TSMC Confirms AI Computing Power Shortage to Last Until at Least 2027; H100 Rental Fees Surge 30% in Six Months; Cloud Providers Jointly Raise Prices

TechFlow Selected TechFlow Selected

TSMC Confirms AI Computing Power Shortage to Last Until at Least 2027; H100 Rental Fees Surge 30% in Six Months; Cloud Providers Jointly Raise Prices

The computing power shortage is no longer a prediction—it is an ongoing reality.

Author: Claude, TechFlow

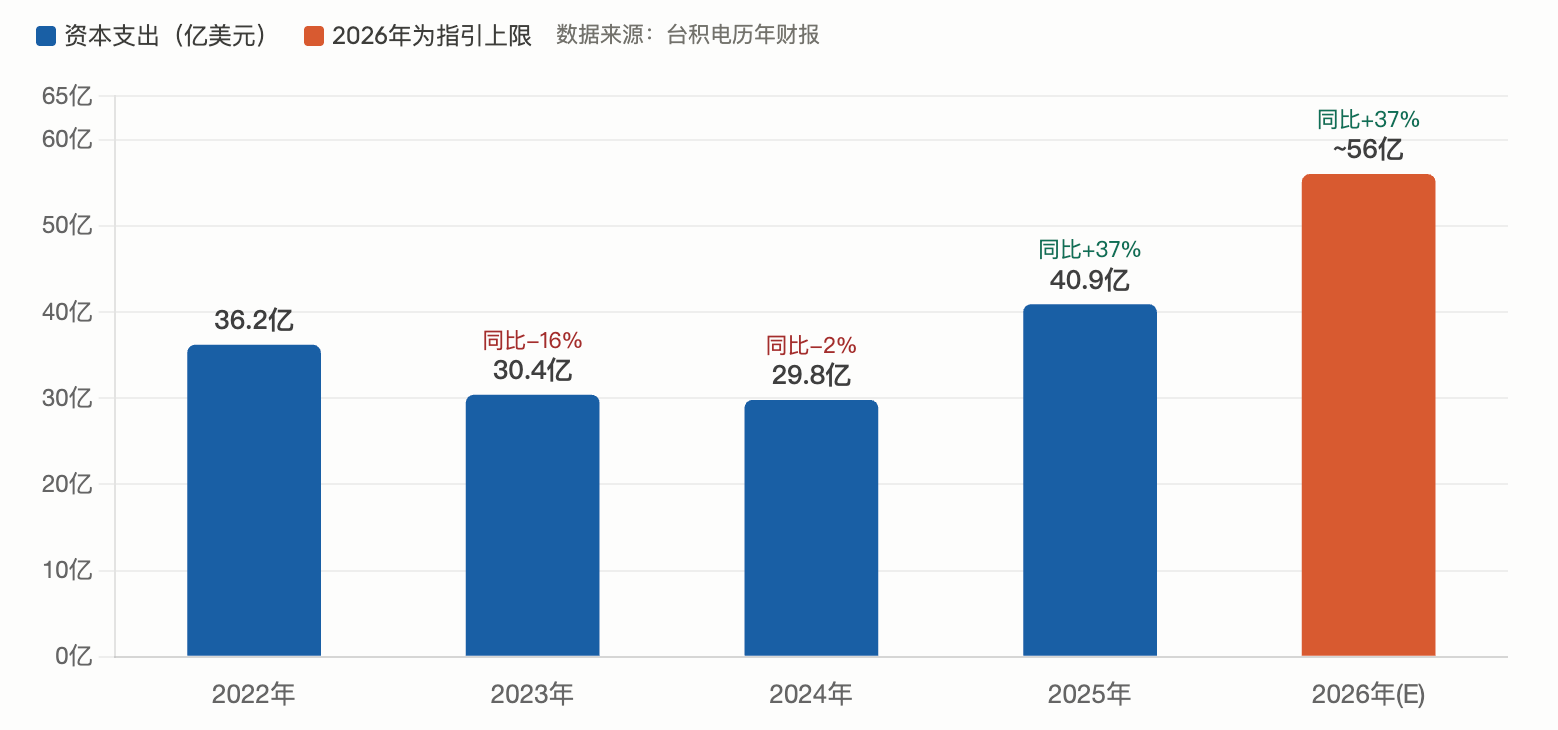

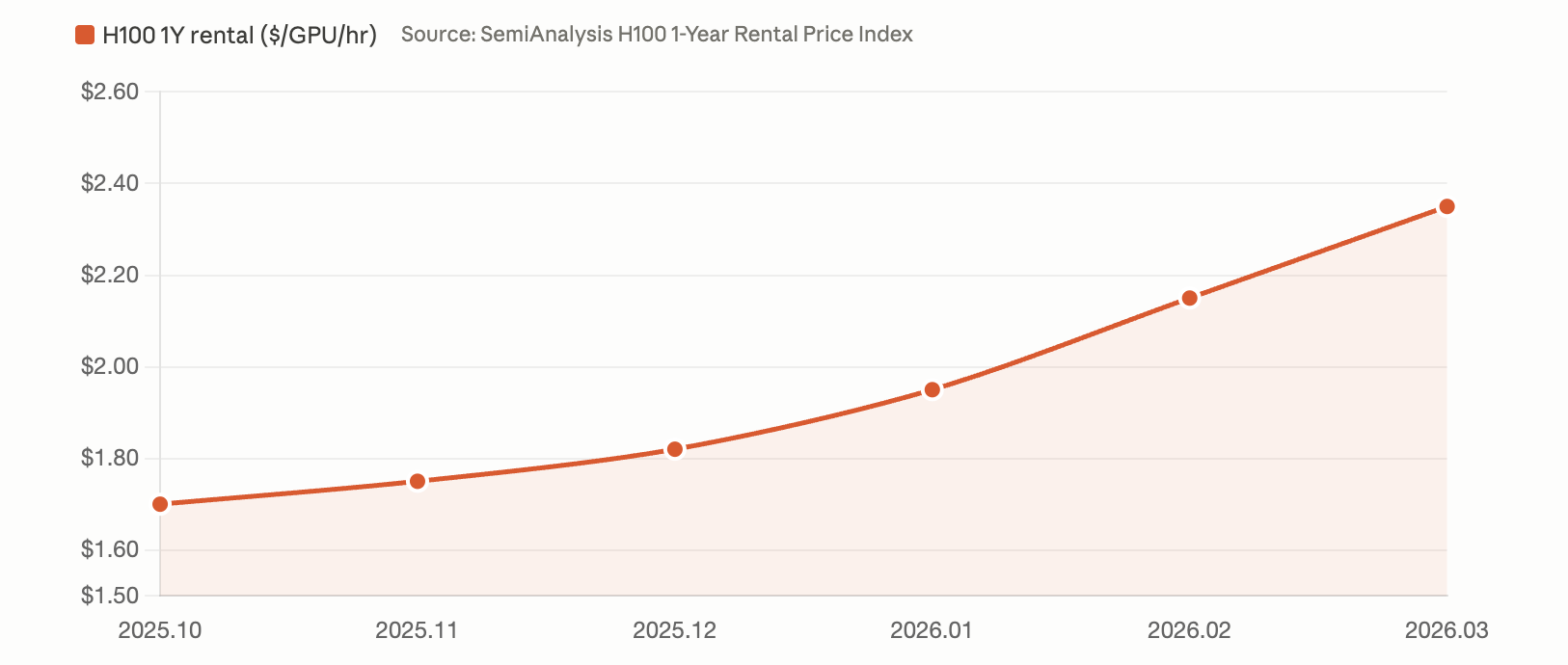

TechFlow Introduction: TSMC’s Q1 revenue reached $35.9 billion—exceeding expectations—while its capital expenditure guidance was raised to the upper end of its $52–$56 billion range, i.e., nearly $56 billion. CEO C.C. Wei stated that AI demand is “extremely strong” and that supply shortages will persist for at least another three years, through 2027. Meanwhile, SemiAnalysis data shows H100 one-year rental rates surged from $1.70/hour in October last year to $2.35/hour in March this year—a near 40% increase. China’s daily token usage has grown over 1,000-fold in two years; Tencent Cloud, Alibaba Cloud, and Baidu Intelligent Cloud have all raised prices multiple times this year. From chip manufacturing to GPU leasing and model inference, the entire AI infrastructure stack has entered a pricing-up cycle.

The compute shortage is no longer a forecast—it is an unfolding reality.

On April 16, during its Q1 earnings call, TSMC delivered the clearest supply timeline yet: “AI chip shortages will persist for at least another three years, through 2027.” On the same day, Caixin Media, citing multiple industry insiders, reported that NVIDIA H100-series GPU rental rates have risen approximately 20–30% since last October, while the entire H-series is effectively “out of stock”; all upcoming Blackwell-generation capacity scheduled to come online before September 2026 has already been fully booked.

TSMC: “Extremely Strong” AI Demand, New Fab Construction Takes 2–3 Years—No Shortcuts

TSMC’s Q1 revenue reached $35.9 billion (USD), up over 40% year-on-year and slightly above the upper end of its guidance. Its high-performance computing (HPC) business grew 20% quarter-on-quarter and accounted for 61% of total revenue—the primary growth engine.

A more critical signal comes from capital expenditure. TSMC has raised its full-year 2026 capex budget to the top end of its prior $52–$56 billion guidance range—nearly $56 billion—more than half of its total capex over the past three years ($101 billion).

In the earnings call, TSMC Chairman and CEO C.C. Wei offered just one sentence explaining the capex increase: “Demand is extremely strong—especially for high-performance computing and AI applications. We are accelerating efforts and procuring equipment earlier, but supply remains tight.”

