A Letter to Saylor: Why Bitcoin's True Value Lies in Circulation

TechFlow Selected TechFlow Selected

A Letter to Saylor: Why Bitcoin's True Value Lies in Circulation

Bitcoin's role as a medium of exchange is twice as significant as its store of value function.

Written by: Bitcoin Magazine

Translated by: Wu Zhu, Jinse Finance

Michael Saylor, you're forced to recognize that all store-of-value (SoV) assets are flawed, pushing you to focus on the only asset without flaws. That doesn't mean you're immune to the state of medium-of-exchange (MoE). When you look at the real estate market from one angle, you see how massive it is; from another, how terrible. But if you've experienced the pain of trying to preserve billions in purchasing power, housing becomes a decent tool.

Your obsession with SoV completely misses the point. Bitcoin’s greatest feature is its role as a medium of exchange. Although fiat systems increasingly separate money's functions, that doesn’t mean they should. I know saying Bitcoin is a medium of exchange stirs up controversy—every other monetary ruler will try to block it. It would be great if they joined instead of fighting it. That would convince all billionaires they can invest their money into it. But using Bitcoin solely for storing value is an attack on it. This approach turns it into digital gold 2.0—captured and constrained.

No medium of exchange means no store of value! The medium of exchange comes first. You receive Bitcoin through transactions, then store it. If store of value were the main point, imagine announcing you lost your Bitcoin stack’s private key—you could still “perfectly” store it, but without the medium-of-exchange function, the market would erase its top-layer fictional fiat value. That value exists precisely because Bitcoin remains liquid and usable in trade.

An oxygen tank is crucial for reserves, but breathing matters more. Store of value is secondary, dependent on exchange capability. Without transactional ability, store of value is meaningless. Michael, you personally experienced this when your million-dollar assets in Argentina were diluted by 90%. You struggled to preserve value—not because you didn’t foresee it coming, but because you couldn’t use it as a medium of exchange. Indeed, poor store-of-value weakens the medium of exchange, but why does the latter take priority? Because exchange capacity is what enables you to react.

