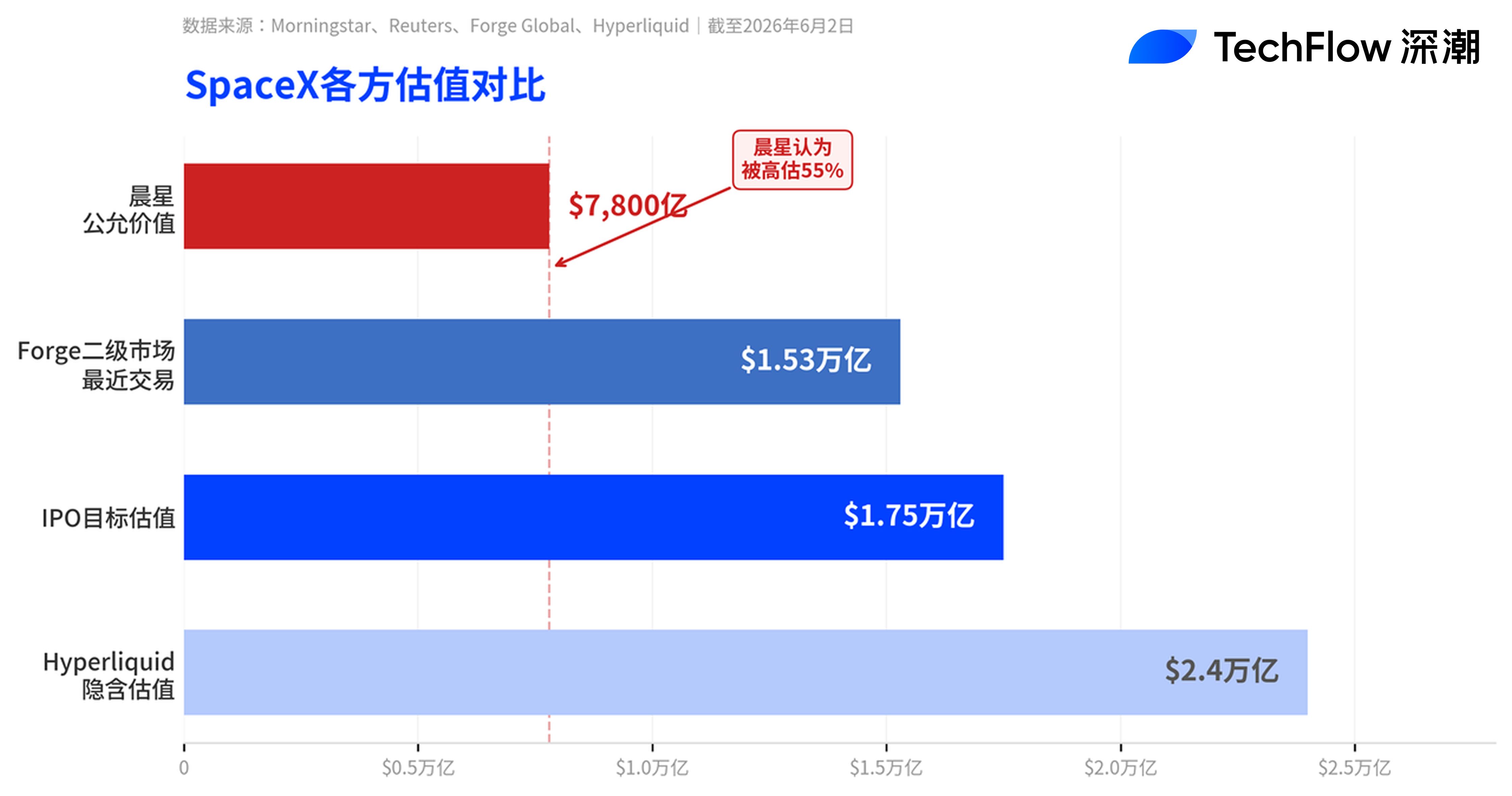

Morningstar values SpaceX at just $78 billion—less than half its IPO target—raising questions about whether the “largest IPO in history” is overpriced?

TechFlow Selected TechFlow Selected

Morningstar values SpaceX at just $78 billion—less than half its IPO target—raising questions about whether the “largest IPO in history” is overpriced?

SpaceX plans to launch its roadshow the week of June 8, price the offering on June 11, and begin trading on the Nasdaq under the ticker symbol SPCX on June 12.

Author: Claude, TechFlow

TechFlow Intro: SpaceX’s roadshow kicks off this week—but Morningstar has already thrown cold water on it. The research firm applied a DCF model to arrive at a fair value estimate of $780 billion, just 45% of SpaceX’s $1.75 trillion IPO target valuation. Analysts bluntly stated the company is “significantly overvalued.” Morningstar valued SpaceX’s core launch and Starlink businesses at $611 billion, assigning only a $17 billion probability-weighted valuation to its AI-related businesses (including xAI). Still, Morningstar acknowledged that SpaceX’s extremely low free float and Nasdaq-100 fast-track inclusion mechanism could push its stock price higher in the short term.

