From “Riddle Game” to “Ad Hoc Rules”: A Decade of Absurdity in Crypto Regulation

TechFlow Selected TechFlow Selected

From “Riddle Game” to “Ad Hoc Rules”: A Decade of Absurdity in Crypto Regulation

Value must originate from the programmed operation of a fully functional system, not from someone’s promise.

By: Thejaswini M A

Translated by: Block unicorn

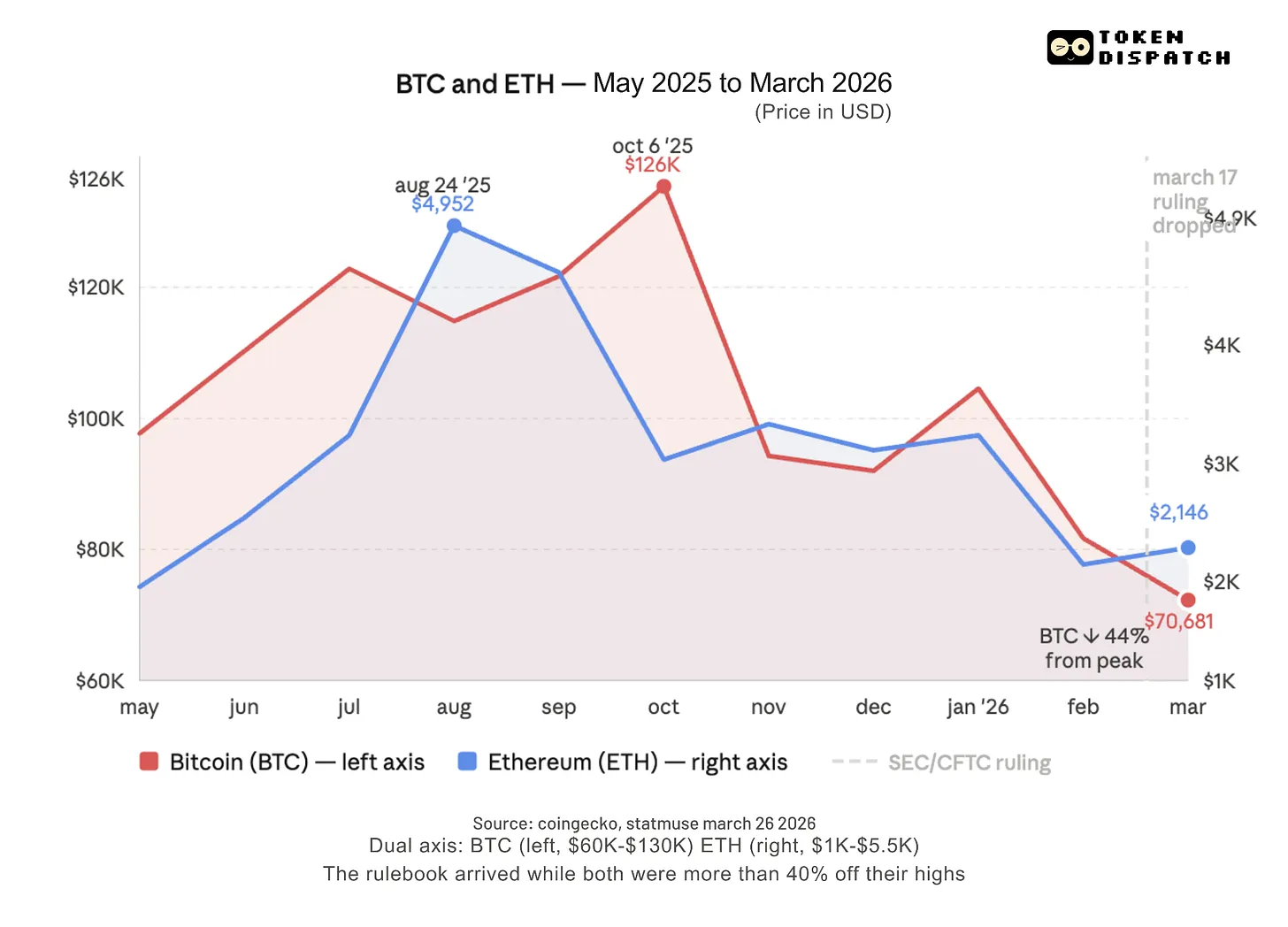

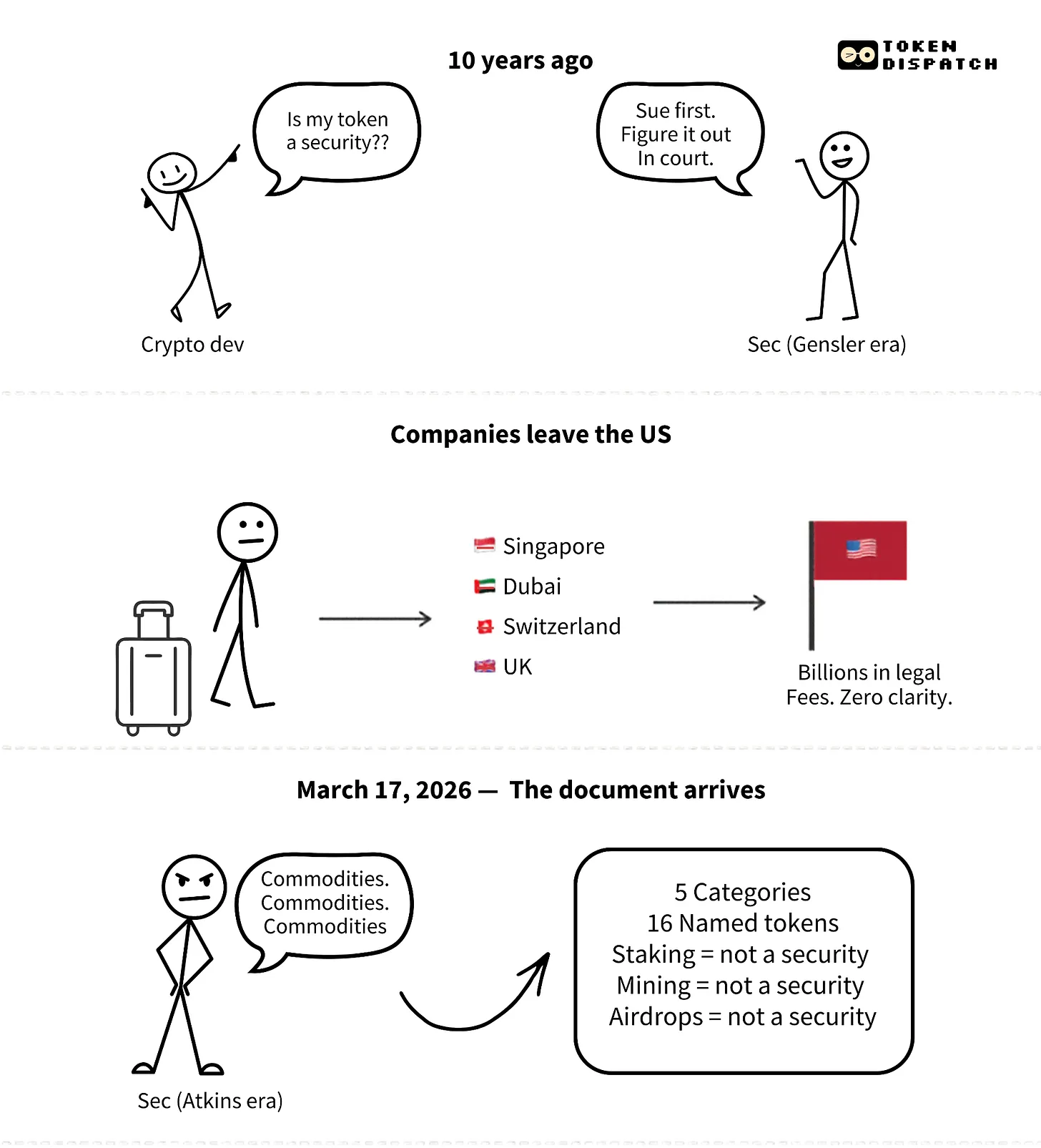

On March 17, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) jointly issued a long-awaited rulebook for the cryptocurrency industry—the first since 2013. I’m relieved—and actively working toward compliance.

