Resolv: Experiment to verify Ethena's on-chain feasibility

TechFlow Selected TechFlow Selected

Resolv: Experiment to verify Ethena's on-chain feasibility

Once large capital makes its choice, the market for small capital becomes vacant.

Author: Zuoye

Once large capital makes its choices, the market space opens up for smaller capital.

In this cycle, bull and bear markets never rest—VCs, KOLs, and stablecoins represent three major trends, with KOLs themselves being an asset class that can be tokenized.

As VC options become increasingly limited, targeting stablecoins and "simple investment" products has become a trend. Reinvesting in already-launched projects offers lower risk and more predictable returns.

On April 16, Resolv, a chain-native Delta-neutral yield-bearing stablecoin (YBS) project, closed a $10 million seed round led by Maven11. This marks its first public funding since its founding in 2023.

Compared to Ethena’s explosive growth, Resolv remains relatively low-key—but its innovations are no less impressive. In summary: a more unique yield model, more on-chain yield sources, and more complex tokenomics.

The American Gold Rush Dream of Russian Tech Enthusiasts

A gesture of goodwill from Trump brought Russians back into global contention.

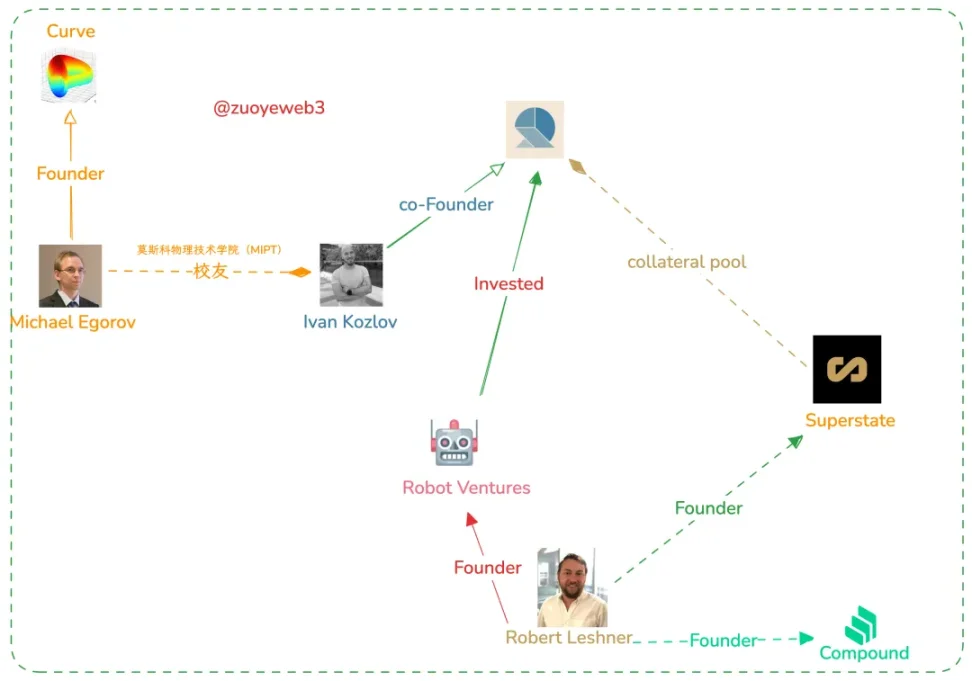

Maven11, the lead investor, is based in the Netherlands, while participating funds such as Robot Ventures are primarily U.S.-based. The three Resolv founders—Ivan Kozlov, Fedor Chmilevfa, and Tim Shekikhachev—are all technically trained men educated in Russia.

It's reasonable to suspect this funding round was completed earlier but withheld for reputational reasons. Considering Ethena required exchange-backed VC support, a YBS project at minimum needs liquidity reserves to withstand black swan events.

Image caption: Social mapping of the Resolv founding team

Image source: @zuoyeweb3

When it comes to on-chain viability, Ethena believes it's unworkable. Arthur Hayes argues that forming strategic alliances with CEXs is necessary to secure USDe liquidity—this is why ENA tokens were distributed to exchange VCs, effectively trading minting rights for long-term protocol stability.

In contrast to Ethena’s compromise, Resolv embraces the on-chain ecosystem more fully and demonstrates determination to capture market share through higher yields.

More Complex Tokenomics

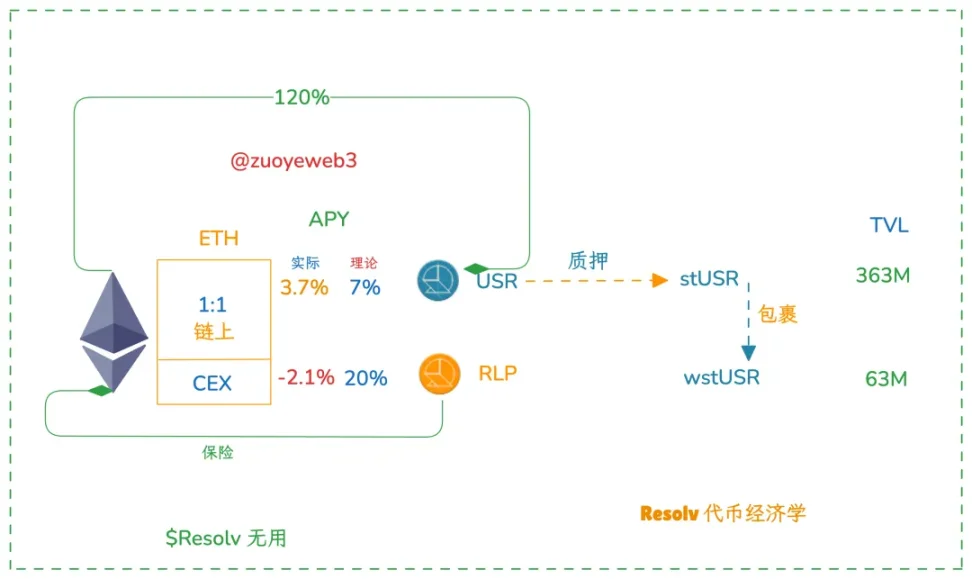

Unlike Ethena’s dual-token system (stablecoin + governance token), Resolv effectively operates with three tokens: the stablecoin USR, the insurance fund and LP token RLP, and the governance token $RESOLV.

