Report Interpretation: How Does the U.S. Treasury's Think Tank View Stablecoins?

TechFlow Selected TechFlow Selected

Report Interpretation: How Does the U.S. Treasury's Think Tank View Stablecoins?

Interpreting how stablecoins have evolved from "on-chain cash" into a significant factor influencing U.S. fiscal policy.

By: TechFlow

Stablecoins have undoubtedly been the hottest topic in the crypto market over the past week.

First, the U.S. GENIUS Stablecoin Bill passed a procedural vote in the Senate, followed by Hong Kong’s Legislative Council passing the Stablecoin Bill at third reading. Stablecoins have now become a significant variable in the global financial system.

In the United States, the future development of stablecoins not only affects the prosperity of the digital asset market but may also profoundly impact Treasury demand, bank deposit liquidity, and the U.S. dollar's dominance.

About a month before the GENIUS Act passed, the U.S. Treasury’s “think tank”—the Treasury Borrowing Advisory Committee (TBAC)—released a report thoroughly examining the potential implications of stablecoin expansion on U.S. fiscal and financial stability.

As a key component in shaping the Treasury’s debt financing strategy, TBAC’s recommendations directly influence U.S. Treasury issuance and could indirectly shape the regulatory path for stablecoins.

So, how does TBAC view the growth of stablecoins? Could this think tank’s perspective affect the Treasury’s debt management decisions?

We will use TBAC’s latest report as a starting point to explore how stablecoins have evolved from “on-chain cash” into a critical factor influencing U.S. fiscal policy.

TBAC, the Treasury’s Think Tank

First, a brief introduction to TBAC.

TBAC is an advisory committee that provides economic insights and debt management recommendations to the U.S. Treasury. Its members consist of senior representatives from buy-side and sell-side financial institutions, including banks, broker-dealers, asset management firms, hedge funds, and insurance companies. It is also a vital part of the Treasury’s debt financing planning process.

TBAC Meetings

TBAC meetings primarily provide financing advice to the U.S. Treasury and are a crucial component of its debt financing planning. The quarterly financing process includes three steps:

1) Treasury debt managers solicit input from primary dealers;

2) After meeting with primary dealers, Treasury debt managers seek recommendations from TBAC; in response to questions and discussion materials raised by the Treasury, TBAC issues formal reports to the Secretary of the Treasury;

3) Treasury debt managers make decisions on changes to debt management policies based on research and private-sector feedback.

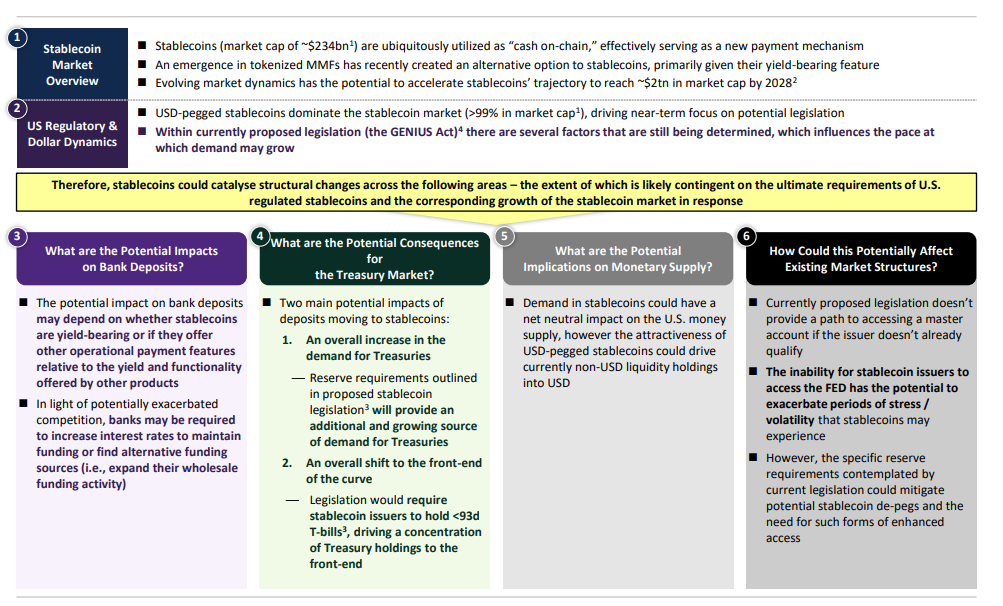

Report Summary: Impact on U.S. Banks, Treasury Markets, and Money Supply

-

Bank Deposits: The impact of stablecoins on bank deposits depends on whether they offer yield and their payment functionality relative to other financial products. Amid increasing competition, banks may need to raise interest rates to retain deposits or seek alternative funding sources.

