Base's "Onchain Summer" has finally arrived

TechFlow Selected TechFlow Selected

Base's "Onchain Summer" has finally arrived

The boundary between on-chain and off-chain is being further blurred.

By shushu, BlockBeats

On June 18, the U.S. Senate officially passed the GENIUS Act, marking the first time the U.S. government has legislatively recognized the legitimacy of compliant crypto assets, ending the regulatory vacuum caused by the previously ambiguous jurisdictional boundaries between the SEC and CFTC.

Against this favorable regulatory backdrop, JPMorgan Chase and Coinbase both announced major developments on the same day—advancing initiatives in on-chain banking and tokenized securities—signaling a deepening integration between traditional finance and the crypto ecosystem.

JPMorgan's deposits can now go on Base

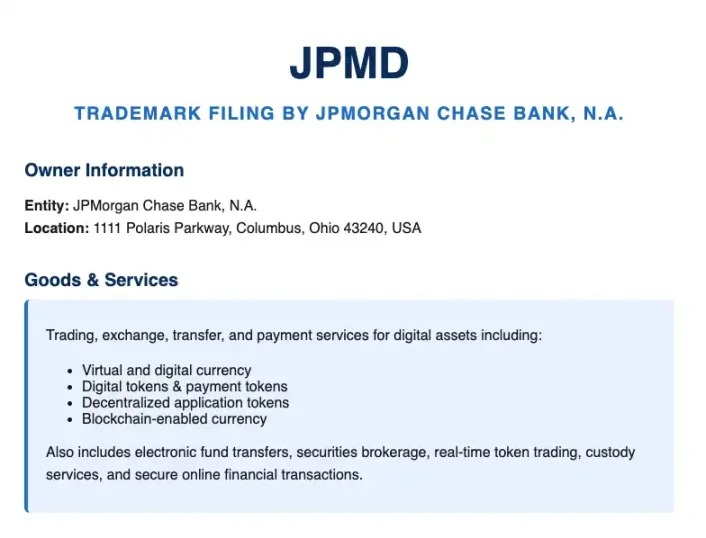

JPMorgan Chase, one of the earliest and most proactive traditional financial institutions in blockchain adoption, announced the launch of a pilot project called JPMD (JPMorgan Deposit Token). JPMD is an on-chain token representing customers’ U.S. dollar bank deposits, operating under a fractional reserve model, and will be deployed on Base, the public blockchain supported by Coinbase.

Naveen Mallela, Co-Head of Kinexys, JPMorgan’s blockchain division, said the bank will complete its first JPMD transfer within days—moving funds from its digital wallet to the Coinbase platform—to pave the way for institutional clients to use the token for on-chain transactions.

The pilot is expected to last several months, marking JPMorgan’s continued exploration of efficient, secure institutional-grade trading tools via on-chain deposit tokens. The day before the announcement, the bank had already filed a trademark application for "JPMD," covering digital asset payments, transfers, and transaction services—indicating its long-term strategic intent for the product.

JPMorgan’s decision to pilot JPMD on Base not only reflects confidence in Base’s security and transaction efficiency but also suggests that institutional clients may soon conduct on-chain fund settlements directly through the Base and Coinbase ecosystems. This would inject a core source of liquidity into Coinbase’s vision of building a “CeDeFi bridge.”

Why “deposit tokens”?

Although JPMD’s launch sparked speculation about JPMorgan entering the stablecoin market, Naveen Mallela, executive at Kinexys, clarified in a Bloomberg interview that deposit tokens are a superior alternative to stablecoins for institutional users due to their fractional reserve mechanism, which offers greater scalability.

He explained that deposit tokens represent actual U.S. dollar deposits held in customer bank accounts and operate within the traditional banking system. In contrast, stablecoins are merely digital representations of fiat currency backed by cash or equivalents, with legal status and operational logic more detached from the conventional financial system.