Bitcoin has fallen 44% from its October high. Ethereum trades around $2,000—less than half its price from seven months ago. The total market cap of altcoins has evaporated by $47 billion from its peak. The Fear & Greed Index stands at 11—not 11 out of a bad week, but 11 out of 100. That means people have stopped debating where the bottom is and are now dumping whatever crypto they have left.

And right then—on March 17—the SEC and CFTC released a document that finally answered the question: What *is* the token you hold? After a decade of litigation, hundreds of enforcement actions, and billions in legal fees, the answer arrived. Some firms even relocated to Singapore rather than continue playing Gary Gensler’s guessing game. And it came just as Ethereum dipped below $1,900.

But here’s the key: while the token economy itself lies in ruins, everything underneath it is booming. Stablecoin circulation has surpassed $316 billion. On-chain real-world assets (RWAs) now total $26.5 billion—and growing. That’s why Morgan Stanley is building a crypto trust bank. Meta abandoned the metaverse—but is rolling out stablecoins on WhatsApp. Stripe processes $400 billion in stablecoin transactions annually. Nasdaq is building a tokenized stock trading platform. Cryptocurrency is becoming the backbone of global finance—and most of the time, it doesn’t depend on tokens at all.

Cryptocurrency is no longer just a speculative asset class. The regulatory framework announced on March 17 was designed for first-generation crypto—but it arrived only after second-generation crypto had already taken hold.

That doesn’t mean it’s meaningless.

SEC Chair Paul Atkins once said: “We’re no longer the ‘Securities and Everything Commission.’” Was that statement made a little too late?

U.S. regulators have, for the first time, established a unified definition for cryptocurrencies—five categories, with every token falling into one. Below are those definitions. Read them as if you’ve never heard of any of these concepts before.

Digital commodities are the headline act. A digital commodity is a crypto asset whose value arises from the programmatic operation of a fully functional crypto system and its supply-and-demand dynamics—not from management by a central issuer. If the network is truly decentralized and operating properly, with no company propping it up, the asset qualifies as a commodity—regulated by the CFTC, not the SEC.

Sixteen major tokens—including Bitcoin, Ethereum, Solana, XRP, Cardano, Avalanche, Polkadot, Chainlink, Dogecoin, and Shiba Inu—have been officially designated digital commodities. Dogecoin and Shiba Inu qualify because no sponsor or institution drives their value. They make no promises, have no roadmap, and no team’s ongoing work is essential to their value. That’s precisely why they’re treated as commodities—not securities. The test hinges on whether someone promises returns based on their efforts.

Digital securities refer to tokenized stocks, bonds, and Treasury securities. Put simply: if it was a security before going on-chain, it remains a security afterward—regulated by the SEC. That’s it.

Digital collectibles refer to NFTs tied to specific items or experiences. Digital utilities refer to assets used to access software or services—with no expectation of investment return. Stablecoins have their own dedicated category under the GENIUS Act.

Staking, mining, and airdrops are now explicitly permitted. The ruling clarifies that receiving mining rewards, participating in on-chain staking, or claiming digital commodity airdrops does *not* constitute securities transactions. This eliminates one of the largest legal risks facing proof-of-stake networks since the Gensler era. Packaging non-security tokens is also now permitted.

All 16 named tokens are foundational infrastructure, backed by years of decentralized development. DeFi protocol tokens—like JUP, POL, METEOR, and the vast majority launched over the past two years—were *not* named and clearly do not meet the bar. A fully functional crypto system without centralized oversight is a high threshold—and most actively developed protocols fall short. The gray area this interpretation was meant to resolve remains just as murky—for the tokens most people actually hold.

Value must arise from the programmatic operation of a fully functional system—not from anyone’s promise. That single test transforms a decade of ambiguity into something compliance officers can actually work with.

There’s a Catch

This announcement does *not* constitute formal rulemaking under the Administrative Procedure Act—and carries no legal force or binding regulatory authority.

