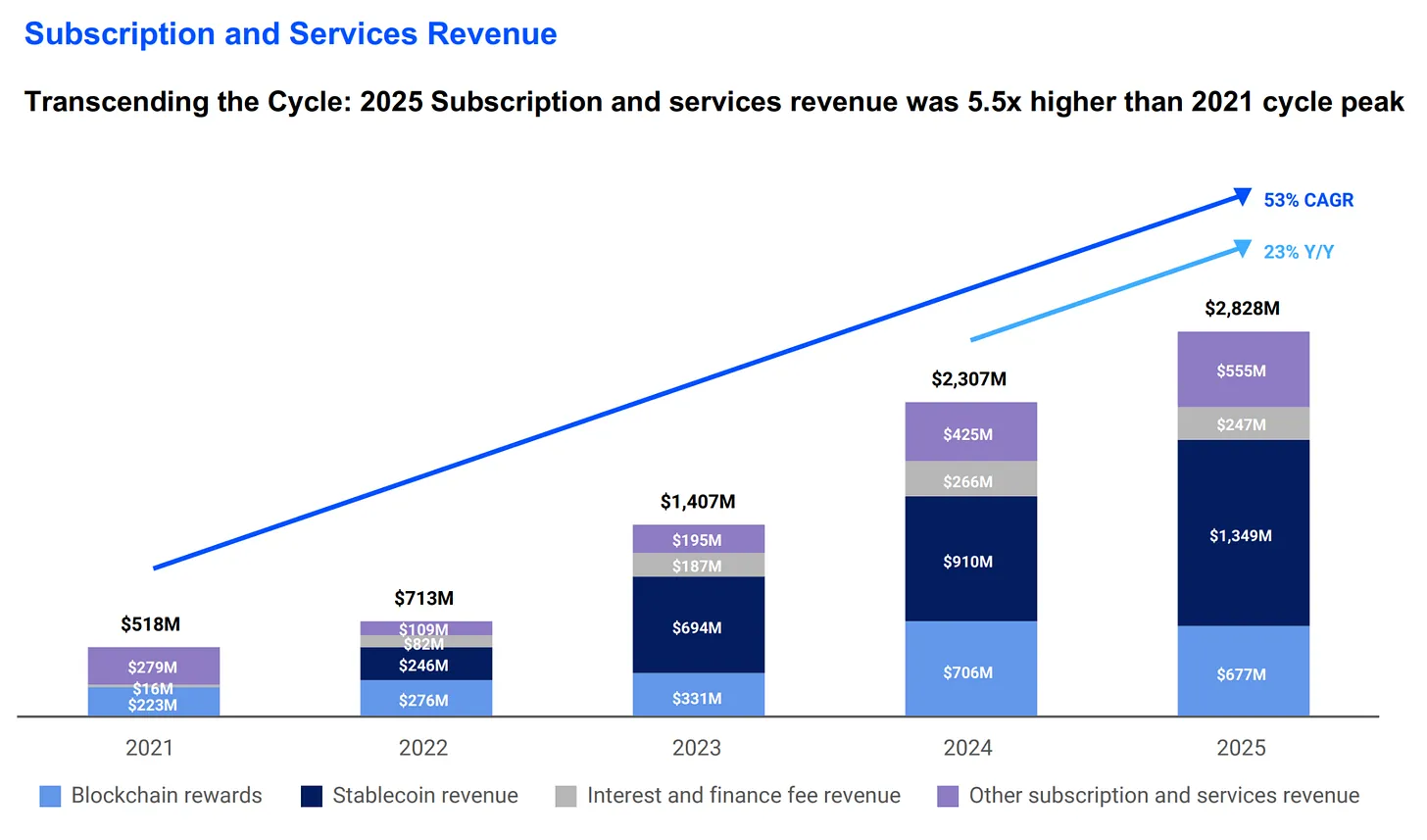

Coinbase’s Subscription & Services (S&S) revenue reached $2.8 billion in 2025—up 5.5x from its 2021 cycle peak and double its 2023 level. This signals broadening revenue foundations across stablecoins, custody, and blockchain rewards. In Q4, the value of USDC held on Coinbase products hit a record $17.8 billion—up 18% quarter-on-quarter. Today, Coinbase holds more crypto assets than any other company globally, representing 12% of all crypto assets worldwide.

