Facing the New Crypto Reality: HODL is Dead, DAOs are a Joke, Say Goodbye to DeFi

TechFlow Selected TechFlow Selected

Facing the New Crypto Reality: HODL is Dead, DAOs are a Joke, Say Goodbye to DeFi

"HODLing ETH is the biggest mistake I've made in this cycle."

Author: Ignas | DeFi Research

Translation: TechFlow

What fascinates me about crypto markets as part of finance and trading is how clearly they tell you whether you're right or wrong.

Especially in this chaotic world—where the lines between truth and lies are blurred in politics, art, journalism, and many other industries—crypto is refreshingly straightforward: If you're right, you make money; if you're wrong, you lose money. That's it.

Yet even so, I fell into a very basic trap: I failed to reassess my portfolio when market conditions changed. When trading altcoins (alts), I became overly complacent with "untouchable HODL" assets like ETH.

Of course, adapting to new realities is easier said than done.

There are too many variables to consider, so we often default to simple narratives like HODLing, because it frees us from actively monitoring the market.

But what if the era of HODLing is over? In this ever-changing landscape, what role does cryptocurrency play? And what have we missed?

In this blog post, I’ll share the major shifts I believe are happening in the market.

The End of the HODL Era

Let’s go back to early 2022:

ETH had settled around $3,000 after a sharp drop from its previous high of $4,800. BTC was hovering near $42,000. Then both dropped another 50% due to rising interest rates, the collapse of centralized finance (CeFi), and the FTX implosion.

Still, the Ethereum community remained optimistic: ETH was about to transition to PoS (Proof-of-Stake), and just months earlier, the EIP introducing ETH burning had launched. The narrative of ETH as “Ultrasound Money” and an environmentally friendly, energy-efficient blockchain was gaining strong traction.

However, for the remainder of 2022, both ETH and BTC underperformed, while SOL crashed catastrophically—down 96%, leaving it at just $8.

Ethereum won the L1 (Layer-1) war, while other L1s either migrated to L2s or faced extinction.

I remember attending bear market conferences where most attendees firmly believed ETH would rebound the strongest. They piled into ETH, underweighting BTC and completely ignoring SOL. The strategy was simple: HODL, then sell at the top of the 2024/25 bull run. Easy.

Reality slapped us hard!

SOL rebounded afterward, while Ethereum faced its worst fear, uncertainty, and doubt (FUD) in history.

The “Ultrasound Money” narrative is dead (at least for now), and the environmental (ESG) narrative never truly took off.

HODLing ETH was my biggest mistake this cycle. I believe it’s a shared regret among many.

My bullish thesis on ETH was that it would become the most productive asset in crypto.

Through restaking, ETH would gain “superpowers,” securing not only Ethereum but also critical DeFi and crypto infrastructure. Restaking yields on ETH would surge, and airdrop rewards would accumulate continuously via restaked ETH.

With rising yields, demand and price for ETH should logically increase. In short: To the moon!

Clearly, that didn’t happen—because the value proposition of restaking was never clearly demonstrated, and Eigenlayer underdelivered on its token launch.

So, what does this have to do with the death of the HODL metaverse?

For many, ETH has always been a “buy-and-forget” asset. If BTC rises, ETH usually rallies harder, making holding BTC seem pointless.

When my restaking-driven bullish thesis on ETH failed to materialize, I should have recognized it and adjusted my strategy. Instead, I grew lazy and complacent, unwilling to admit I was wrong. I told myself: ETH will bounce back someday, right?

HODLing is bad advice not just for ETH—but for nearly every asset, with perhaps one exception: BTC (more on that later).

Crypto markets move too fast to realistically expect retiring after holding an asset for months or years. Chart analysis shows most altcoins have given back their gains from this bull cycle. Clearly, profits come from selling—not holding.

A successful memecoin trader once said he typically holds a memecoin for less than a minute instead of HODLing.

