Circle IPO May Be Delayed: What’s the Valuation of the “First Stablecoin Stock”?

TechFlow Selected TechFlow Selected

Circle IPO May Be Delayed: What’s the Valuation of the “First Stablecoin Stock”?

A Closer Look at the 5 Key Uncertainties Surrounding Circle's IPO.

Author: Wenser (@wenser 2010)

In late March, according to Fortune, stablecoin issuer Circle had hired investment banks to initiate IPO preparations and planned to publicly file its listing application with the SEC by late April. On April 1, Circle officially submitted its S-1 registration statement to the U.S. SEC, aiming to list on the New York Stock Exchange under the ticker symbol CRCL. Just as the market assumed this might mark the first crypto IPO under the Trump administration—seemingly a done deal—within days, following the official launch of Trump’s tariff-driven trade war, reports emerged suggesting Circle would delay its IPO process. Thus, amid Trump’s push for a crypto-friendly government, the question of which company will claim the title of first crypto IPO remains unresolved.

Odaily Planet Daily will analyze the current state of the stablecoin market, U.S. crypto regulatory trends, and compare Circle’s valuation framework against other potential IPO-bound crypto projects in this article.

Question One: Can Circle Secure the Title of “First Stablecoin-Related Public Company”?

To cut to the chase: Circle is highly likely to secure the title of “first publicly traded stablecoin company.”

The reasons are as follows:

1. Its main competitor has no intention of pursuing an IPO path. After Circle filed its IPO prospectus, Paolo Ardoino, CEO of Tether—the issuer behind USDT—stated that Tether does not need to go public. (Odaily Planet Daily note: Notably, Paolo accompanied his tweet with a photo of himself standing beside the Wall Street Bull, conveying a strong message: “I don’t need to court Wall Street investment banks—they need me.”)

Tether CEO's bold statement

2. Circle firmly holds the second position among stablecoin issuers. According to data from Coingecko, USDC currently has a market cap of $60.14 billion, ranking second only to USDT at $144 billion, and stands as the sixth-largest cryptocurrency by market capitalization.

3. Circle boasts a robust compliance framework, earning it the reputation as the “most compliant stablecoin issuer.” Circle is registered in the U.S. as a Money Services Business (MSB) and complies with the Bank Secrecy Act (BSA) and related regulations. It holds money transmission licenses across 49 U.S. states, Puerto Rico, and the District of Columbia. In 2023, Circle obtained a Major Payment Institution license from the Monetary Authority of Singapore (MAS), enabling operations in Singapore. In 2024, it received an Electronic Money Institution (EMI) license from France’s Prudential Supervision and Resolution Authority (ACPR), allowing it to issue USDC and EURC in Europe under the EU’s Markets in Crypto-Assets Regulation (MiCA). Indeed, USDC is one of the few stablecoins operating legally in the U.S., Europe, and parts of Asia.

Therefore, considering its progress in filing IPO documents, USDC’s market standing, and competitors’ positions, Circle appears poised to claim the title of “first publicly traded stablecoin company.”

The next question is: Will Circle’s core business support its post-IPO market valuation? The answer lies within Circle’s IPO filings.

Question Two: Is Circle’s USDC Stablecoin a Lucrative, Risk-Free Business?

Again, straight to the point: Currently, Circle’s operational performance is far from ideal.

Previously, in our article “‘Top Stablecoin’ USDT Hits Record Market Cap: Unveiling Tether’s Billion-Dollar Empire,” we provided a detailed analysis of Tether, the dominant player in the stablecoin sector, including its business model. In another piece, “7 Top Crypto Cash Machines: $14 Billion Annual Profit — Who Is the Ultimate ‘Tax Collector’ in Crypto?”, we analyzed Tether’s extraordinary profitability—nearly $14 billion in annual profit with fewer than 200 employees—earning it the top spot in operational efficiency.