-

Treasury Market: Overall Treasury demand increases, as reserve requirements in stablecoin legislation create an additional and growing source of demand for Treasuries; the overall maturity profile shifts shorter, since legislation requires stablecoin issuers to hold Treasury bills with maturities under 93 days, concentrating holdings in short-term instruments.

-

Money Supply: Stablecoin demand may have a net neutral effect on the U.S. money supply. However, the appeal of dollar-pegged stablecoins could shift existing non-dollar liquidity holdings toward dollars.

-

Impact on Existing Market Structure: Current legislative proposals fail to provide pathways for unqualified issuers to access master accounts. Without access to the Federal Reserve, stablecoin issuers may face heightened risks during periods of stress or volatility.

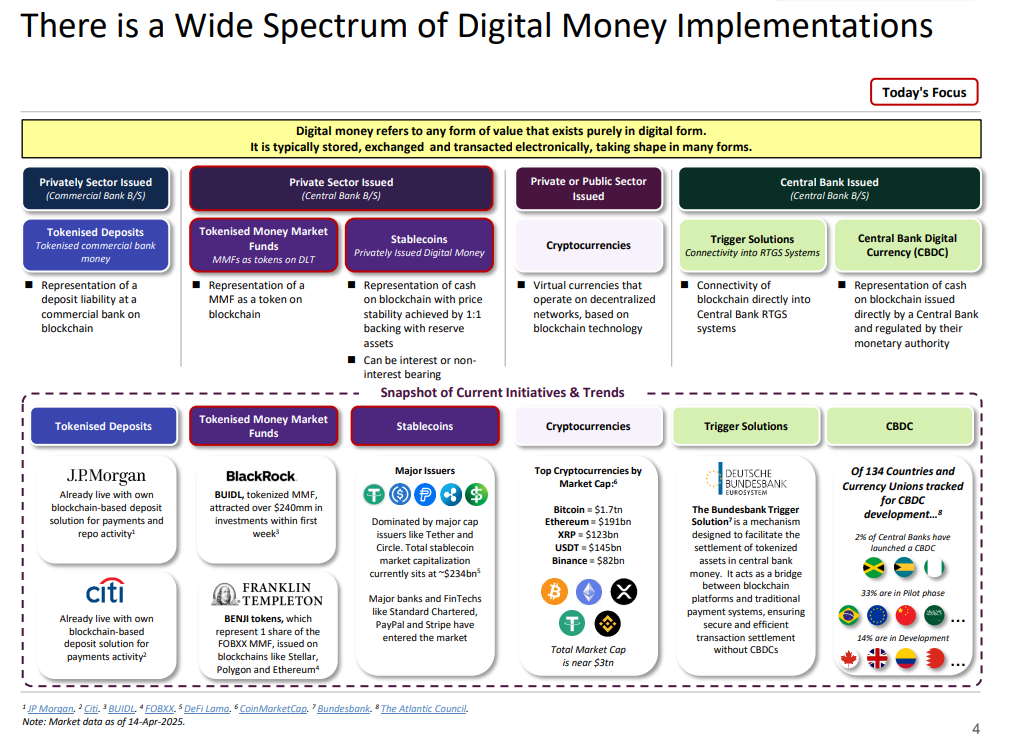

Digital Currency's Diverse Implementations: From Private Sector to Central Bank Perspectives

This chart presents a comprehensive view of digital currencies, illustrating their diverse implementation paths and real-world applications across various domains.

-

Classification of Digital Currencies

-

Private Sector Issuance (Commercial Bank Balance Sheets)

-

Tokenised Deposits: Blockchain representations of commercial bank deposit liabilities.

