Buy the Rumor Series: Growing Expectations for Improved Regulatory Environment – Which Cryptocurrency Benefits Most Directly?

TechFlow Selected TechFlow Selected

Buy the Rumor Series: Growing Expectations for Improved Regulatory Environment – Which Cryptocurrency Benefits Most Directly?

The ETH Staking sector could see the most direct gains, and Lido, as the leading project, may also overcome its current price困境.

Author: @Web3Mario

Summary: There's a well-known market adage, "Buy the rumor, sell the news." Prior to the U.S. election in October, I published an article titled "DOGE’s New Value Cycle: Political Momentum and Musk’s 'Department of Government Efficiency' (D.O.G.E) Political Career", which received positive feedback and delivered expected investment returns. I am grateful for everyone’s support. In my view, during the current transition period before Trump officially takes office, numerous similar trading opportunities will emerge. Therefore, I’ve decided to launch a new series—“Buy the Rumor”—to identify and analyze current market hype themes and extract actionable trading insights.

Last week, a notable trend emerged: with Trump’s strong comeback, markets began pricing in expectations that U.S. SEC Chair Gary Gensler might resign. You can now find analyses across major media outlets discussing potential successors. In this article, we’ll explore how improving regulatory outlooks could directly benefit specific cryptocurrencies. Let me state the conclusion upfront: I believe ETH staking will be among the biggest beneficiaries, and Lido—the leading project in this space—may finally break out of its current price slump.

Recap: Lido’s Regulatory Challenges – The Samuels v. Lido DAO Lawsuit

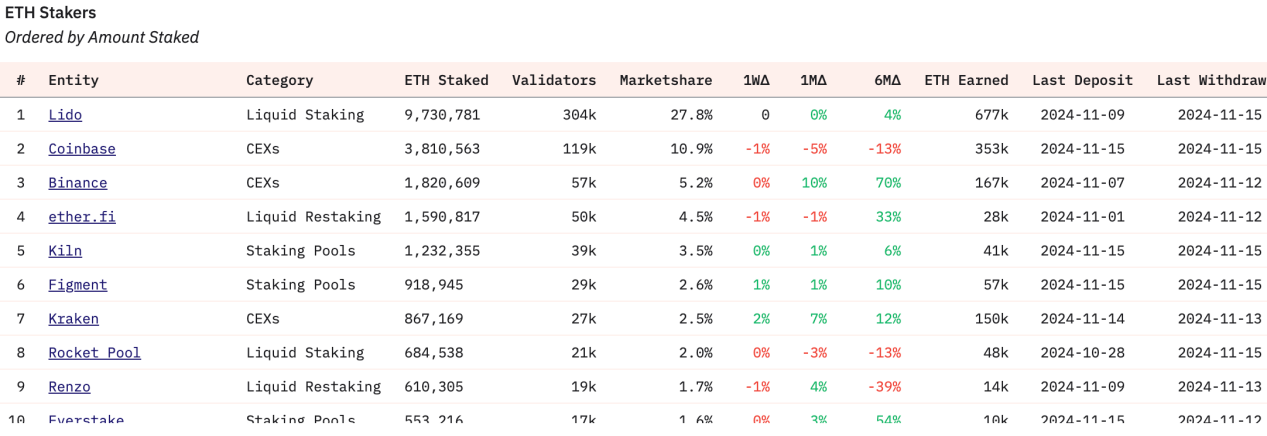

First, some background. Lido is the dominant player in the ETH staking sector. It provides non-custodial technical services that allow users to participate in Ethereum’s Proof-of-Stake consensus and earn rewards, while lowering both the technical barriers and the 32-ETH capital requirement of native staking. Through three funding rounds, Lido raised a total of $170 million. Since launching in 2022, it has maintained around a 30% market share due to first-mover advantage. According to Dune data, Lido still holds 27% of the market today, with no significant decline—indicating strong underlying demand for its services.

