Review of Recent Developments in 10 Key DeFi Projects and the Latest Market Trends

TechFlow Selected TechFlow Selected

Review of Recent Developments in 10 Key DeFi Projects and the Latest Market Trends

Although Base and Solana are leading in the AI agent space, NEAR is quietly carving out its own path in AI innovation.

Author: Ignas | DeFi Research

Translation: TechFlow

"Please forgive me, my enthusiasm for meme coins has reached its peak."

I’ve found myself obsessed with meme coins, to the point where it’s affecting my attention toward other developments in crypto. The recent market downturn gave me time to catch up on these innovations—but the dip didn’t last long.

In this article, I want to share 10 developments in DeFi and the broader cryptocurrency ecosystem that have caught my attention—and I believe you should be watching them closely too.

Avalanche 9000: Is L1 the new L2?

Avalanche has just launched Avalanche9000, its biggest upgrade ever, making it easier, cheaper, and more flexible to create L1 blockchains.

The old subnet model is gone. Now, instead of requiring developers to validate the mainnet or pre-stake 2,000 AVAX, they pay a small recurring fee—drastically lowering costs.

This sounds a bit like Polkadot and Cosmos.

Inspired by Ethereum’s EIP-4844 (which slashes gas fees on L2s via Proto-Danksharding), Avalanche brings L1 costs down to levels comparable with Celestia-based rollups—but with better interoperability and reliability.

The upgrade also introduces L1-only validators, allowing each L1 to manage its own rules—whether PoS or Proof-of-Authority chains—leading to improved tokenomics and value accrual.

The cost of running a validator has dropped from 2K AVAX (~$100,000) to just 1.33 AVAX per month.

Avalanche has launched a $40 million grant program, Retro9000, and already has 700 L1s in development, spanning gaming to DeFi. By focusing on tokenization, Avalanche has attracted traditional finance partners and projects like Off The Grid, carving out its niche amid competition from Solana and Ethereum.

NEAR AI

While Base and Solana lead in AI agents, NEAR is quietly building its own path in AI innovation.

NEAR supports agent-based on-chain functionality and is developing more tools and features.

Its standout feature is native chain abstraction for multi-chain AI agents, enabling developers to build interconnected systems more easily.

Additionally, NEAR Intents introduces a new transaction model enabling cross-chain settlement between AI agents, services, and end users. A highlight is the collaboration between Infinex and NEAR, letting users trade BTC, XRP, and others on a single decentralized platform.

NEAR has also launched NEAR.ai, an AI assistant that can act on behalf of users by connecting to other AI agents and bridging web2 and web3 services. While NEAR’s wallet experience used to be poor, it's significantly improved (I recommend Near Mobile). This is similar to what Cortex Protocol is building—worth checking out.

Interestingly, social agents built on NEAR are now hosting X Spaces together.

Moreover, NEAR has launched a research center to explore new AI models and partnered with Delphi on an AI accelerator to support developers in the space.

Notably, the zero-knowledge computing blockchain Nillion Network is being built on NEAR, bringing privacy-preserving tech for training private LLMs and inferring sensitive data—potentially unlocking user-owned AI at full scale.

Liquity v2 Launch

LQTY surged 120% within a month.

Two reasons: overall bullish market sentiment and the launch of V2. You can try the testnet here.

Traditional DeFi lending models have issues:

-

Money markets like Compound and Aave set interest rates based on utilization, leading to unpredictable borrowing costs;

-

Governance-driven protocols like MakerDAO adjust slowly, often leaving rates stagnant due to governance delays.

Even Liquity V1’s fixed-rate model couldn't adapt to changing market conditions.

Liquity V2 solves this with user-set interest rates and BOLD—a stablecoin focused on decentralization, user control, and yield.

Borrowers open “Trove” positions to set their own rate—opting for lower rates to save costs or higher ones to avoid liquidation. Treasuries with the lowest rates are prioritized for redemption.