-

Tokenised Money Market Funds: Money market fund shares tokenized on blockchains.

-

-

Private Sector Issuance (Central Bank Balance Sheets)

-

Stablecoins: Blockchain-based forms of cash backed 1:1 by reserves, which may be interest-bearing or non-interest-bearing.

-

-

Private or Public Sector Issuance

-

Cryptocurrencies: Virtual currencies built on decentralized networks.

-

Central Bank Issuance

-

Trigger Solutions: Integration between blockchains and central bank Real-Time Gross Settlement (RTGS) systems.

-

CBDC (Central Bank Digital Currency): Blockchain-based forms of cash directly issued and regulated by central banks.

-

-

-

Current Market Trends

-

Tokenised Deposits

-

J.P. Morgan and Citi have launched blockchain-based solutions for payments and repo activities.

-

-

Tokenised Money Market Funds

-

BlackRock’s BUIDL has attracted over $240 million in investments.

-

Franklin Templeton launched the BENJI token, supported on Stellar, Polygon, and Ethereum blockchains.

-

-

Stablecoins

-

The market is dominated by major issuers like Tether and Circle, with a total market cap of approximately $234 billion.

-

-

Cryptocurrencies

-

Total market cap approaches $3 trillion, led by Bitcoin ($1.7 trillion) and Ethereum ($191 billion).

-

-

Trigger Solutions

-

A mechanism launched by the German central bank facilitates settlement between blockchain assets and traditional payment systems.

-

-

CBDC

-

Among 134 tracked countries and monetary unions, 25% have launched CBDCs, 33% are in pilot stages, and 48% remain in development.

-

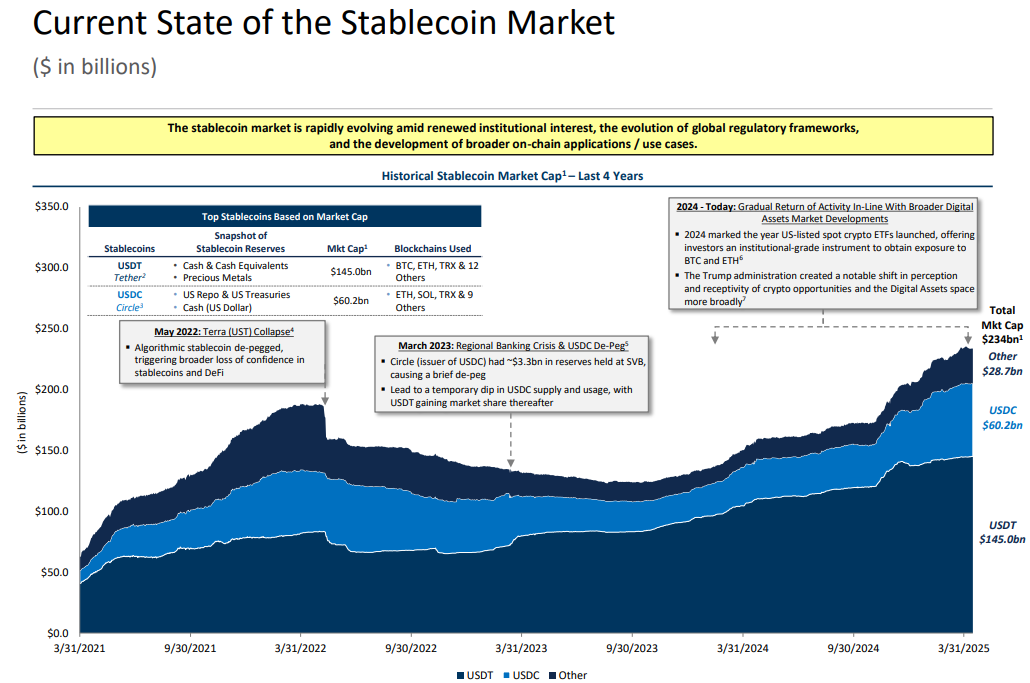

Current State of the Stablecoin Market: Market Cap and Key Events

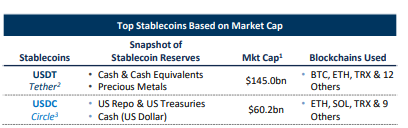

The stablecoin market has experienced notable volatility and growth in recent years. As of April 14, 2025, the total market cap reached $234 billion, with USDT (Tether) leading at $145 billion, followed by USDC (Circle) at $60.2 billion, and other stablecoins totaling $28.7 billion.

