Why should you choose to start building on Base now?

TechFlow Selected TechFlow Selected

Why should you choose to start building on Base now?

As long as ETH remains hot, Base should stay heated up as well.

Author: lazyvillager1, crypto KOL

Translation: zhouzhou, BlockBeats

Editor's Note: Since Trump’s election victory, COIN and BTC have surged significantly. However, the author remains bullish on ETH and is optimistic about the development of the Base L2 ecosystem. Base has the potential to stand out in competition by attracting Memes, consumer dApps, and more on-chain activity. ETH remains central to digital assets, while Base, as Coinbase’s on-chain lever, benefits from Coinbase’s resources and support, possessing scarcity and innovation that can attract users over the long term without relying on traditional token incentives. The growing activity and TVL within the Base ecosystem demonstrate its strong potential among ETH-L2s.

Below is the original content (slightly edited for clarity):

Basic Outlook for Future Development

Since Trump’s election win on November 5, COIN and BTC have led the market rally, rising 70% and 16% respectively. I remain personally biased toward ETH, and based on my October writings about meme coins, I believe multiple favorable factors are converging for the Base L2 ecosystem:

1. "Winning" against other L2s—and even the Ethereum mainnet—by becoming the preferred ecosystem for memes, consumer dApps, and attention capture

2. Competing as a top-tier EVM-compatible ecosystem alongside SOL’s “full-stack” integrated casino model

My core thesis is simple: ETH remains the key center of the digital asset ecosystem. To date, all derivative projects have relied on two fundamental principles to drive network effects:

a. The underlying asset must perform strongly relative to its competitors;

b. The underlying asset must possess "scarcity";

Therefore, in this battle for attention, most participants are effectively choosing an asset (even if this is a simplification) to express their conviction. In the coming weeks (as this trend has already begun), the CT community will debate why a particular asset might prevail (e.g., SOL vs. others, or meme coins) or why a specific application supporting an asset might succeed (such as utility tokens, DeFi governance, etc.).

What I want to suggest is that starting today, a more risk-adjusted advantageous play may be betting on ecosystems without their own native tokens. In my view, Base’s structure creates the strongest potential for sustained adoption, with the caveat that it may depend on ETH’s resurgence.

However, given that I believe ETH’s potential is currently underestimated—if/when BTC, ETH, and SOL see relative value appreciation in the coming weeks—there will inevitably be a need for a "reservoir" to absorb this newly generated and recycled wealth.

