After Marvell’s Stock Surges 32%, the Chinese-American Chip Family Behind It Emerges

TechFlow Selected TechFlow Selected

After Marvell’s Stock Surges 32%, the Chinese-American Chip Family Behind It Emerges

Marvell’s stock surged to a new high, bringing into focus the top Chinese semiconductor family behind it—a family that has spent 30 years building a billion-dollar network poised to capture AI-driven profits.

Author: Ada, TechFlow

On June 2, Marvell surged 32.5% in a single day, closing at $290.79—its all-time high. Over the past 12 months, its stock has risen 265%. The immediate catalyst was Jensen Huang’s keynote at Computex, where he named Marvell’s custom ASICs and optical interconnects “core components of the AI data center architecture.”

It is already rare for a company to receive an on-stage endorsement from NVIDIA’s CEO. Yet this company was founded in 1995 by Weili Dai and her husband Sehat Sutardja—in their living room. Weili Dai is the youngest of the Shanghai-based Dai siblings—the “Dai Three”—and one of the key architects behind her family’s three-decade-long footprint across the global semiconductor industry.

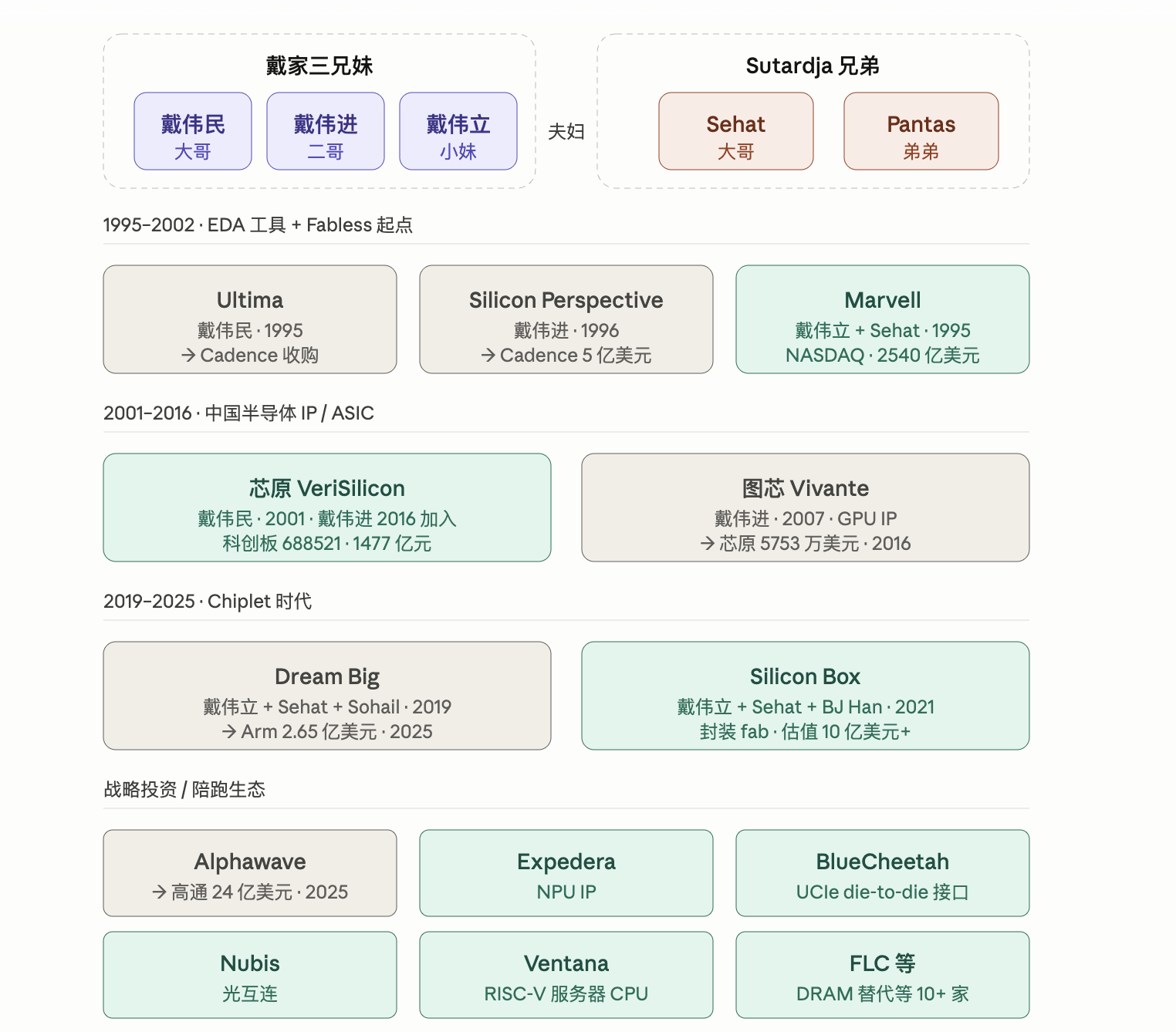

The eldest brother, Weimin Dai, is based in Shanghai and serves as Chairman of VeriSilicon—the A-share “first semiconductor IP company”—which had a market capitalization of approximately RMB 150 billion in 2026. Its AI ASIC orders have set new quarterly highs for six consecutive quarters. The second brother, Weijin Dai, currently serves as Director and General Manager of the IP Business Unit at VeriSilicon. In 2007, he founded Vivante, which VeriSilicon acquired for $57.53 million.

Looking back over three decades, the Dai siblings have launched six companies—two went public, four were acquired. That is only half the story. What truly flows beneath is a semiconductor-industry network woven by the marriage alliance between the Dai and Sutardja families—a network spanning from the U.S. to China, from EDA tools to advanced chiplet packaging fabs and production lines, and from IP licensing to AI SuperNICs.