Looking back over the past four years, two major events marked turning points for the industry.

In May 2022, the collapse of algorithmic stablecoin UST triggered a crisis of confidence across the DeFi sector. UST’s de-pegging not only cast doubt on the viability of algorithmic stablecoins but also undermined confidence in other stablecoins.

Then, in March 2023, the regional banking crisis caused further turmoil. Circle, the issuer of USDC, had about $3.3 billion in reserves frozen at Silicon Valley Bank (SVB), causing USDC to briefly de-peg. This event prompted the market to re-evaluate the transparency and security of stablecoin reserves, while USDT further consolidated its market share during this period.

Despite these crises, the stablecoin market gradually recovered in 2024, aligning with broader developments in the digital asset space. In 2024, the U.S. launched its first spot crypto ETFs, providing institutional investors with tools to access BTC and ETH.

Currently, stablecoin market growth is driven by three main factors: increased institutional investor interest, gradual refinement of global regulatory frameworks, and continuous expansion of on-chain use cases.

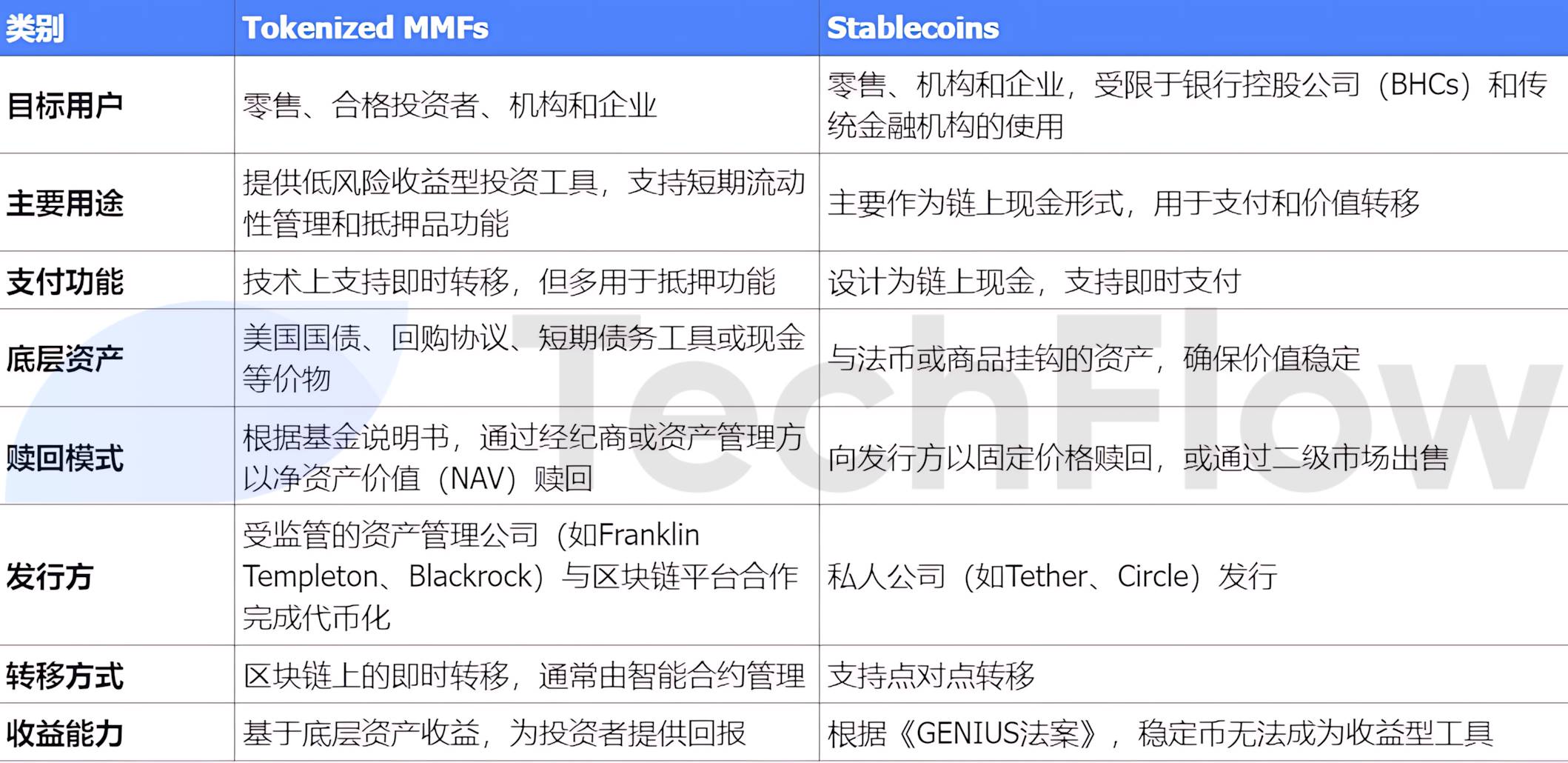

Tokenized Money Market Funds vs. Stablecoins: A Comparison of Two On-Chain Assets

