From Xiang Feng's blockchain origin to the Fourth Industrial Revolution and the token economy engine

TechFlow Selected TechFlow Selected

From Xiang Feng's blockchain origin to the Fourth Industrial Revolution and the token economy engine

"We wanted transatlantic airplanes, but instead we invented Zoom."

Author: Will Wang

It's now 2025. For those within the industry, this cryptocurrency market—having evolved over a long period (more than ten years), weathering multiple bull and bear cycles—is vast and dramatic. Every surviving code ticker today is familiar to us, each carrying a sense of historical weight.

Yet in reality, the total size of crypto assets stands at just $3 trillion, a mere fraction—less than 1%—of the $400–600 trillion traditional financial markets. Despite last year’s groundbreaking Bitcoin ETFs pushed by Grayscale, which disrupted Wall Street, they still struggle to uphold Bitcoin’s claim as "digital gold," failing to align with Nasdaq while diverging from real gold.

In such a market we so fervently pursue, is this merely survivorship bias—or is it a testing ground for a new financial revolution?

As Dr. Xiao Feng stated, to answer this question, we must return to the origin of blockchain, examine cryptocurrencies, crypto markets, and the underlying blockchain technology through first principles and foundational perspectives.

I. Blockchain: The New Financial Infrastructure

If viewed through a single lens—such as that of the U.S. SEC—crypto assets might simply be categorized as commodities or securities. From a macroeconomic perspective, the crypto market could be seen as a niche segment within digital economic development. But if we look deeper into blockchain and draw parallels with past industrial or technological revolutions, blockchain emerges clearly as a new financial infrastructure—one reminiscent of the Age of Exploration, setting sail and forging ahead through stormy seas.

All of this rests on blockchain technology. Therefore, we must return to our origins and ask: What exactly is blockchain?

1.1 The First Principle of Blockchain

The first principle of blockchain is not a single technology, but a systematic integration of decentralization, cryptography, consensus mechanisms, transparency, and incentive structures. This system was crystallized in Satoshi Nakamoto’s 2008 whitepaper:

The Bitcoin white paper combined innovative technologies with a redesigned social production relationship, aiming to transform the centralized financial system centered around traditional banks, solve issues of centralized trust, and offer users a more secure, convenient, and low-cost payment method (a peer-to-peer version of electronic cash (system) would allow online payments to be sent directly from one party to another without going through a financial institution).

Bitcoin: A Peer-to-Peer Electronic Cash System

Extending from Bitcoin’s vision, blockchain’s inherent nature is that of financial infrastructure, fundamentally designed to solve finality in payment and settlement. Cryptocurrencies built on blockchain unlock tremendous advantages: near-instant settlement, 24/7 availability, low transaction costs, and the programmability, interoperability, and composability of tokens within DeFi—features that are both desired and unattainable in traditional financial systems.

Investor Will Wang summarized it well: *In Trustless We Trust*. And if I must add a timeframe, I’d say: ten thousand years.

1.2 The Essence of Finance

What is the essence of finance? It is the temporal and spatial mismatch of value across time and space—a truth unchanged for millennia. But the methods of service evolve: from no banks to banks, from no central banks to central banks.

New finance based on blockchain can dramatically enhance financial efficiency:

A. Across Time

On one hand, this reflects the time value of money—using tomorrow’s money today requires paying interest. When implemented via DeFi, this interest model breaks through the limits of traditional banking capital turnover (around 12 times per year), greatly increasing capital efficiency. On the other hand, instant settlement enables wire transfers from Hong Kong to the U.S. to settle in seconds via Web3, with near-zero fees and no need for reconciliation among five institutions—an optimal solution.

B. Across Space

A clear example occurred in 2023 when Warren Buffett issued nearly zero-interest yen-denominated bonds to heavily invest in high-return Japanese trading companies. However, institutions like banks and central banks often become bottlenecks and barriers to global value flow. This is precisely where new finance breaks through: enabling global cross-border value allocation. In blockchain and Web3, there’s no concept of “going global”—we’re Day One Global. We’re different.

C. Value

Stablecoins, synthetic dollars, or dedicated currencies are essentially USD-pegged tokens. Through digital currency and blockchain technology, the intrinsic attributes of money are further highlighted, core functions strengthened, operational efficiency improved, and costs reduced. Beyond that, tokens on blockchain can represent other assets—like tokenized money market funds (MMF)—whose value transfers can also be completed instantly. Visa has long described itself as being about “money transfer,” but with blockchain, it should now shift to “value transfer.”

