Arthur Hayes' new article: Fed rate cuts and yen strength will send Bitcoin "To The Moon"

TechFlow Selected TechFlow Selected

Arthur Hayes' new article: Fed rate cuts and yen strength will send Bitcoin "To The Moon"

At the final stage of the third quarter, statutory liquidity conditions were as favorable as could be.

Author: Arthur Hayes

Translation: TechFlow

(The views expressed here are those of the author alone and should not be taken as investment advice, nor should they be interpreted as a recommendation to engage in any trading activity.)

I ended my Northern Hemisphere summer break by heading south for two weeks of skiing. Most of my time was spent on backcountry ski touring. For those unfamiliar with this activity, it involves attaching climbing skins to the bottom of your skis so you can ascend slopes. Once at the top, you remove the skins, switch your boots and skis into downhill mode, and enjoy deep, powdery snow. Much of the mountain I visited is accessible only via this method.

A typical four- to five-hour ski day consists of 80% uphill climbing and 20% downhill skiing. As such, the physical demands are intense. Your body burns calories to maintain core temperature and homeostasis. The legs—the largest muscle group—are constantly engaged, whether ascending or descending. With a base metabolic rate of around 3,000 kcal, combined with the energy required for leg movement, my total daily energy expenditure exceeds 4,000 kcal.

Given the immense energy required, the composition of food I consume throughout the day is critical. I start with a hearty breakfast of carbohydrates, meat, and vegetables—what I call "real food." This keeps me full initially, but as I enter cold forests and begin the first ascent, these initial energy stores deplete quickly. To manage blood glucose levels, I carry snacks I normally avoid—much like how Su Zhu and Kylie Davies evade BVI court-appointed liquidators. Every 30 minutes, I eat a Snickers bar and syrup, even if I'm not hungry. I don’t want my blood sugar to drop and impair performance.

Consuming sugary processed foods isn't a sustainable long-term solution for meeting my energy needs. I also require "real food." After completing each loop, I typically stop for a few minutes, open my backpack, and eat meals I’ve prepared myself—usually stored in containers: chicken or beef, stir-fried leafy greens, and plenty of white rice.

I pair periodic sugar spikes with sustained intake of clean, long-burning real food to maintain performance throughout the day.

I describe this pre-ski meal planning to introduce a discussion on the relative importance of price versus quantity in money. To me, the price of money is like eating Snickers and syrup—delivering a rapid glucose boost. The quantity of money, however, is like slow-burning, enduring “real food.” At last Friday’s Jackson Hole central banking conference, Powell announced a policy shift: the Federal Reserve (Fed) has finally committed to lowering policy rates. Additionally, officials from the Bank of England (BOE) and European Central Bank (ECB) signaled they will continue cutting policy rates.

Powell made this announcement around 9 AM GMT-6, corresponding to the red oval. Risk assets—represented by the S&P 500 index (white), gold (yellow), and Bitcoin (green)—rose as the price of money declined. The dollar (not shown) weakened over the weekend as well.

The market’s initial positive reaction is logical: investors believe that cheaper money should lift asset prices denominated in fixed-supply fiat currencies. I agree—but we’re forgetting that the anticipated future rate cuts by the Fed, BOE, and ECB will shrink the interest rate differential between their currencies and the yen. Yen carry trades will become risky again and could disrupt this rally unless central banks expand their balance sheets—i.e., print more money—to increase the quantity of money.

Please read my article Spirited Away for an in-depth discussion of this yen carry trade phenomenon, which I will reference frequently in this piece.

The USD/JPY strengthened by 1.44%, yet immediately dropped after Powell’s announcement. This was expected, as narrowing interest rate differentials result from lower U.S. rates and stable or rising Japanese rates.

The remainder of this article aims to explore this dynamic further and examine key developments in the coming months leading up to the U.S. election, when indifferent voters will choose between Trump or Biden.