However, Circle’s IPO prospectus reveals a significant gap between its operations and those of Tether:

-

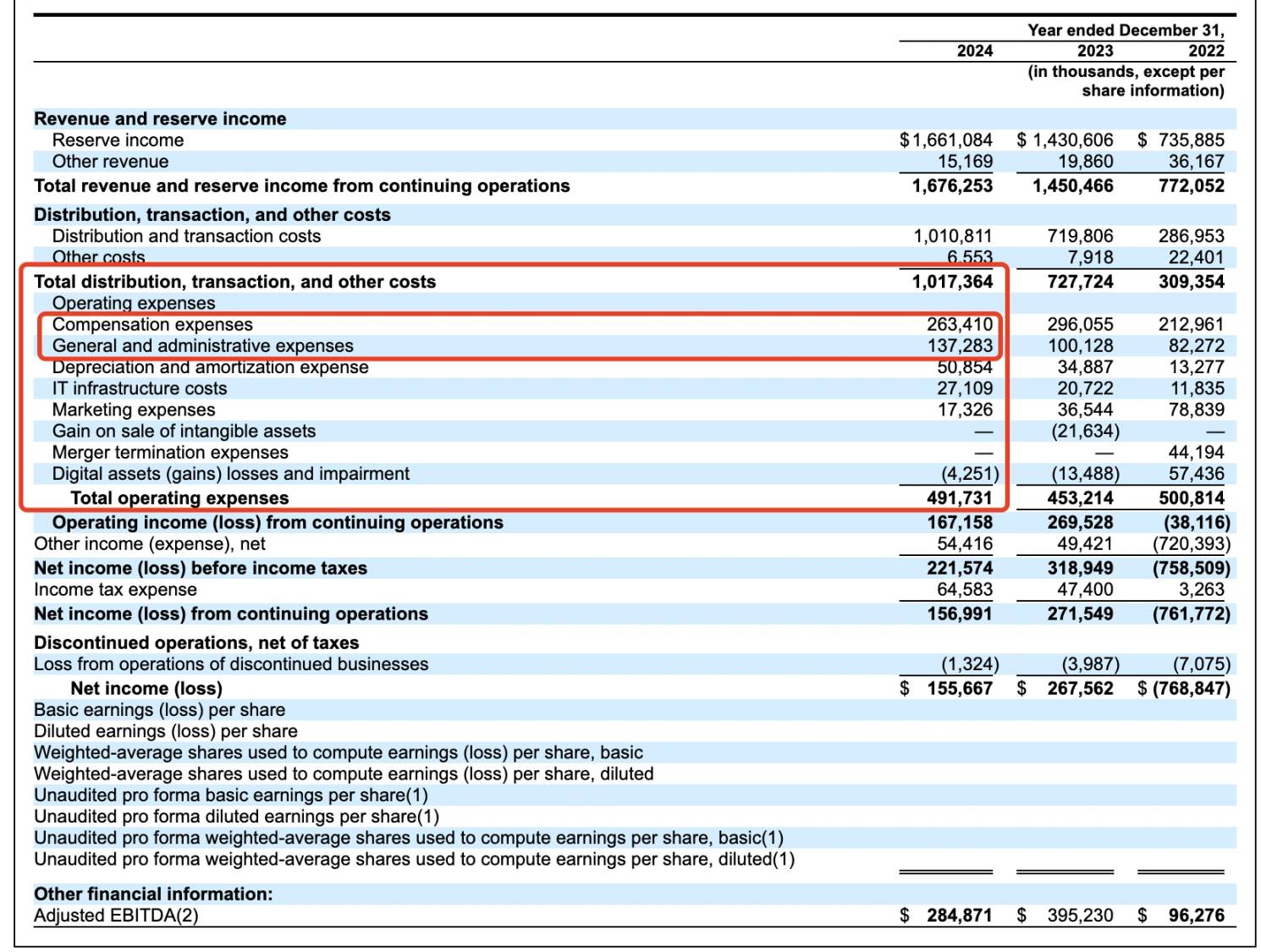

Revenue details: In 2024, Circle reported $1.68 billion in revenue, up from $1.45 billion the previous year—a 16.5% increase. However, net profit dropped from $268 million to $156 million, a 42% decline year-over-year. A major factor was $908 million in distribution costs paid to partners such as Coinbase and Binance.

-

Reserve assets: Approximately 85% of USDC’s reserves are invested in U.S. Treasuries, managed by BlackRock’s Circle Reserve Fund, while about 20% are held as cash deposits in the U.S. banking system. In contrast, USDT’s reserves are more diversified, including 5.47% in Bitcoin.