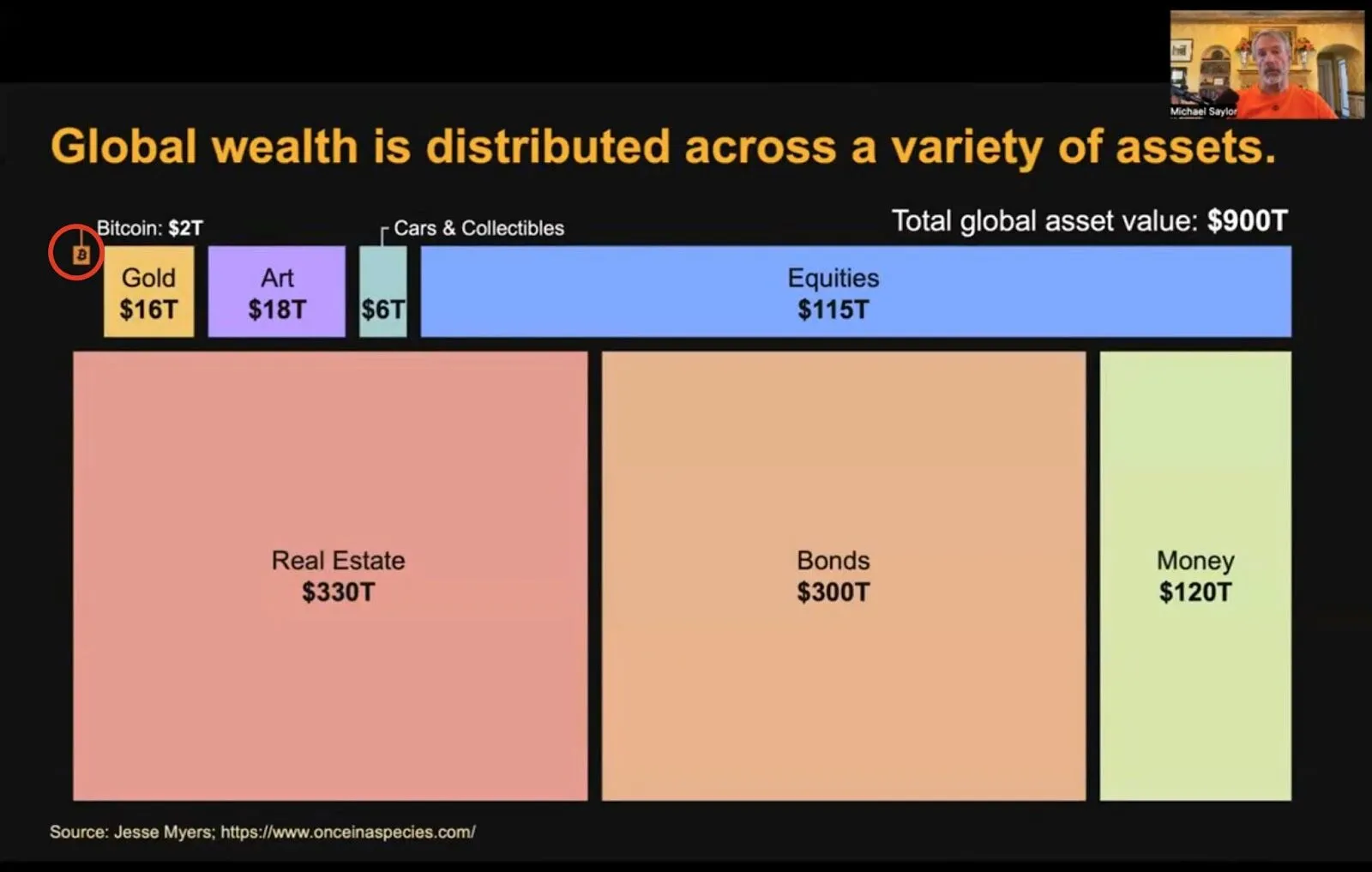

By now, most people who’ve touched Bitcoin know the chart by Jesse Myers that you promote. You claim there’s no better idea than a clean $9 trillion store of value, then immediately call Bitcoin one of the world’s most liquid markets, operating 24/7. Guess what? Liquidity means medium of exchange.

Now, let’s break down Jesse’s chart, starting with real estate. Valued at $330 trillion, it’s an extremely poor medium of exchange, with only $13 trillion traded annually. Regulations and taxes make property transactions harder. Still, because it’s over 100 times better as a store of value, billionaires favor it, dominate the market more each year, and increasingly exclude younger generations.

A house may be valuable, but its appreciation doesn’t come just from itself—it stems from connections to nearby utilities. Build a road to it, and its value rises. Add a supermarket or gas station, or connect it to the grid, and value climbs again. Networks create opportunities for energy inflow, increasing chances to convert energy into economic value (like money). Thus, transactions within the network are what boost a house’s worth. But I see the flip side: if you’re a billionaire and everyone covets your resources, you won’t want a large network built around your home. You’ll prioritize privacy. The house may depreciate, but the goal shifts to raising others’ costs of access, reducing exposure to attacks.

What about bonds? Worth $300 trillion as a store of value, with $140 trillion traded annually and $25 trillion in new issuances. This implies its annual use as a medium of exchange accounts for roughly 50% of its total value. In this sense, it’s better than real estate, but the numbers still show it’s primarily used as a store of value.

Next, stocks. Valued at $115 trillion, with about $175 trillion traded annually. This indicates their strength as a medium of exchange outweighs their store-of-value role. Take MicroStrategy stock—something you understand better than anyone. How much value did it store last year, versus how much was transacted through it?

The next two categories are interesting. The art industry has such minimal annual trading volume it isn’t even shown on the chart. Meanwhile, cars and collectibles generate nearly $4 trillion in annual transactions. This highlights how these are mainly seen as stores of value each year—but also reveals how poorly real estate performs as a medium of exchange—even worse than the car market.

Ah, gold! Gold enthusiasts passionately declare it has existed for over 5,000 years, calling it the ultimate store of value for whatever reason—but it makes up only 1.78% of the store-of-value market. This shows that once stripped of its exchange role, it becomes easily captured and manipulated. Sorry, gold bugs, that genie isn’t going back in the lamp. Gold holds $16 trillion in value, and gold lovers claim it could store $120 trillion worth of capital. They desperately want to get rich, but the market disagrees, valuing flawed fiat currency tenfold above shiny, lifeless rock. Is gold a better medium of exchange? With $54 trillion traded annually—driven by derivatives—its exchange usage is 3.5 times its store-of-value role.

