Exclusive Interview with Richard, Co-Founder of Huma Finance: Serving Real-World Payment and Financing Needs, User Education Remains the Biggest Challenge

TechFlow Selected TechFlow Selected

Exclusive Interview with Richard, Co-Founder of Huma Finance: Serving Real-World Payment and Financing Needs, User Education Remains the Biggest Challenge

Understand Huma's operational logic, current development status, and perspectives on the future of the entire PayFi sector.

Author: Nancy, PANews

Huma is a legendary mythical bird from Middle Eastern and Persian mythology, symbolizing hope, divinity, and good fortune. According to legend, the Huma never lands; whoever is lucky enough to be touched by its shadow will be blessed with kingship—this very idea inspired the naming of Huma Finance.

As one of today’s most talked-about PayFi protocols, discussions around Huma Finance's product mechanics and development trajectory have been intensifying recently—receiving both praise for its innovative model and scrutiny over transparency and profitability.

Recently, PANews conducted an exclusive interview with Richard Liu, co-founder of Huma Finance, aiming to provide a comprehensive understanding of how Huma operates, its current status, and its vision for the future of the entire PayFi sector.

Breaking Financial Barriers with On-Chain Technology, Backed by Solana Foundation

Richard is a multidisciplinary entrepreneur with extensive experience across startups, venture capital, and top-tier tech companies, combining deep technical expertise with profound insights into the financial industry.

During nearly eight years at Google, Richard led multiple "zero-to-one" innovation projects, including Google Fi, widely used by international users. In 2016, he left Google to dive into entrepreneurship, co-founding Leap.ai—a smart career development platform—and serving as CEO. The AI-powered platform helped match tens of thousands of job seekers with suitable roles and was later acquired by Facebook (Meta).

Following that, Richard joined fintech company EarnIn as CTO—an app enabling users to access their wages in advance. This experience planted the crucial seed for what would become Huma Finance.

"While people in China tend to save, many Americans live paycheck to paycheck. If there’s a child’s birthday or an unexpected emergency, they might genuinely not have the money. Seeing users feel such gratitude and relief when they can withdraw wages early through an app—that became our daily source of motivation," recalled Richard during the interview.

EarnIn processed up to $10 billion annually in lending volume. Yet despite being a large-scale, profitable company, it still faced resistance from traditional financial institutions when seeking funding. "You can’t get financing from banks—you’re forced to turn to private equity (PE). But once they realize you rely on just one or two disbursement channels, they start squeezing you. Harsh terms, little room to maneuver," said Richard.

This experience highlighted a critical imbalance: high-quality financial assets are often accessible only to PEs, funds, and family offices, while ordinary individuals are excluded—even though these assets could enhance market liquidity and generate returns for broader participation.

Richard began wondering whether blockchain technology could bring such assets on-chain—offering businesses wider funding options while giving everyday users access to previously inaccessible investment opportunities. However, he recognized that not all asset types are suitable for blockchain. "Many crypto users tolerate volatility in cryptocurrencies, but show almost zero tolerance for credit risk." Thus, he decided to focus on payment financing—a domain characterized by extremely low credit risk and short cycles.

In April 2022, Richard officially co-founded Huma Finance. Initially launched as a DeFi lending protocol, the project aimed to bring massive real-world financial demand onto the blockchain, primarily targeting fintech firms. Through continuous exploration, the team gradually narrowed its focus to payment financing due to its minimal credit risk and predictable timelines.

Then in 2024, when the Solana Foundation identified PayFi as a strategic priority, Richard had a pivotal meeting with Lily Liu, Chairperson of the Solana Foundation. She told him directly: “You understand the underlying logic of payment financing—it aligns perfectly with Solana’s strategy. You should build on Solana, and we’ll fully support you.”

"We're a multi-chain platform, but right now Solana is our main battlefield," emphasized Richard. He noted that Solana provides an ideal environment for Huma Finance’s high-frequency PayFi settlement operations. What truly impressed the team, however, was the Solana Foundation’s proactive and substantial support throughout collaboration—for instance, assigning expert engineers to assist Huma Finance during its initial integration phase when technical familiarity was limited. Additionally, during early on-chain fundraising stages, Solana introduced numerous early LPs (liquidity providers), helping establish trust via institutional participation. Furthermore, Huma Finance and the Solana Foundation plan to jointly host five PayFi ecosystem conferences to drive industry progress.