USDT reserve composition details

Personnel and administrative costs: According to the prospectus, Circle spends over $260 million annually on employee compensation and nearly $140 million on administrative expenses. Depreciation and amortization costs reach $50.85 million, IT infrastructure costs hit $27.1 million, and marketing expenses amount to around $17.32 million. Clearly, Circle’s cost structure is significantly more complex than Tether’s.

Circle's financials over the past three years

Moreover, Circle’s revenue streams are far narrower than Tether’s: 99% of its income—approximately $1.661 billion—comes from interest on reserves, while transaction fees and other income total only $15.169 million.

In other words, Circle is currently in the business of “depositing funds and earning interest,” unlike Tether, which runs a dual-revenue model—earning both from reserve interest and charging fees during redemption processes. Consider that the cross-border payments market is valued at $150 trillion, a space now largely dominated by the more decentralized and less-regulated USDT.

In contrast, Circle remains constrained by its “partners” such as Coinbase and Binance.

Question Three: Will the Ambiguous Relationship with Coinbase Continue?

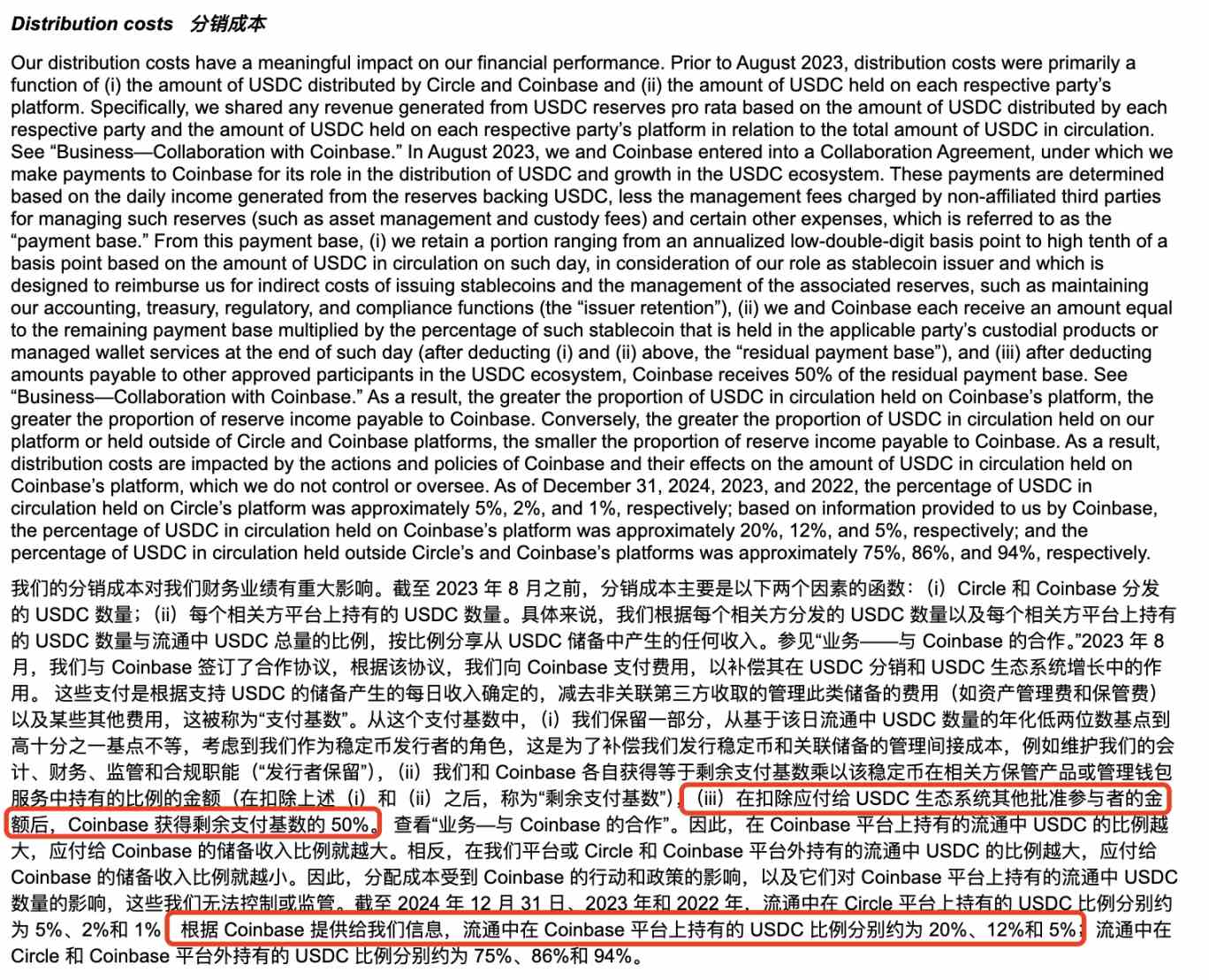

Circle’s full name is Circle Internet Financial, Inc., founded in 2013 by Jeremy Allaire and Sean Neville. USDC governance was originally managed by the Centre Consortium, co-founded by Circle and Coinbase. However, amid shifting regulatory landscapes, in August 2023, Circle acquired Coinbase’s stake in the Centre Consortium for $210 million in stock, taking full control of USDC issuance and governance. Nevertheless, the existing 50:50 revenue-sharing agreement remains intact.

Distribution cost details from Circle’s prospectus

