Bitcoin funding rate hits three-month low—what did the bears already know?

TechFlow Selected TechFlow Selected

Bitcoin funding rate hits three-month low—what did the bears already know?

BTC funding rate plunges to a three-month low ahead of the NFP report; the derivatives market sees risk before any narrative.

Author: CryptoSlate

Translated & edited by TechFlow

TechFlow Intro: This article explains a critical market mechanism: before macroeconomic data releases, the Bitcoin derivatives market had already clearly signaled risk across three dimensions—funding rates, open interest, and liquidations. Understanding this logic reveals real market stress earlier than chasing any narrative.

Full Text Below:

The Bitcoin derivatives market offers the best explanation for this week’s macroeconomic pressure.

Funding rates plunged sharply into negative territory, open interest remained elevated, and then the U.S. jobs report was released. Taken together, these three developments indicate that the market had already heavily positioned itself for downside hedging well before the arrival of an actual macro catalyst.

This sequence matters—it reveals how macro volatility enters the crypto market.

It typically appears first in perpetual contracts—the venue with the fastest hedging speed and highest leverage usage.

The funding rate tells you which side is paying to maintain its position; open interest tells you how much position remains outstanding in the system; and liquidation data tells you when those positions begin to collapse.

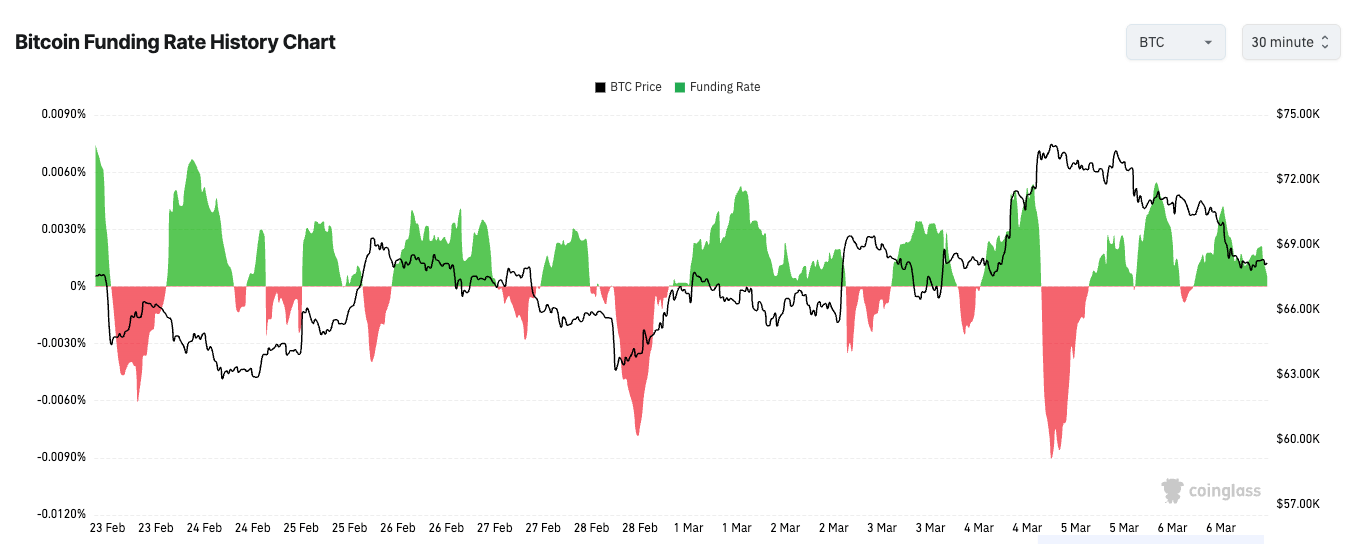

On February 28, Bitcoin perpetual contract funding rates dropped to approximately -6%, among the most negative readings in the past three months. Open interest denominated in BTC rose from roughly 113,380 BTC at the start of the year to 120,260 BTC.

This combination is significant because it points simultaneously to two things: traders are aggressively betting on downside, and they’re doing so amid rising leverage. The market is both highly anxious and highly crowded.

This is the simplest way to understand how macro pressure enters the crypto market.

