2024 & 2025: Bitcoin's Final Mega Cycle

TechFlow Selected TechFlow Selected

2024 & 2025: Bitcoin's Final Mega Cycle

BTC's Value and Price Theory.

Author: Ling Ziang (Tony Ling), pen name Longye

Executive Summary:

-

As of Q4 2024, we are at the beginning of a new bull market cycle in the crypto industry.

-

BTC’s value can be understood across three levels: macro, meso, and micro. At the macro level, BTC is analogous to bonds and stocks in financial history—a “fuel” for humanity's next wave of technological advancement. At the meso level, it represents both the currency and index of the digital world that humans will inevitably enter. At the micro level, with increasing regulatory clarity and compliant token issuance, BTC will attract global grassroots investment demand.

-

This may be the last "wild west" cycle for the crypto industry—the final mega-cycle where BTC sees massive beta gains. After this cycle, BTC’s beta will significantly decline. However, this does not mean there won’t still be alpha opportunities offering 100x returns in the broader token ecosystem.

-

The peak of BTC’s current bull run is expected in Q4 2025, reaching $160,000–$220,000. Prior to that, beyond the already completed “first wave,” two more significant mid-bull market surges remain.

-

Right now is like 1999 during the internet era—within the next 12–18 months, after the bull market peaks, the crypto industry will face a prolonged winter similar to the dot-com crash of 2000–2001. Of course, this also presents an opportunity for industry reshuffling. And I welcome it.

When I sense a bull market approaching, my writing output reaches its highest.

About four years ago, at the start of the previous bull cycle, I wrote “How Should We Invest in Digital Currencies in 2021?”. When discussing the entire cryptocurrency industry, we inevitably must first address BTC’s value and price.

If you already believe in Bitcoin’s value, feel free to skip directly to Part V, which discusses expectations for Bitcoin’s future price trajectory.

I

From an industrial perspective, I’d like to further elaborate on BTC’s value by dividing it into macro, meso, and micro dimensions. Macroscopically, BTC embodies the global financial market’s避险 expectation and represents the third major capitalizable “financial medium” in human history after bonds and stocks. At the meso level, BTC is the best “index” reflecting the economic output of the Web3 world—an inevitable destination for humanity’s digital future. At the micro level, as regulations around BTC mature, it will attract substantial “traditional old money” from mainstream countries such as the United States, while in developing nations, it will absorb pent-up grassroots investment demand unmet by local financial systems.

At the macro level, viewing Bitcoin as a landmark asset in financial history requires understanding the evolution of finance itself. In “How Should We Invest in Digital Currencies in 2021? – Part One”, I positioned digital currencies within the context of technological history. Behind every technological revolution lies the emergence of critical financial infrastructure and new financial “media.”

Finance reflects changing times. Today may mark the most uncertain period in global political and economic affairs over the past three decades—a moment when traditional financial order appears fragile and ripe for upheaval. I cannot recall whether formal trading venues akin to the London Stock Exchange or NYSE existed during famous historical bubbles like the Dutch Tulip Mania—or if Dutch traders simply conducted informal transactions without rules, causing the bubble to eventually burst. Yet throughout history, every major technological innovation remembered by humanity has been accompanied by shifts in financial paradigms, which themselves arise inevitably from broader socio-political transformations. These forces interact symbiotically, ultimately leaving indelible marks on human civilization. Likewise, I wonder—if the American Civil War hadn’t radically reshaped U.S. social structures and encouraged technological innovation in industry, would the Second Industrial Revolution have truly flourished in America rather than remaining centered in Britain?

At the same time, I hold a more radical view: while everyone talks about economic stagnation and searches for viable business models—why must commerce even require a “business model”? Has the term itself become meaningless?