Even though some still try to sell you the HODL dream, what we’re seeing is more of a “quick in, quick out” cycle rather than true HODLing.

BTC Is the Only Macro Crypto Asset

The only exception to the “quick in, quick out” approach is BTC.

Some attribute BTC’s strong performance to Michael Saylor’s “infinite buy order,” as we’ve successfully marketed BTC as “digital gold” to institutional investors.

Yet the battle is far from over.

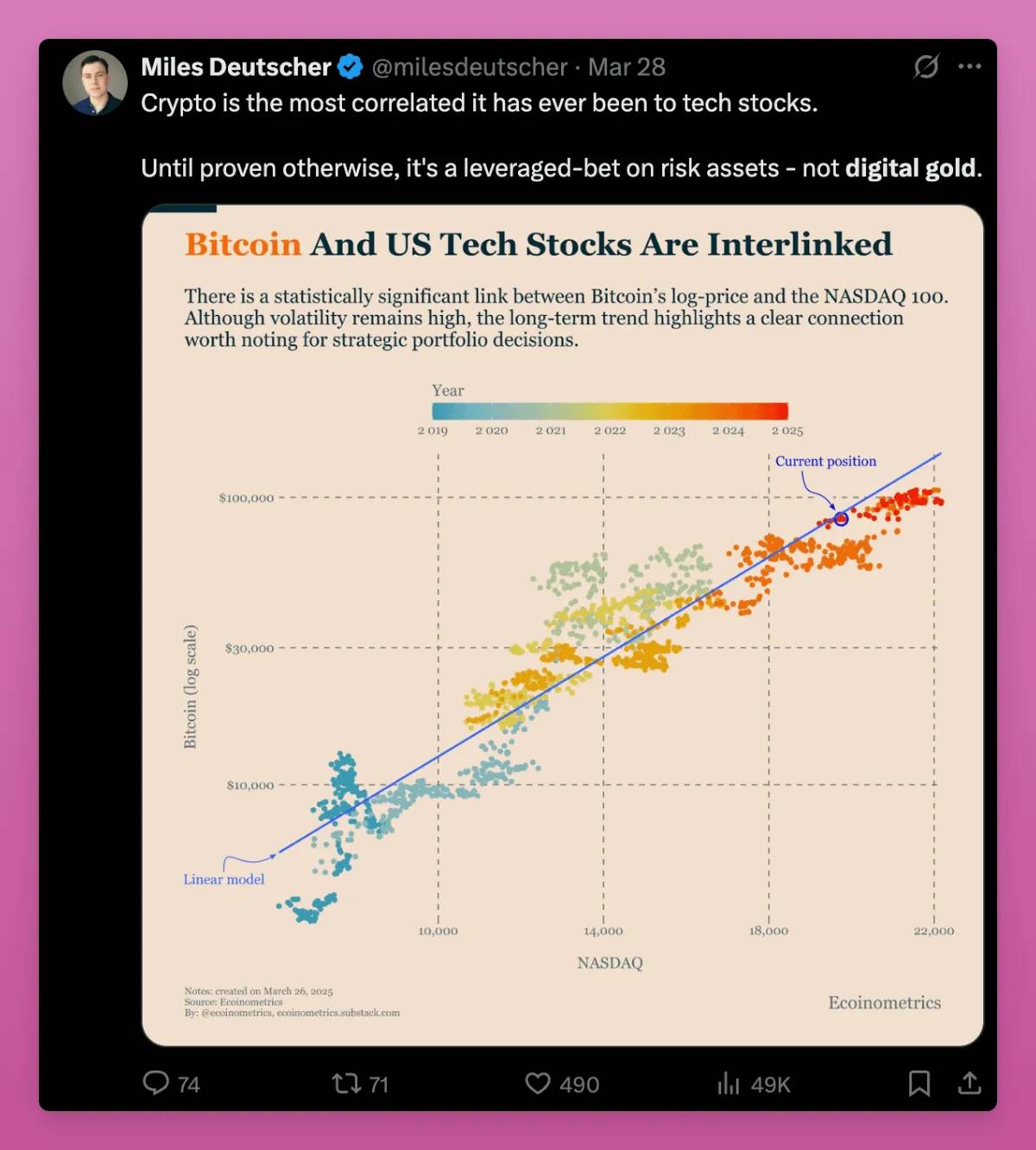

Many crypto commentators still view BTC as a highly volatile risk asset—akin to betting on the S&P 500.