With loan-to-value ratios (LTV) up to 90% and leverage up to 11x, Liquity V2 achieves remarkable capital efficiency.

Borrowers can use not only ETH but also liquid staking tokens (LSTs) like wstETH and rETH as collateral, earning staking rewards while borrowing BOLD.

Thus, BOLD is fully backed by ETH and LSTs, redeemable at any time, and avoids traditional financial risks.

Unlike USDC, BOLD doesn’t rely on real-world assets (RWAs), eliminating counterparty and censorship risks. It maintains its $1 peg through a simple mechanism:

-

When $BOLD trades below $1, arbitrageurs buy and redeem it for ETH, pushing the price back up.

-

When $BOLD exceeds $1, lower borrowing rates attract more supply, stabilizing the price.

Users depositing into the Stability Pool earn 75% of protocol revenue (in BOLD and ETH), while the remaining 25% funds Protocol Incentives for Liquidity (PIL) to boost BOLD’s liquidity across DeFi.

A key change in Liquity V2 is its Forkonomics model.

One of DeFi’s most frequently forked protocols, Liquity now requires teams to obtain permission to use its code and must airdrop tokens to LQTY holders. In return, teams gain Liquity’s support, shared security resources, and potential LQTY rewards.

This model helps forked projects get better support while mitigating security risks as BOLD expands across chains.

Liquity V2 is currently live on the Base Sepolia testnet.

Pendle’s New Protocol – Boros

Most assumed Pendle V3 would be just another fork or minor update. Turns out, Pendle had something entirely different in mind.

Pendle recently launched a brand-new protocol called Boros, focused on leveraged yield trading. Simply put, Boros lets users trade yield with leverage.

The core of Boros is funding rates—the cost of borrowing in leveraged perpetual contracts. Historically, funding rates were hard to hedge or trade effectively; Boros aims to solve that.

With Boros, users can:

-

Hedge against funding rate volatility for more stable returns.

-

Speculate on funding rate movements using leverage for potentially higher gains.

For example, protocols like Ethena that profit from funding rates can lock in stable yields via Boros, while speculators can profit from fluctuations.

Why do funding rates matter?

Perpetual exchanges handle $150–200 billion in daily volume, and funding rates are central to these markets. Yet, this area has been largely overlooked in DeFi.

Boros turns funding rates into tradable assets, offering new tools for protocols, market makers, and traders.

Pendle now covers the full spectrum of yield trading through V2 and Boros:

-

V2 focuses on tokenizing on-chain yield—staking, RWAs, BTCfi.

-

Boros targets funding rates and off-chain opportunities.

Notably, Pendle did not launch a new token—continuing to use $PENDLE and vePENDLE.

Both tokens support both V2 and Boros, with unchanged revenue distribution: 80% to vePENDLE holders, 10% to the protocol treasury, 10% to operations.

Boros arrived right on time as the points narrative cools down.

Zircuit

Possibly the most confusing Layer 2 in crypto.

Zircuit recently completed its Season 1 and 2 airdrops on November 20, distributing 300 million tokens for users to claim. They generously airdropped to nearly every partner protocol.

What’s next for Zircuit? How will they keep users engaged and create real utility for their token?

The answer seems to be the hottest topic right now: artificial intelligence.

Zircuit is developing a new product called Gud AI.

It’s an AI agent similar to AIXBT, capable of identifying investment opportunities. Follow it on X. There’s also a native AI token, $GUD, fairly launched and requiring $ZRC staking.

Not a bad strategy for a new Layer 2.

Zircuit is a Layer 2, but takes a different approach from other L2 infrastructures. It emphasizes not just scalability, but also security, efficiency, and usability.

One of Zircuit’s standout features is Sequencer-Level Security (SLS). Most blockchains detect malicious transactions after execution; SLS identifies threats before they even reach the chain.