Tokenization and Unified Ledger—Blueprint for the Future Monetary System

Just as the essential attribute of money (unit of account) and its core function (medium of exchange) remain unchanged—even as its forms have evolved from seashells and tally sticks to cash, deposits, e-money, and stablecoins—the essence of new finance remains constant. What needs transformation are the service providers—banks, exchanges—and how we deliver better financial services in a distributed, digital environment that transcends time and space.

1.3 The New Financial Revolution

Compared to traditional finance, the greatest innovation of new finance is the change in accounting methods—the public, transparent, global ledger enabled by blockchain. Human accounting has only transformed three times in thousands of years, each profoundly shaping economic forms and social structures, each reflecting the co-evolution of technology and civilization.

Single-entry bookkeeping in Sumerian times (3500 BC) allowed humanity to transcend oral communication, facilitating early trade and state formation through tax and commerce records. Commercial dispute clauses even appeared in Babylon’s Code of Hammurabi.

Double-entry bookkeeping fueled the commercial revolution of the Renaissance (14th–15th centuries). As Mediterranean city-states thrived in trade, Genoese fleets expanded, and the Medici family established multinational banking, complex financial tools became necessary—spurring the rise of banks and multinational corporations, and establishing commercial credit.

Then came what we know today: distributed ledger technology initiated by Bitcoin in 2009, catalyzing decentralized finance, transforming trust mechanisms, and giving rise to digital currencies.

This new finance, rooted in a shift to distributed ledgers, is inseparable from blockchain, smart contracts, digital wallets, and programmable money. Blockchain, as the settlement layer of financial infrastructure, is inherently designed to solve finality in payment and clearing. When digital currencies and smart contracts converge on a distributed ledger, they unlock infinite possibilities: near-instant settlement, 24/7 availability, low-cost transactions, and the programmability, interoperability, and composability of tokens within DeFi.

Thus, new finance brings three major shifts:

First, accounting evolves from centralized double-entry to decentralized distributed ledgers;

Second, accounts transition from bank accounts to digital wallets;

Third, units of account shift from fiat currencies to digital currencies.

Most importantly, distributed ledgers emerge from the digital characteristics of transcending time, space, and organizations—they form the financial foundation of the Fourth Industrial Revolution.

II. The First Three Industrial Revolutions

Dr. Xiao Feng cited research from a Nobel laureate in economics: “The Industrial Revolution had to wait for a Financial Revolution.” This scholar argued that every industrial revolution relied on new financial service models to take root, grow, and scale. Conversely, without a financial revolution, industrial revolutions might never succeed. Another economist further emphasized that each industrial revolution combines energy, industrial, and financial revolutions—with the financial revolution typically serving as the prerequisite.

This research covers the first three industrial revolutions. Now, we are entering the Fourth Industrial Revolution—the era of intelligence and digitization. Let’s first review the previous three:

The First Industrial Revolution (1760s–1840s), marked by the steam engine, began in Britain. The British national debt system and joint-stock banks provided financing for railways and factories, dramatically boosting productivity.

Douglass North, in *The Rise of the Western World* (1973), pointed out that before the Industrial Revolution, Britain’s financial reforms—including national debt systems, improved banking, property rights protection, and reduced transaction costs—created institutional innovations that enabled capital accumulation and risk-sharing for technological breakthroughs like the steam engine and textile machinery. His assertion that “the Industrial Revolution had to wait for a Financial Revolution” captures this phase perfectly.

The Second Industrial Revolution (late 19th to early 20th century), defined by electricity and wireless communication, emerged in the United States. The U.S. financial system—investment banks and stock markets—provided the capital aggregation necessary for technological innovation. For example, railroad construction required massive long-term investment. The U.S. attracted domestic and foreign capital through railway bonds and stocks, with investment banks like J.P. Morgan playing a pivotal role in consolidating fragmented capital.

The Third Industrial Revolution (late 20th to early 21st century), characterized by computers, code, and the internet, also originated in the U.S. The Silicon Valley venture capital model (e.g., Sequoia Capital, KPCB) became the core funding mechanism. VC equity investments provided early-stage capital for high-risk, high-reward tech startups like Apple, Microsoft, and Google. Between 1970 and 2000, annual U.S. VC investment grew from hundreds of millions to hundreds of billions of dollars, directly accelerating the commercialization of semiconductors, software, and internet technologies.