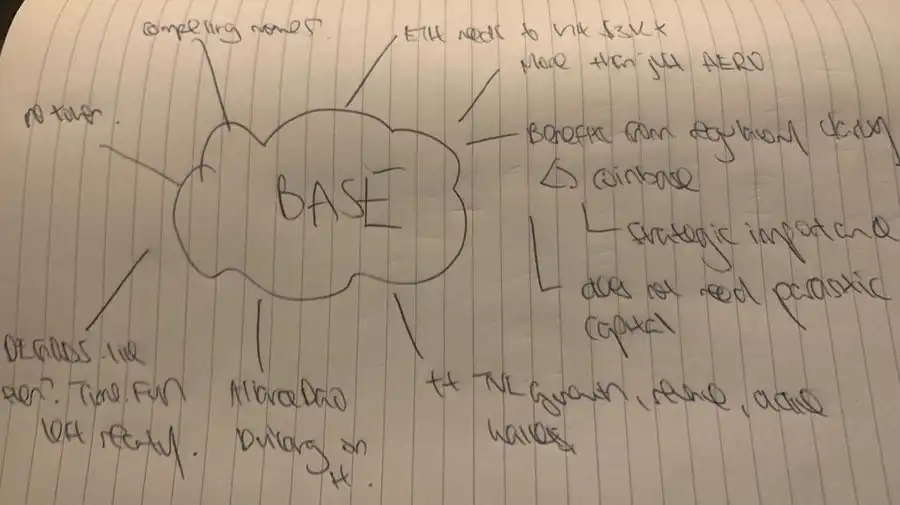

I Believe Base Is Poised to Win This Position

1. The interconnectivity of "faucets" on Base has improved dramatically this year, yet remains underappreciated.

2. Base holds significant strategic value for COIN and has a real balance sheet to back it up.

3. Base has been tested multiple times this year and has performed exceptionally well.

I have adjusted my positioning accordingly and will elaborate in upcoming threads on my rationale, along with the risks and mitigation strategies involved in redirecting on-chain traffic to what I consider the most vibrant "playground": Base.

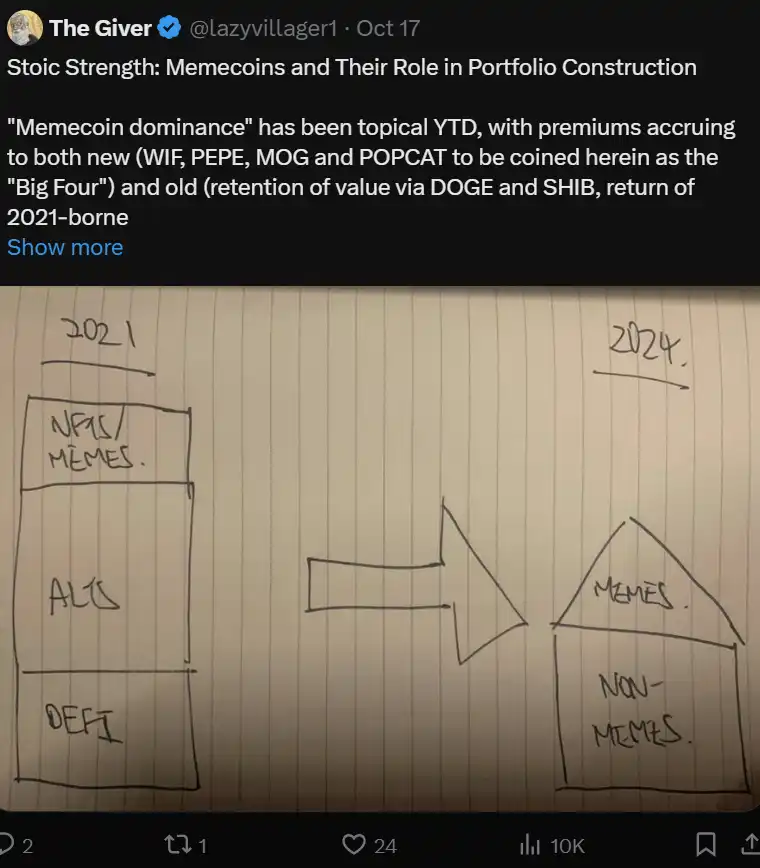

Meme Coins and Their Typical Conditions for Success

The key point is that low-market-cap meme coins often deliver uncorrelated returns, and on-chain activity typically heats up around periods of major uncertainty.

Reflecting on the Strength of Major Assets and Their Impact on On-Chain Activity

Based on the above, I believe on-chain activity will show very strong performance in the coming weeks.

This trend is supported by the performance of major assets—buying pressure is primarily spot-driven, and open interest (OI) for both ETH and BTC has largely reset to pre-election levels. The rise in funding rates stems mainly from a lack of new short positions being established (and recent breakouts—short liquidations have reached $1 billion, the highest level this year)—not from excessive leverage.

Therefore, assuming current price ranges hold, I believe on-chain activity will become a convergence point for off-chain capital, new inflows, and recycled funds. Compare the capital created in the past week with that from 3–4 weeks before the election. The latter saw sharp increases in fundraising and open interest, but beyond BTC, other assets struggled to truly attract what I call "mercenary capital."

The capital flows seen in the past week not only extend broadly beyond BTC (with all selected assets seeing widespread global gains), but even include DOGE—a very important signal reflecting the nature of these buyers: willing to use leverage, speculative, and trading 24/7. These buyers are not confined to U.S. trading hours, similar to BTC’s October rally.