In the era of Ethereum restaking, Zircuit’s LRTs are worth watching, having attracted over $2 billion in TVL. Zircuit gained momentum in Phase 2 of its mainnet launch, which is now live and includes:

-

Fast bridge from Ethereum—transactions settle in minutes. Since launch, net deposits into Zircuit have surged to $300 million.

-

Native DeFi dApps such as ZeroLend and Elara Labs for lending, Ocelex and Dodo for swaps and liquidity mining.

Recently, Zircuit distributed 2% of its supply to over 190,000 EigenLayer restakers.

Zircuit is backed by Binance Labs, Pantera Capital, and Dragonfly Capital.

But still not listed on Binance :) I think it’s inevitable.

Starknet

Despite heavy FUD around the STRK airdrop, Starknet has undeniably made major progress recently.

They’re pushing the boundaries of Layer 2s and deserve close attention.

A key move was launching native token STRK staking—the first L2 to offer native staking, now live on mainnet.

Bitwise, managing $11 billion in crypto assets with over $3.5 billion in staked ETH, has joined the Starknet ecosystem by supporting STRK staking.

On the technical side, deployment costs are now just $5, with verification under $1. Thanks to various teams, SNARK proofs can now even be verified on-chain—opening doors for developers to build real-world ZK-powered apps like private identity verification or secure document signing.

Deployment costs are now just $5, with verification under $1. This opens opportunities for developers to build real-world ZK-powered applications, such as private identity verification or secure document validation.

They also rolled out v0.13.3, reducing blob gas costs by 5x through smarter compression and block optimization. As Ethereum’s blob usage grows, this keeps fees low. Looking ahead, Starknet plans further efficiency upgrades. Even Vitalik offered praise.

Another exciting step is their progress on a trust-minimized Bitcoin bridge (a PoC bridge enabled by OP_CAT), developed with sCrypt. This shows connectivity between Starknet and Bitcoin is possible—a major leap in interoperability that could unlock novel use cases.

Mode AI

Post-airdrop, Mode is advancing with two big moves: veMODE and the AIFi ecosystem.

Mode is the first OP-stack L2 to introduce the vote-escrow (ve) governance model via veMODE. Users stake MODE or MODE/ETH LP tokens to gain voting power—the longer they lock, the higher the voting weight (up to 6x).

Unlike pool-specific voting, veMODE focuses on protocol-level decisions to foster ecosystem-wide growth.

In Season 3, Mode will distribute $2 million in OP incentives through this system. Future plans include a bribery marketplace and even AI agents to simplify participation—letting AI vote on behalf of users.

Mode stands out with its focus on AIFi.

Backed by a $6 million grant from Optimism, Mode is bringing AI agents into DeFi to streamline and scale on-chain interactions. These agents can handle tasks like yield farming, risk management, and governance—requiring minimal human input.

Mode’s AIFi ecosystem consists of three layers:

-

AI-Secured L2 Sequencer: Detects and blocks malicious transactions before they enter the blockchain.

-

On-Chain Agent Infrastructure: Partners like Giza, Olas, and RPS AI deploy agents, while Mode’s Dapp Intents SDK enables agents to learn and execute advanced strategies.

-

AI-Powered Interfaces: Tools like Mode’s AI wallet simplify interactions, making DeFi more accessible.

To kickstart the AIFi ecosystem, Mode launched an AI Agent Store—an AI agent discovery platform designed for DeFi. Notable agents include:

Giza’s ARMA: Optimizes USDC yields across money markets.

Olas’ MODIUS (coming soon): An AI-driven yield farming strategist.

Brian: Makes DeFi interactive through natural language prompts.

Sturdy V2: An AI-powered yield vault optimizing returns.

So, Near, Mode, and Zircuit are all well-positioned in the emerging AIFi landscape.

Polkadot

DOT rose 75% in a month. What’s behind this surge?