With the rapid growth of tokenized money market funds (MMFs), an alternative narrative to stablecoins has emerged. Although both share similar use cases, a key difference lies in the fact that under the current GENIUS Act, stablecoins cannot serve as yield-bearing instruments, whereas MMFs can generate returns for investors through their underlying assets.

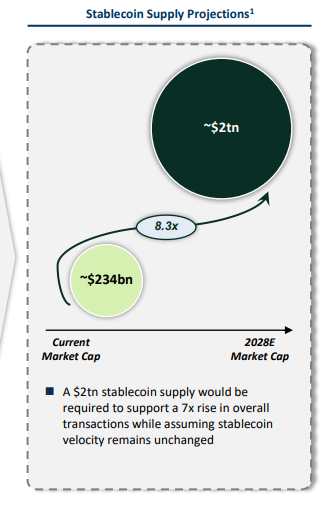

Market Potential: From $230 Billion to $2 Trillion

The report suggests that the stablecoin market cap could reach approximately $2 trillion by 2028. This growth trajectory depends not only on organic market demand but also on several key drivers, which can be categorized into adoption, economics, and regulation.

-

Adoption: Participation by financial institutions, migration of wholesale transactions on-chain, and merchant support for stablecoin payments are gradually pushing stablecoins toward mainstream payment and trading tools.

-

Economics: The value storage function of stablecoins is being redefined, particularly with the rise of interest-bearing stablecoins, offering holders income-generating potential.

-

Regulation: If stablecoins are incorporated into capital and liquidity management frameworks and banks are permitted to operate on public blockchains, their legitimacy and credibility will be significantly enhanced.

(Note: The stablecoin bill had not yet passed when the report was issued, though it had entered the voting stage.)

The stablecoin market is projected to grow from its current $234 billion to $2 trillion by 2028. This expansion requires a substantial increase in transaction volume, assuming stablecoin velocity remains constant.