The Three Siblings Placed Six Bets Over Thirty Years—Each Perfectly Timed

All three Dai siblings graduated in electrical engineering from UC Berkeley. Their entrepreneurial timelines align precisely with three major paradigm shifts in the semiconductor industry.

In 1995, Weili Dai, her husband Sehat Sutardja, and Sehat’s younger brother Pantas Sutardja co-founded Marvell in Silicon Valley, focusing on hard-disk storage controllers under a pure fabless model. In the same year, elder brother Weimin Dai founded Ultima in Silicon Valley, developing EDA tools. This was near the tail end of PC proliferation—fabless design and EDA tooling were defining features of the semiconductor industry’s first major restructuring. The Dais hit both targets simultaneously. Ultima was acquired by Cadence in 2000; Marvell went public the same year.

In 1996, Weijin Dai co-founded Silicon Perspective, specializing in digital implementation EDA tools. It was acquired by Cadence in 2002 for approximately $500 million. Around the same time, Weimin Dai turned his attention to China, returning to Shanghai in 2001 to found VeriSilicon (VeriSilicon), betting on the “IP licensing + one-stop chip customization” model to supply semi-finished chips to domestic SoC design startups just getting off the ground. That same year, China joined the WTO—and local chip design firms exploded from just over 100 to several thousand. VeriSilicon became the ammunition supplier for this wave.

In 2007, Weijin Dai founded Vivante, focusing on embedded GPU IP targeting automotive and IoT applications—just before the mobile internet boom, when every terminal began demanding graphics capabilities. In 2016, Weimin Dai’s VeriSilicon acquired Vivante outright for $57.53 million; Weijin Dai transitioned from Vivante CEO to General Manager of VeriSilicon’s IP Business Unit. This intra-family acquisition connected two critical threads: “China’s leading IP provider” and “embedded GPU IP.”