Bull Case Premise

As observed this August, a rapidly appreciating yen spells danger for global financial markets. If major economies’ rate cuts cause the yen to appreciate against their domestic currencies, we should expect negative market reactions. We face a clash between positive forces (rate cuts) and negative ones (yen appreciation). Given that globally, yen-funded financial assets exceed tens of trillions of dollars, I believe the negative impact of a sharply strengthening yen on carry trades will outweigh any benefits from minor rate cuts in the dollar, pound, or euro. Moreover, I suspect policymakers at the Fed, BOE, and ECB understand they must be willing to ease policy and expand balance sheets to offset the adverse effects of yen appreciation.

In line with my skiing analogy, the Fed is trying to grab a “sugar high” from rate cuts before hunger sets in. From an economic standpoint, the Fed should be raising rates—not cutting them.

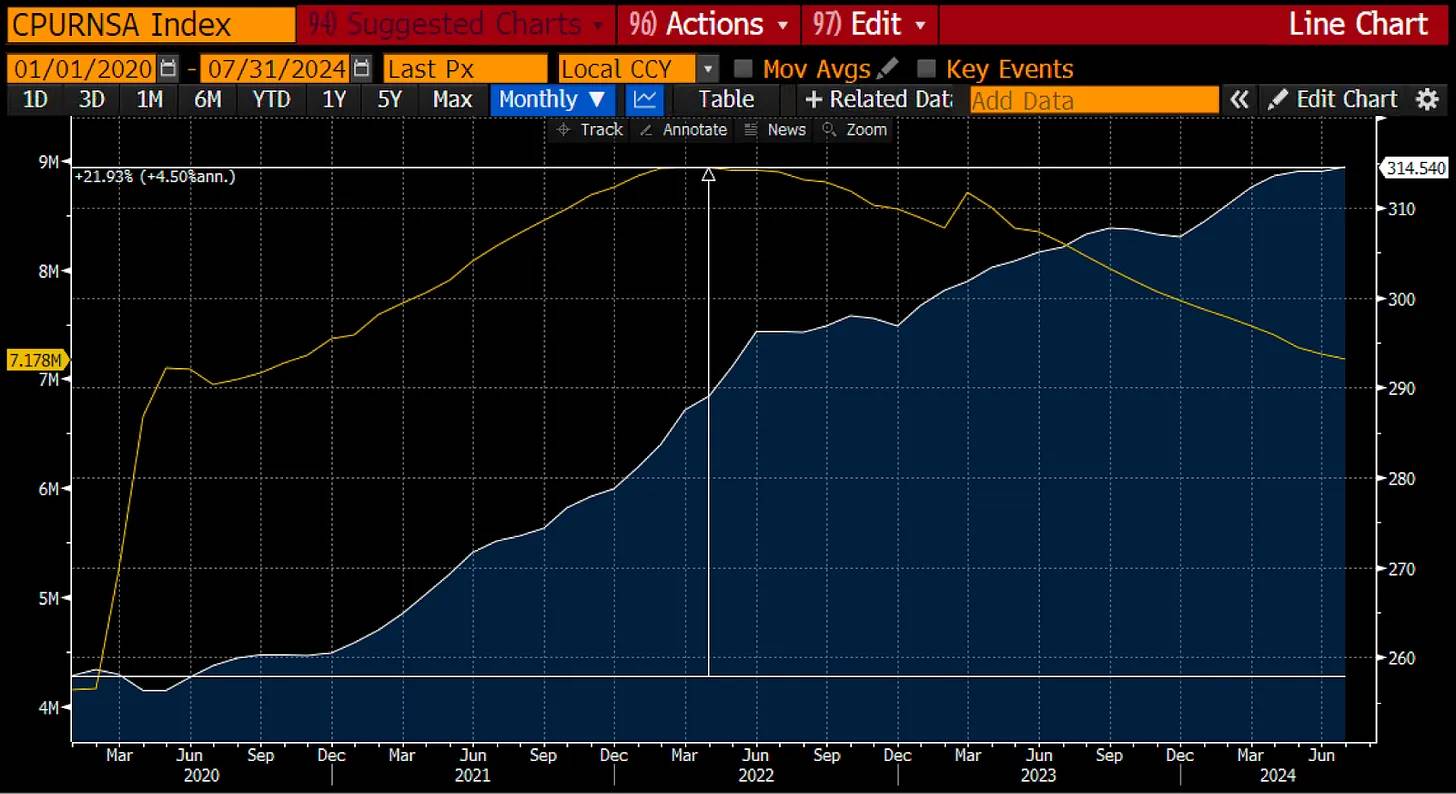

Since 2020, the manipulated U.S. Consumer Price Index (white) has risen 22%. The Fed’s balance sheet (yellow) has grown by over $3 trillion.