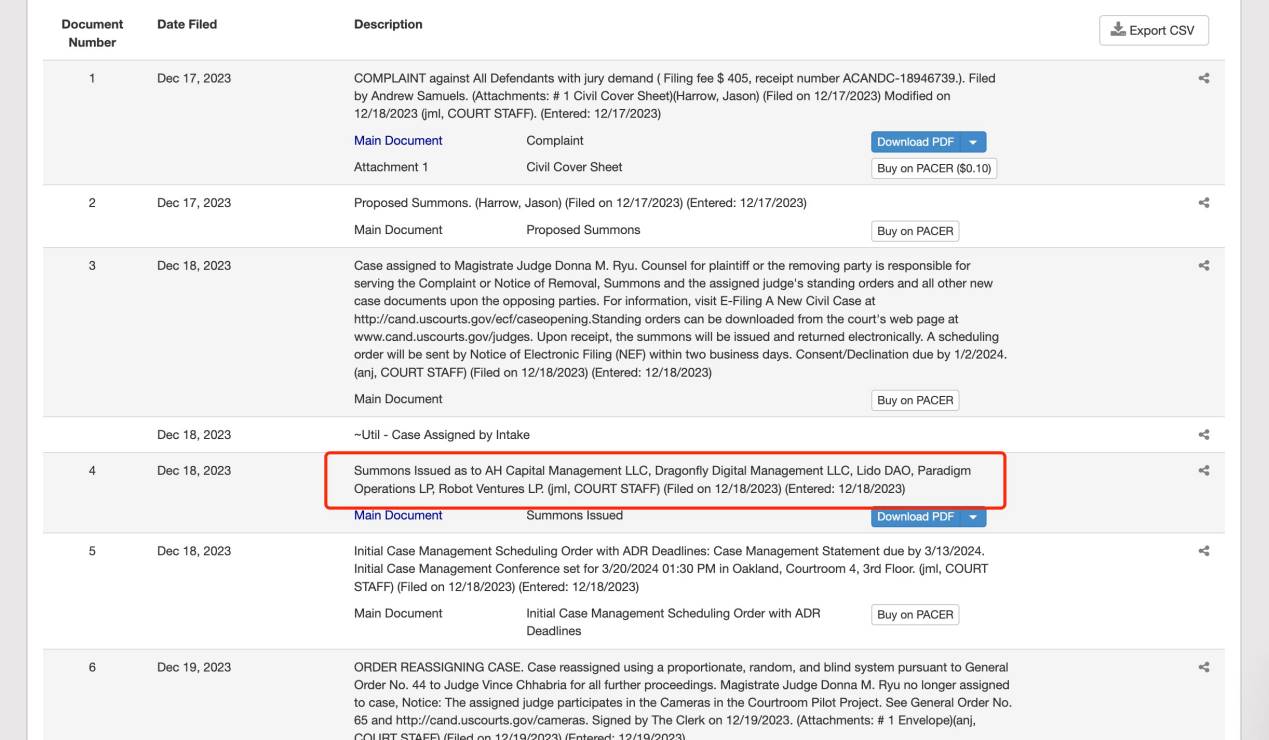

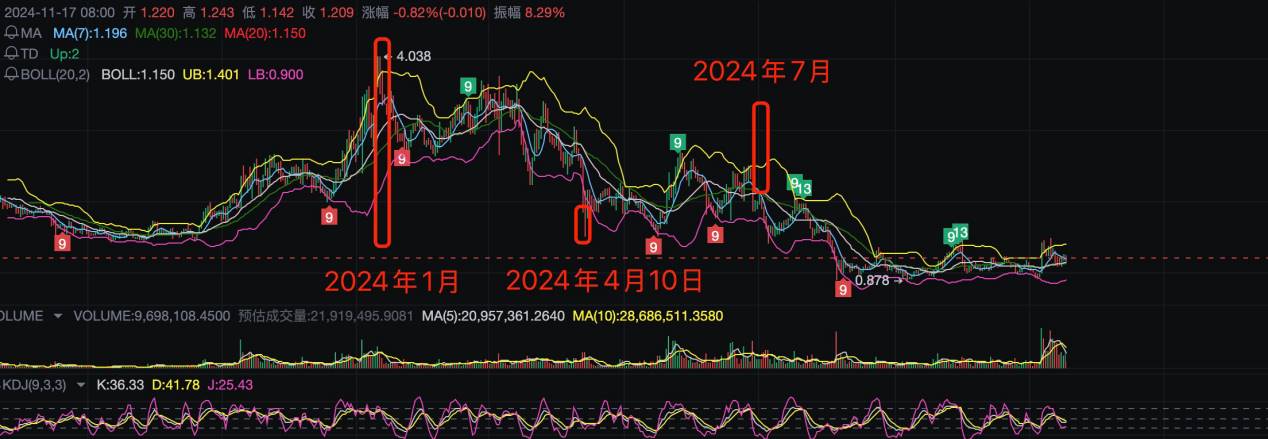

The reason behind Lido’s current price stagnation traces back to late 2023. At that time, its governance token LDO reached an all-time high, achieving a $4 billion market cap. Then came the lawsuit: *Samuels v. Lido DAO*, case number 3:23-cv-06492. On December 17, 2023, an individual named Andrew Samuels filed suit against Lido DAO in the U.S. District Court for the Northern District of California. The core allegation was that Lido DAO—and its associated venture capital firms—sold LDO tokens to the public without registration, violating the Securities Act of 1933. Additionally, by pooling users’ Ethereum assets for staking, Lido created a highly profitable business model but failed to register LDO as a security with the U.S. Securities and Exchange Commission (SEC). Plaintiffs like Samuels claimed they purchased LDO based on belief in the project’s potential and suffered financial losses, thus seeking legal compensation.

The lawsuit didn’t just target Lido DAO—it also named key investors including AH Capital Management LLC, Dragonfly Digital Management LLC, Paradigm Operations LP, and Robot Ventures LP. These institutions began receiving subpoenas from the court in January 2024, right when LDO prices were peaking. Afterward, legal proceedings remained confined between the institutional lawyers and Samuels’ legal team, limiting broader impact at first.

