Is the Dollar Stablecoin Bill really a genius bill?

TechFlow Selected TechFlow Selected

Is the Dollar Stablecoin Bill really a genius bill?

BTC is like a black hole in the blockchain universe, exerting a powerful gravitational pull on dollar liquidity.

Author: Liu Jiaolian

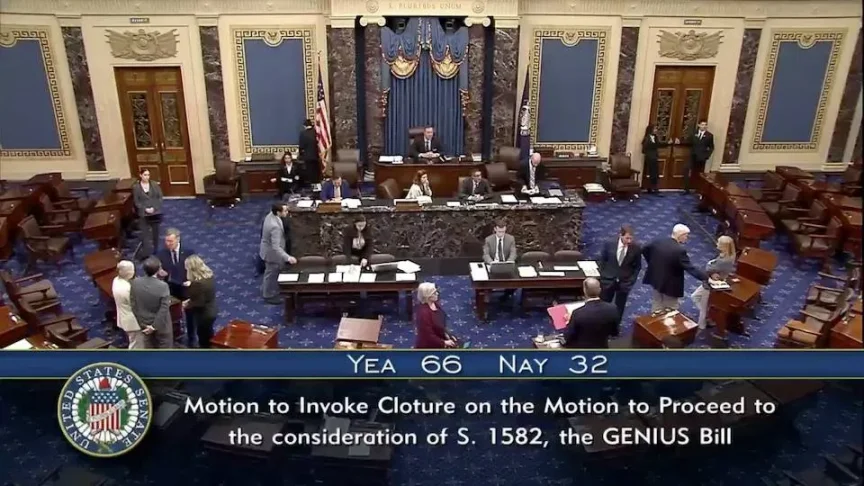

Recently, a major event has taken place in the crypto space: the U.S. Senate passed a procedural motion on the so-called dollar-backed stablecoin bill by a vote of 66 to 32, advancing it into the federal legislative stage.

The full name of this bill is the "Guiding and Establishing National Innovation for the U.S. Dollar Stablecoin Act," whose English acronym happens to be GENIUS, hence its nickname the "Genius Bill."

Financial and economic circles around the world are now buzzing with debate over whether this so-called Genius Bill represents the final desperate struggle before the total collapse of the U.S. dollar and Treasury bond system—or if it truly possesses genius-level insight that resolves the U.S. debt crisis while upgrading dollar hegemony to version 3.0.

As is well known, the original U.S. dollar was merely a voucher backed by gold. The United States established dollar hegemony 1.0 through its performance in World War II. The gold-backed dollar became part of the postwar world order, institutionalized via systems and organizations such as the Bretton Woods system, the World Bank, and the International Monetary Fund. Under Bretton Woods, the dollar was pegged to gold at a fixed exchange rate, while other countries’ currencies were linked to the dollar. (For further reading, see Liu Jiaolian’s “The History of Bitcoin,” Chapter 10, Episode 42)

However, just 25 years after the war, the U.S. could no longer maintain the dollar's anchor to gold. American economist Robert Triffin discovered that for the dollar to serve as an international currency, the U.S. must continuously export dollars abroad. Since dollars were tied to gold, exporting dollars equated to exporting gold, inevitably depleting U.S. gold reserves until they could no longer support the growing supply of dollars—leading to inevitable decoupling.

Specifically, the following three goals form an unattainable “impossible trinity”: first, maintaining a U.S. trade surplus and stable external value of the dollar; second, keeping sufficient U.S. gold reserves; third, maintaining a stable dollar value at $35 per ounce of gold. These three objectives cannot be achieved simultaneously—the so-called “impossible trinity.”

This inherent flaw is also known as the “Triffin Dilemma.”

In 1971, when President Nixon abruptly announced on television a unilateral termination of the agreement, declaring that the dollar would no longer be convertible into gold, it marked the onset of a collapse crisis for dollar hegemony 1.0. Without gold backing, the dollar’s value became precarious.

But destiny had a role to play. In 1973, Henry Kissinger became Secretary of State under President Nixon. He proposed the “petrodollar” strategy, persuading Nixon to fully support Israel during the Yom Kippur War (the Fourth Arab-Israeli War). Under intense U.S. military pressure, Saudi Arabia secretly reached a pivotal agreement with the U.S. binding oil, the dollar, and U.S. Treasuries:

-

Saudi oil would be priced and settled exclusively in U.S. dollars, requiring other nations purchasing oil to hold dollar reserves.

-

Saudi Arabia would invest its oil revenue surplus into U.S. Treasury bonds, creating a mechanism for dollar recycling.

Many people are misled by the surface meaning of “petrodollar,” claiming that dollar hegemony 2.0 shifted its anchor from gold to oil. But what a currency can buy has never been its anchor. A currency’s anchor is what constrains and supports its issuance.