We’re less than a week into this price environment—the market dislocation is evident: capital needs time to assess whether these inflows are irrational or substantive. During this period, projects capable of large marginal swings should experience the most pronounced repricing effects.

Base Is Already Winning—Despite Having No Token

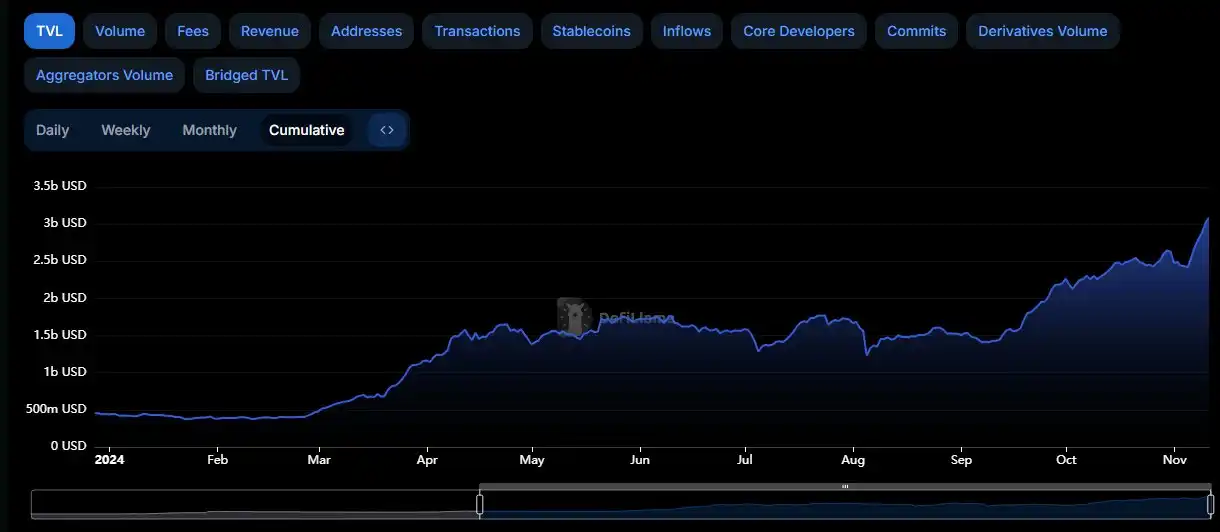

Base may be one of the most misunderstood ecosystems today. Due to its unique construction, Base lacks typical crypto-native investors/KOLs to manage and spread information. Yet across metrics, Base is winning. The attention Base receives relative to its user/wallet/TVL growth is likely the most disproportionate among all current projects.

See the chart below—an attention capture of Base by elfa ai. In terms of collective mentions, Base had approximately 18 mentions on CT over the past 7 days, ten times lower than ARB, and roughly equivalent to STARKNET, BLAST, and OP.

It is the only ETH-L2 whose TVL has grown consistently throughout the year, despite lacking user incentive programs like other L2s (e.g., BLAST GOLD). With a TVL of $3 billion, it even surpasses ARB (which hosts the highly popular HyperliquidX, with ~$1 billion TVL).

In October, Base also generated the highest revenue among developing ecosystems (a month when TRON declined while Base and ETH grew). Currently, Base also leads in independent active wallets and transaction count (actual data should be treated cautiously, but this is the only picture we can draw).

Base evokes memories of SOL in Q4 last year—a builder-friendly environment gaining traction during a period of low attention.

Base Disrupts and Breaks Traditional L1/L2 Operating Models

The traditional operating model usually follows these steps:

1. A concept for an ecosystem is developed, ideally with a unique variation (faster, more reliable, more decentralized, easier to build on, less trust-dependent, etc.)