I’ve explored these thoughts in greater depth elsewhere—they’re complex and beyond the scope here—but they’ll form a core part of my upcoming article titled *Crypto Capitalism Series: Philosophical Notes on Business and Investment (Special Edition)*. (See related reading: “Crypto Capitalism Series Part One: Token Issuance, A New Financing Paradigm”)

[Excerpt: Discussing business models in today’s commercial and financial environment refers implicitly to the dominant corporate model developed over the past century—scaling up markets, expanding headcount, and eventually going public, with valuations based on profit × PE multiples. This path may no longer hold in the future.

Today, equity-based enterprises likely account for 95% of the total value held by contemporary “social capital” (or what we call “private economy”), with publicly listed companies anchoring most of that value via stock prices. But moving forward, this value may increasingly reside in alternative forms—such as “businesses” under limited partnerships or “tokens” issued by foundations.]

II

Let me spend more time elaborating on the meso-level argument for BTC. In the concluding section of my 2021 book, among eight predictions, the very first was that BTC is unbeatable. See the postscript of my e-book *Unlocking the New Code: From Blockchain to Digital Currency*:

From a technology industry standpoint, Web3 is an inevitable trend, and Bitcoin is the core asset of the entire Web3 world—or in economic terms, the “currency.” In ancient barter economies, gold served as the primary medium of exchange; in modern nation-states and financial systems, national currencies dominate. Looking ahead, with the dawn of the digital age and virtual spaces like the metaverse, a new form of “currency” will be needed for all aspects of life in digital worlds.

Thus, fixating on questions like “why are you investing in just a token?” is pointless. Just as someone might say, “I’m investing in equity firms” or “I’m investing in internet companies,” blockchain and crypto represent a new market mechanism and financial medium increasingly integrating with other industries: Blockchain + AI = DeAI, Blockchain + Finance = DeFi, Blockchain + Entertainment/Art = NFT + Metaverse, Blockchain + Science = DeSci, Blockchain + Physical Infrastructure = DePIN…

The trend is clear—but what does it mean for us? How do we gain wealth appreciation once we see the direction?

Let’s turn our attention to AI.

In recent years, the business world has had two main currents—one visible, one hidden. AI is clearly the hot topic, openly celebrated and pursued by capital. Crypto, meanwhile, flows beneath the surface—filled with legends and stories of overnight riches, yet constrained by regulations, making it inaccessible to many.

The potential of the AI market is widely seen as being in the trillions, especially in generative AI, AI chips, and supporting infrastructure. Investors believe in AI as a sunrise industry and are eager to allocate funds—but into what exactly? Can we invest in an AI ETF that comprehensively tracks the ecosystem’s growth?

No. In 2024, Nvidia’s stock rose nearly threefold, while most AI-themed ETFs performed modestly. Going forward, Nvidia’s performance won’t necessarily correlate with overall AI sector growth—chip dominance will never belong to just one company forever.

Comparison of Major AI ETFs vs. Nvidia Stock Performance in 2024

AI is the main theme, but is there any product that can track the total market cap growth of the AI industry—so that as the AI economy expands, the value of the product rises proportionally? Like how the Dow Jones or S&P 500 ETFs represent Web0 (equity enterprises), or how Nasdaq ETFs capture Web1/Web2 investment opportunities—Web3, or the entire digital economy of the future, needs its own index. And the most suitable candidate is BTC.

Why must BTC be the benchmark for Web3’s value?

Because from the moment computers and the internet emerged, humanity was destined to spend increasing amounts of time in virtual worlds rather than physical ones. In the future, putting on VR/AR glasses, you could tour Yellowstone from home, walk through Tang Dynasty palaces in China, or meet friends face-to-face in a virtual conference room on the opposite side of the globe… The boundary between reality and virtuality will blur—that’s the future of the digital world, the metaverse. And when you want to decorate your virtual space or have a digital avatar dance for you, you’ll need to pay. It won’t be dollars or yuan, nor physical assets. The only currency I can envision as universally accepted across the entire digital world is Bitcoin.

Recall the film *The 1911 Revolution*, where Dr. Sun Yat-sen holds up a 10-yuan bond: “After the revolution succeeds, this bond will redeem 100 yuan.”

III

Back to the present.