When JPMorgan analysts directly asked how long the supply crunch would last, Wei responded unequivocally: building a new fab takes 2–3 years, and ramping capacity takes additional time; based on current progress, supply constraints are expected to continue through at least 2027. He repeatedly emphasized: “There are no shortcuts.”

To address the demand shortfall, TSMC announced an unprecedented global 3-nanometer capacity expansion plan. Historically, TSMC stops adding capacity once it reaches target output for a given node—but this time, it broke precedent: a new 3-nanometer fab in Tainan Science Park (mass production in first half of 2027); Arizona Fab 2 adopting 3-nanometer process (mass production in second half of 2027); and a second Japanese fab planned for 3-nanometer (mass production in 2028). Additionally, existing 5-nanometer tools in Taiwan are being retrofitted for 3-nanometer production.

Wei stated that TSMC is “fully confident” in the long-term AI trend and expects capex over the next three years to be significantly higher than over the past three. The company’s full-year 2026 revenue guidance calls for over 30% year-on-year growth.

H100 Rental Rates Surge in Six Months; Entire H-Series “Out of Stock”

On the same day TSMC confirmed upstream capacity bottlenecks, downstream GPU leasing market data validated the strength of real-world demand.

This month, semiconductor research firm SemiAnalysis released its H100 one-year lease price index, showing H100 contract rates rose from $1.70 per GPU per hour in October 2025 to $2.35 in March 2026—a near 40% increase. This index is based on monthly surveys of over 100 market participants, including NeoCloud providers and compute buyers/sellers.

Multiple domestic compute industry insiders interviewed by Caixin Media cited slightly lower increases than SemiAnalysis’s global figures—but directionally consistent: “H100 rental rates have risen roughly 20–30%.” In absolute terms, H100 rack-inclusive monthly rents have rebounded from previous lows of RMB 40,000–50,000 to RMB 80,000–90,000. Not only H100s, but the entire H-series has seen broad-based rent hikes.

According to SemiAnalysis’ survey, half of the GPU suppliers surveyed reported the H-series as “out of stock”; most said they had no expiring H-series cards available for subleasing, and some H100 contracts feature renewal terms stretching up to four years. All upcoming Blackwell-series capacity scheduled to go online before August–September 2026 has likewise been fully reserved.

Cloud Providers Raise Prices Collectively—Cost Pressure Propagates Up the Chain

The direct consequence of token scarcity is across-the-board price hikes by cloud and model providers.

On March 11, Tencent Cloud announced price increases for its Hunyuan series models, with input/output pricing rising over fourfold. On March 18, Alibaba Cloud announced up to 34% price hikes for AI compute and storage products. On the same day, Baidu Intelligent Cloud raised prices for AI compute products by roughly 5–30%. Zhipu has also announced price increases three times this year.

The April price hike wave continues: Tencent Cloud announced on April 9 that effective May 9, list prices for AI compute-related products would rise uniformly by 5%; Alibaba Cloud announced on April 15 that certain model services on its Bailian platform would rise 2–7%, effective May 15.

A compute supply chain insider told Caixin Media about a key price transmission logic: “Historically, major domestic firms leased servers, but now they sell models or tokens directly—so their price hikes are multiples higher. By comparison, hardware cost increases of 20–30% seem modest—driven purely by severe supply shortages and acute scarcity.”

$70 Billion in Capex Chasing Limited Capacity—Supply-Demand Imbalance Unlikely to Ease Soon

Putting TSMC’s supply-side constraints alongside GPU market demand data makes the structural drivers of the AI compute shortage clear: demand growth far outpaces capacity expansion—and new capacity takes years to deliver.

On the demand side, the four hyperscalers—Alphabet, Microsoft, Meta, and Amazon—have collectively guided toward nearly $700 billion in capex for 2026, up over 60% from 2025. NVIDIA holds roughly 85–90% market share in the GPU space, meaning the vast majority of that spending ultimately flows to NVIDIA chips—which are almost entirely manufactured by TSMC.

On the supply side, TSMC’s $56 billion capex is already a record high. Yet constructing a new fab—from groundbreaking to mass production—takes 2–3 years, and capacity ramp-up requires another 1–2 years. The 2-nanometer process only entered mass production in Q4 2025; even TSMC’s global 3-nanometer expansion won’t contribute meaningful incremental capacity until the first half of 2027 at the earliest.

This timing mismatch means that, at minimum through 2027, pricing power for AI compute will remain firmly in the hands of suppliers. For downstream players, rising GPU rental costs, cloud service price hikes, and increasing model inference expenses show no signs of reversal in the near term. For upstream players—including TSMC, NVIDIA, and HBM memory vendors Samsung and SK Hynix—this represents a highly predictable growth window.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News