"Whether it’s technical issues or institutional resource connections, Solana has delivered—and often exceeded our expectations," admitted Richard. Today, Huma Finance stands as a flagship representative of PayFi within the Solana ecosystem.

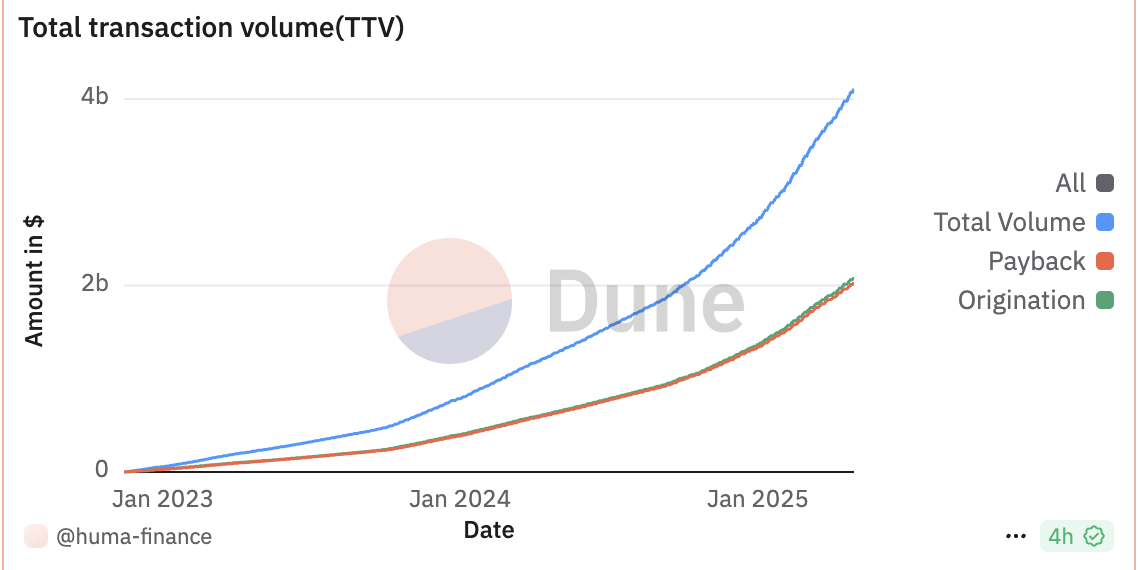

For Richard, Huma Finance represents both a continuation of his mission since the EarnIn days and a natural extension of his cross-domain expertise in technology and finance. To date, Huma Finance has publicly raised over $46 million, with on-chain transaction volumes surpassing $4 billion.

Focusing on Cross-Border Payment Advances and Credit Card Financing, Building a Platform + Application Strategic Loop

During the interview, Richard explained that Huma is the first PayFi network, built upon a robust PayFi infrastructure—especially at the financing layer—alongside a suite of proprietary and third-party applications. Core use cases within the PayFi ecosystem fall into three main categories: cross-border payment advances, credit card financing, and trade finance. Currently, Huma Finance focuses primarily on the first two.

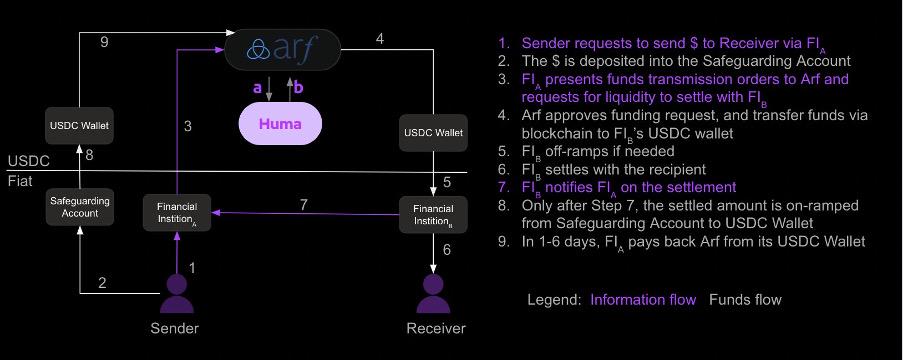

Addressing external questions about Huma’s profitability, Richard pointed out that in cross-border payment advances, Huma Finance leverages its subsidiary Arf to offer short-cycle advance services exclusively to payment companies. These transactions typically last only several days, ensuring higher capital efficiency and more manageable risk profiles. As Richard noted, this industry already has a stable pricing structure: SWIFT transfers usually cost RMB 20–60 per transaction, whereas using payment company channels incurs fees between 2% and 5%. Inter-institutional borrowing rates among payment providers hover around 10 basis points per day.