We live in economically stable countries where fiat currency is trustworthy. But this stability doesn’t extend globally. Argentina’s newly elected president’s first act was abolishing the national fiat system—after all, few citizens trusted government-issued money anyway. Turkey saw inflation exceed +127% in 2023, and correspondingly, 52% of its population owns cryptocurrencies. In developing nations, as information technology infrastructure improves, traditional mobile fiat payments and cryptocurrency adoption have advanced almost simultaneously. Compared to China’s leap from pre-digital POS systems straight to mobile payments around 2010, many developing countries today are skipping mobile payment (2.0) altogether and adopting cryptocurrency (3.0) directly—making crypto payments commonplace in daily life.

An interesting debate arises: Bitcoin has no central controller, so how can it fulfill the macroeconomic regulation functions of fiat currencies? In truth, even the U.S. dollar is effectively issued by corporations, and so-called government control often serves powerful interest groups. Capital, not governments, drives the world. If fiat claims macro-control, then Bitcoin mining cartels are its true regulators.

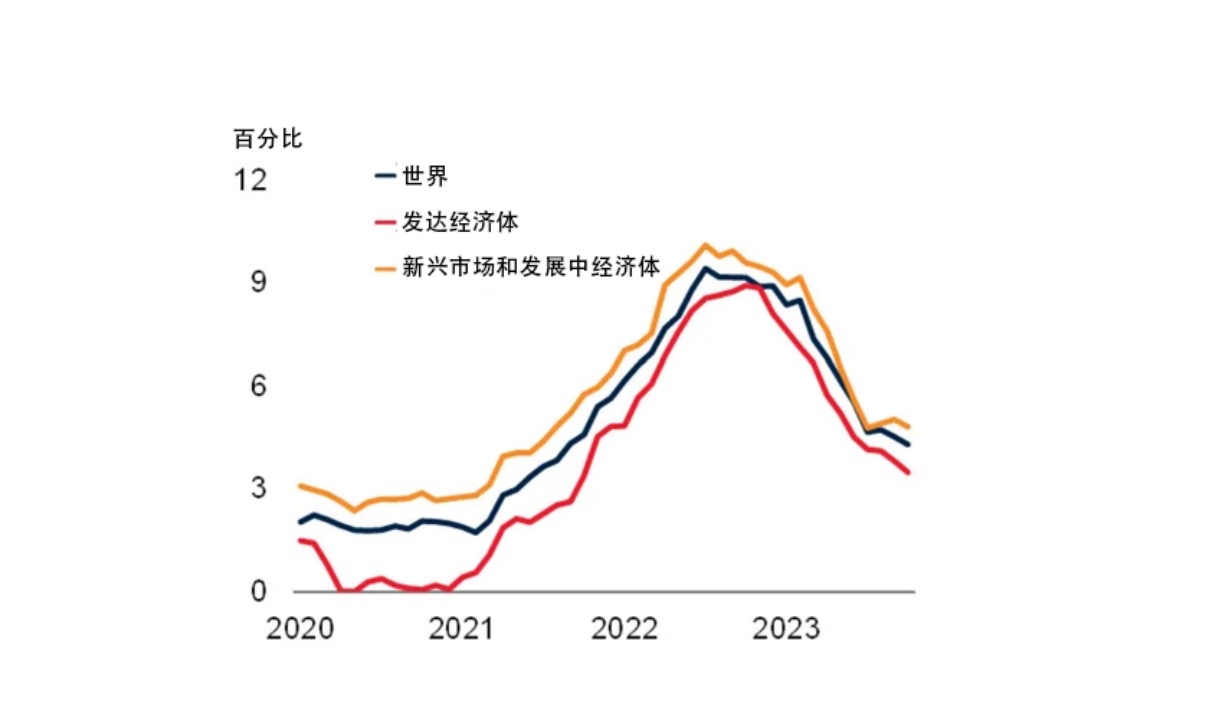

Inflation Trends Across Major Economies in Recent Years

Argentina's Inflation Rate Changes in Recent Years

From a micro perspective, as capital velocity increases, tech and financial cycles shorten. In fragile economic environments, traditional equity markets require 8–10 year lockups—long horizons that raise liquidity concerns. Token ownership offers early exit options, attracting retail capital and giving early investors more flexible liquidity expectations.