Read that sentence again. The 68-page document we’ve waited years for is merely an interpretive release—not law, not regulation—just a policy statement issued by the current chairs of the SEC and CFTC, revocable at any time.

Still, this interpretation *is* a formal agency action—and binding. But absent legislation, future administrations may revise it. The document itself reserves each agency’s right to refine or expand its views. A future SEC chair with different political priorities could overturn this interpretation without congressional approval. The next administration won’t need new laws—just new leadership.

Atkins knows this well. He flagged it the same day the release dropped, urging Congress to act and deliver lasting clarity. He framed the interpretation as a transitional measure—pending congressional action on comprehensive market structure legislation: the CLARITY Act. That bill is currently pending in the Senate.

The CLARITY Act

The House passed the CLARITY Act in July 2025 by a vote of 294–137. Such strong bipartisan support signals genuine consensus.

Then it stalled in the Senate.

The main roadblock? Stablecoin yield. Banks argue allowing crypto platforms to pay interest on stablecoin balances would trigger deposit flight—people pulling money from savings accounts to hold USDC for higher returns. Banking lobby groups mobilized quickly. The Senate Banking Committee canceled its scheduled January 2026 markup. For the next two months, the bill went nowhere.

On March 20, Senators Thom Tillis and Angela Alsobrooks confirmed a principles-based agreement on stablecoin rewards—endorsed by the White House. The deal: passive yield on stablecoins is banned; activity-based rewards tied to payments or platform usage remain allowed. Neither side is happy—but that’s how compromises happen.

Yet the yield agreement is just *one* of five steps required before the CLARITY Act becomes law. The remaining four legislative milestones fall within the year’s most politically congested period.

- Senate Banking Committee markup—and full Senate vote (requiring 60 votes)

- Reconciliation with the Agriculture Committee

- Reconciliation with the House version

- Presidential signature

The Banking Committee markup is scheduled for the second half of April—after Easter recess. Senator Bernie Moreno warned that if the bill fails to reach the Senate floor by May, digital asset legislation could stall for years.

Meanwhile, the Iran war dominates Senate floor time. Trump has signaled he wants voter ID legislation passed first. Provisions on decentralized finance (DeFi) remain unresolved—and Senate Democrats express concern about illicit finance risks. Ethics provisions are also unsettled—especially whether senior government officials should be barred from profiting from crypto assets. Given this administration’s holdings, that issue is politically sensitive. Senate Republicans are now discussing attaching community bank deregulation provisions as a bargaining chip—sparking entirely new rounds of negotiation.

The House Financial Services Committee recently held a hearing titled “Tokenization and the Future of Securities: Modernizing Capital Markets.” Witnesses included Kenneth Bentsen of SIFMA, Summer Mersinger of the Blockchain Association, Christian Sabella of DTCC, and John Zecca of Nasdaq. Both Nasdaq and NYSE are building tokenized stock trading platforms. DTCC handles current settlement. If DTCC endorses blockchain efficiency, the debate is effectively over.

So infrastructure is being built atop a rulebook that may not exist two years from now. That’s the industry’s current dilemma. Companies are making billion-dollar decisions—building custody systems, tokenization platforms, and staking infrastructure—all based on a persuasive—but legally nonbinding—interpretive release.

What’s Permanent, and What’s Not

For readers holding any of the 16 named tokens—like ETH, SOL, or XRP—their status as digital commodities is now formally recognized under U.S. law, thanks to the public statements of both agency heads. As long as those leaders—or their successors—maintain that stance, the classification stands.

If the CLARITY Act passes, it becomes law. No future chair can unilaterally reverse it without congressional approval. The listed assets will be permanently defined—and the classification criteria will be legally binding.

If it fails to pass by May, the current classification rests solely on the opinion of a single administrative branch. Right now, the 16 named assets are temporarily safe—but not all assets are named. Most DeFi tokens, most newly launched tokens, and any permissionless asset with no clear issuer remain in the gray zone—a gap the prior interpretation did not resolve.

The most eagerly awaited sentence reads like pencil draft—waiting for someone to pick up a pen and make it official.

Everything hinges on the Senate’s next six weeks. Will these rules last long enough for any of this to matter?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News