This view contradicts research by Blackrock, which found that BTC’s risk and return drivers differ from traditional risk assets, making it unsuitable for the “Risk On/Risk Off” framework used by some macro commentators.

In my article Crypto Truths and Lies for the Year, I shared observations on non-obvious truths.

I believe BTC is transitioning from being seen as a leveraged equity bet to being recognized as a digital, safe-haven, gold-like asset. Mexican billionaire Ricardo Salinas exemplifies this—he stands firm in holding BTC.

BTC is the only true macro crypto asset. The value of ETH, SOL, and other cryptos is typically assessed through fees, trading volume, and total value locked (TVL). BTC has transcended these metrics, becoming a macro asset even Peter Schiff can understand.

This shift isn’t complete yet, but the transition from risk asset to safe haven presents an opportunity. Once BTC is widely accepted as a safe-haven asset, its price will reach $1 million.

Corruption in the Private Markets

I sensed something was wrong when nearly every relatively successful key opinion leader (KOL) started pivoting into “venture capitalists” (VCs), investing at low valuations and dumping tokens post-TGE.

Yet no one captured the state of crypto private markets better than Noah in this post:

Here’s the core evolution of private markets over recent years:

In the early days (2015–2019), private market participants were true believers. They supported Ethereum, funded DeFi pioneers like MakerDAO and ETHLend (now Aave), and promoted long-term HODLing.

The goal wasn’t just quick profits—it was to build meaningful things.

During the DeFi summer of 2020–2022, everything changed. Suddenly, everyone chased newer, hotter tokens.

Venture capital firms poured money recklessly into projects with absurd valuations and zero utility.

The game was simple: get in cheap during private rounds, hype the project, then dump tokens onto retail. When these projects collapsed, we should have learned—but nothing changed.

Post-FTX (2023–2025), private markets turned nihilistic. VCs began funding “soulless token machines”—projects recycling old ideas, with questionable founders (e.g., Movement) and no real use cases.

Private round valuations were set at 50x revenue (if any), forcing public markets to absorb the losses. As a result, 80% of tokens in 2024 traded below their private round prices within six months of launch.

This was a predatory phase.

Today, retail trust is gone, and VCs are in disarray.

Many VC portfolio projects now trade below seed round valuations, and several KOL friends of mine are deep in the red.

Yet there are signs of recovery in private markets:

-

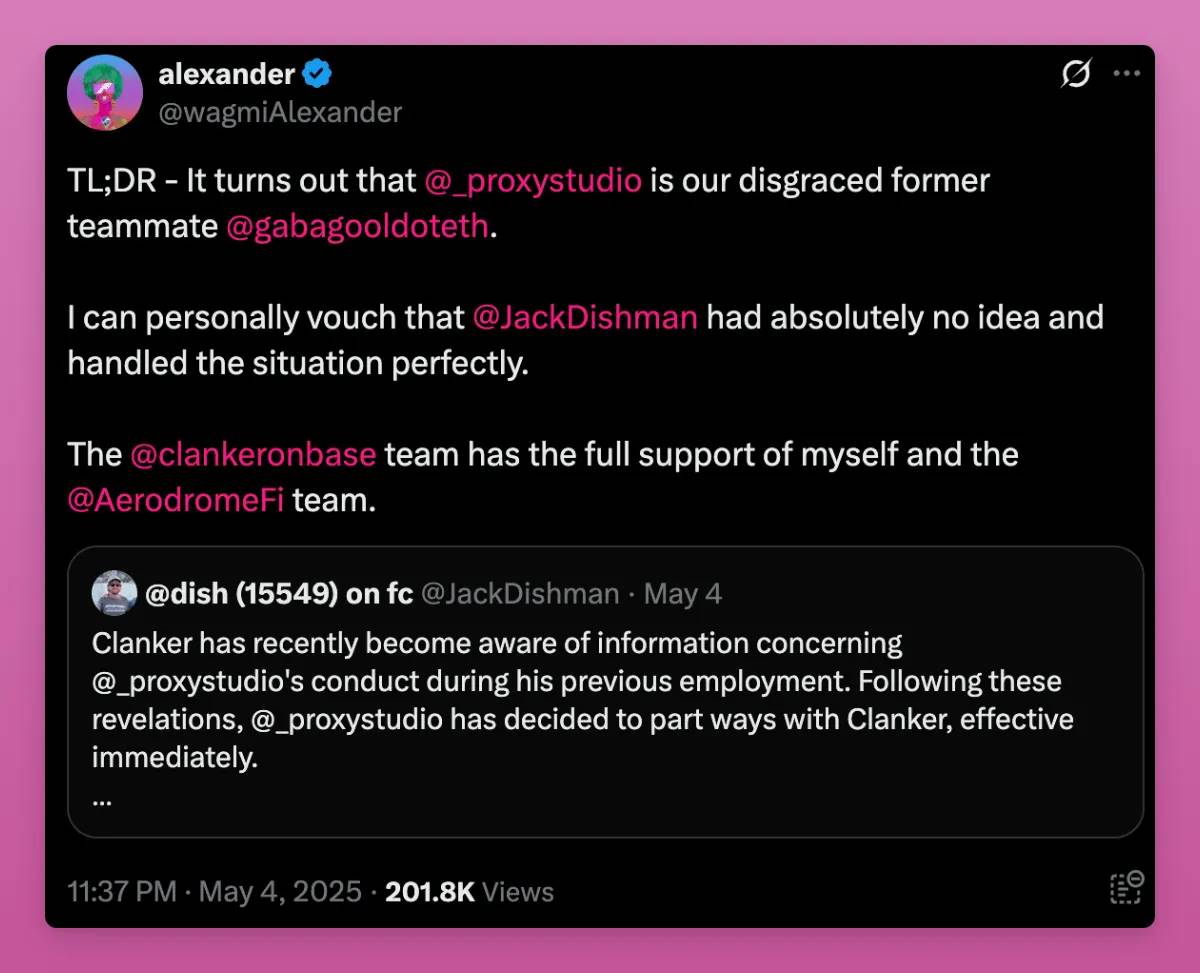

Backlash forced out Movement’s co-founder and Gabagool (former “runner” of Aerodrome). We need more such purges.

-

Valuations in private and public markets are declining.