SpaceX is about to launch what may be the largest IPO in history—and one of Wall Street’s most prominent independent research firms has just doused it with cold water.

According to a Reuters report dated June 2, Morningstar issued its first-ever research coverage of SpaceX just ahead of the company’s planned roadshow launch this week, estimating a fair value of $780 billion—nearly halving SpaceX’s most recent secondary-market valuation of $1.53 trillion on Forge Global, and amounting to only about 45% of its $1.75 trillion IPO target valuation.

Morningstar equity analyst Nicolas Owens left no room for ambiguity: “We believe the company is significantly overvalued, and investors will have an opportunity to buy shares at a more attractive price after the IPO.”

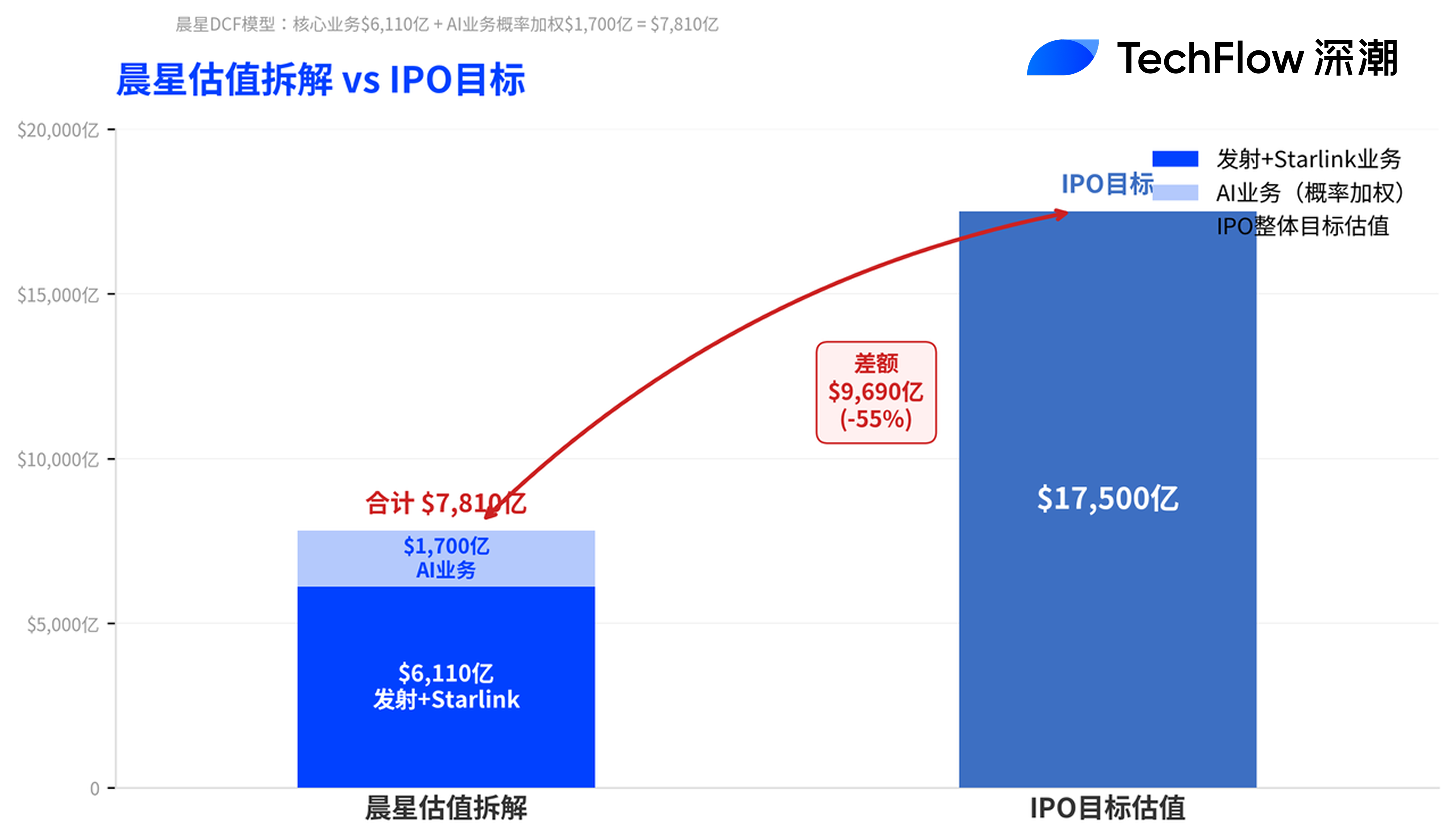

Where Does the $780 Billion Come From? Launch + Starlink = $611B; AI = Just $17B

Morningstar’s valuation breakdown reveals the crux of the disagreement.