Building on this, the NASDAQ stock exchange, founded in 1971, became the primary channel for tech companies to go public, offering low entry barriers, high liquidity, and openness to tech firms. Companies like Microsoft (IPO in 1986) and Amazon (IPO in 1997) raised expansion capital through IPOs. Instruments like stock options and Employee Stock Ownership Plans (ESOPs) tied human capital to financial capital, attracting talent to innovative enterprises.

III. The Fourth Industrial Revolution

If the fourth financial revolution, built on blockchain, has already met its foundational conditions, then following the logic that “the Industrial Revolution had to wait for a Financial Revolution,” we are now asking: Where will the Fourth Industrial Revolution emerge?

The term “Fourth Industrial Revolution” was formally introduced by Germany in 2013, emphasizing the application of information technology in manufacturing to replace standardized, mass production with highly flexible, intelligent industrial models. However, limiting intelligent IT solely to industrial applications fails to recognize the profound impact of AI- and blockchain-driven technological revolutions on human civilization.

3.1 Cathie Wood’s Vision of Technological Revolution

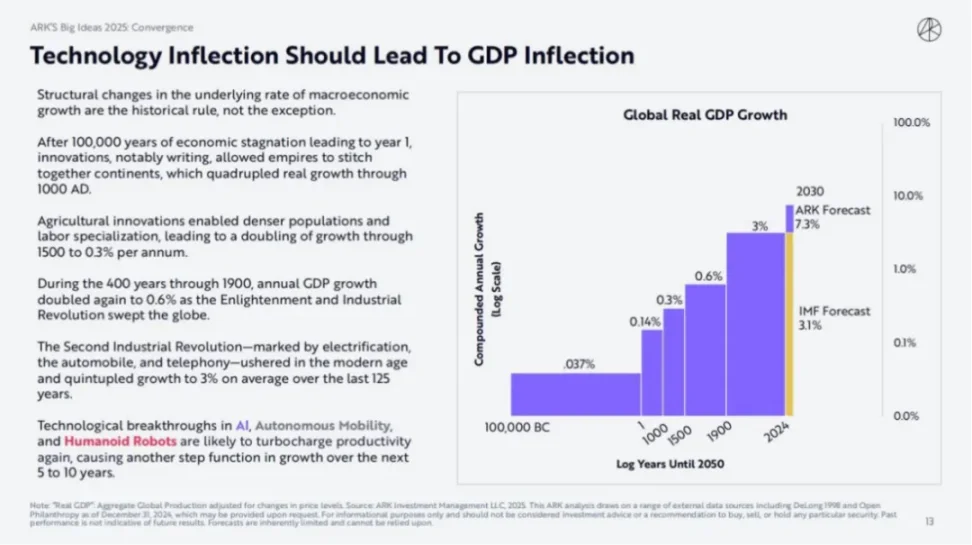

Cathie Wood, known as the “Queen of Tech Investing,” released ARK Invest’s *Big Ideas 2025* report at the beginning of the year. While the IMF predicts global economic growth of 3.1% by 2030, she believes the actual rate could exceed 10%!

ARK Invest argues that macroeconomic growth follows historical patterns of stepwise leaps, each driven by major technological transformations.

For 100,000 years, human economies were stagnant. Innovation—especially writing—allowed empires to connect continents, quadrupling real growth by 1000 AD. Agricultural innovations increased population density and labor specialization, doubling growth to 0.3% annually by 1500.

The First Industrial Revolution raised average annual growth to 0.6%. The Second, powered by electrification, automobiles, and telephones, modernized society and quintupled growth over the past 125 years to an average of 3%.

Without new technological breakthroughs, the IMF’s forecast may hold. But Cathie Wood believes that advances in AI, blockchain, and intelligent robotics could again boost productivity, marking another major technological revolution that elevates global growth within the next 5–10 years.

www.ark-invest.com/big-ideas-2025

3.2 AI Reconstructs the Spatial Dimension of Human Economic Activity

I strongly agree with two points Cathie Wood makes:

1) Each technological revolution lifts economic growth to a new level;

2) AI is a major technological revolution.

By 2025, this is largely uncontroversial. My point is this:

Every technological or industrial revolution fundamentally reconfigures the spatial dimensions of human economic activity—breaking through physical or institutional boundaries and creating entirely new arenas for value exchange. This “expansion of economic space” isn’t just geographic—it’s a dimensional leap achieved through techno-economic paradigm shifts, reshaping how production factors combine, where value is created, and how transaction rules are structured.