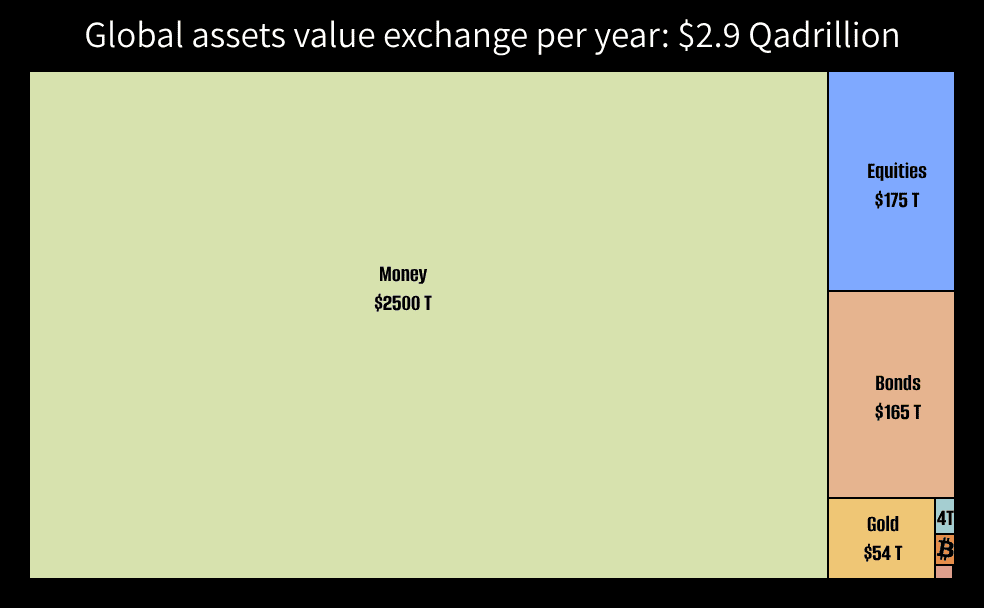

Currency may not dominate in asset-based store-of-value, but it’s far ahead as a medium of exchange. No other store-of-value asset comes close. What if the U.S. dollar—the top currency—became purely a store of value? It would destroy the dollar’s network. As non-U.S. asset networks step in to meet demand, non-U.S. asset values would rise. Over time, their store-of-value assets would appreciate while dollar-denominated assets plummeted. Global currency supply is about $120 trillion, but look at major central bank transaction volumes: Fedwire ~$1,182 trillion, TARGET2 ~$765 trillion, CHAPS ~$145 trillion, others (partial) ~$500 trillion (conservative estimate due to incomplete data). So while store of value stands at $120 trillion (per Jesse’s chart), the transactional utility of these networks exceeds it by over 20x—around $2,500 trillion. What if we include 2 billion unbanked people? How many transactions would that enable? What if microtransactions became possible?

Where does Bitcoin fit among all this? The mainstream narrative urges holders never to sell, positioning Bitcoin solely as a store of value. Yet the market tells a different story. In 2024, Bitcoin reached a $2 trillion market cap, while value transacted on its Layer 1 blockchain hit $3.4 trillion. Accounting for the Lightning Network (though exact figures remain elusive), the total may approach $4 trillion. This suggests Bitcoin’s role as a medium of exchange is twice its store-of-value function. So what happens when the long-standing “HODL forever” narrative begins to fade?

Due to fiat’s flaws, bonds and stocks are financial “instruments” pretending to be money. This creates a market that blocks most people from protecting their wealth, further splitting money’s store-of-value function. But how inclusive are these instruments? Or are they merely tools siphoning value from fiat mediums of exchange, channeling it into the hands of privileged individuals, billionaires, and others who hoard?

Globally, only 10–20% of people have exposure to bonds, mostly indirectly through pensions or investment funds, not direct ownership. For stocks, it’s 15–25%. This means up to 80% of humanity lacks access to these tools for self-protection, leaving them vulnerable to exploitation. Separating store of value from medium of exchange creates an extractor vs. extracted dynamic. This amplifies the “Cantillon Effect”: those who can print the medium of exchange buy up store-of-value assets, marginalizing 80% or more. It’s a feedback loop that weakens the system and widens the gap between rich and poor. The more money printed, the weaker money’s store-of-value function becomes.

Another critical part of the entire system is fees. Sending dollars through the banking system costs money—a service fee. But what’s the cost when converting from a medium of exchange to a store-of-value instrument? Much higher. This creates massive friction across the system, preventing the poor from storing value. At this point, the medium of exchange increasingly becomes an extraction medium, not a transactional one. This is also why the store-of-value case appears more attractive within the fiat system.