In 2024, of the $908 million in distribution costs paid by Circle to Coinbase, $224 million was distributed as staking rewards to users (offering up to 4.5% APY on USDC holdings, previously reaching as high as 12%, according to user reports), while the remaining ~$686 million went directly to Coinbase.

@0x_Todd’s actual yield and corresponding interface

This strategy may be seen as a deliberate “open play” by Circle and Coinbase to boost USDC’s circulation and market share. That said, such high staking yields inevitably raise suspicions: Are Circle and Coinbase resorting to an aggressive “high-interest deposit grab” to inflate metrics ahead of their IPO?

Besides Coinbase, Binance also benefits from Circle’s generous distribution incentives.

The prospectus reveals that in November 2024, Binance became the first approved participant under Circle’s Stablecoin Ecosystem Program. Under the agreement, Binance must promote USDC on its platform and maintain a certain amount of USDC in its treasury reserves. Circle paid Binance a one-time upfront fee of $60.25 million and agreed to monthly incentive payments based on Binance’s USDC holdings. These incentives apply only if Binance holds at least 1.5 billion USDC, with a commitment to hold up to 3 billion (exceptions allowed under specific conditions). The two-year agreement covers both marketing promotion and treasury reserve components. If Binance terminates the marketing portion early, it must still fulfill reduced-payment obligations and promotional duties for one additional year. Either party may terminate the agreement early under special circumstances.

Clearly, Circle understands the importance of high-profile alliances to expand its market footprint.

Additionally, over the past year, Circle has been actively expanding into ecosystems like Solana and Base. In the Solana ecosystem alone, Odaily Planet Daily estimates that since 2025, over 3.25 billion USDC have been issued in 13 separate minting events, with individual issuances reaching up to 250 million.