The First Industrial Revolution used steam power to move production from workshops to factories, while railroads and steamships expanded trade geographically—integrating surface resources and colonies into a unified capitalist production network. The Second Industrial Revolution, driven by electricity and internal combustion engines, accelerated urbanization and multinational corporations, expanding economic activity beyond local borders to national and global scales. The Third, powered by information technology and especially the internet, created a virtual digital economy—e-commerce, digital services—that completely shattered geographical constraints. The Fourth Industrial Revolution, involving AI, blockchain, and IoT, will further blur the lines between physical and digital spaces, potentially even encompassing economic activities of AI agents in silicon-based worlds.

The greatest value of AI lies in embodied and spatial intelligence, requiring vast numbers of physical robots and virtual AI agents. Investor Wang Chao once noted that if the future becomes a society composed of tens of millions of AI agents, then interactions—between humans, machines, and systems—will require viable solutions. Crypto is one of the few practical frameworks available.

Cathie Wood suggests that AI agents will transform how people search and shop, with digital wallets serving as the carrier. Digital wallets can integrate traditional banking functions—savings, lending, insurance, investment, consumption—and through AI agent paradigms, shift the value chain of global e-commerce and digital consumption upstream.

I similarly believe that only programmable money via blockchain-based smart contracts can handle value flows in an AI-driven silicon civilization, carried by Web3 digital wallets. This implies that the Fourth Industrial Revolution must be built on new finance rooted in blockchain; otherwise, it risks becoming merely a cost-cutting upgrade of traditional finance.

IV. The Token Economy Engine

Britain’s credit and bond markets powered the First Industrial Revolution. America’s investment banks and capital markets drove the Second. The Third was fueled by Silicon Valley’s venture capital (VC) and the NASDAQ stock market. Then surely, doesn’t the Fourth Industrial Revolution demand a new financial model?

As Dr. Xiao Feng said:

Many hesitate to admit blockchain is the infrastructure for the Fourth Industrial Revolution, hence the frequent talk of “consortium chains” or “blockchain without tokens.” But a decade of practice shows most such attempts fail. We must courageously acknowledge that blockchain, as a tool for restructuring production relationships, finds its core entry point in finance. Without financial demand, we wouldn’t need blockchain. This means that as humanity enters the Fourth Industrial Revolution—innovating in digital, intelligent production relationships—a new financial revolution is indispensable. Otherwise, none of this will happen—or succeed.

Clearly, the new financial model based on blockchain is already in place. Above it, the token economy engine has begun to roar.

Though tokens can be classified in many ways—from Dr. Xiao Feng’s original three-token model, to today’s five types, to a16z’s recent seven-type framework—while it’s true that “Online is New Onchain” and all assets will eventually be tokenized, I believe utility tokens—those tied to project network access—are the key drivers of the crypto market. If other token types represent upgrades, utility tokens represent true innovation.

In 2023, Dr. Xiao Feng delivered a closing keynote titled *The Three-Token Model for Web3 Applications* at the Hong Kong Web3 Festival. I wrote an article in July 2023, *Value Capture and Regulatory Compliance: Exploring the Application of the Three-Token Model in China*, discussing utility tokens—a framework that remains highly relevant today.

Dr. Xiao Feng’s Closing Keynote at Hong Kong Web3 Festival 2023

Web3, built on blockchain networks, represents an economic model based on value networks—what some call stakeholder capitalism—emphasizing data verifiability, data sovereignty, and interconnected value. Under the premise that all value can be tokenized, value includes not just ownership, but crucially, usage rights.

Usage rights are non-exclusive, inherently shareable, multi-licensable, and can even be open-sourced or CC0-licensed for infinite reuse—enabling broad participation and shared value for ordinary users. At the heart of this usage-rights regime is stakeholder capitalism. Traditional organizational forms no longer fit. Decentralized Autonomous Organizations (DAOs), built on open-source or nonprofit foundations, naturally align with stakeholder capitalism and have become the dominant organizational form in the Web3 economy.

Under this system, all participants in decentralized organizations collaborate at scale as stakeholders, contributing and sharing value. In this context, shareholder ownership represented by centralized projects becomes meaningless. What truly matters is project usage rights.

Usage rights cannot be securitized—but they can be tokenized. Combined with blockchain’s distributed ledger technology, usage rights can be standardized and fractionalized into tokens, directly linking value to every participant in the network. These are known as utility tokens.

In this new Web3 economic model, tokens are essentially carriers of value. Only by deeply understanding the intrinsic value of tokens can we design optimal economic models for Web3 applications, create multi-layered growth flywheels, and properly incentivize all participants.