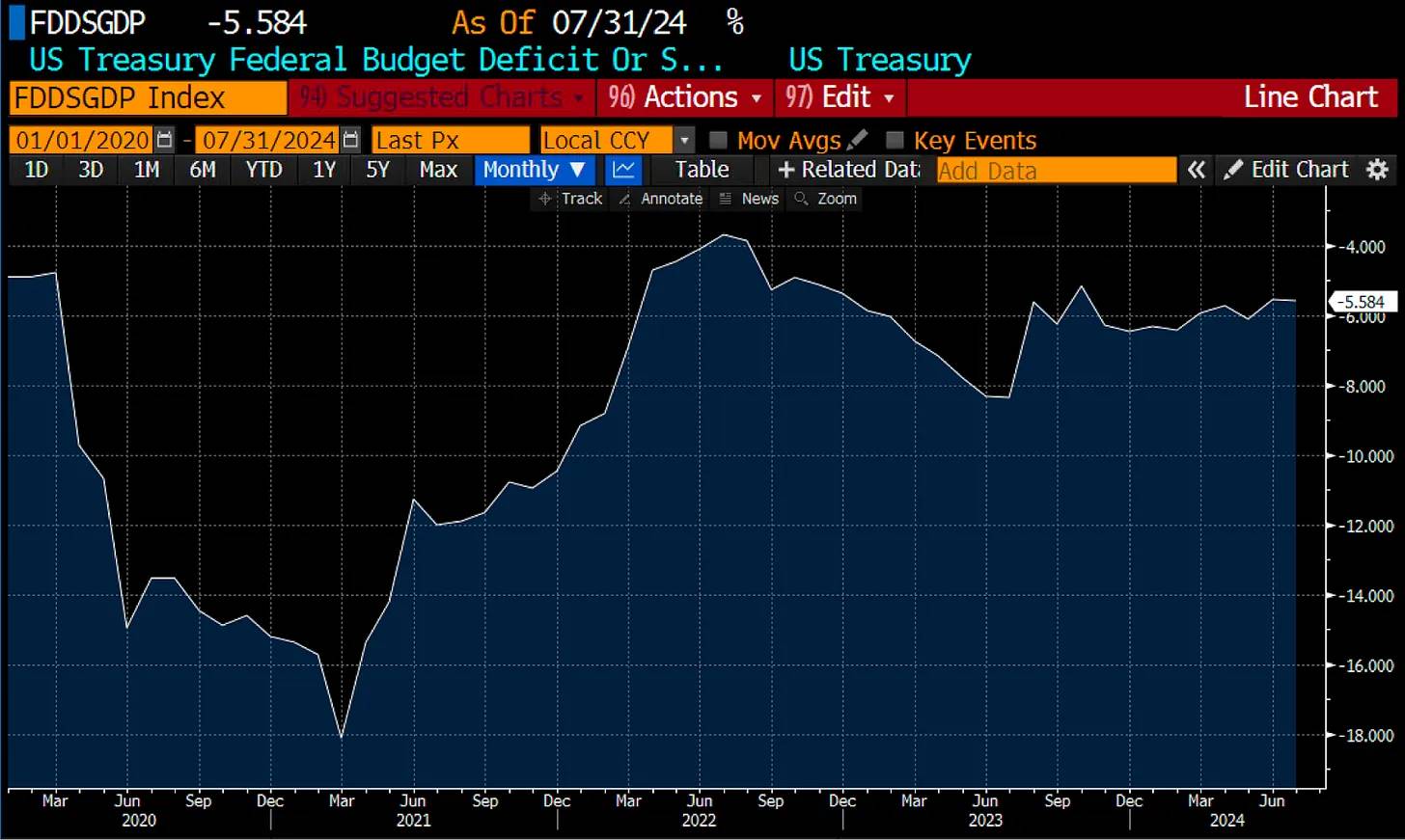

U.S. government deficits have reached record levels, partly because debt issuance costs haven’t risen enough to force politicians to raise taxes or cut subsidies to balance the budget.