-

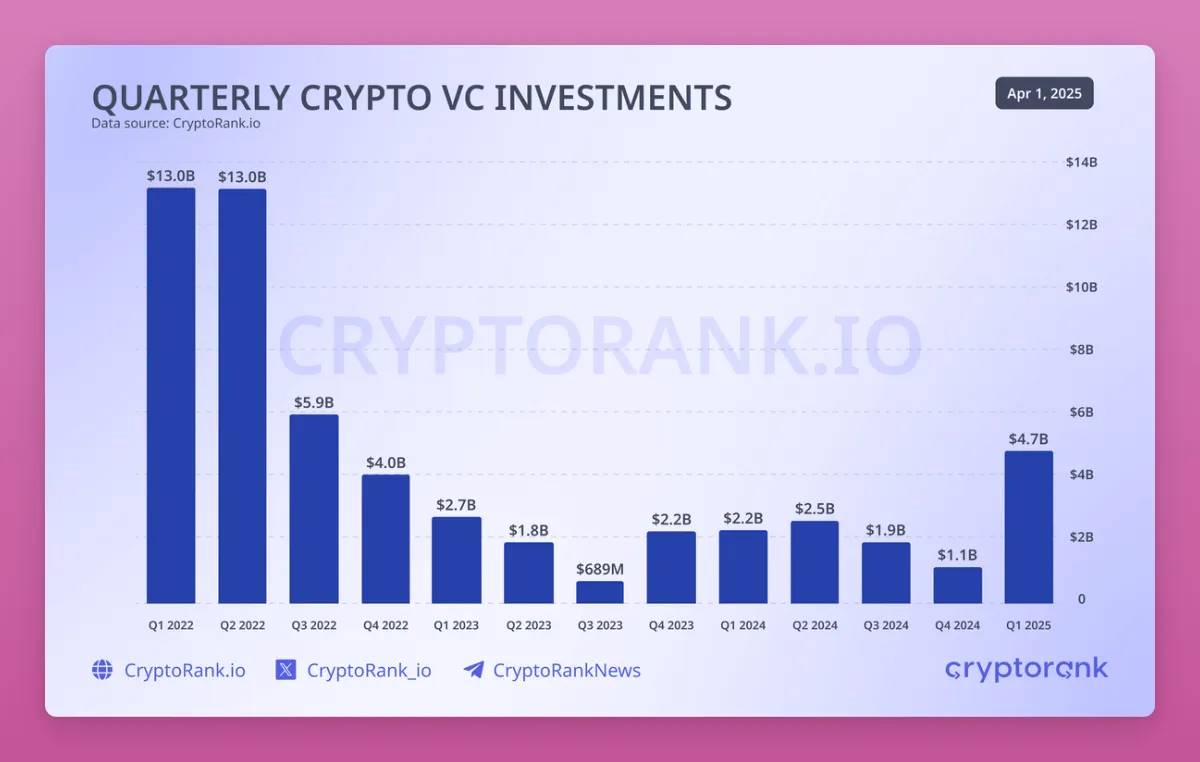

Crypto VC fundraising is finally rebounding: Q1 2025 saw $4.8B raised—the highest since Q3 2022—with capital flowing into areas with real utility.

According to CryptoRank’s Q1 2025 Crypto Fundraising Report:

-

Q1 2025 was the strongest quarter since Q3 2022. While Binance’s $2B deal played a key role, 12 deals over $50M signal renewed institutional interest.

-

Capital flowed into areas with real utility and revenue potential, including CeFi, blockchain infrastructure, and services. Emerging focus areas like AI, DePIN, and RWA gained strong traction.

-

DeFi led in number of funding rounds, but smaller sizes reflect more conservative valuations.

We’re experimenting with new token distribution models that reward early supporters instead of insiders.

Echo and Legion are leading this shift. Base has already launched a cohort on Echo. The Kaito InfoFi metaverse also shows strong bullish momentum, as even those without financial capital can benefit through social influence.

The market seems to have learned its lesson. The ecosystem is gradually healing—though KOLs still dominate access to the best opportunities.

Goodbye DeFi, Welcome Onchain Finance

Remember the short-lived narrative of yield aggregators? Yearn Finance led the charge, followed by countless forks.

Now we’re in the era of yield aggregators 2.0—only now we call them “vault strategies.”

As DeFi grows increasingly complex, with endless protocols emerging, vaults offer an attractive option: deposit your assets and earn optimal risk-adjusted returns.

But unlike first-gen yield aggregators, the key difference now is rapidly increasing centralization of asset management.

Vaults have “strategist” teams—often groups of “institutional investors”—who deploy your funds to chase the best opportunities. It’s a win-win: they earn yield on your capital while charging management fees.