From the perspective of commodity production, the petrodollar capital cycle goes: oil → dollar → U.S. Treasury.

But from the perspective of capital movement, this process becomes a pure capital appreciation loop: dollar → U.S. Treasury → dollar. Oil production is merely a byproduct of the capital cycle.

When China began its reform and opening-up at the end of the 1980s, the same dollar-Treasury capital cycle was applied to drive massive Chinese industrial production, achieving astonishing results. For this capital circuit, whether the byproduct is oil or industrial goods is ultimately irrelevant. Financial capital only cares about extracting profits continuously through high-speed circulation.

Now the U.S. no longer fears exporting dollars. Previously, exporting dollars meant exporting gold, but since the U.S. lacks alchemy, it couldn’t create gold out of thin air, quickly exhausting its gold stockpiles. Now, however, flooding the world with dollars simply means issuing more U.S. Treasuries—essentially IOUs written by the U.S. Treasury, which can be printed in unlimited quantities at will.

This marks the era of dollar hegemony 2.0—from the 1970s to the 2020s, roughly 45 years. This version of the dollar, rather than being a “petrodollar” or anything else, is fundamentally a debt dollar—essentially an IOU dollar.

The key to the debt dollar lies in firmly anchoring the dollar to U.S. Treasuries. Achieving this requires two conditions:

-

U.S. Treasury issuance, interest payments, trading, and all related mechanisms must be globally dominant—exhibiting the strongest discipline, most reliable systems, most credible repayment capacity, and highest liquidity.

-

The U.S. must possess the world’s strongest military deterrent force, compelling nations accumulating large dollar reserves to actively purchase U.S. Treasuries.

To this end, the dollar 2.0 system was designed as a checks-and-balances double-helix structure: the Treasury issues debt “disciplinedly” within congressionally approved debt ceilings but cannot directly issue dollars; the Federal Reserve controls monetary policy, issues dollars, and adjusts interest rates through open market operations involving Treasury securities.

Yet while dollar 2.0 solved the problem of gold scarcity, it introduced an even bigger flaw: any human-imposed constraint ultimately fails to restrain the desire to print money. Congressional approval is not an insurmountable barrier. From then on, the dollar embarked on an uncontrollable path of infinite debt expansion, swelling to a staggering $36 trillion within just a few decades.

After the Alaska meeting in 2020 ended on bad terms, the entire dollar 2.0 system nearly collapsed. Why? Because China slammed the table.

The massive pile of U.S. Treasuries resembles a towering domino stack, propped up at the base by just a few small tiles supporting the entire wobbling giant. Any sufficiently strong shock could trigger a collapse from the top down.

Even without external shocks, the sheer scale of U.S. debt is gradually becoming unsustainable, trapped in an ever-growing expectation of eventual collapse.

Thus, a genius solution emerged: the nascent dollar hegemony 3.0—the dollar-backed stablecoin. We might also call it blockchain dollar or crypto dollar.

It must be said that the U.S. remains far ahead in financial innovation. Clearly, if the on-chain dollar, i.e., the dollar stablecoin strategy, succeeds spectacularly, we may soon witness five earth-shattering transformations:

-

The Federal Reserve’s monopoly on dollar issuance will be dismantled. Dollar stablecoins become the “new dollar,” with issuance decentralized among numerous stablecoin issuers.

-

The U.S. Treasury assets on the Federal Reserve’s balance sheet will be absorbed. Stablecoin issuers will compete like sharks for U.S. Treasuries to serve as legally mandated reserves backing their stablecoins.

-

As increasing amounts of traditional dollar assets are tokenized on blockchains under RWA (real-world assets) or other labels, massive trading volumes between RWA assets and crypto-native assets (such as BTC) will generate enormous demand for dollar stablecoins, driving explosive growth in their scale.

-

As the transaction volume of “RWA assets – dollar stablecoins” grows explosively, the transaction volume of “traditional assets – dollars” will gradually be surpassed and fade into obsolescence.

-

As the dollar’s role as a medium in asset transactions diminishes, it will become a mere appendage within the closed loop of “U.S. Treasury – dollar – dollar stablecoin.”

The traditional U.S. Treasury-dollar issuance mechanism works as follows: the Treasury issues Treasuries into the market, absorbing dollars. The Federal Reserve issues new dollars and purchases Treasuries from the market, thereby injecting liquidity. This achieves indirect linkage, using Treasuries to back dollar issuance.

The dollar stablecoin issuance mechanism works differently: stablecoin issuers receive customer dollars and issue dollar stablecoins on the blockchain. Then, these issuers use the received dollars to purchase U.S. Treasuries from the market.

Let us illustrate this with semi-quantitative assumptions.