However, this revenue stream is highly sensitive to interest rate changes. When rates—and crypto prices—fall, yield on stablecoins, staking rewards, and interest income on custody balances all decline. This sensitivity is evident in the company’s Q1 2026 guidance, which forecasts S&S revenue—including stablecoin and custody lines—to drop from $727 million in Q4 to $550–630 million.

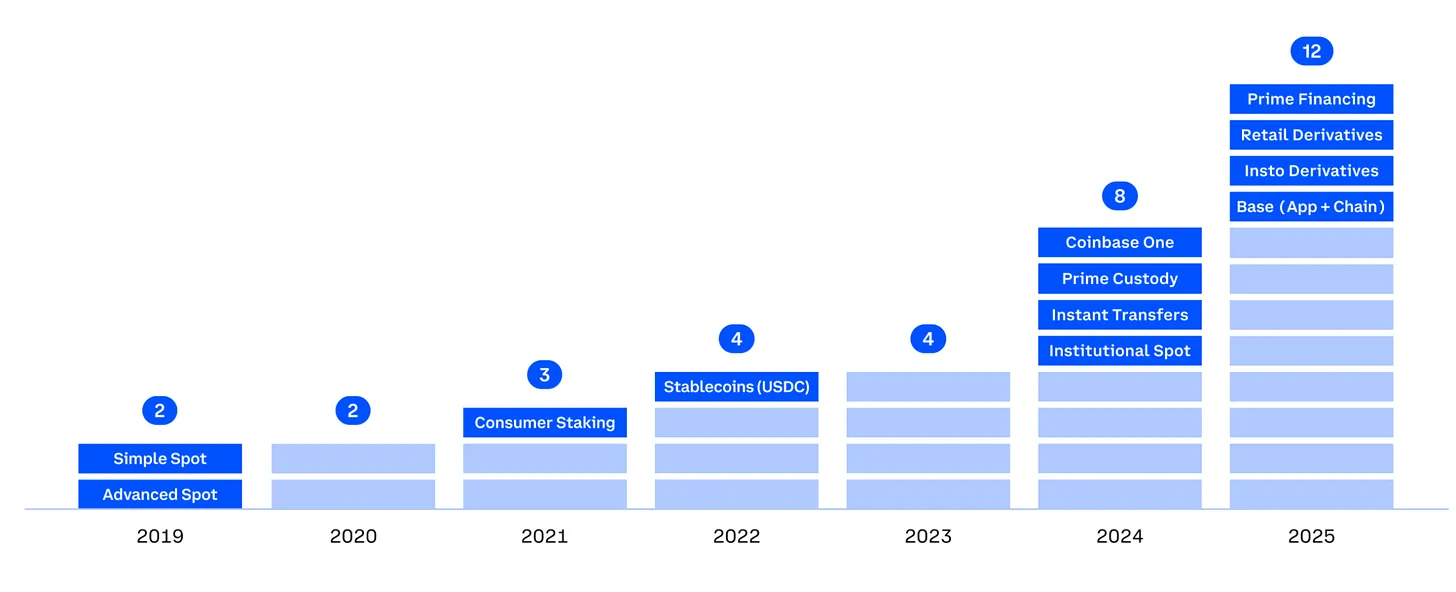

Coinbase’s systematic diversification across multiple business lines—reducing reliance on the crypto cycle—should bolster investor confidence. Today, Coinbase operates 12 business units generating over $100 million annually, six exceeding $250 million, and two surpassing $1 billion.

Coinbase’s acquisition of Deribit—the largest crypto acquisition ever—positions it to capture high-volume derivatives trading, especially during periods of extreme spot market volatility.

Coinbase’s “Everything Exchange” vision is increasingly manifesting beyond traditional finance. Earlier this week, Armstrong revealed on X that five of the world’s largest Global Systemically Important Banks (G-SIBs) are actively partnering with Coinbase.

JPMorgan has signed an agreement enabling customers to directly link bank accounts to Coinbase. BlackRock’s Bitcoin ETF custodial services run on Coinbase’s infrastructure. These initiatives signal Coinbase’s long-term ambition: to become the settlement layer institutions rely on as they move finance onchain.

Coinbase’s recently launched prediction markets follow the same retail-first playbook. Launched two weeks ago, they expand the “everything is tradable” vision by introducing event-based trading. This creates a new asset class, unlocks fresh revenue streams, and gives users stronger reasons to keep assets on Coinbase rather than migrating elsewhere.