Incomplete statistics

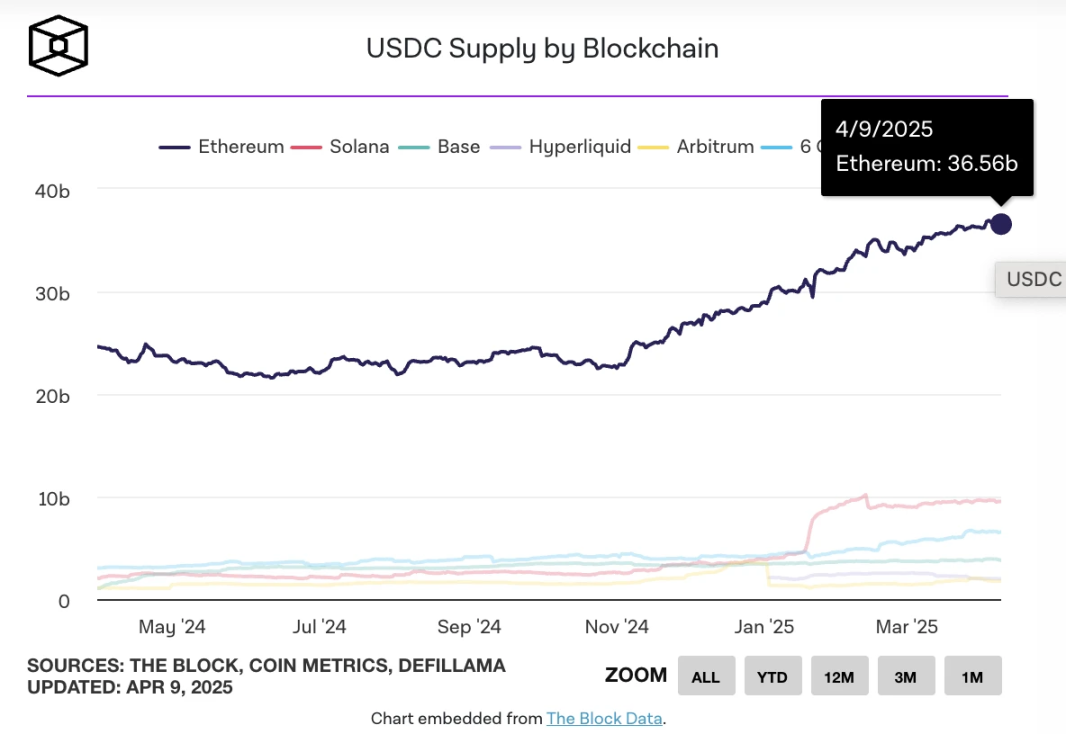

On March 26, when the on-chain issuance of USDC surpassed $60 billion, The Block reported the breakdown as follows:

-

Ethereum: ~$36 billion

-

Solana: ~$10 billion

-

Base: ~$3.7 billion

-

Hyperliquid: ~$2.2 billion

-

Arbitrum: ~$1.8 billion

-

Berachain: ~$1 billion

TheBlock’s USDC issuance distribution across chains

As of now, USDC’s circulating supply remains around $60 billion. According to DefiLlama, the total stablecoin market cap stands at approximately $233.535 billion, down 0.58% over the past seven days. USDC’s market share is about 26%.

Thus, we can draw a preliminary conclusion: Circle’s future growth will continue to rely heavily on Coinbase’s support, and it may persist in transferring roughly 50% of its distribution revenue to Coinbase.

Question Four: Will Circle Be Affected by U.S. Stablecoin Regulatory Legislation?