In traditional equity markets, angel or early-stage investors typically seek partial exits around five years post-founding—when companies are mature enough but still far from IPO or acquisition (usually 8–10 years out)—via share transfers or buybacks. While this reduces time costs, it remains far less liquid compared to tokens.

The appeal of token-based models lies in enabling earlier capital recycling through token issuance and circulation, drawing broader participation. This flexibility could profoundly reshape traditional equity markets. For deeper analysis, see “Crypto Capitalism Series Part Two (Down): VC or Token Fund? The Battlefield Without Smoke”.

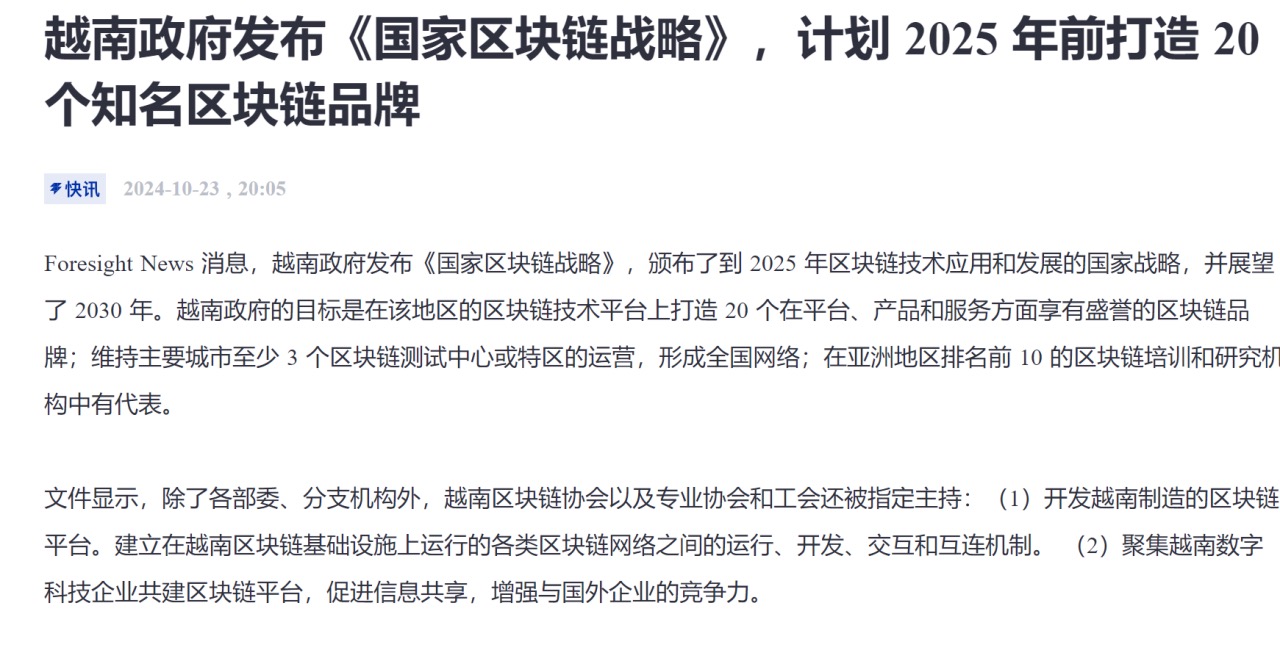

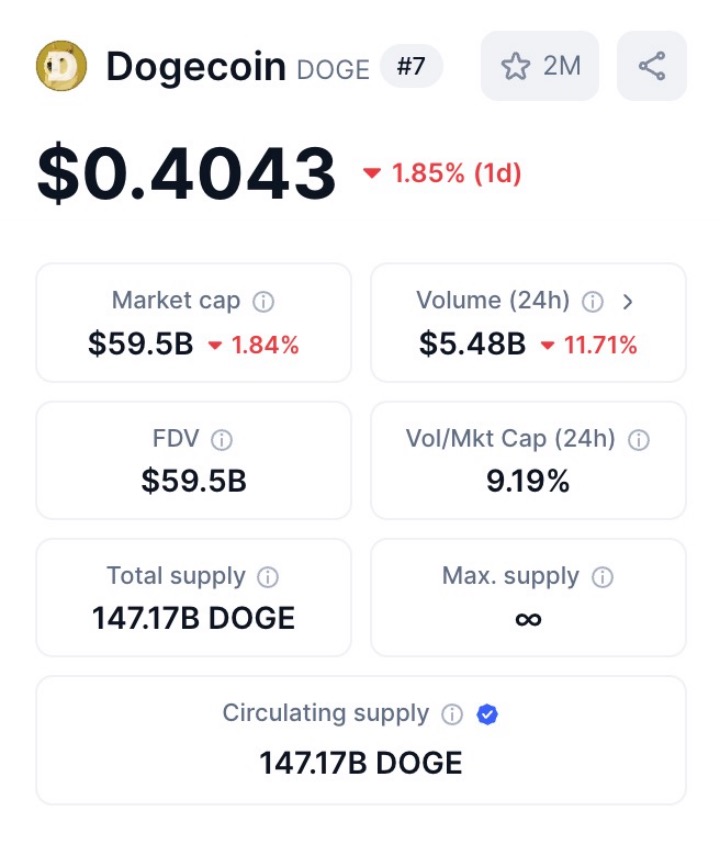

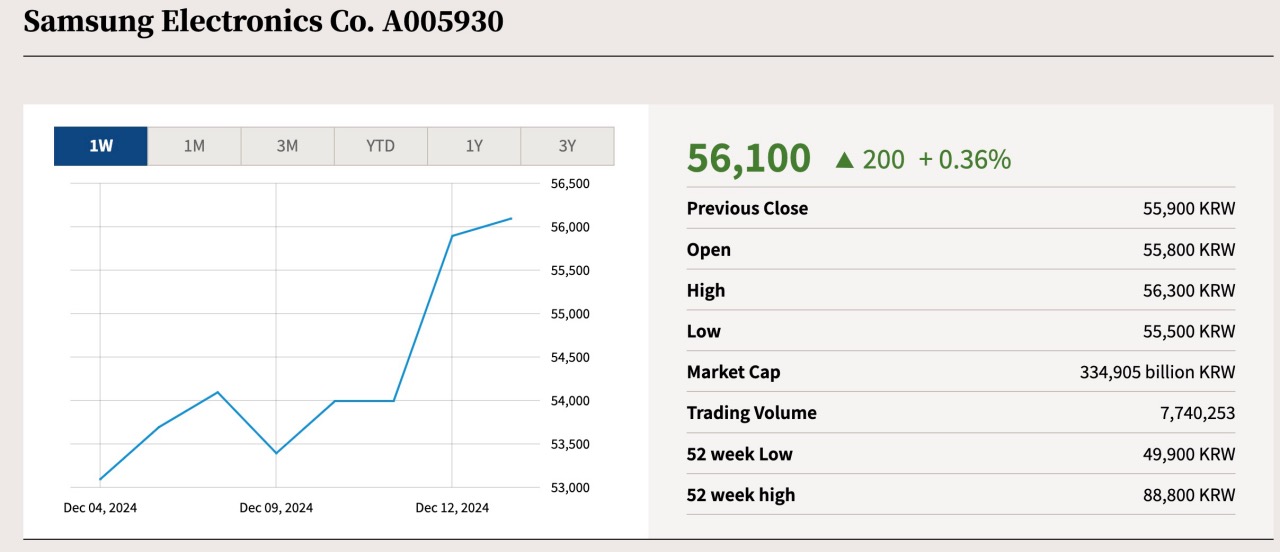

Additionally, most sovereign financial markets worldwide are fragmented and illiquid. Crypto’s inherent global nature strongly attracts capital from places like South Korea, Argentina, and Russia. In Southeast Asian countries like Vietnam, stock market development lags behind middle-class wealth accumulation, prompting this emerging class to bypass domestic financial systems entirely and transition straight into crypto. As global crypto regulation advances and integrates with mainstream finance, grassroots investment demand in these nations cannot be met by weak local financial infrastructure—South Korea’s KOSPI and KOSDAQ exchanges list over 2,500 firms, yet 80% have market caps below $1 billion, with negligible daily trading volume. By contrast, the global crypto market, fueled by retail capital, offers abundant liquidity, becoming their preferred investment vehicle.

Current Market Cap and Trading Volume of Doge

Current Market Cap and Trading Volume of Samsung