Though short-term revenue from this new line may be modest, its strategic intent is unmistakable. How do I know? Prediction markets have already become Robinhood’s fastest-growing business line—that’s proof enough.

Now let’s turn to the other side…

Part II: Robinhood — Deep Consumer Engagement

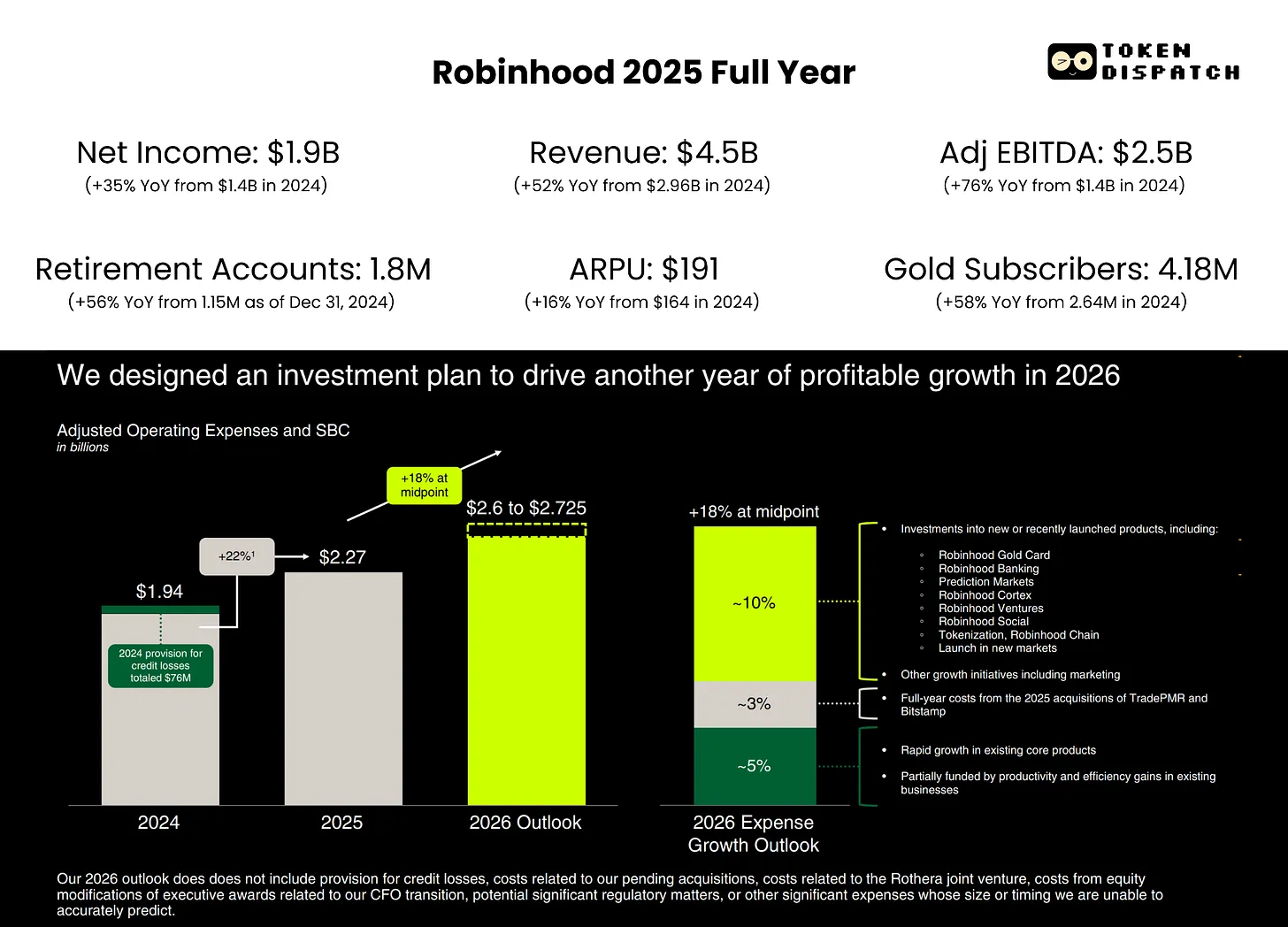

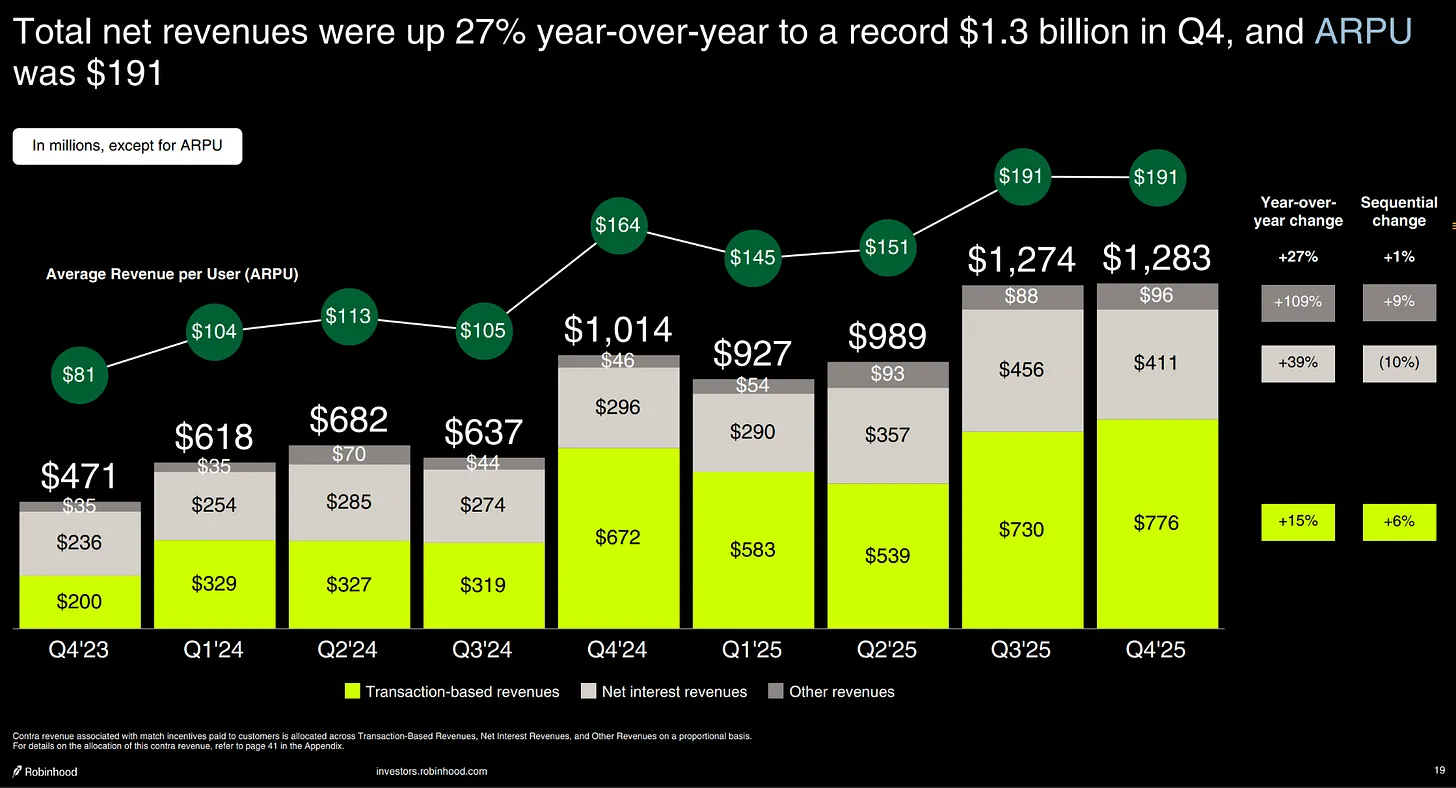

Robinhood’s Q4 results were actually quite solid—but punished for the wrong reasons. Revenue missed expectations due to lower crypto trading volume and the end of football season. To me, neither matters.

Most striking is its Average Revenue Per User (ARPU), up 27% year-on-year to $191—while paid users grew only 7%. This means Robinhood is extracting significantly more revenue per customer without needing rapid user growth. It reflects a far more diversified business model than the one it launched with in 2021.

Where does ARPU growth come from? Partly from its fastest-growing “Other Trading Revenue” line—up 300% to $147 million, driven primarily by prediction markets. Options revenue rose 41% to $314 million. Net interest income and Gold subscription growth also contributed.