"At Huma, users typically pay 6–10 basis points per day in funding costs, which is entirely standard in the current market. Beyond offering competitive pricing, we also utilize stablecoins as the underlying settlement mechanism, integrating the inherent advantages of blockchain and stablecoins to create an efficient, secure clearing system—a technological upgrade over existing systems," Richard stated frankly. He added that cross-border payment advances represent a $4 trillion super-market. Given the vast size of this market and Huma Finance’s relatively small current scale, its impact on overall pricing remains negligible. Only when platform transaction volumes reach tens or hundreds of billions might downward pressure on industry-wide costs begin to emerge. By then, alongside Huma Finance, other competitors will likely have improved brand credibility and optimized funding cost structures, collectively driving shifts in market dynamics.

Beyond cross-border payments, Richard sees even greater potential in credit card advances—a $16 trillion global market. In the U.S., for example, after consumers swipe their cards, issuing banks must settle payments to merchants via payment networks within two to three days; in emerging markets like Brazil, this delay can stretch up to 30 days. During this period, banks effectively act as financiers, covering the merchant’s receivables before cardholders repay. Meanwhile, merchants themselves face cash flow waiting periods—but many are willing to pay a fee for instant access to funds.

Richard emphasized that both he and co-founder Erbil have hands-on experience in card issuance, having worked closely with the Google Pay ecosystem and led card programs at EarnIn. This gives them deep insight into the design and execution of credit card payment flows—meaning the team doesn’t just understand the industry’s complexity, but also possesses firsthand experience building products and models from the ground up.

Regarding trade finance, Richard acknowledged that while Huma Finance’s system technically supports such activities, the longer repayment cycles and slower capital turnover conflict with Huma’s current “high-frequency, short-cycle” strategy, so direct involvement is currently off-limits.

On the capital side, prior to Huma 2.0, participation was largely limited to professional investors and institutions. With the recent launch of Huma 2.0, retail participation has been opened under compliance frameworks, allowing users to choose between Classic or Maxi modes. Richard views this not merely as a product expansion, but as a meaningful step toward fulfilling Huma’s core philosophy of community ownership.

Additionally, considering users’ general reluctance toward forced lockups, Huma has designed a balanced approach: although B2B assets typically come with fixed terms (e.g., three months) and cannot be withdrawn immediately, the platform allocates approximately 80% of funds to payment transaction financing while reserving around 20% in highly liquid assets to meet user redemption demands.

"We won't force users to lock up funds—that’s a clear message we’ve received from our community. To ensure smooth redemptions, we maintain a buffer of liquid assets, allowing most withdrawals to be processed within one to two days," stressed Richard.

Furthermore, Richard explained why Huma Finance actively embraced DeFi mechanisms in its early fundraising stages rather than relying solely on traditional financial institutions. Unlike slow, bureaucratic processes typical of legacy finance, DeFi offers a fast, transparent funding path. "Anyone involved in asset allocation knows how hard it is to scale asset size—especially early on. Traditional institutions move slowly and require complex coordination, making growth feel like pushing a heavy snowball uphill. There’s plenty of capital in the market eager to back quality assets, but under traditional systems, there’s no transparent, accessible way to participate. By openly sharing our asset data on-chain, we earn trust and funding from the DeFi community, significantly accelerating our development speed."

Beyond efficiency and transparency, Richard also underscored the value of community co-creation. "What excites me most about Web3 is the possibility of genuine shared ownership and collective contribution—something nearly impossible in traditional finance."