Note: As shown, Doge’s current market cap is ~$60B, while Samsung’s is ~$234B—about four times larger. Yet Doge’s 24-hour trading volume (~$5.5B) exceeds Samsung’s by tens of thousands of times.

In the strategic epicenter of global crypto—America—2025 may bring transformative legal changes, notably the FIT21 and DAMS bills, which could shape the future of the industry. These blockchain bills, regulated by the Commodity Futures Trading Commission (CFTC) instead of the Securities and Exchange Commission (SEC), classify token issuance as commodity trading rather than securities, placing them under CFTC jurisdiction. Given that these bills are Republican-led, and current SEC Chair Gary Gensler represents Democratic views, passage faces strong resistance. However, should Donald Trump win re-election, with Republicans in control, the likelihood of approval rises sharply.

In simple terms, treating token issuance as a commodity under CFTC oversight legalizes it, greatly boosting fundraising incentives. Companies can raise capital legally and transparently, attracting more institutional capital into crypto. With sustainable, compliant channels established, more people will stay committed long-term—even after profiting. Most importantly, once the U.S. leads in this legislation, international competition in digital finance and blockchain technology will intensify, sparking fierce battles for projects and talent. In a fully globalized, freely flowing crypto space, founders currently based in relatively friendly jurisdictions like Singapore or Switzerland may soon migrate en masse—if U.S. policy becomes more welcoming, turning token issuance from a gray-area activity into a respected financial innovation.

IV