As the JPMD pilot launched, three key executives from JPMorgan held closed-door discussions with the SEC’s Crypto Task Force, discussing how capital market instruments could migrate onto public blockchains, the potential impact on market structure, and how institutions should evaluate risk and return models in on-chain finance.

According to meeting minutes released by the SEC, topics included digital repos, digital debt instruments, and on-chain financing. JPMorgan also stated it is actively assessing whether it can establish structural competitive advantages in asset tokenization and on-chain settlement efficiency.

Beyond meme coins: buying stocks on Base

In parallel with JPMorgan’s exploration of on-chain banking, Coinbase is evolving from an exchange platform into an infrastructure provider for on-chain assets. Paul Grewal, Coinbase’s Chief Legal Officer, revealed the company is seeking a no-action letter from the U.S. SEC to launch tokenized stock trading services for U.S. customers under exemption or authorization. A no-action letter would mean SEC staff would not pursue enforcement action against Coinbase for offering such services.

If approved, Coinbase would create an integrated asset flow loop on a single platform: “stablecoin purchase → on-chain settlement → stock trading → rewards-based spending.” This not only challenges brokerages like Robinhood and Charles Schwab for dominance in trading access but may also force them to consider integrating stablecoin payments and on-chain settlement, accelerating the entire securities industry’s transition into the era of on-chain assets.

Tokenized stocks promise faster settlement, extended trading hours, and lower operational costs. However, U.S. investors currently lack access to such products. Coinbase’s new initiative signals that it aims not only to become the “Nasdaq of crypto,” but also the on-chain gateway to traditional stock trading.

Coinbase’s move isn’t its first attempt in this space. As early as its S1 filing stage prior to going public in 2021, the company planned to tokenize its own stock (COIN), but the plan was shelved due to lack of SEC approval.

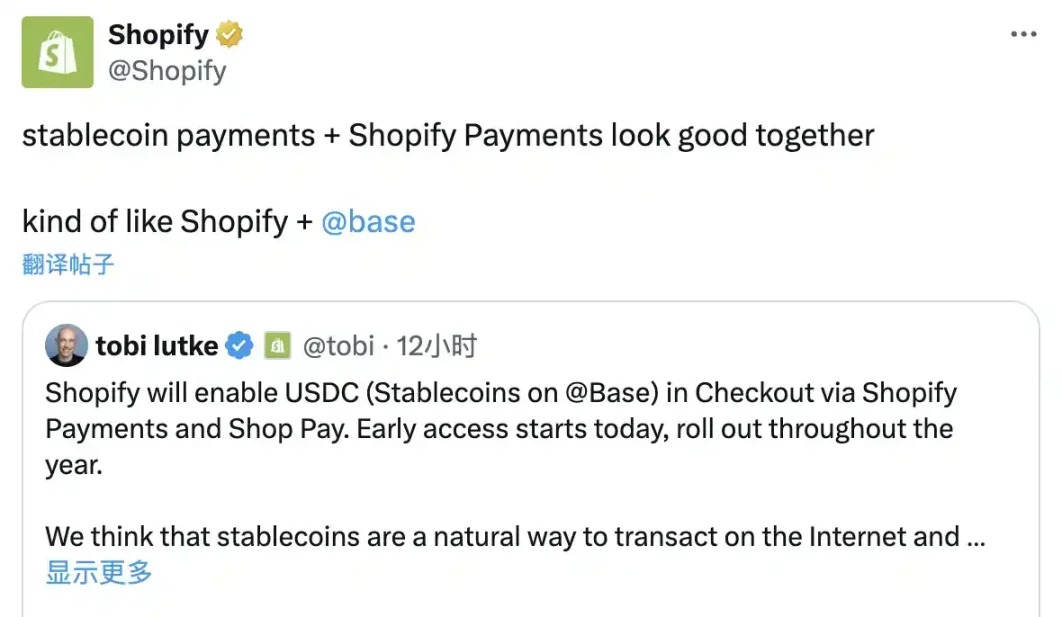

This latest effort marks Coinbase’s newest step to expand beyond crypto assets, aiming to open new revenue streams and drive deeper institutional adoption. Just last week, Coinbase launched a credit card powered by American Express and partnered with Shopify and Stripe to promote USDC stablecoin payments.