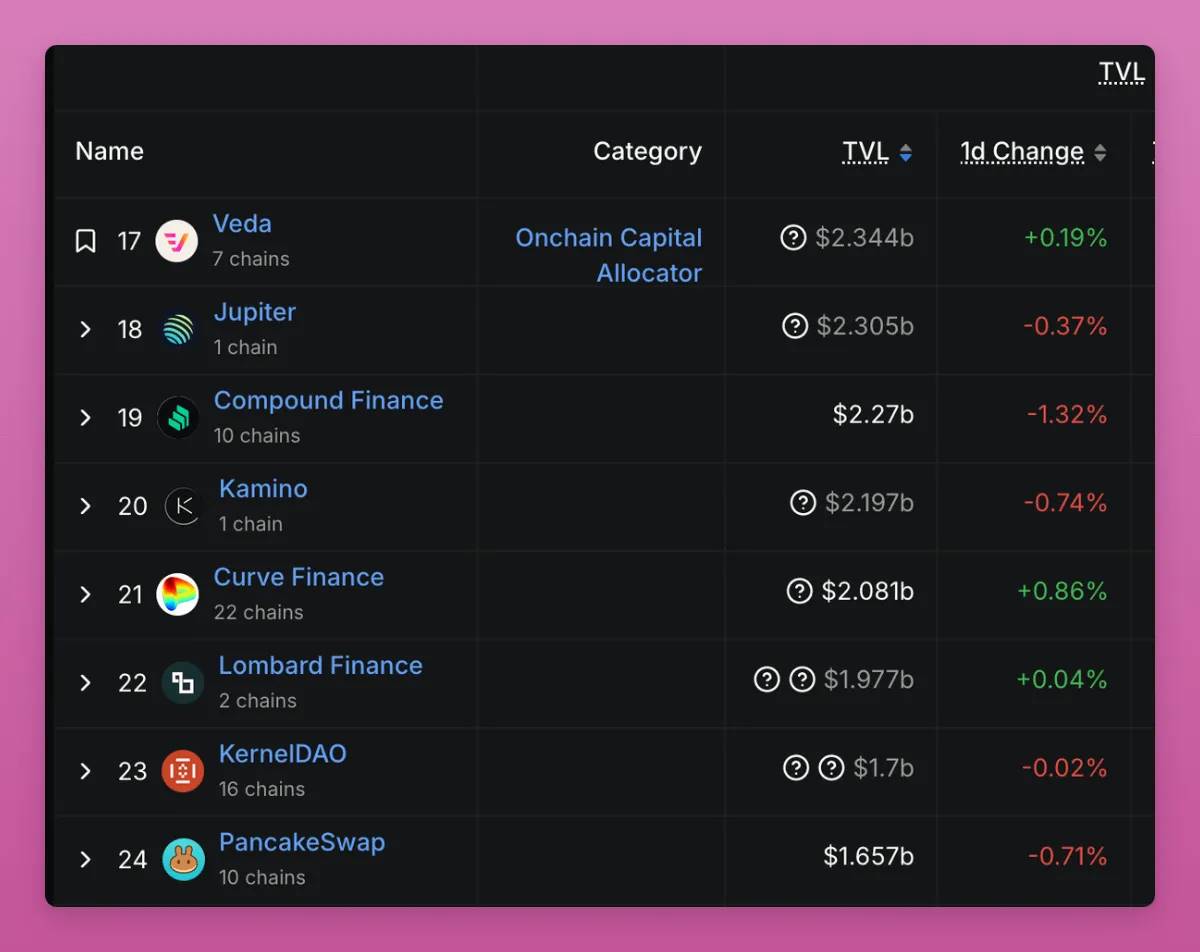

Examples include strategist teams like MEV Capital, Seven Seas, Gauntlet, and Veda, collaborating with protocols like Etherfi, Upshift, and Mellow Protocol.