Although transaction-based crypto revenue grew over 40% year-on-year in 2025, eight out of every $10 Robinhood earns still comes from non-crypto businesses—ensuring low exposure to crypto cycles.

A $300 Million Business

The strongest indicator of Robinhood’s future trajectory is its prediction markets. CEO Vlad Tenev calls this less-than-one-year-old product line the fastest-growing in Robinhood’s history—a statement that speaks volumes. In its first year, it achieved $300 million in annualized revenue and $12 billion in contract trading volume—an explosive pace clearly signaling what lies ahead.

Robinhood is doubling down on prediction markets through Rothera LLC, its joint venture with Susquehanna. Rothera acquired MIAXdx in January 2026. The deal gives Robinhood its own CFTC-registered exchange and clearinghouse—critical infrastructure allowing it to control pricing, contract selection, and economic models for these markets.

Even though the NFL season has ended, short-term tailwinds are keeping Robinhood’s prediction markets resilient. In January, NBA contracts traded on the platform surpassed NFL contracts. Government shutdowns also triggered a sharp spike in trading volume the same week the NFL season concluded. Later this summer comes the FIFA World Cup—right after the ongoing Winter Olympics. Beyond sports, Robinhood is building an entirely new non-sports vertical.

The Diversification Challenge

Beyond prediction markets—and Robinhood’s current profit engines like options, margin, and Gold subscriptions—other developments should further boost investor confidence. $HOOD is also building its next layer of distribution via private markets, family offices, and banking.

Robinhood Banking officially launched months ago for early customers. As of end-January, it had 25,000 paying customers and $400 million in deposits. Over half have enabled direct deposit—a development Tenev calls “the most encouraging sign.” It signals users are shifting their entire financial lives—not just experimenting—into the Robinhood ecosystem. Still, $400 million in deposits remains negligible relative to this $324 billion platform. Banking is a long-game endeavor, and Robinhood must prepare for the challenges ahead.

While the world races to build prediction markets, I believe private markets could be Robinhood’s ultimate differentiator—a space with few competitors. Tenev himself suggests private markets may scale “beyond prediction markets.” Robinhood Ventures—the company’s registered fund designed to give retail investors access to private companies—is not yet live. Last year, European users got a taste via tokenized stock giveaways for OpenAI and SpaceX—though those sparked controversy. Robinhood Ventures launches in the U.S. in 2026, with massive potential. Tenev repeatedly cites the ongoing $100 trillion intergenerational wealth transfer. If Robinhood captures even a sliver—especially as private assets shift from institutional to retail hands—it would fundamentally reshape its revenue profile.

A bigger challenge lies in managing customer expectations by drawing clear boundaries between tokenized equity and traditional equity.

Private markets may kick off as a revenue stream in 2026—but scaling will take time.