Traditional method: the Federal Reserve creates $100 million in new dollars, buys $100 million worth of Treasuries from the market, injecting $100 million in liquidity. The Treasury issues $100 million in Treasuries, absorbing $100 million in liquidity.

The problem arises when the Federal Reserve insists on its so-called policy independence and refuses to carry out Treasury purchases to inject liquidity. This puts significant pressure on Treasury issuance, forcing auction rates higher—an outcome clearly detrimental to future U.S. government debt repayment.

Now assume a sufficiently large dollar stablecoin ecosystem: a stablecoin issuer absorbs $100 million and mints $100 million in stablecoins. The issuer uses the $100 million to buy Treasuries, injecting $100 million in liquidity into the market. The Treasury issues $100 million in Treasuries, absorbing $100 million in liquidity.

Note that leverage loops are possible here. If in the future most tradable assets are tokenized as RWA assets, the $100 million absorbed by the Treasury will eventually flow into various RWA assets. Specifically, the Treasury spends $100 million, and institutions receiving those dollars convert all $100 million into dollar stablecoins via stablecoin issuers (here, $100 million in stablecoins are newly minted), using them to buy various RWA assets—or simply hoard BTC—thus returning the $100 million to the stablecoin issuers.

The stablecoin issuers, upon receiving this $100 million, can then purchase another $100 million in Treasuries, injecting fresh liquidity. The Treasury can then issue another $100 million in debt to absorb it. This cycle repeats endlessly.

At this point, we see that only $100 million is used as seed capital, yet it enables near-infinite issuance of both U.S. Treasuries and dollar stablecoins. Each cycle increases U.S. debt by $100 million and dollar stablecoins by $100 million. After N cycles, both increase by N × $100 million.

Of course, in reality, the loop isn’t 100% lossless. Some dollars won’t return to the stablecoin system. Assuming a 20% leakage rate, the total leverage multiplier is easily calculated as 5x—similar to the money multiplier in fractional reserve banking.

With current U.S. debt at $36 trillion, and assuming the Fed can no longer sustainably print (i.e., the existing dollar supply remains constant), dollar stablecoin recycling with a 5x leverage multiplier could expand the U.S. debt ceiling dramatically: 36 trillion × 5 = 180 trillion dollars.

The U.S. Treasury—i.e., the U.S. government—can then happily continue issuing debt without having to bow to the Federal Reserve!

The additional 180 - 36 = 144 trillion dollars in debt aren’t backed by dollars printed by the Fed, but by dollar stablecoins issued across various blockchains by stablecoin issuers.

The Federal Reserve’s dollar seigniorage is thus deconstructed and replaced by stablecoin issuers’ stablecoin seigniorage.

And once dollar stablecoins become widely used in cross-border or daily payments, the traditional dollar itself can step aside, fully reduced to a supporting role within the “U.S. Treasury – dollar stablecoin” loop.

What role does BTC play throughout this entire process?

Jiaolian offers an analogy: a black hole.

In the universe, black holes exert such powerful gravity that even light cannot escape.

BTC acts like a black hole in the blockchain universe, exerting immense gravitational pull on dollar liquidity, sucking value in irreversibly. Thus, dollar liquidity is continuously drawn into the blockchain universe and converted into dollar stablecoins. Dollars are then re-released as liquidity by swapping for Treasuries, fueling endless cycles.

However, if the massively inflated supply of dollar stablecoins cannot be sold globally—at least matching the corresponding economic scale—then the inevitable result is depreciation in the actual purchasing power of dollars or dollar stablecoins.

Currently, the total supply of dollar stablecoins remains far below one times the size of U.S. debt, estimated at less than $200 billion. Even multiplying $200 billion by 5 yields only $1 trillion; expanding that by another 36 times reaches current debt levels. Further exponential growth would be required to meaningfully expand the debt capacity.

Even using the earlier estimate of a 5x leverage multiplier, the compounded multiplication factor becomes 5 × 36 × 5 = 900—nearly 1,000x.

Given today’s ratio of ~$200 billion in stablecoins to ~$2 trillion in BTC market cap (a 10x relationship), if stablecoins successfully scale by 1,000x, BTC’s market cap could grow by 1,000 × 10 = 10,000x—from $2 trillion to $20 quadrillion. Consequently, one BTC could rise from $100,000 to $1 billion, meaning 1 satoshi equals $10.

Considering that much future liquidity may be diverted to RWA assets—unlike today’s market where BTC captures the vast majority of flows—we might apply a discount of 1/10 to 1/100 to the above figures: resulting in a BTC market cap of $200 trillion to $2 quadrillion, and a BTC price of $10 million to $100 million, or 1 satoshi equaling $0.1 to $1.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News