Veda alone has become the 17th largest “protocol” in DeFi, surpassing Curve, Pancakeswap, or Compound Finance.

Yet vaults are just the tip of the iceberg. The original decentralized vision of DeFi is dead—it has evolved into Onchain Finance.

Consider this: the fastest-growing segments in DeFi and crypto are RWAs, yield-bearing assets, and risk-free arbitrage stablecoins like Ethena and Blackrock’s BUIDL—completely diverging from DeFi’s original vision.

Or projects like BTCfi (and Bitcoin L2s), which rely on multisig wallets where you must trust custodians not to “rug pull.”

Note: Not targeting Lombard specifically—just using it as an example of vault and BTCfi trend convergence.

This shift began when Maker transformed from a decentralized DAI issuer into a yield-generating RWA protocol. Truly decentralized protocols today are rare and small (Liquity being one example).

But this isn’t necessarily bad: RWAs and tokenization help us escape the era of DeFi Ponzi schemes built on loops and leverage.

It does mean risk factors are expanding, making it harder to fully understand where your money is. I wouldn’t be surprised if CeDeFi protocols misuse user funds.

Remember: hidden leverage always finds a way to seep into the system.

DAO—Just a Joke?

Likewise, the illusion of decentralization in DAOs is unraveling.

The past theory relied on a16z’s 2020 concept of “Progressive Decentralization” (Progressive Decentralization).

The idea:

Protocols first find product-market fit (PMF) → As network effects grow, communities gain more power → Teams “hand over the keys,” achieving full decentralization.

Five years later, I believe we’re reverting to centralization. Take the Ethereum Foundation, which is now more actively involved in scaling L1.

In my prior blog Fearful State of the Market and What’s Next #6, I highlighted multiple issues with the DAO model:

-

Voter apathy

-

Increased lobbying risks (vote buying)

-

Execution paralysis

Arbitrum and Lido DAOs are moving toward higher centralization (via more active team involvement or BORG mechanisms), while Uniswap faces major turmoil.

The Uniswap Foundation voted to allocate $165M in liquidity mining rewards to boost Uniswap v4 and Unichain. Another conspiracy theory suggests this funding was meant to meet liquidity thresholds for Optimism’s OP grants program.

Either way, DAO delegates are furious. Why should the foundation pay all $UNI rewards while Uniswap Labs (a centralized entity) earns millions from frontend fees?

Recently, a top-20 delegate resigned from their Uniswap representative role.

Here are the author’s core arguments:

-

Governance Theater: Formalized Governance in DAOs Uniswap’s DAO appears open but actually marginalizes dissenting voices. Despite following process (discussion, voting, forums), outcomes feel pre-determined, reducing governance to ritual.

-

Power Concentration: Uniswap Foundation Operations The foundation consolidates power by rewarding loyalty, suppressing criticism, and prioritizing optics over accountability.

-

Failure of Decentralization If DAOs prioritize brand over actual governance, they risk irrelevance. DAOs lacking real accountability resemble “dictatorships with extra steps.”

Ironically, a16z—the largest $UNI holder—failed to push Uniswap toward progressive decentralization.

Perhaps DAOs are merely smoke screens to avoid regulatory scrutiny that centralized crypto firms might face.

Thus, tokens serving only as voting tools aren’t worth investing in. Real revenue sharing and tangible utility are what matter.

Goodbye DAO, welcome LMAOs—Lobbied, Mismanaged, Autocratic Oligopolies.

DEX vs CEX: The Rise of Hyperliquid

Here’s a conspiracy theory of mine:

FTX launched Sushiswap because they feared Uniswap could threaten their spot market dominance. Even if FTX didn’t directly create Sushiswap, they likely provided close development and funding support.

Likewise, the Binance team (or BNB ecosystem) launched PancakeSwap for the same reason.

Uniswap poses a serious threat to centralized exchanges (CEXs), but it hasn’t challenged CEXs’ more profitable perpetual futures business.