In 2019, Weili Dai launched her third venture. After leaving Marvell, she co-founded Dream Big Semiconductor in Silicon Valley with Sehat and former Marvell executive Sohail Syed, building open chip platforms and AI SuperNICs. In 2021, Weili Dai, Sehat, and Korean semiconductor veteran Han Byung Joon jointly founded Silicon Box in Singapore—an advanced chiplet packaging fab. Chiplets represent the industry’s sole viable path forward for boosting single-chip performance amid Moore’s Law slowdown—a bet squarely placed on the post-Moore era.

In August 2020, Weimin Dai’s VeriSilicon listed on the STAR Market, raising RMB 1.862 billion and earning the moniker “China’s first semiconductor IP stock.” In October 2025, Weili Dai’s Dream Big was acquired by Arm for $265 million in cash.

Over thirty years, six companies—two public, four acquired by top-tier buyers. An impressive record—but focusing solely on that record misses the true second half of the story.

An Industrial Foundation Built by Two Families

The founding trio of Marvell in 1995 consisted of Weili Dai, Sehat Sutardja, and Sehat’s younger brother Pantas Sutardja. Sehat was born in Jakarta, Indonesia; at age 13, he earned his amateur radio license. He received his Ph.D. in Electrical Engineering from UC Berkeley in 1988—and met and married Weili Dai there. From day one, Marvell was a joint venture of the Dai and Sutardja families—not merely a husband-and-wife startup.

This advantage amplified steadily over three decades.

The Dais possess deep roots in China’s semiconductor ecosystem. Weimin Dai’s VeriSilicon—the domestic IP leader—has collaborated with SMIC and Hua Hong since SMIC’s inception. VeriSilicon’s first standard cell library for SMIC’s 0.18-micron process solved SMIC’s early IP export-control challenges. Weijin Dai’s journey—from Silicon Perspective to Vivante and back to VeriSilicon—layered EDA expertise, GPU IP, and IoT customer networks into China’s indigenous SoC ecosystem.

Meanwhile, the Sutardja family’s engineering network, rooted in Marvell, extends across Southeast Asia and Europe. In 2021, Weili Dai and Sehat co-founded Silicon Box in Singapore with Han Byung Joon. By early 2024, the company had crossed the unicorn threshold and built a ~$2-billion advanced semiconductor packaging facility in Tampines, Singapore—and is constructing a $3.6-billion new factory in Italy. These two facilities reflect strategic alignment with Singapore’s Economic Development Board and Italy’s national industrial policy. Such East Asia–Europe capacity coordination cannot be achieved through the Dais’ mainland China relationships alone.

Even more revealing is the shared investment portfolio of the “Dai + Sutardja” families. Within the chiplet ecosystem, they have publicly invested in or co-founded at least 15 companies: Alphawave (high-speed SerDes interconnect IP, acquired by Qualcomm for $2.4 billion in December 2025); Expedera (NPU IP); BlueCheetah (UCIe die-to-die interface IP); Nubis (optical interconnect); Ventana (RISC-V server CPU); FLC (DRAM alternative). Combined with VeriSilicon, Vivante, Dream Big, and Silicon Box, these cover nearly every layer required in the chiplet era—semiconductor IP, interconnect standards, packaging fabs, and domain-specific compute chips. Together, the two families have constructed an entire industrial foundation for the post-Moore era.

Reproducing Marvell’s Rally Logic

What explains Marvell’s recent surge?

Over the past year, bottlenecks in AI data centers have quietly shifted. GPU compute shortages defined 2023–2024. But by late 2025—after hyperscale training and inference workloads ramped up—the real constraints became threefold: custom ASICs (to reduce reliance on NVIDIA’s general-purpose GPUs), high-speed interconnects between chips, and advanced packaging capability to integrate them into a single package.

Marvell has secured positions in the first two. It designs custom ASICs for Google and Amazon (e.g., TPUs) and supplies optical communication chips for high-speed transmission. That’s the real reason behind its 265% annual gain—and why NVIDIA itself invested $2 billion in Marvell in March. Jensen Huang needs that interconnect backbone, too.