"Just as Google uses Android, along with core apps like Gmail, YouTube, and Search as ecosystem anchors to drive growth and retention, we aim for our PayFi platform to provide foundational capabilities and scalability, while also hosting key applications that drive real demand and capital flow," Richard elaborated. He emphasized that Huma Finance isn't just building a single product, but a full PayFi infrastructure platform capable of supporting diverse applications—its value far exceeds any standalone app.

Precisely for this reason, Huma acquired its largest client, Arf, forming a closed-loop “platform + app” ecosystem. Richard believes the platform itself holds greater long-term value than any individual application, acting as a connector between capital and asset sides, enabling broader financial innovation across use cases.

Notably, Richard also discussed Huma Finance’s phased goals and roadmap. Previously, he announced a target of exceeding $10 billion in cumulative transaction volume by 2025. Expanding on this, he said, "Currently, our primary transaction growth comes from Arf’s core clients. While we’ve established a strong pipeline of potential partners, onboarding each customer takes time—often several months—due to varying requirements such as bank account setup and local regulatory approvals. Our current priority is streamlining this process. We’re actively exploring more efficient support systems to accelerate customer integration."

On the capital side, Huma continues refining user experience and appeal. "Since launching Huma 2.0, market feedback has been overwhelmingly positive," Richard reported. Despite capped deposit limits, liquidity pools filled rapidly. Both participant numbers and engagement in Maxi mode surpassed expectations. Capital-side activity and interest remain high, and once deposit caps are lifted and larger participants onboarded, growth potential is substantial. Moving forward, the team will focus on accelerating the migration of Arf clients’ transactions onto the blockchain, while advancing the deployment of credit card financing use cases on-chain.

Integrating Traditional Financial Risk Controls, Building Multi-Layered Asset Security

Huma Finance’s PayFi model has sparked debate in the market, with some investors expressing concerns about default or collapse risks.

In response to security concerns, Richard explained that Huma Finance adopts classic risk management principles from traditional structured finance, incorporating mechanisms such as First-Loss Cover and senior/junior tranching, complemented by multiple safeguards. The goal is to build a DeFi product suite with institutional-grade risk control—particularly evident in Arf’s cross-border payment advance business.

Specifically, in counterparty selection, Huma Finance’s Arf business serves only licensed financial institutions in developed countries (such as the U.S., U.K., France, and Singapore), avoiding regions with complex foreign exchange controls. These institutions must meet strict compliance standards and exhibit low intrinsic credit risk, forming a foundational layer of protection against counterparty defaults. Additionally, Huma Finance maintains a rigorous internal risk rating system for partner institutions, evaluating factors such as financial health, remittance path stability, and counterparty exposure, classifying them into Tier 1, 2, and 3—currently serving only Tier 1 and Tier 2 clients. Operationally, advance disbursements occur only after confirming receipt of incoming payments, which are deposited into dedicated accounts monitored by banks and restricted solely to that specific cross-border transaction. Huma Finance releases funds only after verifying the funds have arrived and passed preliminary risk assessments. Legally, assets involved in Arf operations are managed through independent SPVs (Special Purpose Vehicles), completely segregated from Huma Finance or Arf’s corporate balance sheets. Even in extreme scenarios such as Arf’s bankruptcy, user assets remain legally protected. Regarding repayment timelines, Huma Finance designs ultra-short cycles, typically completing advances and collections within days. Should any institution exhibit delayed payments or credit deterioration, the system can swiftly adjust or suspend credit lines, enabling early detection and containment of risks. Historical data shows that financial systems globally have experienced bad debt rates of just 0.25% over the past 20 years; by focusing on short-term advances in developed markets, Huma Finance operates in a context where expected defaults are even lower.

Even in the face of mass redemptions or systemic shocks, Richard noted that Huma Finance has implemented several contingency measures: For example, Arf maintains a 2% margin reserve—many times higher than typical default rates—built gradually from platform profits and prioritized for absorbing potential losses. Regardless of whether user funds are locked, all redemptions follow a principle of “fair settlement” in extreme conditions, preventing structural unfairness where early exiters profit at others’ expense. In cases of partner default or insolvency, because client funds reside in segregated accounts and flow through regulated systems, Huma Finance retains the legal ability to recover most, if not all, of the funds. While this mechanism hasn’t been triggered historically, its legal and procedural framework makes recovery feasible in practice.