Web3 New Economy and Tokenization

Web3 New Economy and Tokenization

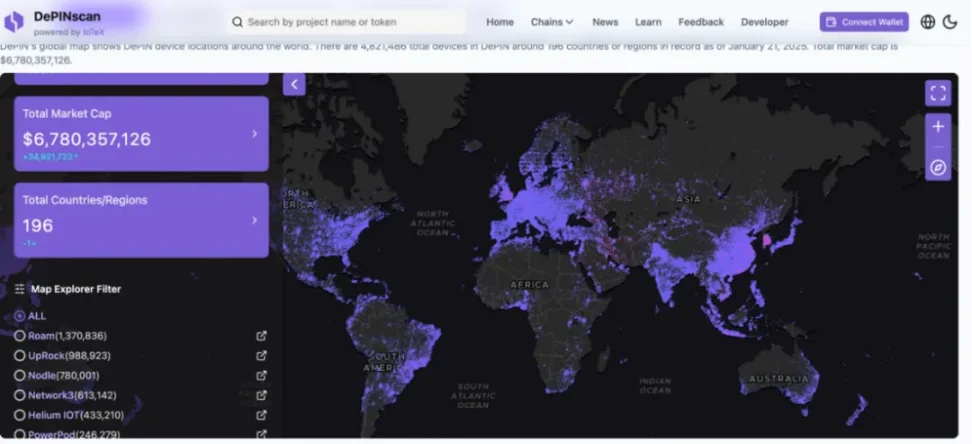

Let’s examine a vivid case of a token economy engine—Roam, a Web3 decentralized telecom operator. This project genuinely solves persistent pain points in Web2 scenarios through Web3 methods, exemplifying the real-world application of Web3.

Roam aims to build a global open wireless network, ensuring seamless, secure connectivity for humans and smart devices, whether stationary or mobile. Unlike traditional telecom operators constrained by geography and homogenized services, Roam leverages blockchain’s inherent global advantage. By building a decentralized communication network using the OpenRoaming™ Wi-Fi framework and integrating eSIM services, it has created a global, free wireless network.

In just over two years, Roam now operates 1,729,536 nodes across 190 countries, serves 2,349,778 app users, and conducts 500,000 daily network verification activities—making it the world’s largest decentralized wireless network. Additionally, users who build and verify Wi-Fi nodes receive free eSIM data, allowing Roam to operate like an internet-native telecom provider.

depinscan.io/projects/roam

Globally, traditional Wi-Fi still carries over 70% of data traffic, yet outdated infrastructure and privacy concerns limit its potential. To address these challenges, Roam collaborates with the Wi-Fi Alliance and Wireless Broadband Alliance (WBA), combining traditional OpenRoaming™ technology with Web3’s DID+VC (Decentralized Identity + Verifiable Credentials) to build a decentralized communication network. This reduces the high upfront costs of global network deployment and enables seamless login and end-to-end encryption comparable to cellular networks.

Roam encourages users to participate in network building via the Roam App—sharing Wi-Fi nodes or upgrading to more secure and convenient OpenRoaming™ Wi-Fi. Users enjoy seamless connectivity across four million OpenRoaming™ hotspots worldwide, and can even find Roam-built nodes in remote areas like Siberia and northern Canada, significantly expanding coverage and enhancing user experience.

Through free global Wi-Fi+eSIM access and diverse network incentives, Roam accelerates the growth of decentralized networks. The ideal of a Network State must be built upon communication infrastructure. Projects like Roam—as Web3 decentralized telecom operators—could become the digital bedrock of such ideals.

When aligned with the narrative of the Fourth Industrial Revolution, projects like Roam clearly serve as communication infrastructure for AI-driven silicon civilizations and enable value transmission at internet-like speeds. This Web3 economic model, built from the ground up in just two years, represents a true disruption of traditional Web2 economics—powered critically by the token economy engine.

V. Final Thoughts

Professor Yang Peifang said: “Looking back at human history, the Chinese nation once dominated the agrarian civilization era with sericulture, silk, and holistic philosophy; the West then ruled the industrial civilization era with machinery, electricity, and reductionist philosophy.”

In this Fourth Industrial Revolution, despite geopolitical forces driving waves of deglobalization, we are still being pulled together by blockchain’s unified ledger. You’ll realize—the world really is flat. As one book put it: “We wanted transoceanic flights, but we invented Zoom.”

In this parallel global market, we can ignite global momentum through the token economy engine, achieve instant global value transfer via blockchain settlement networks, and realize global financial inclusion and equality through new financial infrastructure. There’s much more we can do—and much more to be done.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News