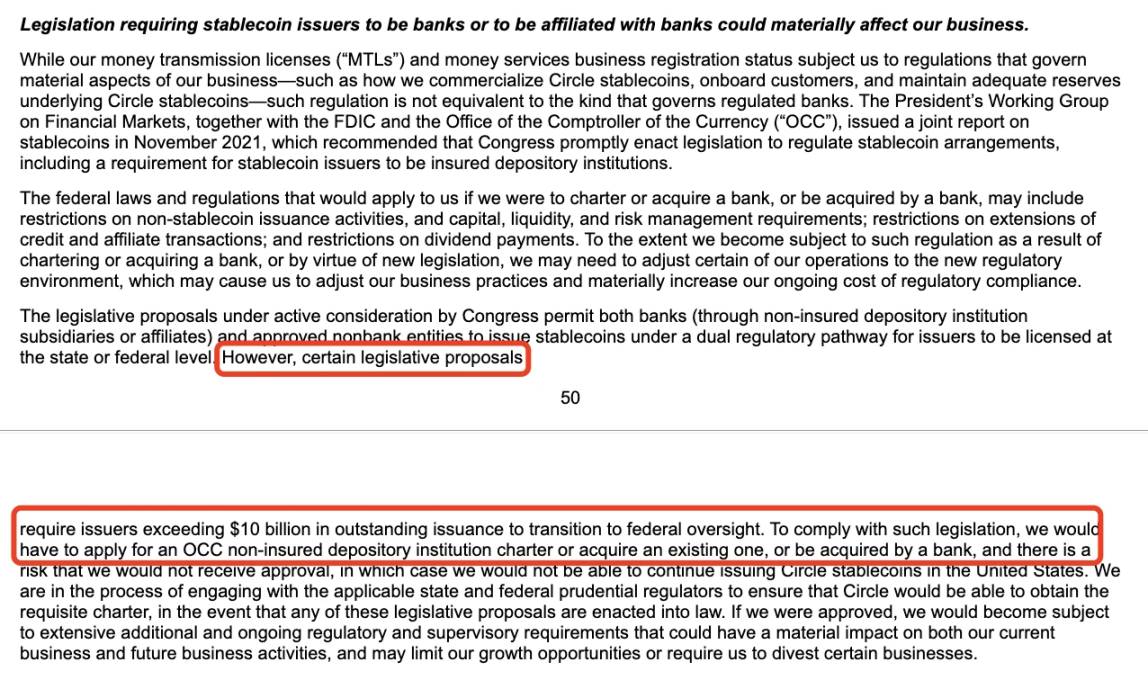

In its prospectus, Circle highlighted potential regulatory risks, such as proposals requiring stablecoin issuers with over $10 billion in issuance volume to either become banks or operate under bank affiliation.

Risk disclosure section from the prospectus

Based on current developments, here is the latest status of U.S. stablecoin legislation:

In February 2025, Senator Bill Hagerty and others introduced the GENIUS Act (Guidance for National Innovation in Stablecoins Act), aiming to establish a federal regulatory framework for payment stablecoins. The bill stipulates that stablecoin issuers with a market cap exceeding $10 billion would fall under Federal Reserve oversight, while smaller issuers could opt for state-level regulation. All issuers must fully back their tokens 1:1 with high-quality liquid assets (e.g., USD, Treasuries), and algorithmic stablecoins would be banned.

At the same time, Representative Maxine Waters introduced the STABLE Act (Stablecoin Transparency, Accountability, and Better Ledger Economy Act), requiring all stablecoin issuers to obtain federal licenses and submit to Federal Reserve supervision. The bill emphasizes consumer protection, mandating full reserve backing, and strict adherence to anti-money laundering (AML) and KYC rules.

As a compliance leader in the stablecoin space, Circle’s risk disclosures are appropriate. Although there were reports that “Tether is collaborating with U.S. lawmakers to influence fiat-backed crypto regulation,” Circle, backed by allies like Coinbase and BlackRock, should be well-positioned to manage regulatory pressures.

Therefore, this risk remains relatively manageable.

Question Five: What Is Circle’s Valuation?

Although Circle’s S-1 filing does not specify an IPO price, secondary market trading suggests a current valuation of around $4–5 billion. Its equity structure includes Class A shares (1 vote/share), Class B shares (5 votes/share, capped at 30%), and Class C shares (no voting rights), ensuring founder control. The IPO will also provide liquidity for early investors and employees.

Compared to its previous funding round peak valuation of $9 billion, this represents a 50% drop—attributable to declining stablecoin market share and broader market downturns. Still, there remains room for profit.

In comparison, Coinbase currently trades at $151.47 per share, with a market cap of $38.455 billion—about 8–9 times that of Circle.

Additionally, due to the tariff war initiated by the Trump administration, delayed Fed rate cuts could impact Circle’s revenue—another factor worth considering.

Whether Circle’s future diversified business lines can justify its valuation remains to be seen.

In the author’s view, compared to the more flexible-use USDT, USDC needs to integrate deeper with U.S. banking services to unlock greater growth. For example, U.S. banks Custodia Bank and Vantage Bank recently launched Avit—the first bank-issued stablecoin on a permissionless blockchain (Ethereum)—hinting at increasingly fierce competition in the next phase of stablecoin development.

If Circle wants to maintain its position as the “number two stablecoin issuer,” it may need to learn from Tether’s revenue strategies, such as holding BTC in reserves and charging redemption fees.

Finally, a “hidden gem” from Circle’s prospectus: The company disclosed that as a “remote-first” organization, it faces elevated operational and cybersecurity risks. Given the February incident where Bybit lost $1.5 billion in assets, and prior breaches attributed to North Korean hacker group Lazarus, this warning is not baseless—it’s a risk factor all crypto projects must proactively address.

Circle’s official disclosure on remote work risks

In conclusion, the author predicts Circle will proceed with its IPO earlier than other crypto firms like Kraken and Chainalysis. For a stablecoin company burdened by high operating costs and limited narrative appeal, accessing “mainstream retail investors” through an IPO is a more urgent priority.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News