Polygon Founder: “We Are Already the World’s Largest Stablecoin Payment Chain—Others Are Still Releasing PowerPoint Presentations.”

TechFlow Selected TechFlow Selected

Polygon Founder: “We Are Already the World’s Largest Stablecoin Payment Chain—Others Are Still Releasing PowerPoint Presentations.”

While others are still pitching, real money has already flowed into functional infrastructure.

Author: Sandeep Nailwal

Translated by TechFlow

TechFlow Intro: Over the past few months, yet another wave of public blockchains has announced their entry into the payments space. But Polygon co-founder Sandeep Nailwal lets the data speak: $2.4 trillion in stablecoins have already settled on Polygon—and Revolut, Visa, and Meta have all chosen this chain. While others are still pitching, real capital has already flowed to infrastructure that actually works.

Over the past few months, I’ve repeatedly seen another chain announce its payments strategy—funding secured, roadmap published, testnet launched, long Twitter threads declaring “this time it’s finally happening.” Competition is healthy. When serious teams enter the field, the industry moves forward—I get that. But there’s a world of difference between announcing a payments strategy and becoming the chain where payments *actually run*. So let’s examine exactly where Polygon stands today.

Let’s start with the numbers.

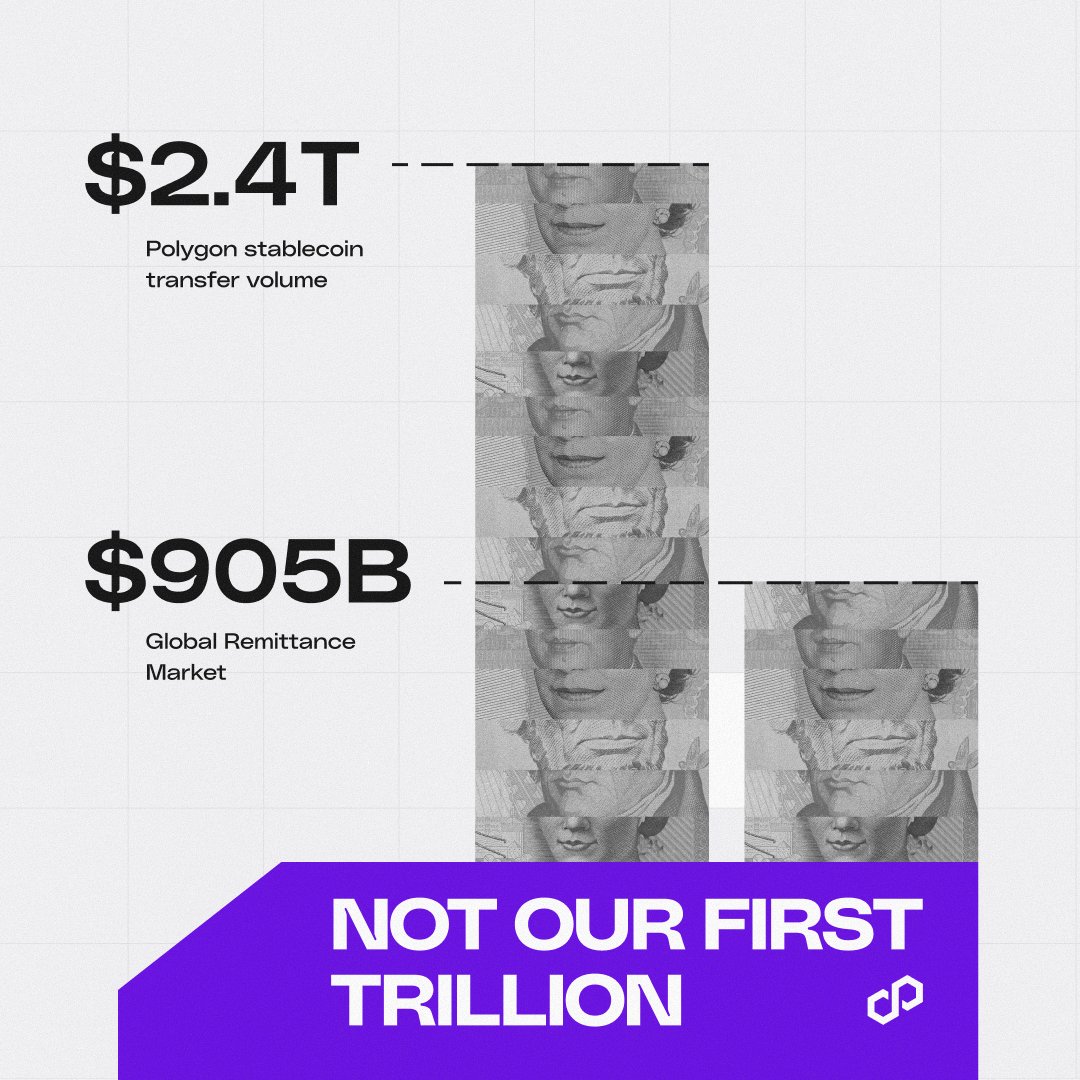

More than $2.4 trillion in stablecoin value has settled on Polygon—this reflects actual on-chain stablecoin transaction volume, not projections. Stablecoin activity on the network grew 264% year-over-year in 2025; in April 2026 alone, the chain processed over 577 million stablecoin transactions. By transaction volume, we are now the world’s largest chain for USD-pegged stablecoins, hosting a total of $3.6 billion in stablecoins on-chain.