Overlay the “Dai + Sutardja family” label onto the same diagram—and the picture transforms completely.

Dream Big bets on chiplet platforms and AI SuperNICs (800 Gbps bandwidth for lateral GPU interconnects). In October 2025, Arm announced its $265 million cash acquisition. Arm’s ambition is clear: to evolve from a CPU IP vendor into a “full-stack data center architect,” mirroring NVIDIA’s $6.9 billion acquisition of Mellanox in 2019.

Alphawave focuses on high-speed SerDes interconnect IP and is listed in London. On December 18, 2025, Qualcomm completed its $2.4 billion acquisition. The Dai + Sutardja family is Alphawave’s second-largest shareholder; Weili Dai realized ~$237 million from this transaction.

VeriSilicon operates domestically on the “IP + one-stop ASIC customization” model—the same business Marvell runs in the U.S., but serving Chinese AI chip buyers like Alibaba, ByteDance, and Cambricon. In 2025, AI compute accounted for 73% of newly signed orders; in the first four months of 2026, AI made up 91% of RMB 8.24 billion in new orders. Its market cap stands at ~RMB 147.7 billion (~$20.5 billion)—roughly 8% of Marvell’s size—but with steeper growth.

Silicon Box bets on chiplet advanced packaging fabs. It crossed the $1-billion valuation threshold in early 2024. The company remains private and unlisted—a cornerstone holding for the Dai + Sutardja family in the critical AI infrastructure capacity layer.

Plus over a dozen other invested or incubated companies—including Expedera (NPU IP), BlueCheetah (UCIe die-to-die interface IP), Nubis (optical interconnect), Ventana (RISC-V server CPU), and FLC (DRAM alternative)—each strategically positioned at one of those three “AI data center bottleneck” points.

Aggregating these assets conservatively, the two families’ AI-wave-related asset portfolio exceeds $22 billion. This figure does not appear on any official list—it’s dispersed across five jurisdictions, four corporate structures, and over a dozen companies—but it exists.

From a family-industrial-portfolio perspective, the two families have placed at least six independent bets in this AI data center wave—each highly aligned with Marvell’s current rally logic. Marvell is their most visible flagship—but far from their only entry ticket.

A Third Path: Building Critical Components at Standards Inflection Points

Today’s AI semiconductor landscape features two dominant narratives.

One centers on platform-scale giants capturing value: NVIDIA sells GPUs + CUDA ecosystem; Broadcom and Marvell sell custom ASICs + interconnects—territory reserved for players with >$150 billion market caps.

The other features independent ASIC startups pursuing IPOs: Tenstorrent, Cerebras, Groq, Etched—bypassing NVIDIA entirely to deliver domain-specific acceleration, betting on establishing a new pole outside the GPU-dominated universe.

The Dai + Sutardja family follows a third path: building critical components for open standards, establishing in-house packaging wafer fabs, and either awaiting acquisition by major players—or building domestic IP leadership. This path makes exceptional sense in the chiplet era, because chiplets themselves are a reaction against closed, vertically integrated architectures. With open standards, critical IP and packaging capacity become scarce resources—far quicker to monetize than going public with a full ASIC.

Yet the trade-off is clear: this path will not produce the next NVIDIA. It enables founders to exit gracefully multiple times while retaining long-term influence within the industrial ecosystem—but it does not place them atop the final podium of AI infrastructure leadership.

In 1995, Weili Dai and her husband launched Marvell from a Silicon Valley living room—then an unknown startup. Today, Marvell is a $254 billion AI data center star—though Weili Dai’s original equity stake has largely been exited over successive rounds. Simultaneously, however, she and her family hold stakes in VeriSilicon, Silicon Box, Alphawave (cash proceeds), Dream Big (sold to Arm for cash), and equity across a dozen chiplet-ecosystem companies.

Marvell is her loudest victory—but neither her only nor her final one.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News