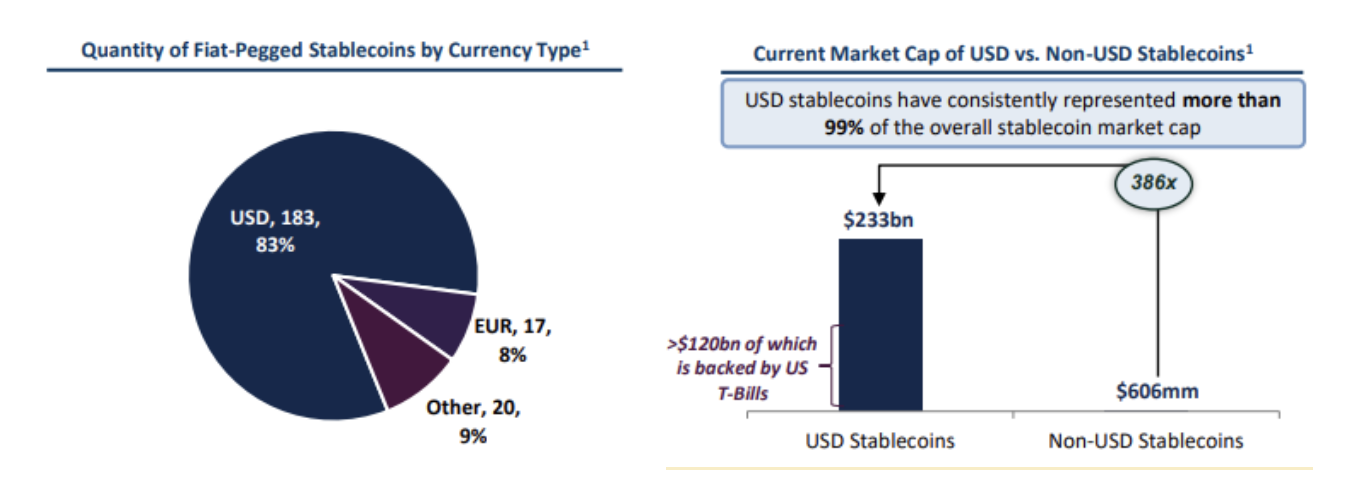

Dominance of USD-Backed Stablecoins

-

USD-backed stablecoins account for 83% of fiat-pegged stablecoins, far exceeding other currencies (EUR at 8%, others at 9%).

-

In the overall stablecoin market, USD-backed stablecoins represent over 99% of the market cap—$233 billion—with approximately $120 billion backed by U.S. Treasuries. Non-USD stablecoins total just $606 million.

-

The market size of USD-backed stablecoins is 386 times larger than non-USD stablecoins, underscoring their absolute dominance in the global stablecoin market.

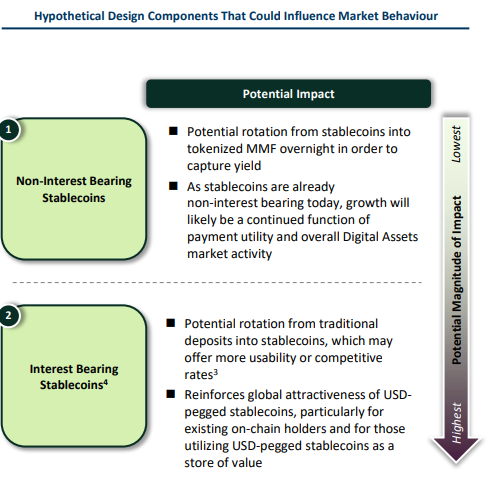

Potential Impact of Stablecoin Growth on Bank Deposits

Stablecoin growth could significantly affect bank deposits, with a key determinant being whether they pay interest.

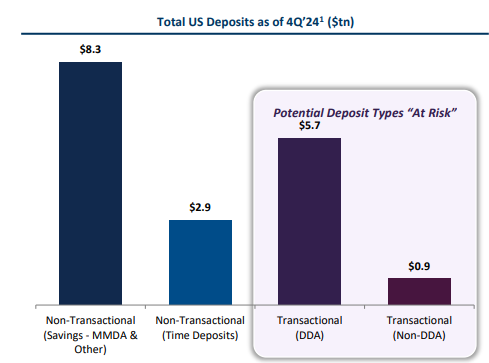

As of Q4 2024, total U.S. deposits reached $17.8 trillion, with non-transactional deposits (including savings accounts and time deposits) making up the majority at $8.3 trillion and $2.9 trillion respectively. Transactional deposits include checking accounts ($5.7 trillion) and other non-checking transactional deposits ($0.9 trillion).

Among these, transactional deposits are considered most “vulnerable” to disruption by stablecoins. These accounts typically earn no interest, are used for daily transactions, and are easily transferable. Uninsured deposits are often moved during periods of market uncertainty to higher-yielding or lower-risk instruments such as money market funds (MMFs).

If stablecoins do not pay interest, their growth will rely primarily on payment functionality and overall activity in the digital asset market, thus having limited impact on bank deposits. However, if stablecoins begin paying interest—especially offering higher yields or greater convenience—traditional deposits could see large-scale outflows. In this scenario, interest-bearing USD-pegged stablecoins would attract not only on-chain users but also serve as important value storage tools, further enhancing their global appeal.