If the Fed truly wanted to uphold confidence in the dollar, it should raise rates to cool economic activity. This would reduce prices across the board, though some would lose jobs. It would also restrain government borrowing, as higher debt costs would act as a constraint.

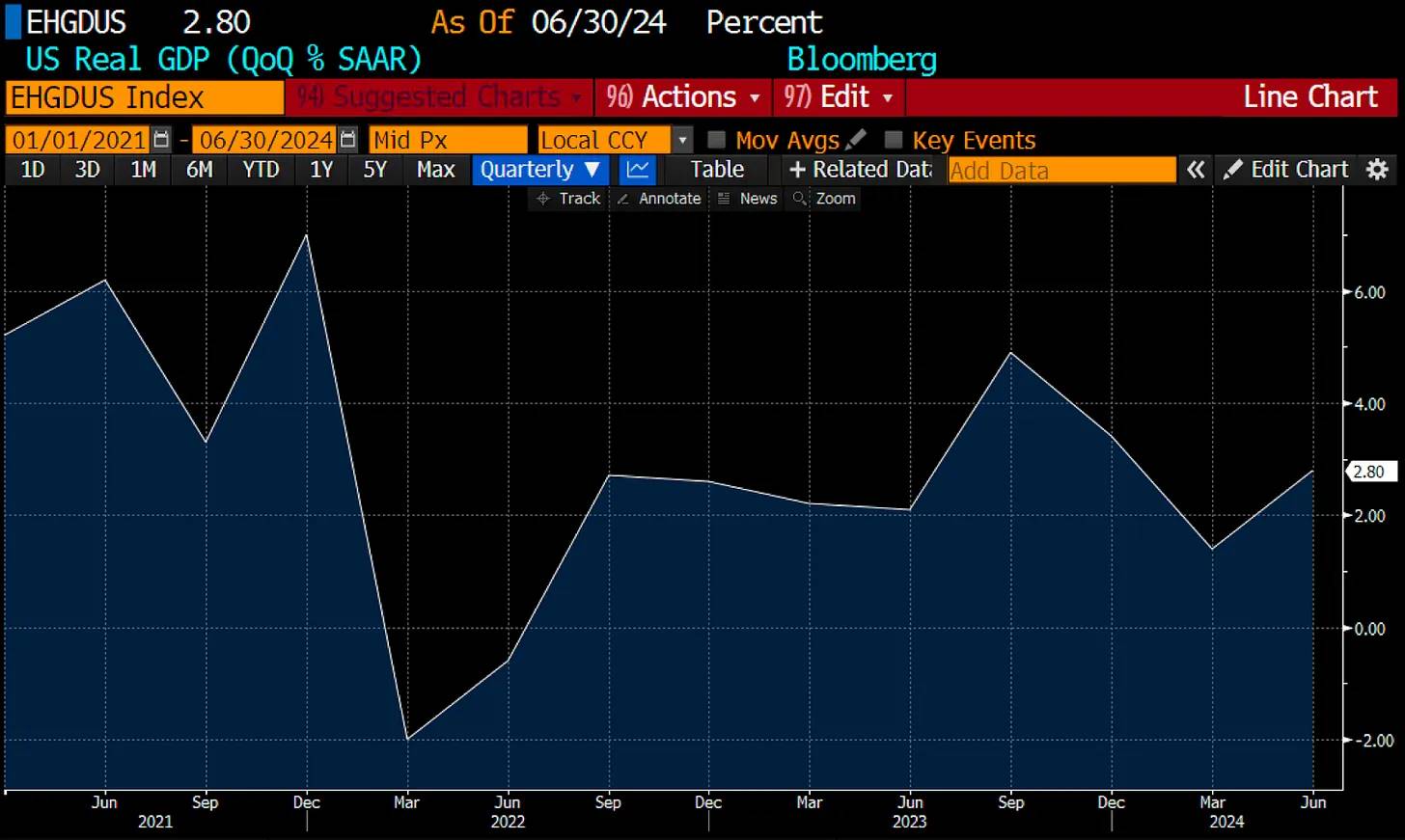

The U.S. economy has experienced only two quarters of negative real GDP growth since COVID—a sign this isn’t a weak economy in need of rate cuts.