How lucrative are perps? Hard to say exactly, but comments give clues:

Hyperliquid brings a different kind of threat. It targets not only perps but also spot markets, while building its own smart contract platform.

Currently, Hyperliquid holds 12.5% of the perp market share.

Shockingly, Binance and OKX openly attacked Hyperliquid using JELLYJELLY. Though Hyperliquid survived, HYPE investors must now seriously consider future attack risks.

Future attacks may not be technical—they could come via regulation. Especially as CZ evolves into a “national strategic crypto advisor,” who knows what he’ll tell politicians? Maybe: “Oh, those KYC-less perpetual exchanges are terrible.”

Regardless, I hope Hyperliquid challenges CEXs’ spot market operations, offers transparent token listings, and avoids high costs draining protocol finances.

I have much to say about HYPE, as it’s one of my largest altcoin holdings.

But one thing is certain: Hyperliquid has become a movement challenging CEXs—especially after the Binance/OKX attack.

Protocols Evolving into Platforms

If you follow my X (Twitter), you’ve probably seen my posts recommending Fluid in the context of protocols evolving into platforms.

The core idea: protocols risk commoditization, while user-facing apps capture most of the value.

Has Ethereum fallen into the commoditization trap?

To avoid this, protocols must become like Apple’s App Store—enabling third-party developers to build on them, keeping value within the ecosystem.

Uniswap v4 and Fluid attempt this via Hooks. Teams like 1inch and Jupiter are building their own mobile wallets. LayerZero just announced vApps.

I believe this trend will accelerate. Projects that capture liquidity, attract users, monetize traffic, and reward token holders will emerge as winners.

Crypto Industry and the Shifting World Order

I intended to cover more major shifts in crypto—from stablecoins to the decline of Crypto Twitter (CT)—because the industry is growing more complex.

Crypto Twitter now offers less “alpha” (exclusive insights), as the space is no longer a closed circle.

Once, we could launch “Ponzi schemes” with simple rules, while regulators either misunderstood crypto or ignored it, assuming it would fade away.

Over time, regulatory discussions have grown louder on CT. Fortunately, the U.S. is becoming more crypto-friendly. With the rise of stablecoins, tokenization, and Bitcoin as a store of value, we feel on the brink of mass adoption.

But this could change quickly: the U.S. government may eventually realize Bitcoin truly undermines the dollar’s dominance.

Regulatory and cultural environments outside the U.S. differ sharply.

The EU is increasingly focused on control, especially as it shifts from a welfare state to a war state, pushing controversial decisions under the guise of “security.”

The EU doesn’t prioritize crypto—it sees it as a threat:

-

“ECB warns U.S. crypto push may bring financial contagion risk to Europe”

-

“EU plans to ban anonymous crypto accounts and privacy coins by 2027”

-

“If blockchain data cannot be deleted individually, entire blockchains may need to be removed”

-

“EU regulators to impose punitive capital rules on insurers holding crypto”

We must assess crypto sentiment within broader political trends. The overall direction is deglobalization, with countries gradually closing borders.

-

EU close to banning visa-free access for “citizenship-by-investment” nations

-

In China, exit bans multiply as political control tightens under Xi

Crypto’s role in the new world order and its transitional phase remains a major unknown.

When capital controls begin, will crypto serve as a tool for financial freedom? Or will nations suppress it through stricter regulations?

Vitalik, in his piece on “The Rings Model of Culture and Politics,” explains that crypto is still forming its norms, not yet as rigid as banking or intellectual property law.

The internet in the 1990s adopted a “let it grow freely” attitude with minimal rules. In the 2000s and 2010s, social media shifted to “this is dangerous, we must control it!” By the 2020s, crypto and AI remain in fierce tension between openness and regulation.

Governments once lagged behind—but now they’re catching up.

I hope they choose to embrace openness, but the global trend toward closed borders deeply concerns me.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News