Owens’ DCF model assigns a combined enterprise value of approximately $611 billion to SpaceX’s core launch business and Starlink satellite broadband operations. It assigns a probability-weighted valuation of roughly $17 billion to SpaceX’s AI businesses—including xAI and the social media platform X. Morningstar awarded SpaceX a “narrow moat” rating, citing cost advantages from reusable rockets and economies of scale from the Starlink constellation—but noted that SpaceX’s recently acquired AI businesses are dragging down its overall rating.

Regarding the AI business specifically, Morningstar modeled three scenarios: the most optimistic “moonshot” scenario carries a $130 billion valuation but only a 7% probability; the most pessimistic “non-viable” scenario would destroy over $81 billion in value and carries a 43% probability. Owens wrote: “We do not consider Grok one of today’s leading AI labs.” He also warned that the future prospects of SpaceX’s AI business hinge on unproven technologies such as orbital data centers.

Starlink’s fundamentals, by contrast, are relatively solid. According to its S-1 filing, Starlink’s 2025 revenue is projected to grow 50% year-on-year to $11.3 billion, with operating profit exceeding $4.4 billion and subscriber count surpassing 10 million—the only profitable segment within SpaceX today. Yet even so, at the $1.75 trillion valuation, SpaceX’s projected 2025 total revenue of ~$18.7 billion implies a price-to-sales (P/S) ratio approaching 100x.

Musk Responds from Afar: “Just Wait and See”

Facing valuation skepticism, Musk responded by invoking Tesla’s history. In a post early Tuesday morning on X, he wrote: “Tesla’s market cap at IPO was just 0.1% of its current value.” When users pressed him on how to justify a P/S ratio exceeding 50x, Musk replied with just three words: “You shall see.”

Yet the analogy faces obvious challenges. According to Yahoo Finance, Tesla’s current market cap stands at approximately $1.3 trillion, with a P/S ratio of ~15.7x and a P/E ratio nearing 400x. Even by Tesla’s already lofty valuation standards, SpaceX—despite generating far lower revenue—is seeking a higher market capitalization, implying a significantly steeper valuation hurdle.

Ed Elson, co-host of NYU Stern professor Scott Galloway’s podcast, used even sharper language. As cited by Motley Fool, he described SpaceX’s IPO registration documents in an article as “ unserious, hollow, hallucinatory, and nearly dishonest.”

Staggered Unlock + Nasdaq Fast-Track Inclusion: Short-Term Rally, Then Decline?

Although issuing a bearish valuation, Morningstar acknowledges SpaceX’s stock price may still rise in the short term post-IPO. Three factors underpin this view: extremely low initial free float (only ~3% of shares offered publicly), strong investor demand for AI infrastructure assets, and Nasdaq-100’s fast-track inclusion mechanism.

According to CNBC, Nasdaq introduced new rules on May 1 allowing ultra-large newly listed companies to enter the Nasdaq-100 Index just 15 trading days after their IPO—SpaceX qualifies fully given its expected valuation. Once included, all passive funds tracking the index will be compelled to buy shares, generating a wave of short-term index-inclusion buying pressure.

But medium-term selling pressure also warrants caution. SpaceX employs an unconventional staggered unlock structure: insiders may sell up to 20% of their locked shares upon release of the company’s first post-IPO quarterly report (covering April–June); if the share price rises more than 30% above the IPO price at that time, an additional 10% becomes unlocked. Thereafter, 7% unlocks on each of days 70, 90, 105, 120, and 135. Another 28% unlocks following the third-quarter report, with the remainder fully unlocked 180 days post-IPO. Elon Musk himself is subject to a 366-day lockup period.

According to the S-1 amendment filing, SpaceX has also reserved up to 5% of IPO shares for employees and designated executives—holders of these shares are exempt from standard lockup restrictions. Motley Fool analysis suggests investors need not rush into the IPO’s first-day trading; waiting until all lockup provisions expire and index inclusion is complete may prove wiser.

$20 Billion Bridge Loan and Governance Risks

Morningstar also flagged two structural risks.

First, much of SpaceX’s recent debt accumulation relates to AI infrastructure investments—$20 billion of which exists as bridge loans maturing 15 months post-IPO, posing refinancing risk. Morningstar expects SpaceX to raise $50–80 billion via the IPO, with part of the proceeds allocated to repay this loan.

Second, corporate governance concerns. Musk holds approximately 85% of voting power through a dual-class share structure. Additionally, the $25 billion acquisition of xAI earlier this year was not conducted at arm’s length—a related-party transaction that lifted SpaceX’s valuation from ~$1.5 trillion to its IPO target level, despite the AI business itself having yet to demonstrate economic viability.

SpaceX plans to launch its roadshow during the week of June 8, price the offering on June 11, and begin trading on the Nasdaq under the ticker SPCX on June 12. This will be the largest IPO in history—and possibly the most polarizing in recent years.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News