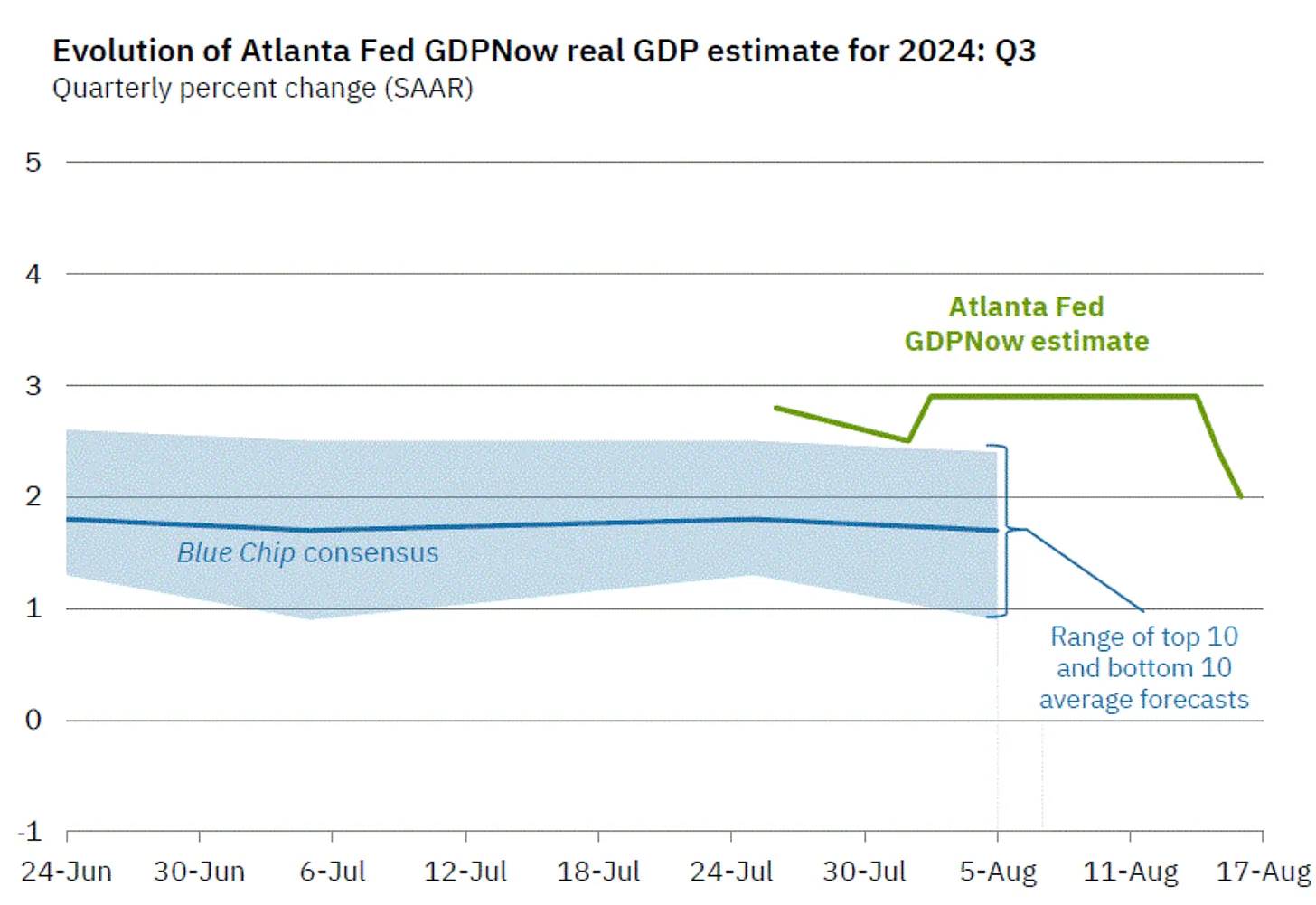

Even recent estimates for Q3 2024 real GDP stand at +2.0%. Again, this does not reflect an economy crushed by overly restrictive rates.

Just as I eat candy and syrup even when not hungry to prevent low blood sugar, the Fed pledges never to let financial markets stall. The U.S. is a highly financialized economy that requires continuously rising fiat asset prices to make citizens feel wealthy. In reality, stocks may be flat or declining, but most people ignore real returns. Nominal stock gains increase capital gains tax revenue in fiat terms. In short, market declines are harmful to the financial health of Pax Americana. Thus, Yellen began interfering with the Fed’s rate-hiking cycle in September 2022. I believe Powell, under pressure from Yellen and Democratic leaders, is sacrificing his integrity by cutting rates despite knowing he shouldn’t.

I include the chart below to illustrate what happened when the U.S. Treasury, under Yellen, began issuing large volumes of Treasury bills (T-bills), pulling funds out of the Fed’s Reverse Repo Program (RRP) and injecting them into broader financial markets.

To understand the above paragraph, please refer to my article Water, Water, Every Where.

All prices indexed to 100 on September 30, 2022—the peak of the RRP at approximately $2.5 trillion. The RRP (green) has declined 87%. The S&P 500 (gold) has delivered a nominal fiat-dollar return of +57%. I argue that the Treasury Department holds more power than the Fed. While the Fed raised the price of money until March 2023, the Treasury found ways to simultaneously increase the quantity of money. The result: a nominal stock market boom. When priced in gold—the oldest form of real money (as opposed to credit-based fiat)—the S&P 500 (white) rose only 4%. When priced in Bitcoin—the emerging hardest form of money—the S&P 500 (magenta) fell 52%.

The U.S. economy doesn’t need rate cuts, but Powell will deliver the sugar rush anyway. Because monetary authorities are extremely sensitive to any decline in fiat stock prices, Powell and Yellen will soon provide some form of “real food”—expanding the Fed’s balance sheet—to counteract the impact of yen appreciation.

Before discussing yen appreciation further, I want to briefly address Powell’s flimsy justification for rate cuts—and how this strengthens my conviction in rising risk asset prices.