Regulatory uncertainty has long been the main barrier to widespread adoption of blockchain-based securities trading. But with the SEC increasingly engaging with DeFi and stablecoin frameworks, regulation appears to be a diminishing concern for Coinbase.

Meanwhile, competition is intensifying. Coinbase’s announcement follows Kraken’s launch of its xStocks project just weeks earlier, which already offers on-chain trading of over 50 stocks and ETFs to users in Europe, Latin America, Africa, and Asia. Coinbase needs faster and clearer regulatory pathways to stay competitive in this new race toward crypto-enabled brokerage services.

All for revenue

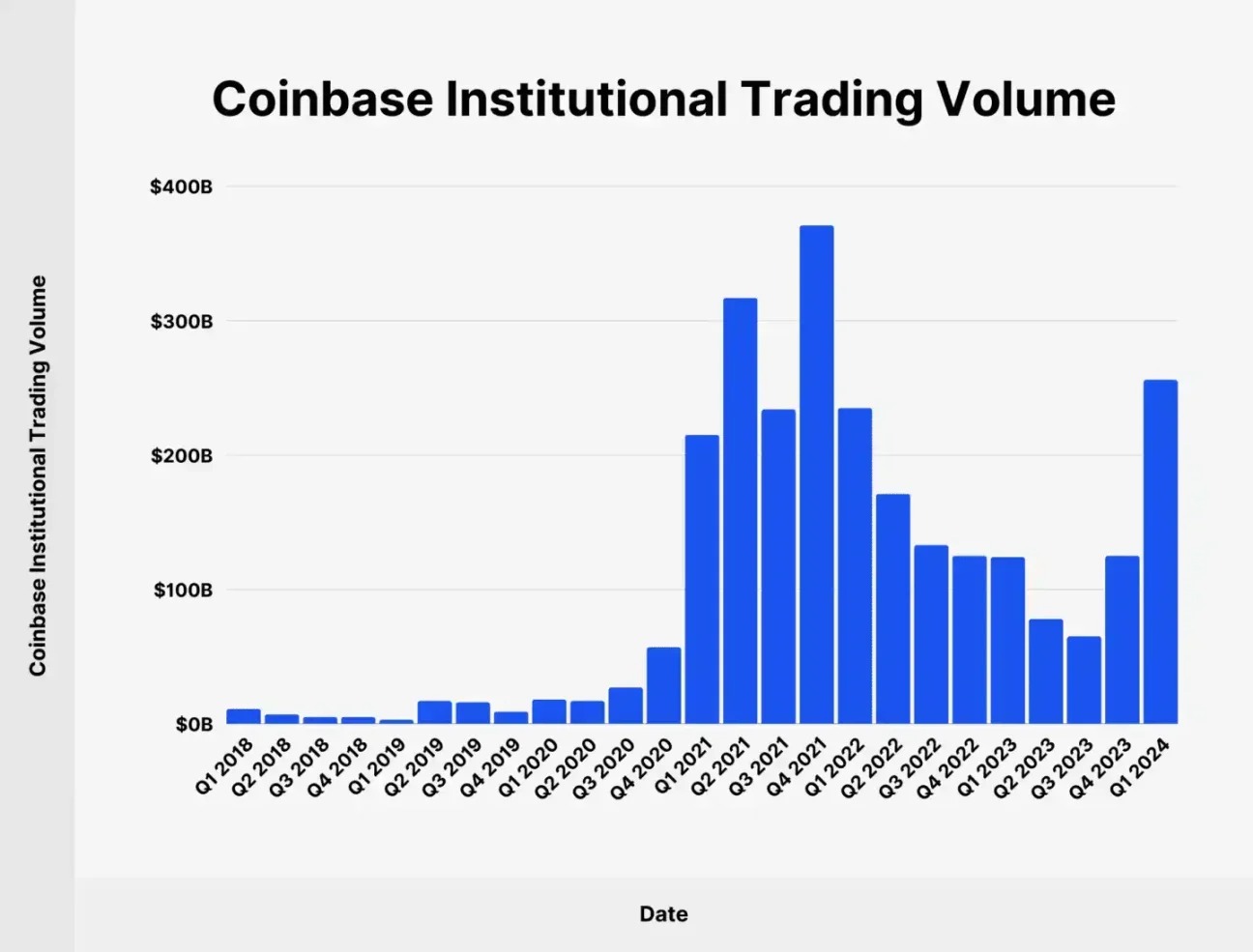

Data shows that retail trading accounts for only about 18% of Coinbase’s volume. Since 2024, institutional trading volume has steadily increased (reaching $256 billion in Q1 2024, or 82.05% of total volume). With Coinbase’s integration of DEXs on Base, tens of thousands of Base-native tokens are expected to gain significant liquidity. More importantly, numerous products in the Base ecosystem now have a viable path to connect with regulated off-ramp channels via Coinbase.

This month, Coinbase has taken multiple steps: partnering with Shopify to enable USDC payments on Base at e-commerce checkout, entering the cross-border stablecoin payment space; integrating Base’s DEX into the main Coinbase app to bridge flows between on-chain assets and CeFi users; and most disruptively, launching 24/7 perpetual futures trading in the U.S. under the CFTC regulatory framework.

These moves collectively point to one core goal: rebuilding Coinbase’s revenue model. As spot trading income declines year-over-year, Coinbase’s financial reports show its transaction revenues remain overly dependent on crypto market cycles. In this context, derivatives offer a more counter-cyclical income stream. By integrating Deribit’s liquidity and user base, Coinbase is building a global derivatives trading loop targeting institutional clients, while CFTC endorsement provides a compliance moat in the U.S. market.

