The New Financial Cluster Revolution: Why the PayFi Market Could Be 20x Larger Than DeFi?

TechFlow Selected TechFlow Selected

The New Financial Cluster Revolution: Why the PayFi Market Could Be 20x Larger Than DeFi?

As high-performance blockchain technology advances, PayFi's true value will rapidly expand and scale.

By Shigeru Satou

PayFi, short for Payment Finance, refers to an innovative technological model that integrates payment functionality with financial services within the blockchain and cryptocurrency space.

The core of PayFi lies in the processes surrounding sending, receiving, and settling cryptocurrencies—not trading itself. This model encompasses not only crypto payments and transactions but also lending, wealth management, cross-border payments, and other financial activities. By leveraging decentralized technology, PayFi makes financial operations faster and more secure while reducing friction and costs inherent in traditional financial systems, thereby enabling seamless global value transfer and advancing financial inclusion.

The concept of PayFi was first introduced by Lily Liu, President of the Solana Foundation, at EthCC in July 2024. In her view, PayFi represents a new way of building financial markets—centered around the Time Value of Money (TVM)—to create novel financial primitives and user experiences that are difficult or impossible to achieve in traditional or even Web2 finance.

The vision of PayFi is to revolutionize payment systems using blockchain technology, enabling more efficient and lower-cost transactions while delivering entirely new financial experiences. It aims to build complex financial products and applications, integrating them into a unified value chain and forming a new financial cluster.

The CGV Research team believes that as high-performance blockchain technologies evolve, the true value of PayFi will rapidly scale and expand. This growth will accelerate the integration of payments and financial services, making cryptocurrencies more practical and efficient for daily transactions and sophisticated financial operations alike. In the future financial ecosystem, PayFi will become a key driving force.

PayFi: Inheriting and Expanding Bitcoin’s Payment Vision

Bitcoin originated from Satoshi Nakamoto's revolutionary whitepaper, "Bitcoin: A Peer-to-Peer Electronic Cash System," which proposed the idea of a “decentralized payment” system. This concept introduced not just a new form of currency—Bitcoin—but more importantly, envisioned a global payment network that operates without intermediaries, bypassing the constraints of traditional financial institutions to enable faster, transparent value transfers. Nakamoto’s vision aimed to overhaul existing payment systems by eliminating high fees, long settlement times, and financial exclusion.

However, despite successfully sparking the cryptocurrency revolution, Bitcoin has largely failed to fulfill its original purpose as a medium for everyday payments. Instead, it is primarily treated as a store of value rather than a currency used in daily transactions.

Over time, stablecoins have filled this gap. By mapping fiat currency values onto blockchains, stablecoins bridge the real-world financial system with the crypto economy, creating the first practical use case for blockchain-based payments. Since 2014, stablecoin adoption has grown exponentially, demonstrating strong market demand for blockchain-powered payments. Stablecoins allow users to enjoy the transparency and decentralization benefits of blockchain while avoiding the volatility risks associated with cryptocurrencies. To date, stablecoins support approximately $2 trillion in annual payments—approaching Visa’s yearly transaction volume.

Nevertheless, despite their contributions, blockchain payments still face numerous challenges such as poor user experience, transaction delays, high costs, and compliance issues. These obstacles limit the widespread adoption of blockchain payments as a mainstream payment method.

The further expansion of the payment ecosystem depends heavily on financial tools and financing mechanisms. In traditional finance, instruments like credit cards, trade financing, and cross-border payment systems significantly enhance global payment usage by providing liquidity and financing options.

As an emerging industry, blockchain doesn’t need to rebuild the market from scratch. Instead, it can build upon existing markets by offering more valuable products and solutions through blockchain technology. It is precisely in this context that PayFi emerges.

By leveraging the high performance and low-cost transaction capabilities of advanced public blockchains, PayFi not only enables blockchain payment systems to potentially surpass traditional financial mechanisms but also creates a more liquid and adaptable global financial market.This evolution represents both a return to Bitcoin’s original intent and a major innovation built upon it. Through PayFi, blockchain-based payment systems can finally unlock their full potential, pushing the global financial system toward greater efficiency and inclusivity.

Core Concept of PayFi: Time Value of Money (TVM)

"Time is more valuable than money. You can get more money, but you cannot get more time."