On transparency, Richard revealed that all Huma Finance funds are custodied via Fireblocks wallets, routed exclusively through pre-defined compliant paths requiring multi-signature approval, ensuring no misappropriation. Moreover, fund flows are fully traceable in real-time on-chain. Currently, partial data is disclosed via Dune Dashboard, with plans to gradually expand the dashboard to offer richer visibility into fund movements. Additionally, Huma Finance publishes monthly fund flow reports detailing pool allocations and usage, with intentions to eventually encode reporting into smart contracts—further enhancing decentralization, transparency, and auditability.

Clearly, Huma Finance’s core logic does not rely on market sentiment or Ponzi-like dynamics to sustain liquidity. Instead, it builds a highly resilient, accountable DeFi financial ecosystem through layered risk controls, legal structuring, and self-funded buffers. While extreme risks can never be entirely eliminated, its systematic safeguards and settlement principles aim to establish multiple lines of defense for user asset security.

Strengthening Community Engagement: User Education Is Our Greatest Challenge

"Disrespecting the community or users is an absolute red line for Huma Finance. Authenticity is the sharpest tool to cut through noise," said Richard, who promptly issued a public letter following recent community backlash over communication styles from a team member, further elaborating on the team’s reflections and future improvements regarding community building.

Richard candidly admitted that mismatches between personnel and roles led to communication breakdowns. "Our colleague is incredibly hardworking and creative, but I placed her in a role unsuited to her strengths—external community communications. That wasn’t her forte, and I should have realized it sooner." As a result, Richard restructured communication responsibilities: he now personally oversees Chinese-speaking communities, while English communications are handled by co-founder Erbil Karaman.

"We believe community engagement is one of the most critical functions for any crypto company. Founding members best embody the company’s mission and values—they must lead from the front in community dialogue." This restructuring represents Huma Finance’s direct response and structural fix to past shortcomings.

Moreover, Richard emphasized that the team has reached internal consensus: every piece of community feedback, regardless of tone, deserves careful listening and reflection. "When criticized, we must maintain a healthy mindset and try to understand the root of their concerns. Either we clarify misunderstandings, or acknowledge shortcomings and commit to improvement. For instance, we didn’t prioritize transparency highly enough in the past—we’ll elevate it going forward, ensuring disclosures become clearer and more systematic."

In closing, Richard shared his broader perspective on the PayFi space—highlighting the key to bridging the gap between traditional finance and DeFi, as well as the challenges and solutions in user education and adoption.

"The essence of PayFi is using blockchain technology to serve real-world payment and financing needs," Richard stated. While many financial institutions and payment companies express strong interest in this model, actual implementation often stalls at the most traditional hurdles—compliance and banking infrastructure.

He added that compliance and fiat on/off ramps are the most critical middleware in the entire ecosystem. If Hong Kong were to introduce clearer legislation allowing local payment firms to legally and seamlessly connect to on-chain services, it would not only mark a breakthrough for Hong Kong but significantly propel the entire PayFi ecosystem forward.

Beyond connecting with traditional finance, Richard expressed a deeper ambition: "We don’t just want users to invest in Huma Finance—we want these PayFi assets to ‘go out’ into the broader DeFi ecosystem and become core components within the entire DeFi landscape."

Yet between vision and reality lies the toughest barrier—user education. "This is actually our biggest challenge today," Richard admitted. DeFi users are accustomed to high-APY “token emission” models and find it unfamiliar to consider yield generated purely from real-world lending without token incentives. "Even when I tell them we can deliver real 12.5% returns—higher than many on-chain protocols—their first reaction is often: Are you running a Ponzi? Is this fake?" On the other hand, traditional finance professionals harbor deep skepticism toward DeFi’s technical approach. "Many ask me directly: Why can’t we just use fiat accounts? Why do we need stablecoins?" Once stablecoins or on-chain settlements enter the picture, regulatory uncertainty triggers hesitation.

Richard observed that this “cognitive mismatch” stems from both communities speaking different languages and operating under different logics. "That means our team must fluently speak both dialects—using precise DeFi terminology while also communicating effectively in traditional financial language. PayFi has a long road ahead. We need to collaborate with the community to produce more educational content, helping more people understand PayFi and jointly build this sector into crypto’s most successful real-world application."

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News