Image caption: Resolv tokenomics

Image source: @zuoyeweb3

Notably, Resolv’s governance token does not serve the same alliance-building function as ENA. In practice, ENA acts as a proportional representative for Authorized Participants (APs). To put it bluntly, ENA holds little value for retail users but is essential for Ethena’s operation.

Resolv focuses instead on the dual-yield system formed by USR and RLP. Users deposit USDC/USDT/ETH and can theoretically mint USR at a 1:1 ratio. These assets are mostly deposited into on-chain protocols or Hyperliquid, minimizing asset losses from CEX hedging.

Cleverly, Resolv introduced the RLP token, primarily used to cover funds hedged on CEXs. Beyond that, it offers significantly higher yields: USR yields between 7%-10% APY, while RLP targets 20%-30%. However, these figures remain theoretical—for now, neither has reached target levels.

More On-Chain Yield Sources

Compared to Ethena, Resolv more actively embraces the on-chain ecosystem. From a yield perspective, YBS models generally consist of income from interest-bearing assets like stETH, plus CEX futures hedging fees.

On-chain yield potential could surpass CEX hedging returns, but the key issue lies in liquidity—Hyperliquid clearly lags behind competitors like Binance. Currently, hedging orders split roughly 7:3 between Binance and Hyperliquid, which is precisely where RLP adds value.

RLP is a leveraged yield token, achieving higher returns with less capital. For example, RLP’s current TVL stands at just $63 million—less than 20% of USR’s—making it suitable for high-risk-tolerant participants.

A quick critique: due to ETH’s price trajectory, the assumed YBS model wherein long ETH positions pay fees to shorts may not hold true for some time. Currently, RLP’s yield is negative.

A More Unique Yield Model

USR and USDe are not vastly different, but Resolv introduces RLP as an insurance mechanism. Since Resolv cannot yet fully eliminate reliance on off-chain CEXs and USDC, it aims to minimize their negative impact.

Image caption: Resolv data

Image source: @ResolvLabs

Theoretically, USR will be over-collateralized entirely by on-chain assets (currently at a 120% ratio, with 40% being on-chain). Some collateral will be used for institutional custody and off-chain CEX hedging.

This approach is clearly less capital-efficient than Ethena’s fully off-chain CEX hedging. Thus, Resolv’s RLP must “compensate” for this gap—at minimum, matching Ethena’s returns.

Outlook for YBS’s Future

Ethena opened the door to YBS—but did not close it.

USR offers base yields of 7%–10%, while RLP targets 20%–30%, with risk isolation built in. For example: 1.2 USD worth of ETH mints 1 USR; the reserve is hedged on-chain and via Hyperliquid, while 0.2 USD is allocated to mint RLP and hedged on Binance.

Even if Binance collapses, USR can still maintain full solvency. In theory, RLP’s maximum risk exposure is only 8%. This represents progress over Ethena, which relies entirely on perpetual CEXs for capital efficiency and security.

Or perhaps it’s a step back: under Ethena’s design, as long as CEXs don’t maliciously attack, a death spiral is nearly impossible. In extreme cases, Ethena can stabilize the market through negotiations with large holders and proprietary funds—similar to how Curve’s founder stabilized the price via OTC deals during past crises.

By placing more capital and yield generation on-chain, Resolv must contend with various on-chain risks. Binance may not target ENA, but that doesn’t mean it won’t target Hyperliquid—recall prior analysis: Hyperliquid is “9% Binance, 78% centralized.”

In the end, amid fierce competition, balancing safety and yield is often unattainable. Resolv launched around the same time as Ethena, yet its TVL and issuance volume lag far behind. For latecomers, available options will only shrink further.

Yet, more vessels will join this YBS age of exploration. In a low-interest environment, project launch costs are lower than during DeFi Summer.

This seems counterintuitive: during DeFi Summer, even a basic product prototype could attract massive capital inflows. But remember, farming strategies typically demanded returns above 20%—UST being a clear example—while Ethena’s baseline sUSDE yield stabilizes below 5%.

In other words, as long as new YBS projects offer APY above 5%, adventurers will participate, creating opportunities to bootstrap flywheels. But convincing uninformed retail users to adopt new YBS projects won’t be solved simply by hiring KOLs or securing VC endorsements.

Conclusion

The combination of USR and RLP resembles a hybrid of Hyperliquid and Ethena—an LP Token + YBS fusion. I call this the Sonic/Berachain-ification of the YBS ecosystem: using increasingly complex mechanisms to surpass existing products.

At the same time, risks clearly rise. Any LP token mechanism faces the paradox of creating liquidity solely for the sake of liquidity. Moreover, RLP’s insurance mechanism hasn’t been tested under extreme market conditions—unlike USDe, which has already experienced depegging.

Depegging is a stablecoin’s rite of passage. Let’s hope Resolv can pass this test.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News