It shows up on the derivatives ledger—not as a polished X narrative or a tidy economist’s report. Traders act there first because perpetual contracts offer high liquidity, low usage costs, and immediate availability.

When they grow concerned about growth, interest rates, or broader risk sentiment, they short perpetuals; these contracts trade below spot, pushing funding rates negative, as shorts must pay longs to maintain their positions.

Why Negative Funding Rates Persist

Yet a negative funding rate alone is not a bottom signal—it merely indicates the direction in which the market is tilting.

This distinction is crucial, because traders love turning every extreme reading into a forecast.

Extremely negative funding rates can foreshadow short covering, and last week’s setup clearly created that possibility. But when hedging demand is genuine, such extremes can persist longer than expected.

Sharp spikes and drops in funding rates reflect one-sided positioning, which may endure during strong directional moves.

Such persistence usually stems from two sources.

Some traders hedge genuine spot exposures—meaning they aren’t precisely forecasting the next move but rather protecting their portfolios. Others are simple trend followers, willing to pay funding fees as long as the market continues moving in their favor. Both groups can sustain negative funding rates even after the initial panic has subsided.

That’s why the true signal isn’t whether funding rates are negative. A more interesting setup emerges when funding rates remain persistently and significantly negative while price fails to make new lows. At that point, pressure begins accumulating beneath the surface: shorts continue paying to hold positions, yet the market no longer rewards them in the same way. That’s how conditions for short covering form.

The Jobs Report Delivered Real Macro Input

This week’s macro catalyst came from the U.S. labor market. On March 6, the Bureau of Labor Statistics reported a decline of 92,000 nonfarm payrolls in February and an unemployment rate of 4.4%.

Such reports trigger broad repricing, as they touch multiple market themes simultaneously. A weaker labor market could push yields lower if traders believe the Fed may adopt a more dovish path. It could also dampen risk appetite if traders interpret the data as a sign of genuine economic softening.

Crypto markets often feel this debate more acutely, because leverage transforms macro concerns into position events.

If traders are already heavily shorted, even a brief easing in financial conditions—triggered by macro data—could spark a sharp price rally as shorts are forced to cover.

If the data deepens risk-off sentiment, the same crowded positioning could exert continued downward pressure, as shorts remain comfortable while longs begin capitulating.

Funding rates act as a pressure gauge; open interest serves as fuel; and liquidations mark the moment pressure bursts through the system.

Liquidation Data Is the Scoreboard

Liquidation data tells you whether price action is orderly or reactive.

Short liquidations typically confirm a covering event; long liquidations typically confirm a downside washout. When both sides are liquidated within a short timeframe, the market signals that volatility has taken control—and neither side has much room left to defend its position.

That’s why liquidation data works best as a confirmation layer. Funding rates set the stage—but liquidations tell you whether those conditions have actually forced price movement.

Open interest matters here too. If participation shrinks concurrently, falling prices and negative funding rates tell us little.

This may simply mean traders are stepping aside to wait. But when open interest rises alongside negative funding rates, it signals that new bearish or defensive positions are being established.

Tracking open interest in BTC terms removes some distortion caused by price volatility, making a rise in BTC-denominated open interest during a price decline a clearer indicator of growing market participation.

From this perspective, last week wasn’t truly about Bitcoin’s strength or weakness—it was about where pressure was building.

The derivatives market had already revealed a heavily shorted or hedged structure before the jobs data landed.

The jobs report then delivered a tangible macro input for global markets to process.

When these two developments converged, crypto markets did what they typically do: express the same macro uncertainty faced by everyone—via larger candles, faster reversals, and more violent position unwinds.

Funding rates don’t predict price—they only reveal which way leverage is tilted. Open interest doesn’t tell you who’s right—it only reveals how many positions remain active. Liquidation data doesn’t explain the entire move—it only tells you when price action becomes involuntary.

That’s why derivatives ultimately became the best macro interpreter this week. Before narratives settle, the ledger had already laid out the risks clearly: traders were shorting, leverage remained in the system, and the jobs report gave the market a concrete reference point for reaction.

Everything that followed was simply price discovering just how crowded the room had become.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News