Circle Attempts IPO Again Amid Skepticism: Valuation Nearly Halved, a Desperate Monetization Effort Amid Profit Pressure?

TechFlow Selected TechFlow Selected

Circle Attempts IPO Again Amid Skepticism: Valuation Nearly Halved, a Desperate Monetization Effort Amid Profit Pressure?

Concerns about Circle's business outlook have also been raised by the market, due to issues such as nearly halved valuation, heavy reliance on U.S. Treasury income, and high revenue-sharing costs eroding profits.

Author: Nancy, PANews

After years of failed IPO preparations, Circle, the issuer of the stablecoin USDC, has once again filed with the U.S. SEC for a proposed listing on the New York Stock Exchange. However, concerns over its nearly halved valuation, revenue heavily reliant on U.S. Treasuries, and high distribution costs eroding profits have raised market skepticism about Circle's business prospects.

Valuation Nearly Halved, Equity Swap with Coinbase Secures Full USDC Issuance Rights

One day before the U.S. House planned to revise and vote on the GENIUS Act—the stablecoin regulatory bill—documents from the SEC website revealed that Circle submitted an S-1 filing to conduct an initial public offering under the ticker “CRCL” and apply for listing on the New York Stock Exchange. Meanwhile, Circle has engaged JPMorgan Chase and Citibank to assist with its IPO; both institutions were also part of the financial advisory team for Coinbase’s IPO.

However, Circle did not disclose specific details such as the number of shares to be issued or the target price range in this prospectus. Circle’s valuation has fluctuated significantly along with market conditions and its own scale—rising from $4.5 billion during a SPAC merger deal in 2021, increasing to $9 billion after revising the merger agreement in 2022, then falling to around $5 billion based on secondary market trading valuations in 2024. According to Forbes, in this traditional IPO plan, Circle is targeting a valuation between $4 billion and $5 billion, nearly half its peak value.

Prior to the IPO, Circle fully secured control over USDC issuance rights. As reported by The Block, in 2023, Circle acquired the remaining 50% equity stake in Centre Consortium—a joint venture responsible for issuing the USDC stablecoin originally co-founded by Coinbase and Circle in 2018—for $210 million worth of Circle stock. The Centre Consortium stake had previously been held by Coinbase.

In the "Material Transactions" section of its IPO prospectus, Circle disclosed: “In August 2023, concurrent with entering into a cooperation agreement, we acquired the remaining 50% equity interest in Centre Consortium LLC from Coinbase.” The transaction consideration consisted of approximately 8.4 million shares of Circle common stock, valued at a total fair value of $209.9 million. Following the acquisition, Centre became a wholly-owned subsidiary of Circle and was dissolved in December 2023, with its net assets transferred to another wholly-owned subsidiary of Circle. Coinbase similarly disclosed that it received Circle equity granted under the agreement rather than cash payment. This means Circle used its own shares to gain full control over USDC issuance, a move that does not directly impact Circle’s cash flow.

In fact, Circle began preparing for an IPO as early as 2021, when it reached a merger agreement with SPAC company Concord Acquisition Corp. to go public via a SPAC route. However, the deal was delayed due to lack of SEC approval and ultimately terminated by the end of 2022. In January 2024, Circle again indicated it had secretly submitted an IPO application, stating it would proceed once SEC review procedures were completed.

Compared to previous attempts, the context surrounding this latest filing has significantly changed: the stablecoin market has experienced qualitative growth and strong momentum, with stablecoins like USDC gaining increasing influence in global finance. At the same time, the U.S. maintains a positive stance toward compliant stablecoins, creating more room for development in the sector. Major players including JPMorgan, PayPal, Visa, Fidelity, and Ripple are all moving into stablecoins, while even Trump-affiliated project WLFI plans to launch one. Additionally, amid increasingly clear U.S. crypto regulations, companies such as Kraken, eToro, Gemini, and CoreWeave are also pursuing IPOs.

Revenue Heavily Reliant on U.S. Treasuries, High Fees Paid to Coinbase Erode Profits

Nevertheless, Circle’s IPO prospects face multiple challenges, sparking intense debate over its core business model and profitability.