The Time Value of Money (TVM) is a fundamental concept in finance that emphasizes the difference in the value of money across different points in time. The basic principle of TVM is that a given amount of money today is worth more than the same amount in the future because funds held today can be immediately invested to generate returns or spent to yield immediate utility.

In simple terms, the key idea behind TVM is “opportunity cost.” When someone holds onto money instead of using it immediately, they forgo potential investment opportunities and the returns those could generate. Therefore, the present value of money must reflect these foregone opportunities. For example:

-

Loans and Mortgages: Interest rates in bank loans are calculated based on TVM—the interest paid by borrowers compensates lenders for the temporary use of capital;

-

Investment Evaluation: Investors assess the present value of future earnings when evaluating stocks, bonds, or real estate to determine investment attractiveness;

-

Capital Budgeting: Companies evaluate future cash flows of various projects and discount them to present value to help management make optimal investment decisions.

PayFi leverages blockchain technology to allow users to realize the time value of money on-chain at extremely low cost and high efficiency. Using smart contracts and decentralized platforms, PayFi enables users to manage and invest funds without intermediaries, maximizing capital utilization. This new model dramatically reduces transaction costs and processing times, allowing funds to quickly re-enter the market for reinvestment or other purposes.

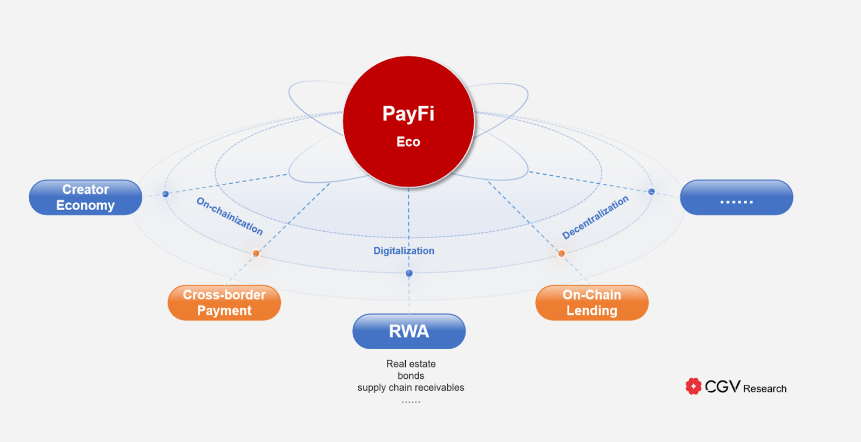

Additionally, PayFi’s infrastructure opens the door to developing more complex on-chain financial products—such as on-chain credit markets, installment payment systems, and automated investment strategies powered by smart contracts—expanding into more sophisticated financial products and applications, creating an integrated value chain and forming a new “financial cluster.”

Bridging RWA + DeFi: Building a New Financial Cluster Centered on PayFi

In the financial system, Real-World Assets (RWA) and Decentralized Finance (DeFi) each possess unique advantages but also face distinct challenges: RWAs have massive market size and stable value, yet suffer from relatively low liquidity, limited transparency, and inefficient trading; DeFi offers efficient trading mechanisms and global liquidity but relies mainly on crypto assets and lacks direct connection to the real economy.

Contrary to some industry views—such as “PayFi is merely a subcategory within the RWA sector”—CGV Research believes RWA is part of the PayFi ecosystem. Beyond RWA, PayFi also involves broader crypto assets, smart contract-driven financial services, and decentralized payment and settlement systems. Leveraging DeFi to onboard and apply RWAs is a crucial component in realizing PayFi’s core functions.

RWAs require DeFi to improve liquidity and trading efficiency—using blockchain digitization and smart contracts to enable fast, low-cost global fundraising while enhancing transaction transparency and security. At the same time, DeFi enriches its asset base by incorporating RWAs, reduces volatility risk, provides stable yield sources, connects with the real economy, and promotes real-world adoption and development globally.

Through PayFi, RWAs and DeFi cease to be isolated financial systems—they become interdependent and complementary components, achieving integration and innovation between real-world assets and on-chain financial services.

-

Digitalization and On-Chain Representation: Bringing RWAs onto the blockchain. PayFi platforms first tokenize RWAs via smart contracts, enabling representation and trading on-chain. This ensures transparency and security of RWA value and ownership. Traditional RWA assets can thus be divided into smaller units, facilitating global trading and investment.