At the same time, through partnerships with Shopify and Stripe, Coinbase is driving native usage of USDC in e-commerce payments. Consumers can pay with USDC at Shopify stores, while merchants can choose to settle in stablecoins or local currency. Leveraging smart contract custody and API modules on Base, the process requires no crypto expertise from either party, creating a highly scalable “compliant crypto payment engine.” Stablecoin transactions generate on-chain gas fees and clearing charges, opening up steady revenue streams from small businesses and cross-border e-commerce markets.

The Coinbase One Card, developed with American Express, uses cashback incentives to lock in user assets and further stimulate on-platform trading activity. While such products still face trade-offs between cost and yield, they reflect Coinbase’s broader strategy of integrating “financial services + consumer use cases” into a unified experience.

This multi-pronged approach is no coincidence. At a moment when regulatory tailwinds are emerging and on-chain settlement infrastructure is maturing, Coinbase is positioning itself as a central hub—linking DEXs, stablecoin payments, and derivatives trading—to build a multidimensional revenue network centered on compliance and diverse asset flows. This shift represents a pivotal moment in Coinbase’s transformation from a crypto exchange into an operating system for on-chain finance.

Whether it’s JPMorgan’s bank deposit-backed JPMD or Coinbase’s push into tokenized securities, both developments point to the same trend: on-chain finance is entering a phase of institutional restructuring driven jointly by regulation, infrastructure, and mainstream financial players.

The passage of the GENIUS Act, rising momentum around stablecoin legislation, and ongoing institutional experimentation in on-chain market infrastructure signal that crypto finance is no longer a fringe experiment, but an increasingly viable component of the global financial architecture. The boundary between on-chain and off-chain is being dismantled layer by layer by these early movers.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News