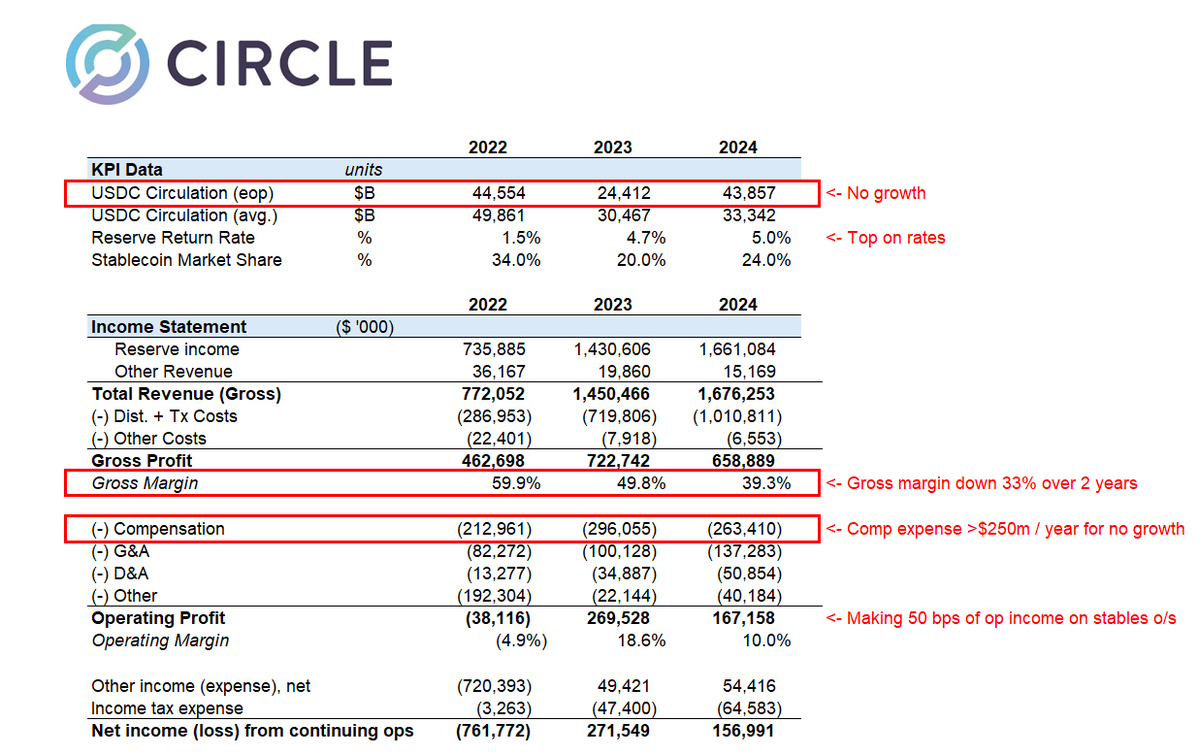

First, Circle’s revenue is highly dependent on U.S. Treasury yields, a model now under threat amid expectations of Federal Reserve rate cuts. According to IPO documents, Circle generated $1.676 billion in total revenue in 2024, with growth primarily driven by reserve income—the interest earned from USDC reserves—which accounted for over 99% of total revenue. This interest income largely comes from U.S. Treasuries. In essence, Circle’s revenue model resembles a U.S. Treasury arbitrage play.

Second, high distribution costs further eat into Circle’s profits. In 2024, Circle posted a net profit of $155.67 million, down 41.8% compared to 2023. This decline stems from sharply rising distribution and transaction expenses, which totaled $1.0108 billion in 2024—60.7% of total revenue—an increase of 40.4% year-over-year. Coinbase serves as the primary distribution platform for USDC. As previously disclosed in Coinbase’s financial reports, Coinbase alone earned $225.9 million from USDC in Q4 2024, with annual revenue expected to reach approximately $900 million. This suggests Circle is spending increasingly more to maintain USDC liquidity across ecosystems, without corresponding revenue growth.

In fact, according to the S-1 filing, Coinbase, as a key partner, receives 50% of the residual returns from USDC reserve earnings. Coinbase’s share is directly tied to the amount of USDC held on its exchange. The document notes that as the volume of USDC hosted on Coinbase increases, so does its revenue share; conversely, it decreases if holdings fall. In 2024, the proportion of USDC held on Coinbase platforms rose dramatically from 5% in 2022 to 20%.

Matthew Sigel, Head of Digital Asset Research at VanEck, stated that although overall revenue has grown, the sharp rise in distribution and transaction costs has negatively impacted Circle’s EBITDA (earnings before interest, taxes, depreciation, and amortization) and net profit. Circle itself warned that Coinbase’s business strategies and policies directly affect USDC distribution costs and revenue sharing, yet Circle cannot control or regulate Coinbase’s decisions.

To reduce reliance on Coinbase, however, Circle has actively expanded its global partnerships in recent years, collaborating with major digital finance firms such as Grab, Nubank, and Mercado Libre.

Yet, according to Omar Kanji, Partner at Dragonfly Capital, there is nothing promising visible in Circle’s IPO filing, nor is it understandable how it could justify a $5 billion valuation. Interest income is severely eroded by distribution costs, the key revenue driver—interest rates—has already peaked and is now declining, the valuation appears astronomically high, and annual compensation expenses exceed $250 million. It feels more like a desperate attempt to monetize quickly and exit before larger players enter the space.

"As Nubank, Binance, and other major financial institutions begin partnering with Circle, it remains unclear how the market will assess its distribution network and Circle’s net profit margins. Market reception will depend partly on how effectively Circle communicates this to investors, executes the narrative it presents to the market, which stablecoin legislation prevails, and most importantly, how the market evolves and how widely stablecoins are adopted. If USDC becomes dominant, Circle could still command high valuation multiples even if its take rate declines, given its vast potential addressable market. Regardless, several points are clear: 1) The model of sharing revenue with B2B partners will persist long-term; 2) As the overall stablecoin market grows, issuers’ profit margins will narrow; 3) Issuers must diversify revenue sources beyond net interest margins," said Wyatt Lonergan, Partner at VanEck Ventures.

Overall, despite improved U.S. crypto regulatory conditions and growing enthusiasm in the stablecoin sector providing a favorable window for listing, whether Circle can strengthen its competitiveness through the IPO remains uncertain, especially under dual pressures of anticipated Fed rate cuts and surging marketing costs.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News