-

Smart Contracts and Payment Systems: Enabling efficient transactions and settlements. Once tokenized, PayFi platforms use smart contracts to automate transaction and settlement processes. This accelerates speed, lowers costs, and ensures transparency and security. Additionally, PayFi’s on-chain payment system simplifies asset transfers and payments, solving common problems in traditional finance such as delayed settlements and high fees.

-

Liquidity Pools and Funding Channels: Providing financial support for RWAs. PayFi’s liquidity pools offer ample funding for RWAs, enabling access to global investor capital. By using RWAs as collateral, PayFi allows investors to participate in financing activities on DeFi platforms while ensuring stable funding sources for RWAs. This model increases RWA liquidity and offers diversified investment opportunities for DeFi investors.

-

Risk Management and Transparency: Enhancing market trust. Blockchain technology ensures all RWA transactions are transparent and verifiable, reducing information asymmetry and operational risk. The automatic execution of smart contracts minimizes human intervention, while blockchain immutability secures transaction records. Together, these factors strengthen market confidence and drive deeper integration between RWAs and DeFi.

In the future, PayFi will play an increasingly vital role in boosting global asset liquidity, lowering transaction costs, and improving market transparency. According to Lily Liu, PayFi brings RWAs and institutional finance into on-chain liquidity pools, creating an integrated value chain and forming a “new financial cluster,” likely the biggest theme in the current crypto market cycle.

Why Will PayFi Happen on Solana?

Why is PayFi emerging on Solana rather than other L1 blockchains or L2 solutions? Lily Liu’s answer: “Solana possesses three key advantages—high-performance blockchain infrastructure, capital liquidity, and talent mobility.” These strengths create barriers that competitors currently struggle to overcome.

First, high-performance blockchain. Solana’s core technical advantage lies in its unique Proof of History (PoH) consensus mechanism, enabling over 65,000 transactions per second (TPS), with typical confirmation times around 400 milliseconds. This far exceeds Ethereum’s 10–15 TPS and longer confirmation times. Even Ethereum’s L2 solutions like Optimistic Rollups cannot match Solana in latency and throughput. While Visa claims peak capacity of 56,000 TPS, in practice it averages only about 1,700 TPS. By comparison, Solana fully meets real-world payment demands.

Second, capital liquidity. As of August 30, 2024, Solana’s ecosystem total value locked (TVL) exceeded $10 billion, attracting major investments from top-tier venture capital firms including Andreessen Horowitz (a16z), Polychain Capital, and Alameda Research. This capital liquidity provides robust financial backing for PayFi’s expansion.

Finally, talent mobility. The Solana Foundation actively fosters developer community growth, organizing over 500 hackathons and global developer education programs. By 2024, the Solana ecosystem had more than 5,000 active developers—one of the fastest-growing blockchain developer communities worldwide. This strong talent pool supports continuous innovation and attracts new technical and financial experts, laying a solid foundation for PayFi development.

PayFi leverages programmable payments to connect the traditional world with the blockchain world, making scalable on-chain credit finance possible through smart contracts. Solana’s strengths not only support PayFi’s growth but also give it strong competitiveness in the future global payment and financial markets.

Take PYUSD as an example: PayPal chose Solana as the new public chain for PYUSD payments due to its fast settlement capability, low transaction fees, and strong developer ecosystem. Solana’s token extension features—including confidential transfers, transfer hooks, and memo fields—provide essential flexibility and commercial utility for PYUSD.

As PayPal stated: “These features aren't optional. If we want PYUSD to function effectively in broader commerce, we must provide them to merchants.” Today, Solana has become the dominant platform for PYUSD, capturing 64% of the market share compared to Ethereum’s 36%. Moreover, as early as September 2023, Visa expanded USDC settlement capabilities from Ethereum to Solana.

PayFi Use Cases and Representative Projects

The essence of PayFi is to reshape and upgrade the traditional financial system using advanced cryptographic technology. Therefore, every financial scenario can—and should—be rebuilt using PayFi.

1. Cross-Border Payments and Trade

Traditional cross-border payments face difficulties due to fragmentation within centralized sovereign currency systems. Influenced by foreign exchange controls and national monetary policies, these payments remain cumbersome, slow, and expensive. Initially, many believed cryptocurrency payments could be an ideal alternative to traditional cross-border payments, but enterprise-level solutions still had significant shortcomings.