In summary, the interest-bearing design of stablecoins directly determines their potential impact on bank deposits:

Non-interest-bearing stablecoins have relatively minor effects, while interest-bearing stablecoins could significantly reshape the deposit landscape.

Potential Impact of Stablecoin Growth on U.S. Treasuries

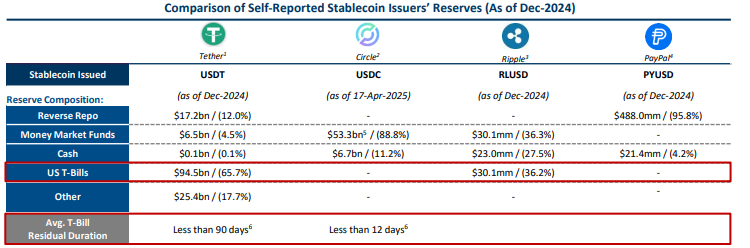

Based on publicly available reserve data, major stablecoin issuers currently hold over $120 billion in short-term Treasury bills (T-Bills), with Tether (USDT) allocating the largest share—approximately 65.7% of its reserves—to T-Bills. This trend indicates that stablecoin issuers have become significant participants in the short-term Treasury market.

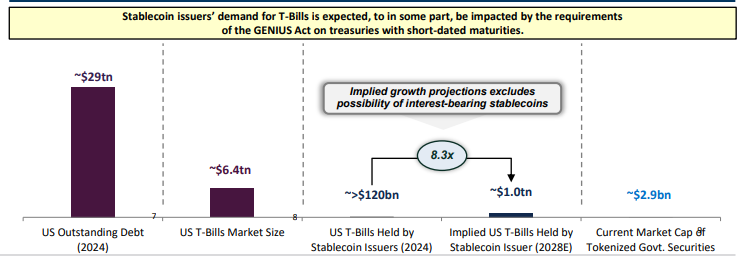

Going forward, demand for T-Bills by stablecoin issuers is expected to closely follow the expansion of the overall market.

In the coming years, this demand could add an extra $900 billion to short-term Treasury demand.

There is an inverse relationship between stablecoin growth and bank deposits. Large amounts of capital may shift from bank deposits to assets backing stablecoins, especially during market volatility or trust crises (such as stablecoin de-pegging), amplifying this movement.

The U.S. GENIUS Act’s requirement for short-term Treasuries could further drive stablecoin issuers to allocate more to T-Bills.

In terms of market size, stablecoin issuers held around $120 billion in T-Bills in 2024, potentially growing to $1 trillion by 2028—a 8.3-fold increase. By comparison, the current market size for tokenized government securities stands at just $2.9 billion, highlighting substantial growth potential.

In summary, stablecoin issuers’ demand for T-Bills is reshaping the ecosystem of the short-term Treasury market, though this growth may also intensify competition between bank deposits and market liquidity.