In recent months, activity on the Polkadot network has hit new highs. Monthly transaction counts hit record levels, while key metrics like fees, active users, and transaction volume are rising—fees alone grew 300% year-on-year, with active users and volume climbing steadily.

A key driver is Polkadot 2.0.

Previously, running a parachain cost ~$16,700 per month. With Polkadot 2.0, this drops to $1,000–$4,000. Projects now lease blockspace using DOT, creating steady demand for the token.

Per governance, some revenue may be burned, reducing supply. This creates a positive feedback loop—higher $DOT demand, potential supply reduction, and a stronger ecosystem. (Detailed reference link)

Polkadot is also improving connectivity with other blockchains.

Hyperbridge links Polkadot with Ethereum, BNB Chain, and others, enhancing cross-chain interaction and opening new possibilities for developers. The network itself has proven robust, handling over 3.3 million transactions in a single day—showing readiness for mass adoption in gaming and beyond.

DeFi on Polkadot is growing too.

Hydration has seen a 50% increase in active users since October, with fees doubling to an all-time high.

If you're familiar with ETH or Solana DeFi, you’ll appreciate Hydration—it integrates trading, lending, and stablecoins into a single appchain.

Its Omnipool simplifies liquidity and allows single-sided deposits, with total value locked (TVL) exceeding $68 million. Hydration’s 2-pool (USDT-USDC) offers up to 36% APY plus vDOT rewards.

Hydration recently launched Borrowing—a fork of Aave V3 on Polkadot that prioritizes on-chain liquidations at the start of each block.

This mechanism reduces losses for borrowers and prevents front-running attacks. Liquidation penalties go to protocol revenue, benefiting HDX stakers and governance participants.

dYdX

The competitive landscape for decentralized perpetual DEXs is fierce, with leaders shifting rapidly—dYdX, GMX, Vertex, and now HyperLiquid.

Yet, I believe the real losers are centralized exchanges (CEXs), gradually losing market share to fast-innovating decentralized platforms.