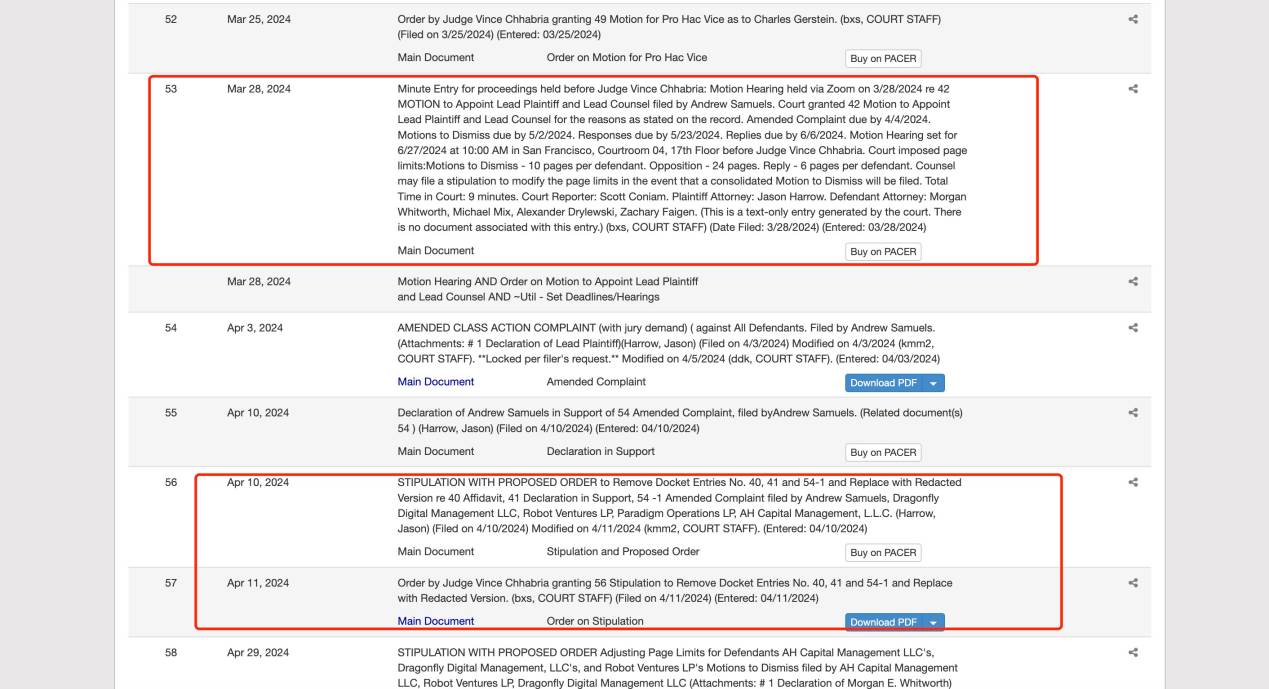

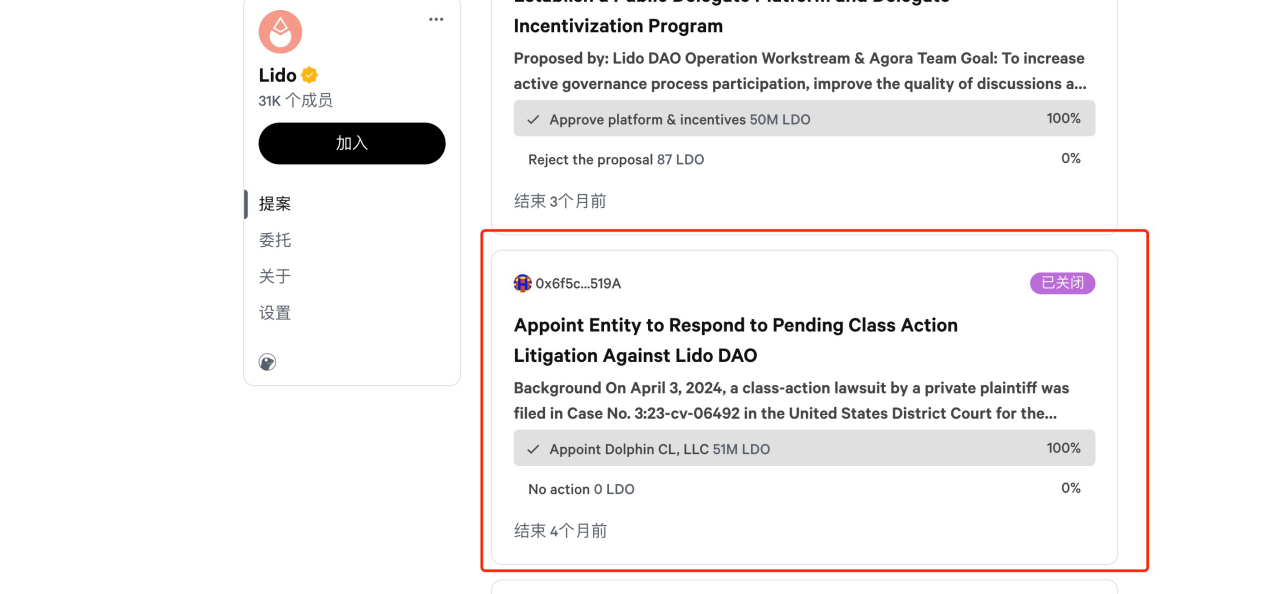

On March 28, 2024, the first motion hearing took place, and on April 10, the court confirmed its decision: after amending certain terms, the case was formally accepted.

Then on May 28, 2024, Samuels’ legal team unilaterally filed a motion requesting a default judgment against Lido DAO. This move was made because Lido DAO, operating as a decentralized entity rather than a traditional company, initially ignored the lawsuit. A default judgment would have been damaging—for example, preventing Lido from defending itself—and following precedents like the Ooki DAO case, outcomes for absent defendants are typically unfavorable. On June 27, the court granted the motion and gave Lido DAO 14 days to respond. As a result, on July 2, 2024, Lido DAO launched a community proposal to hire Dolphin CL, LLC—a Nevada-based law firm—as defense counsel, allocating 200,000 DAI in funding. From this point onward, the case gained widespread attention within the crypto community. After several rounds of legal arguments, the case entered a quiet phase around September.

Meanwhile, another development significantly impacted Lido: on June 28, 2024, the SEC filed a lawsuit against Consensys Software Inc., case number 24-civ-04578. Notably, this occurred the day after the court ruled that Lido DAO had been properly served in the earlier Samuels case. In this action, the SEC alleged that Consensys, through its MetaMask Staking service, engaged in unregistered securities offerings and operated as an unregistered broker via both MetaMask Staking and MetaMask Swaps.