This isn’t just a USD story. Approximately 89% of Latin America’s local-currency stablecoin on-chain activity runs on Polygon, and roughly 66% of Japan’s JPYC stablecoin activity occurs on our chain. Non-USD markets are significantly smaller in absolute scale—but wherever real-world currencies begin flowing on-chain as local-currency stablecoins, Polygon is where it’s actually happening.

Announcing a pivot to payments is one thing; watching fintech companies shift billions of dollars is something entirely different. We have receipts to prove it. Most chains rushing into this narrative today have no idea how long it truly takes to get here.

The names that have genuinely chosen to build on Polygon

If I simply list a bunch of logos here, it looks like marketing material—and tells you nothing. The real picture only emerges when you understand what these enterprises are *actually doing* with the chain, and why they chose Polygon specifically—not somewhere else.

Revolut has moved over $1.3 billion in stablecoin volume on Polygon—and they’re far from the only one operating at this scale. Paxos has processed approximately $1.3 billion in stablecoin payments on-chain via its enterprise payments platform, with monthly transaction volume growing 50x over the past 12 months. Beneath these numbers, this is no longer an experiment—it’s where their actual payment workflows live. The truly staggering part? The total gas fees for Paxos’s entire $1.3 billion in transaction volume amounted to less than $700. Anyone who’s spent time inside traditional payment infrastructure knows precisely how impressive that number is.

Then last week, three more major announcements landed. Visa—the world’s largest payments network—announced its partners can now instantaneously transfer funds for stablecoin settlement via Polygon’s rails. On the same day, Meta launched creator payouts on Polygon. And Modern Treasury—the payments orchestration layer that has already moved over $400 billion for enterprises—added Polygon as a native rail. Stablecoins now sit alongside ACH, wire transfers, RTP, and FedNow in the exact same API that enterprises already use. Household names and enterprise pipelines alike chose Polygon—all in the same week. I hear people say the Polygon payments story is overhyped. Meanwhile, the world’s largest corporations are now placing their trust on this chain. The market is overlooking it—for now. Not for long.

These names didn’t land on Polygon by accident. They evaluated their options. They chose this chain because it works—and continues to work, at scale, day after day.

Why they chose Polygon (this is the part I care about)

Enterprises choose infrastructure because it works—and stay because it keeps working, at scale. What “working” looks like on Polygon today boils down to a few things. Transactions confirm in seconds—often faster than Venmo confirms on your phone. Since the Rio upgrade launched in October 2025, the chain has experienced zero reorgs. For a payments chain, that’s the entire game—you simply cannot ask merchants or fintechs to bear the risk of settlement being reversed one minute after clearing.

We’re hitting over 2,800+ TPS today, with capacity for ~240 million transactions per day. We’re upgrading the network to payments-grade throughput—the kind Visa operates at. When I talk about fighting for the next order of magnitude, I mean it literally.

Fees on-chain have also become predictable enough to build a business around. Applications will be able to price against stable fees—just as they already do against card networks—so no more quoting one cost to customers and paying another at settlement.

Frankly, shipping velocity has been relentless. Three mainnet upgrades have shipped in the past four months—each laser-focused on what real payments businesses care about. The most recent Giugliano upgrade just went live, cutting finality by ~1.5 seconds. For platforms like Polymarket running at full load, this isn’t a superficial win—it’s visibly faster clearing under real-world load.

All of this transforms a chain from “fast enough for crypto” to something genuinely trustworthy for real-world payments. Every number reflects years of engineering work. Honestly, I’m proud of what the team has built.

The Open Money Stack

And even all of this still matters little—if enterprises can’t plug in and use it without first hiring a crypto engineering team. That’s the gap the Open Money Stack is bridging.

If you’re a finance team trying to move funds end-to-end, you need fiat on-ramps connected to banking systems, compliance tools covering KYC, AML, and sanctions—without custom-building for every jurisdiction—and wallets your users can actually use, plus stablecoin interoperability tying it all together. Without these layers, even the best settlement chain on Earth forces enterprises to connect five vendors and burn months on integration before sending their first dollar. That’s why most enterprise crypto projects die in procurement—and nobody talks about it.

So we built the Open Money Stack to bridge that gap. It’s one integration—not five: on-ramps, compliance, stablecoin interoperability, yield, and orchestration—all running on Polygon as the default settlement layer, with the finality and fee transparency financial teams actually expect from infrastructure. We intentionally built the chain first—because without a settlement layer that works the way enterprises need it to, none of the stack above it holds any value. You won’t put your business on rails that can’t carry it.

Where we go from here

New features will roll out for enterprises needing greater customization control. Throughput will push us to payments-grade speed. Cross-chain liquidity will launch via Agglayer. The Open Money Stack will become the default integration point for any enterprise wanting to move money on-chain—without building half the pipeline themselves.

Institutions building on Polygon choose us not because we’re the loudest chain in the space. They choose us because the chain works—when they need it to. And it keeps working, at scale. It’s a trust you earn slowly—and lose quickly. I think about that often. Every upgrade from here is about earning it again at the next order of magnitude—and then the one after that.

Crypto has waited ten years to reach true utility. Stablecoins are it. Payments are the use case. Polygon is going straight for it—until moving money on-chain feels as normal as swiping a card. That’s the only thing that matters now.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News