Recall 2016, when the number of cryptos could be counted on one hand, and BTC felt like a game token—something you could top up directly with RMB in exchanges. That was the dream of our generation of native crypto believers. (For details, see end of “How Should We Invest in Digital Currencies in 2021? – Part One”)

That was my dream too.

I originally thought achieving these goals would take 8–10 years.

But we did it in just four.

And then I formed a new dream—since Bitcoin as a monetary asset is gradually accepted by mainstream society, other digital currencies, or tokens, beyond just digital equity, should also serve as digital commodities. Only by creating utility in humanity’s future digital world—not just financial value—can we truly accelerate the transition into the digital era.

Oh right, later people gave it a new name—NFT.

“Digital goods of the metaverse era”—that’s my definition of NFT’s ultimate destiny, and the most crucial step toward mass adoption of Web3-native, digitized versions of “internet-era goods.”

Hence, I decisively built in the NFT space starting early 2021. My vision for its future is detailed in the series “The Road to the Future—Web3 Five-Part Series”.

V

Naturally, the most compelling draw—and what gets more people to read my articles—is BTC’s price surge.

Now comes the key point. Here’s my forecast for BTC: the peak of this cycle will arrive by the end of 2025, with a reasonable range of $160,000–$220,000. After that, in 2026, I recommend going flat—take profits, rest, and recharge.

In my research paper published January 1, 2019, “Bitcoin Valuation Model Under Miner Market Equilibrium: Based on Derivatives Pricing Theory”, I identified the bottom of the 2018–2021 four-year cycle,

And in 2022, I discussed the bottom of the 2022–2025 four-year cycle.