2. Fundraising occurs by distributing tokens at near-zero valuations (typically to well-connected firms and resource-rich entities)

3. While building, connections are made with dApp developers—each blockchain usually seeks a local "bank," so there may be some form of lending and trading protocols. Developers are compensated with token rewards for on-chain development.

4. Users are attracted through points/token incentive programs, depositing/staking stable capital to earn yield rewards.

5. Users/new TVL provide the founding team with a base to raise funds from new investors at higher valuations in subsequent rounds—pointing to user/fund inflows as proof.

6. After launch, users initially receive non-locked tokens as rewards; investors and team members must wait via locked tokens (but with much larger allocations).

7. Lending protocols often partner with market makers and investors to commit yields and maintain capital on-chain.

8. Gradually, organic capital inflow and retention are hoped for through certain metrics (interoperability, ease of use, ecosystem richness, etc.), reducing or eliminating the need for dilutive capital.

9. Founding teams use tokens to pay early supporters and employees—making tokens effectively free expenses (to pay vendors). Ideally, the ecosystem becomes self-sustaining through recurring revenue.

This model has matured but is now being disrupted. HyperliquidX stands out as the clearest example of launching without reliance on traditional methods and ignoring most of the above steps.

This year, this fundraising model has clearly failed at multiple stages, with pain points including:

• Mining incentives are often poorly defined; once capital is locked, it becomes "hostage," allowing teams to act recklessly and retroactively change terms.

• Investors/team members can stake locked tokens—enabling them to sell staking rewards at TGE (Token Generation Event), severely diluting retail investors.

• New capital is extremely expensive (opportunity cost in crypto is very high), so without heavy dilution or supply manipulation, users are highly mercenary and typically leave once rewards end.

Why Base Is More Likely to Succeed?

Base is not just an L2—it is Coinbase’s on-chain lever. Coinbase gained this opportunity due to reduced regulatory scrutiny following Trump’s election (i.e., improved policy environment).

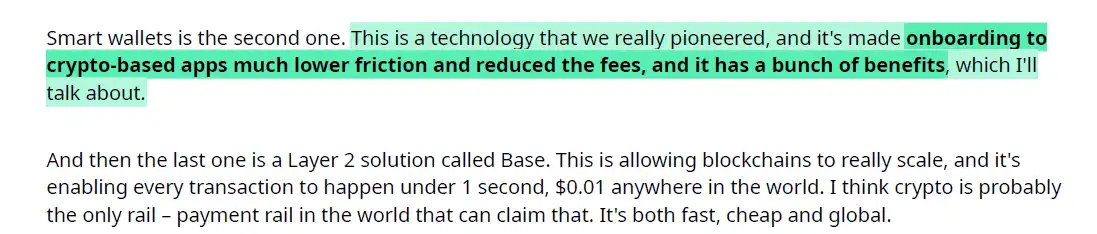

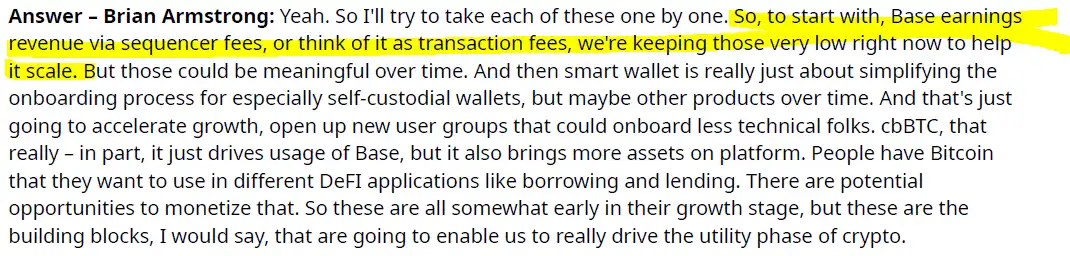

In other words, Base does not intend to win through the traditional "fat-tail" approach I described earlier. What does that mean? Below is an excerpt from Coinbase’s Q3 earnings call, illustrating how the team views Base:

Base is (partial list only):

1. A testing ground for synergies with CIRCLE and smart wallet development. Coinbase can collect real-time data to fully build a truly independent "Eden" ecosystem (i.e.: i. attract users, ii. seamless onboarding, iii. set up smart wallets using passkeys instead of traditional seed phrases, iv. provide a "playground" for speculation)

2. As Coinbase transitions toward recurring service-based revenue (e.g., via Coinbase One subscription), rather than relying on volatile trading fees, the team’s vision is to attract the largest number of retail users long-term, rather than maximizing fees in the short term.

The latter is precisely the epitome of the extractive value-capture model followed by every blockchain—driven by token creation and its inherent nature. By decoupling the ecosystem from a native token, Base can take a longer-term view to "win." In other words, Base’s only future way to generate revenue (since COIN already exists as equity) is by charging applications and users "rent."

The most critical point:

The biggest difference between Base and other blockchain projects is that it is backed by a company with a real balance sheet. Every other ecosystem, at some point, relies on financially incentivized counterparties seeking returns. These counterparties themselves do not possess infinite capital.

Once returns are realized, this support—whether financial or community-based—will withdraw. Therefore, other ecosystems have a lifecycle, or a time limit: eventually, new supporting capital stops flowing in, and products must stand on their own. You’ll see some ecosystems already struggling in the next 12–16 months (e.g., shutting down platforms).

The Base <> Coinbase relationship may be different. If Base stops receiving support, it means a crucial part of Coinbase has failed (and thus, the overall strategic vision has failed). Since Coinbase itself generates traffic and revenue by being "where the price is," we can infer that Base may enjoy a form of "evergreen" funding support.

Base Has Proven Its Resilience

Base first emerged as the foundation for Friend Tech (then essentially an empty shell with limited functionality). Since then, it has gone through several key phases:

1. Application migrations, such as timedotfun. See jessepollak’s response: link. This reflects a very positive, supportive attitude, recognizing that each chain has its unique value.

2. The only project to successfully incubate another L2—degentokenBase. DEGEN captured massive attention during a weekend earlier this year, quickly pushing its valuation to $600 million, comparable to apecoin’s self-built rise this month.

3. The only chain capable of hosting AI-related applications at the scale of SOLANA—VIRTUAL, which rose from $0 to $500 million during October’s AI and meme coin frenzy.

In my view, no other ecosystem could withstand such intense attention and drive capital inflows of this magnitude. So the question is: if others could do it, why haven’t they? Thus, Base clearly demonstrates the ability to support novel and interesting projects/applications far beyond simple yield loops or lending apps.

Here are a few more examples:

warpcast

BlueSocialApp

OnchainKit

liberoverse

Sofamon xyz

BetBase xyz

dreamcoinswow

ethxy

This is not an exhaustive list, nor an endorsement of any names mentioned, but merely a snapshot showing the diverse range of creative projects built on Base since its last iteration—especially post-Friend Tech era (when most of these apps were not yet formally launched).

Buying at a Moment Perceived as a Value Bottom

Profiting from Base is essentially betting on the success of the entire ecosystem—or even acting as a proxy for Coinbase. There is no single token to concentrate demand, so true network effects can be achieved holistically.

Currently, most tokens on Base are at cyclical lows—and I won’t name or recommend any, but sample charts illustrate this; these are randomly selected.

Therefore, I believe Base is the most attractive place to deploy capital, because you're effectively betting on two things—and this has nothing to do with leverage or clever token selection:

1. ETH stabilizes and finds a bottom that supports on-chain demand (as previously discussed),

2. Winners in the ETH ecosystem will want to recycle profits somewhere.

Given the lack of organic options on the mainnet (which have shifted to L2s) and weak NFT market demand this year, I bet this attention and capital will converge on Base.

In summary—as long as ETH stays hot, Base should stay hot too.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News