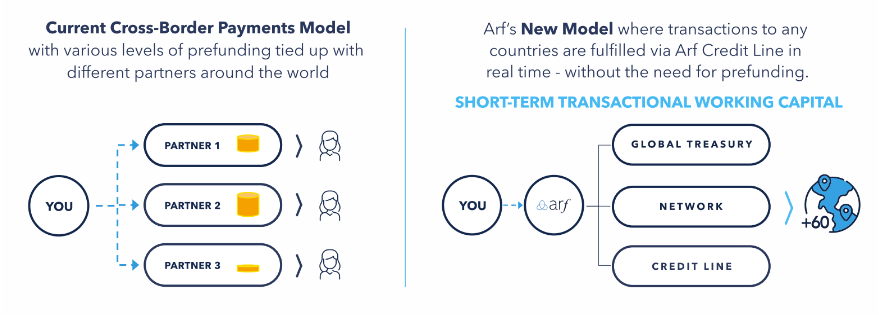

Today, the cross-border payment industry still heavily relies on prefunded accounts to achieve same-day settlement. Currently, over $4 trillion in capital is tied up in these prefunded accounts—an enormous hidden cost for financial institutions and the global payments sector. PayFi optimizes this by leveraging traditional credit finance to power crypto-based services.

Comparison between current cross-border payment models and Arf’s improved model (from: Arf)

Arf (@arf_one): The world’s first regulated, transparent short-term liquidity solution designed to support cross-border payments. Based in Switzerland, Arf eliminates the capital-intensive business model in cross-border payments by providing licensed money service businesses and financial institutions with digital asset-based working capital and settlement services, along with local on/off-ramp capabilities. Arf offers a unified liquidity network for cross-border payments and trade, removing the need for prefunding and delivering 24x7 transparent, compliant services. To date, Arf’s on-chain transaction volume has surpassed $1.6 billion with zero defaults, making it one of the fastest-growing stablecoin use cases.

2. Supply Chain Finance

Supply chain finance combines financial services with supply chain management, offering systematic financial products and services based on trade relationships and transactions within the supply chain. Traditional supply chain finance suffers from complex contracts, legal procedures, difficulty in automation, and slow financing cycles—all severely impacting SMEs’ ability to raise capital. PayFi drastically streamlines processes such as accounts receivable factoring, alleviating corporate financing difficulties.

Global enterprises lose $2.5 trillion annually in trade financing due to limitations of traditional financial institutions (from: Isle Finance)

Isle Finance (@isle_finance): The first project offering an RWA PayFi network for supply chain payments, bringing instant Web3 liquidity into supply chain finance and offering competitive yields backed by A-grade quality to liquidity providers. Through Isle, supply chain payments are combined with blockchain’s real-time settlement and liquidity management, enabling participants to process payments and settlements faster and improve capital efficiency. Meanwhile, on-chain liquidity providers can anchor themselves to the payment stability of high-credit buyers and share in early-payment discounts offered by suppliers. Isle’s primary clients include high-net-worth individuals (HNWIs), crypto-native users, DAO treasuries, asset managers, and family offices. Ordinary users can also stake ISLE tokens to earn liquidity mining rewards.

3. Consumer Finance

PayFi面向 consumers may be the most engaging aspect for end users, primarily occurring in consumer finance—a point Lily Liu emphasized during her PayFi presentation: “Buy Now, Pay Never.” Users can cover current expenses by committing future income, with enforcement handled automatically by on-chain smart contracts. In consumer finance, the key is for merchant network service providers to act as intermediaries accepting these obligations, enabling consumers to access diverse spending scenarios.