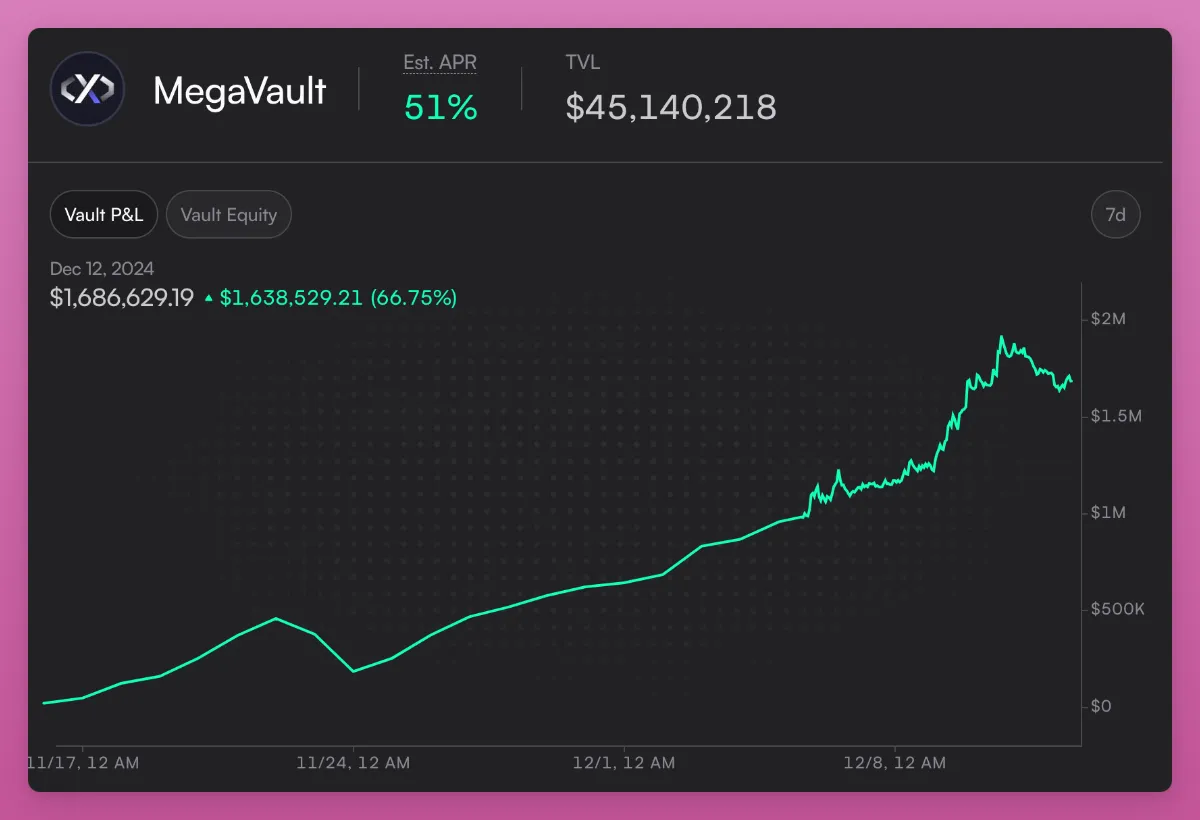

While Hyperliquid gained massive traction post-airdrop, dYdX took a more retail-focused approach, launching dYdX Unlimited and a suite of new features: Instant Market Listing, MegaVault, and an affiliate program.

With Instant Market Listing, users can instantly create and trade new markets without governance approval or long wait times. The process is simple: pick a market, deposit USDC into MegaVault, and start trading.

This is a significant advantage CEXs can't match.

MegaVault is the core of the system, pooling USDC to provide liquidity across all markets.

It funds markets while depositors earn passive income. Half of dYdX’s protocol fees flow into MegaVault, making liquidity provision profitable—similar to Jupiter’s JLP Vault.

dYdX also launched an affiliate program, offering lifetime USDC commissions for referrals. Bybit’s rapid growth was partly fueled by such a program.

Trading rewards include $1.5 million in DYDX tokens monthly, plus a MegaVault depositor prize pool of up to $100,000 in USDC.

As a result, dYdX has achieved solid results: over $40 million in trading volume, with annualized yields reaching 51%.

Aptos

Following Sui, Aptos—a Move-based blockchain—is seeing rapid growth in TVL and DeFi, surpassing $1 billion in TVL for the first time, a 19x YoY increase.

With the rise of TradFi on Aptos, BlackRock expanded its BUILD fund on Aptos—the only non-EVM chain integrated.

Franklin Templeton extended its on-chain U.S. government money market fund to Aptos, one of seven supported blockchains.

Bitwise and Libre launched tokenized funds on the blockchain.

Tether launched native USDt on Aptos in August. Since then, USDT supply on Aptos has steadily grown from ~$20 million to ~$142 million.

Following Tether, Circle announced native USDC and the Cross-Chain Transfer Protocol (CCTP), supported by Stripe’s crypto offering on Aptos.

With native stablecoins flowing into Aptos, key metrics are trending positively—TVL remains above $1 billion, and over 1 million new users have joined the ecosystem.

Notable DeFi milestones on Aptos include:

Daily DEX trading volume on Aptos grew 2,700% (28x) over the past year.

-

Aries Markets, the top lending protocol on Aptos, hit a new TVL high with over $800 million in deposits and $450 million in loans.

-

emojicoin dot fun, a pumpdotfun clone on Aptos, launched mainnet, reporting 16,700 unique addresses within 24 hours.

I suspect APT is following in SUI’s footsteps and performing exceptionally well. I believe SUI, APT, and other L1s are competing with Solana for dominance in the execution layer, while ETH remains the industry benchmark.

If you spot any errors or have feedback, feel free to reach out!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News