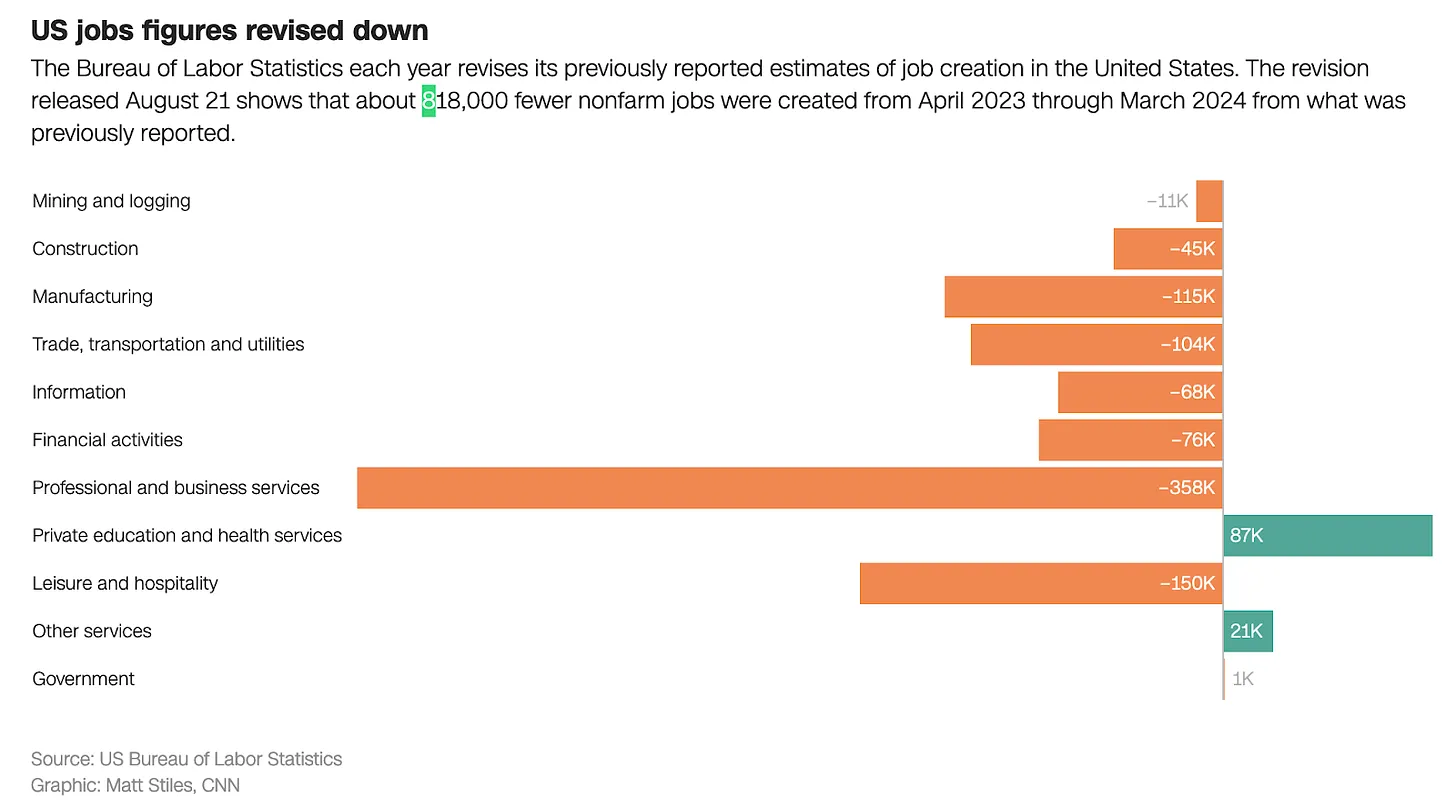

Powell based his pivot on a weak jobs report. Just days before Powell’s Jackson Hole speech, President Biden’s Bureau of Labor Statistics (BLS) released a shocking revision to prior employment data, revealing an overestimation of about 800,000 jobs.

Biden and his dishonest economist allies have long claimed labor market strength under his administration. This supposed strength put Powell in a bind: senior Democratic senators like Elizabeth “Pocahontas” Warren were calling for rate cuts to stimulate the economy and help prevent Trump’s re-election. Powell was trapped. He couldn’t cut rates due to inflation above the Fed’s 2% target. Nor could he justify cuts based on labor market weakness. But let’s sprinkle some political obfuscation and see if we can bail out our “beta cuck towel bitch boy.”

Biden performed like a medicated vegetable during his debate with Trump and was subsequently abandoned by the Obamas. Kamala Harris now takes his place, and if mainstream media narratives are to be believed, she bears no responsibility for any policies enacted during the past four years of the Biden/Harris administration. Thus, the BLS can admit its error without tarnishing Harris, since she ostensibly played no real role in the government she nominally led as Vice President. A truly magical political sleight of hand.

Powell could have used this moment to blame soft labor data for rate cuts—but he didn’t. Now he announces the Fed will begin cutting rates in September, with the only question being the size of the first cut.

When politics overrides economics, I grow more confident in my forecasts. Because Newtonian Political Physics applies: politicians in power want to stay in power. They will do whatever it takes, regardless of economic conditions, to secure re-election. This means that, come what may, the incumbent Democrats will deploy all available monetary tools to keep equities rising ahead of the November election. The economy will not lack cheap and abundant fiat liquidity.