From today’s vantage point, the crypto industry stands at a critical crossroads. The current state of digital currencies mirrors the internet industry at the turn of the millennium. Within the next 1–2 years, a bubble burst is imminent. As crypto-friendly laws like FIT21 pass in the U.S., and regulatory frameworks for token assets solidify, vast sums of capital—from traditional investors who previously knew nothing about crypto, or even dismissed it outright—will begin allocating 1%–10% to BTC. But afterward, unless blockchain and digital currencies integrate meaningfully with real-world industries, driving genuine “blockchain+industry” transformation—just as the internet transformed consumption, social interaction, and media—I struggle to see what new capital inflows could justify another explosive growth phase. DeFi in 2020, NFTs and metaverse in 2021—those were correct directions, sparking waves of innovation. But in 2024, despite BTC repeatedly hitting new highs, the broader blockchain industry has seen little meaningful innovation—only more memes and Layer 1/2/3 projects, lacking novel “business concept breakthroughs.” Looking ahead to 2025, given the prevailing industry sentiment, I am pessimistic about any landmark-level conceptual innovations emerging.

When the tide rises, even small rafts float high. A hundred boats race, their rowers boasting who paddles faster, mocking heavy iron ships powered by engines. But when the tide recedes, wooden rafts run aground—only those with sustained engine power can sail beyond the harbor into the open sea.

Here’s an intriguing prediction: the peak of the crypto bubble will be marked by Warren Buffett—the world’s most prominent Bitcoin skeptic—changing his stance and joining the industry. A revolutionary victory often carries within it the seeds of its greatest crisis.

Think of today’s crypto scene as 1999 in the internet era. After a rapid ascent, the digital currency industry may face severe correction starting late 2025 due to excessive speculation. Historically, the internet boom began with Netscape’s IPO in December 1995, followed by Yahoo!’s listing in April 1996, igniting market frenzy. On March 10, 2000, the Nasdaq hit a record high of 5,408.6 points. Then the bubble burst swiftly, plunging the market into winter by 2001. Though the broader downturn lasted until 2004, the true low came in October 2002, when the Nasdaq nearly broke 1,000—marking the financial nadir.

In 2020, MicroStrategy boosted its stock value significantly by purchasing BTC, marking the first notable stock-crypto联动 effect. Then in February 2021, Tesla announced its Bitcoin purchase—symbolizing the entry of corporate giants. These moments resemble the internet’s “1995–1996” awakening.

Looking ahead, I believe BTC may reach a long-term cyclical peak by late 2025, but could hit a new low by early 2027. Yet if FIT21 passes, it might unleash a nationwide token issuance wave—akin to the golden age of “.com” mania.

If token fundraising barriers drop nearly to zero—so that anyone can issue a token as easily as a high school student builds a website—then limited capital will be rapidly diluted across countless new tokens. In such a scenario, the final “rampage bull market” for token issuers may last no more than three months. Thereafter, due to supply-demand imbalance and capital exhaustion, a full-scale industry collapse becomes inevitable.

But until then, in the coming 12 months, we still have nearly 2x beta upside in BTC, plus countless short-term opportunities for early-stage tokens to deliver “100x–1000x” returns for ordinary investors amid concentrated global liquidity—why wouldn’t you participate?

Reflecting back on the turbulent, much-maligned “bubble” days of the internet industry—today, the Nasdaq has surpassed 20,000 points. In hindsight, the 2000 peak now looks like a mere hill. Even those who entered the internet space in 2000 and persisted to today made arguably the best investment decision possible.

So too with BTC—one peak after another, each higher than the last.

It has been 3,202 days since I bought my first BTC on March 7, 2016.

I still remember the price displayed when I clicked: 2,807 RMB—less than $400.

Many have asked me: how high can BTC go?

That question lacks meaning. Gold prices keep setting new records too, year after year.

The meaningful question is: how high can BTC go before a certain point in time?

Stay tuned.

The best is yet to come.

December 12, 2024

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News