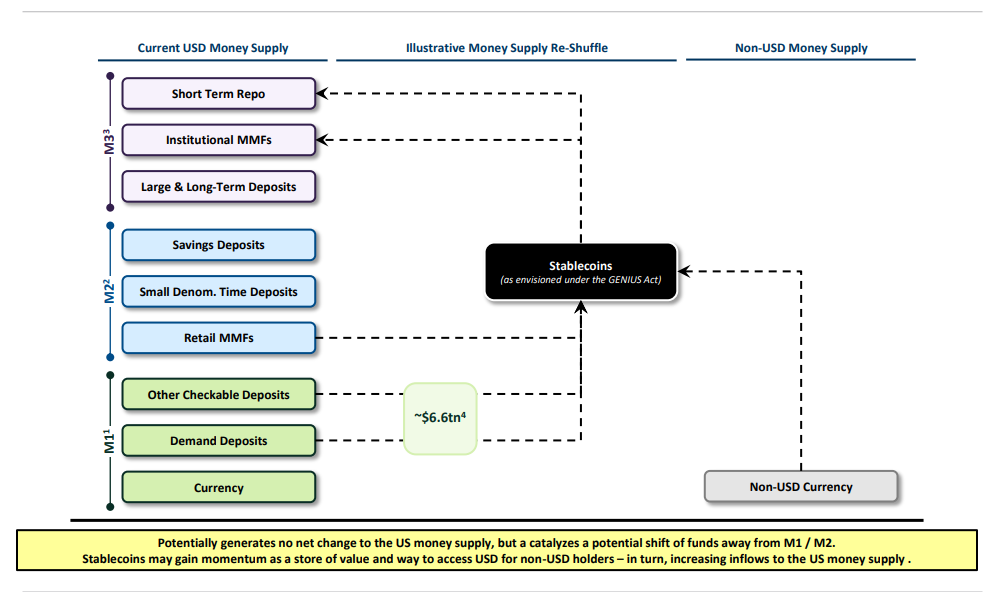

Potential Impact of Stablecoin Growth on U.S. Money Supply Expansion

The impact of stablecoin growth on the U.S. money supply (M1, M2, and M3) mainly manifests in potential fund flows rather than direct changes in total supply.

-

Current Money Supply Structure:

-

M1 includes physical currency in circulation, checking deposits, and other checkable deposits, totaling approximately $6.6 trillion.

-

M2 includes savings deposits, small time deposits, and retail money market funds (MMFs).

-

M3 includes short-term repurchase agreements, institutional MMFs, and large long-term deposits.

-

Role of Stablecoins:

-

Stablecoins are viewed as a new form of value storage, especially within the framework of the GENIUS Act.

-

Stablecoins may draw funds away from M1 and M2 into stablecoin holdings, particularly among non-U.S. dollar holders.

Potential Impacts

-

Fund Flows:

Stablecoin growth may not directly alter the total size of the U.S. money supply, but it could trigger capital shifts out of M1 and M2. Such movements may affect bank liquidity and the attractiveness of traditional deposits.

-

International Impact:

As a means of accessing U.S. dollars, stablecoins could increase non-dollar holders’ demand for dollars, thereby boosting inflows into the U.S. money supply. This trend may promote broader global usage and acceptance of stablecoins.

While stablecoin growth may not immediately change the total U.S. money supply, its potential as a store of value and medium for dollar access could have profound implications for capital flows and international dollar demand. This phenomenon warrants attention in policy-making and financial regulation to ensure financial system stability.

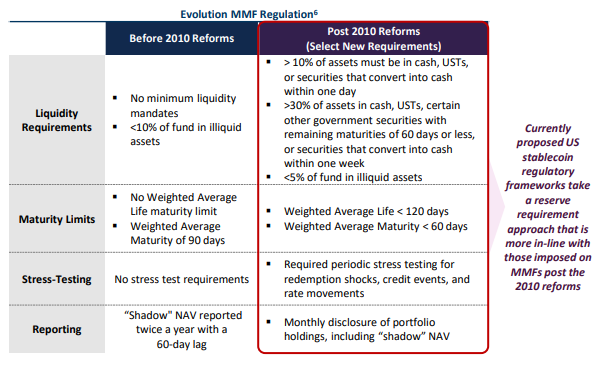

Possible Directions for Future Stablecoin Regulation

The current U.S. regulatory framework proposed for stablecoins resembles the post-2010 reforms for MMFs, focusing on:

-

Reserve Requirements: Ensuring high liquidity and safety of stablecoin reserves.

-

Market Access: Exploring whether stablecoin issuers should gain access to Federal Reserve (FED) support, deposit insurance, or 24/7 repo markets.

These measures aim to reduce the risk of stablecoin de-pegging and enhance market stability.

Conclusion

-

Market Size Potential

The stablecoin market is poised to grow to approximately $2 trillion by 2030, driven by ongoing market and regulatory breakthroughs.

-

Dominance of Dollar-Pegged Stablecoins

The stablecoin market is predominantly composed of dollar-pegged stablecoins, placing recent focus on potential U.S. regulatory frameworks and how legislation could accelerate stablecoin growth.

-

Impact and Opportunities for Traditional Banking

Stablecoins may disrupt traditional banks by drawing away deposits, but they also create opportunities for banks and financial institutions to develop innovative services and benefit from blockchain technology.

-

Far-Reaching Implications of Stablecoin Design and Adoption

The final design and adoption of stablecoins will determine their degree of impact on the traditional banking system and their potential to drive U.S. Treasury demand.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News