According to the SEC complaint, since January 2023, Consensys had facilitated the offer and sale of tens of thousands of unregistered securities on behalf of liquid staking providers Lido and Rocket Pool. These companies issue liquid staking tokens (stETH and rETH) in exchange for staked assets. While standard staking tokens are locked and illiquid during the staking period, liquid staking tokens—by design—are freely tradable. Investors provide funds to Lido or Rocket Pool and receive these liquid tokens in return. The SEC claims that by distributing these tokens, Consensys participated in unregistered securities sales and acted as an unregistered broker in these transactions.

In this lawsuit, the stETH token issued by Lido was explicitly labeled a security by the SEC. This marked the beginning of a regulatory downturn for Lido. The timeline outlined above aligns closely with LDO’s price trajectory. Indeed, the primary factor suppressing LDO’s price has been regulatory uncertainty stemming from litigation, triggering risk-off sentiment among institutional and retail investors alike. An adverse ruling could lead to substantial fines for Lido DAO, which would inevitably weigh heavily on LDO’s valuation.

Is stETH a Security? And Why Lido’s Future Is the Most Watched Narrative

From the above analysis, we can conclude that LDO’s price weakness isn’t due to poor business performance, but rather regulatory uncertainty. The central question in both cases is whether stETH qualifies as a security. In U.S. law, determining whether an asset is a security typically involves the so-called “Howey Test.” Briefly, the Howey Test originated from the 1946 U.S. Supreme Court ruling in *SEC v. W.J. Howey Co.* It sets the benchmark for identifying what constitutes an investment contract—and thus a security—particularly relevant in crypto and blockchain contexts where regulators assess whether tokens fall under securities laws.

The Howey Test hinges on four criteria:

• Investment of money: Whether there is a financial investment involved.

• Common enterprise: Whether investments are pooled into a collective venture.

• Expectation of profit: Whether investors anticipate profits derived from the efforts of others.

• Efforts of others: Whether profits depend primarily on the managerial or entrepreneurial efforts of a third party.

If all four conditions are met, the instrument may be classified as a security and subject to SEC oversight. Given the current hostile regulatory climate toward crypto, the SEC has taken the position that stETH meets these criteria and should be treated as a security. However, the crypto industry disagrees. For instance, Coinbase argues that ETH staking does not satisfy the four elements of the Howey Test and therefore should not be considered a securities transaction.

• No investment of money: During staking, users retain full ownership of their assets; they do not surrender control to a third party, so no true "investment" occurs.

• No common enterprise: Staking operates via decentralized networks and smart contracts. Service providers aren’t running a joint business with users.

• No expectation of profit: Staking rewards are compensation for validation work—akin to wages—not speculative returns from an investment.

• Not dependent on others’ efforts: Staking operators merely run open-source software and hardware to validate blocks. This is technical support, not managerial effort, and rewards aren’t tied to their operational input.

Therefore, there remains room for debate over whether ETH staking derivatives like stETH qualify as securities. The determination relies heavily on subjective regulatory interpretation. With that in mind, here’s why I believe Lido’s future developments deserve the most attention:

1. The main drag on LDO’s price is regulatory pressure—an inherently subjective factor. Technically, LDO is currently trading near historic lows.

2. ETH has already been classified as a commodity (not a security), giving ETH-related arguments more legal grounding compared to other ecosystems like SOL, which face greater classification risks.

3. ETH ETFs have been approved, and the powerful forces behind them have strong incentives to ensure their success. There are growing rumors suggesting that ETH ETF inflows have lagged behind BTC ETFs. One key reason is perceived lack of differentiation: traditional investors easily grasp Bitcoin’s narrative, but ETH ETFs appear less compelling. If ETH ETFs could offer indirect staking yields to investors, their attractiveness would dramatically increase.

4. Legal resolution costs for the ongoing lawsuits are relatively low. In *Samuels v. Lido DAO*, the plaintiff is a private individual, not the SEC. Defending against such a case carries lower financial and reputational risk compared to direct enforcement actions brought by the SEC.

In summary, during this transitional window—with shifting regulatory dynamics on the horizon—I believe Lido represents one of the most compelling watchlist candidates for recovery and growth.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News