Impact of Yen Volatility

Currency exchange rates are primarily driven by interest rate differentials and expectations of future changes in those differentials.

The chart above compares USD/JPY (yellow) with the U.S.-Japan interest rate differential (white), calculated as the Fed’s effective federal funds rate minus the Bank of Japan’s overnight deposit rate. When USD/JPY rises, the yen depreciates and the dollar appreciates; when it falls, the opposite occurs. As the Fed began tightening in March 2022, the yen depreciated sharply. By July this year, yen depreciation peaked as the rate differential hit its widest point.

After the Bank of Japan raised its policy rate from 0.10% to 0.25% at the end of July, the yen rebounded strongly. The BOJ clearly signaled that further hikes could come at some future date. Markets struggle to predict exactly when. Like unstable snowpack, it's impossible to know which snowflake or ski turn will trigger an avalanche. A 0.15% reduction in the rate differential should have been insignificant—but it wasn’t. The yen’s strong rebound began, and markets are now hyper-focused on the future path of the U.S.-yen rate spread. As expected, following Powell’s policy shift and the anticipation of further narrowing spreads, the yen gained strong support.

This is the previous USD/JPY chart. I emphasize again: the yen received strong support immediately after Powell confirmed September rate cuts.

If traders unwind their USD/JPY carry trade positions amid a surging yen, the short-term stimulus from Fed rate cuts could vanish quickly. Further rate cuts to prevent broader financial market declines would only accelerate the narrowing of the U.S.-yen rate differential, further strengthening the yen and prompting more position unwinds. Markets need “real food”—in the form of printed money via an expanding Fed balance sheet—to halt the bleeding.

If yen appreciation accelerates, the first step won’t be a return to Quantitative Easing (QE). Instead, the Fed will reinvest proceeds from maturing bonds into U.S. Treasuries and mortgage-backed securities. This would signal a halt to its Quantitative Tightening (QT) program.

If the pain persists, the Fed might resort to central bank liquidity swaps and/or restart QE to print money. In this scenario, Yellen would boost dollar liquidity by issuing more Treasuries and reducing the Treasury General Account balance. Neither of these market operators will openly admit that ending the yen carry trade poses systemic risks requiring aggressive money printing. Acknowledging that foreign dynamics affect this “land of the free and home of the brave” contradicts American values!

If the USD/JPY exchange rate drops rapidly below 140, I believe they will not hesitate to deliver the “real food” that fiat financial markets demand.

Trade Setup

Toward the end of Q3, fiat liquidity conditions couldn’t be better. As crypto holders, we have the following tailwinds:

1. Global central banks, especially the Fed, are lowering funding costs. The Fed is cutting rates even while inflation remains above target and the U.S. economy continues growing. The Bank of England (BOE) and European Central Bank (ECB) may deliver further cuts at upcoming meetings.

2. Bad girl Yellen has pledged to issue $271 billion in Treasury bills by year-end and conduct $30 billion in buyback operations—injecting $301 billion in liquidity into financial markets.

3. The U.S. Treasury still holds approximately $740 billion in its general account, funds that can and will be deployed to stimulate markets and help elect Harris.

4. The Bank of Japan became extremely concerned about the speed of yen appreciation after its July 31, 2024 meeting, when it raised rates by 0.15%. Consequently, it publicly stated that future hikes will consider market conditions. This is a veiled way of saying, “We won’t hike if we think markets will fall.”

I’m part of the crypto tribe; I don’t follow stocks. So I don’t know if equities will rise. Some point to historical examples where stocks fell during Fed rate-cutting cycles. Others worry that Fed rate cuts signal recession in the U.S. and developed markets. That may be true—but consider what the Fed is doing now: cutting rates despite above-target inflation and strong economic growth. They will ramp up money printing and significantly increase the money supply. This will fuel inflation, which may hurt certain businesses. But for finite-supply assets like Bitcoin, it will send Bitcoin “to the moon.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News