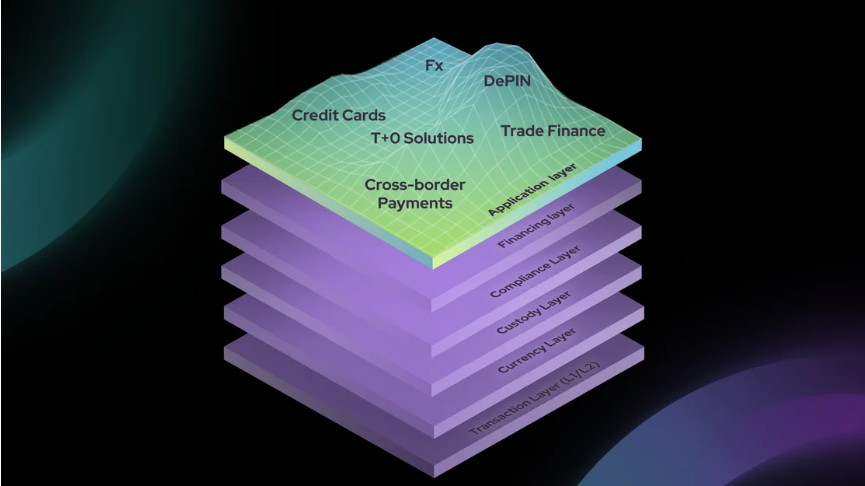

Open stack of Huma Finance’s compliant PayFi financing solution (from: Huma Finance)

Huma Finance (@humafinance): A pioneer in proposing the PayFi Stack—an open-stack framework for building compliant payment financing solutions—and advocating for industry leaders to optimize offerings to meet PayFi’s unique needs. The initial stack includes layers: Transaction, Currency, Custody, Financing, Compliance, and Application. For instance, the financing layer includes credit scoring, underwriting, and RWAs oracles. As a representative of the financing layer, Huma focuses on short-term financing common in payments. As of August 26, 2024, Huma’s total financed payment volume exceeded $280 million with a 0% default rate (single口径).

CrediPay (@Credix_finance): Offers seamless, risk-free credit services that help businesses increase sales and improve cash flow efficiency. Sellers offer buyers flexible payment terms at attractive prices and receive upfront payments. CrediPay manages and protects clients from credit and fraud risks, allowing them to focus solely on what matters most: increasing sales and profitability. Currently, Credix’s services are focused on Latin America, particularly invoice factoring.

Opportunities and Challenges Facing PayFi

1. Market Growth Potential

PayFi’s core goal is to bring the time value of money on-chain and reconstruct the financial system in a more programmable, self-custodial, and decentralized manner. With the rapid increase in global stablecoin issuance and continuous improvements in crypto infrastructure, PayFi is poised to become a transformative force in traditional finance.

According to Statista, the total value of global digital payments is expected to reach approximately $9.46 trillion in 2023, projected to grow to $14 trillion by 2027. Meanwhile, Mordor Intelligence reports that the DeFi market was valued at $46.61 billion in 2024 and is expected to reach $78.47 billion by 2029, representing a CAGR of 10.98%.

CGV Research estimates that if PayFi captures just 10% of global digital payment transaction volume (a conservative assumption), by 2030, the PayFi market (projected at $1.8 trillion) would be 20 times larger than the DeFi market ($87 billion). This indicates immense market potential for PayFi, positioning it to play a major role in the global digital payments landscape.

2. Regulatory and Compliance Challenges

As global stablecoin issuance grows, central banks’ attitudes toward stablecoins are gradually softening. Broadly speaking, fiat-backed stablecoins can be seen as digital extensions of traditional currencies. Since PayFi primarily uses stablecoins as its payment medium, it remains subject to regulation within sovereign monetary frameworks.

On one hand, current PayFi projects emphasize compliance, typically allowing only licensed institutions to participate, while individual users must undergo strict KYC procedures. On the other hand, many PayFi initiatives target developing countries where regulations are often less developed, resulting in fewer regulatory barriers and relatively lower compliance risks.

3. Technological and Security Risks

After years of DeFi development, although security issues haven’t been completely eliminated, most vulnerabilities have been identified. After rigorous audits, the security level of on-chain PayFi is now roughly equivalent to that of traditional DeFi.

However, technical challenges mainly exist off-chain. Because PayFi requires extensive integration with real-world assets, ensuring the enforceability of off-chain logic remains an unresolved issue. Current solutions usually involve intermediary entities to align on-chain and off-chain data, but this approach still requires further refinement.

Conclusion

PayFi, as the new wave of payment finance, is reshaping the global financial ecosystem with its unique appeal. It not only inherits Bitcoin’s original payment vision but also elevates the efficiency and inclusiveness of financial services to new heights through blockchain innovation. With the support of high-performance blockchains like Solana, PayFi’s market scale is poised for exponential growth, becoming a primary driver in future financial markets.

As Lily Liu foresaw, PayFi tightly integrates RWA and DeFi, forming an integrated value chain and giving rise to a new financial cluster. This revolutionary innovation will propel the global financial system toward a more efficient and inclusive future.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News