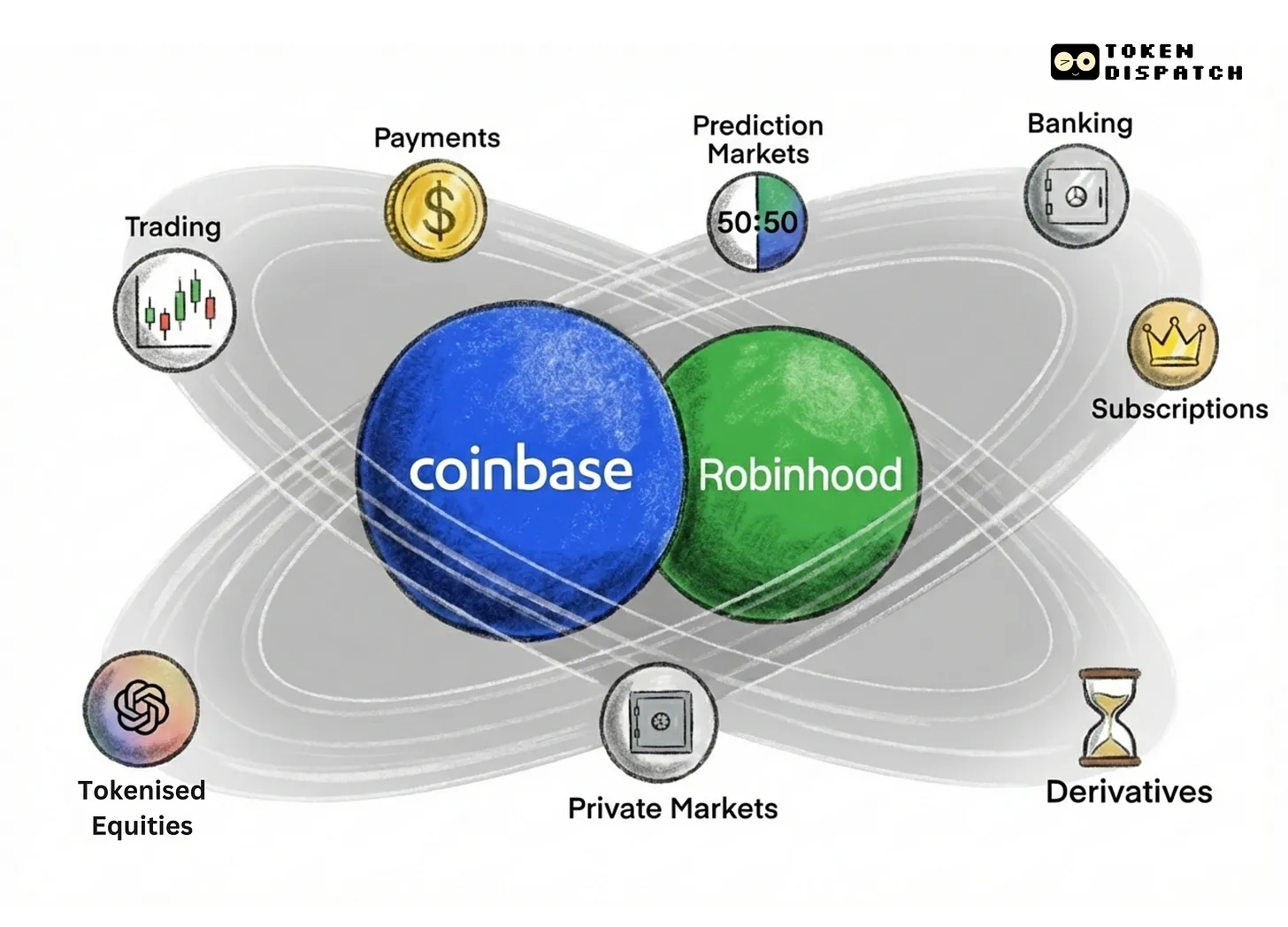

Same Destination, Different Timelines

At first glance, Coinbase and Robinhood appear to be following divergent paths. Indeed, they began at opposite ends of finance. Yet today, both are converging on the same vision: a financial super-app. Their recent evolution confirms this.

Robinhood entered finance the traditional way: commission-free stock trading, built for users who found legacy brokers too expensive and complex. For five years, it has layered crypto-native infrastructure atop traditional finance (TradFi). Today it offers margin accounts, Gold subscriptions, credit cards, banking products, a derivatives exchange, prediction markets, and tokenized strategies.

Coinbase was born in crypto—providing the most trusted way to buy, store, and trade digital assets when Wall Street largely shunned them. Over the past five years, it has expanded outward from its crypto-native core into consumer-facing TradFi products: stocks, subscriptions, credit cards—and now prediction markets.

They’re rapidly converging from opposite directions into the middle ground—where retail finance competition will play out over the next decade.

Prediction markets represent the clearest arena of head-to-head competition today. Robinhood leads here, having launched well before Coinbase’s offering—which debuted just two weeks ago. $HOOD owns its own exchange and clearinghouse; $COIN partners with Kalshi but has no exclusivity.

Tokenization will be another complex battleground. Coinbase treats it as an infrastructure problem—issuing tokenized equities in-house and forging regulatory relationships to enable onchain bonds and securities. Robinhood treats it as a consumer-access problem—opening up trading in tokenized shares of private companies. They’re solving different facets of the same challenge.

Private markets may become the third convergence point. Coinbase advanced here via its acquisition of Echo to enable onchain capital formation, while Robinhood takes its first step through Ventures—bringing private company investments to retail users.

Both companies understand that the broader market will trust whichever platform builds the deepest financial relationships and best meets investors’ evolving needs. Financial services are among the hardest categories for users to switch—people don’t easily change banks, brokers, or custodians. A platform that lets users manage retirement accounts, bank card details, prediction market positions, and eventually private equity portfolios will hold onto customers far more effectively than competitors trying to lure them away.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News