Bitcoin doesn’t pretend to be money like everything else; it’s the first artificial currency that doesn’t corrode like melting ice and doesn’t discriminate. It’s money for those who choose it. With no printer, no one wants to trade it for a “better” store of value—there is no second best. Even those without Bitcoin can use it to shape the lives they want. They’re no longer chasing money to store something, but building on Bitcoin anything that enriches their lives.

The most important idea isn’t storing value, but transferring value. But to transfer value, you must first store some. And again, to store some, someone must first transfer it to you. That’s why the wealthy prefer assets that don’t melt away like ice. Meanwhile, those starting their careers focus more on acquiring value than storing what they don’t yet have.

Why does the store-of-value narrative attract so much attention? One reason might be the effort involved. With store of value, you simply buy and hold—no need to do any work to improve your life. With a medium of exchange, you must actively grow your savings and persuade others to pay you in Bitcoin for goods or services. Another factor: for most people, their fiat portfolio still exceeds their Bitcoin holdings. Only when Bitcoin surpasses their fiat balance will they consider using it to enhance their lives. This shift isn’t hard for the majority of the world’s population lacking savings or assets. Perhaps this explains why the current system refuses to let them exit, instead promoting dependency via Bitcoin custody—trading one dependency for another.

Even rigidity ties into the need for more medium of exchange. Michael, you strongly advocate rigidity, but if Bitcoin isn’t used to reach more people, you’re delaying its adoption. Unlike you, the U.S. knows that to make the dollar the world reserve currency, it must widely distribute it to lock in network effects. They see the network as key to rigidity, and since printing and sharing bills is cheap, it works easily. For Bitcoin, absolute scarcity requires balancing distribution and storage. But that doesn’t mean you shouldn’t spend a single satoshi.

The analogy of storing fat in the body is key to long-term survival. True, but it ignores the need for stable food income before fat storage—to sustain life. Without income, there’s nothing to store—so transactions come first. However, for someone unconcerned about hunger, the focus shifts to storing food to prevent spoilage. I keep emphasizing this to highlight your bias toward store of value, which distorts your judgment and misleads others.

At this stage of my Bitcoin journey, I’m certain of this: chasing money corrupts you. Bitcoin changes that—it stops your endless pursuit of money, letting you use it to live the life you want. What happens when you have enough of what you desire? Then what? With Bitcoin, this is entirely possible, and every Bitcoin user should prepare an answer for that moment. Yet chasing money is a bottomless pit you can never fill. The Bible says the love of money is the root of all evil. I agree—but how does it work? What’s the mechanism? Chasing money—making it the priority, relegating everything else—is the mechanism.

You’re not building a Bitcoin standard—you’re stacking a deck of cards. Like gold in the past, this time you’re hoarding Bitcoin from individuals and institutions, further cementing the fiat standard. Saylor, you’re not attacking the dollar as some believe—you’re supporting it by boosting your stock and its ecosystem. Instead, you speculatively harm those funding your Bitcoin purchases. You don’t just hurt them; by strengthening the dollar, you worsen suffering for other currency holders. Hoarding Bitcoin under the world’s gaze? This isn’t a network city—it’s a gated estate funded by their own money.

I wonder if people would willingly invest their Bitcoin into your securities. How many truly would? I’m sure true Bitcoin maximalists wouldn’t trade their perfect store-of-value asset for fiat “instruments.” Ask yourself: at this point, would you use your Bitcoin to buy Apple stock? After all, you did invest in them before. It makes no sense—I give you Bitcoin just so you turn it into something fiat, pay fiat fees, support fiat custodians and third parties, just so you can buy Bitcoin again on the other end.

Finally, I have no proof, but I’m quite certain you already know everything I’ve said in this article/message. While addressed to you, Michael, it’s aimed at those who see you as the new Bitcoin Jesus—blindly following you without questioning your actions. They make reckless bets in their lives—bets that could wipe out their Bitcoin—without the financial safety nets and interest rates you possess. The message you convey doesn’t apply to most people.

Bitcoin isn’t just another asset or financial tool—it’s borderless, permissionless money. Treating it otherwise diminishes its true value. Simply storing it won’t bring freedom. Letting Sats flow builds the network. Letting Sats flow fosters collaboration for a better future. Letting Sats flow strengthens the ecosystem. Save some for tomorrow, but don’t be the richest man in the graveyard—leave a plan to keep using them in the future.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News