Consensys Sued as U.S. SEC Takes Aim at Staking Again

TechFlow Selected TechFlow Selected

Consensys Sued as U.S. SEC Takes Aim at Staking Again

The SEC alleges that Consensys, through its digital asset wallet MetaMask, "engaged in the issuance and sale of securities."

Author: Mary Liu, Bitpush News

Regulatory headwinds have been relentless lately. On June 28 local time, the U.S. Securities and Exchange Commission (SEC) filed a lawsuit against Consensys at the Brooklyn Federal Court in New York—less than two weeks after the SEC notified Consensys that it had concluded its investigation into Ethereum 2.0.

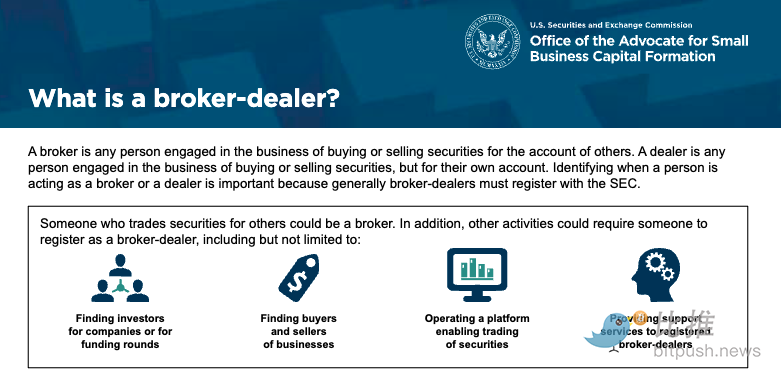

Unregistered as a Broker-Dealer

The SEC alleges that the company engaged in "the issuance and sale of securities" through its digital asset wallet MetaMask, acting as an "unregistered broker-dealer," and claims Consensys earned more than $250 million in fees.

According to the SEC, Consensys "positions itself as a venue for buying and selling crypto assets (including crypto asset securities), recommends trades with the 'best' value (as Consensys itself states), accepts investor orders, routes investor orders, handles customer assets, executes transaction parameters and instructions on behalf of clients, and receives transaction-based compensation."

Court documents state: "Consensys failed to register as a broker-dealer and failed to register certain securities offerings and sales, violating federal securities laws."

Targeting Staking

Regulators claim that Consensys sold thousands of unregistered securities through staking service providers Lido and Rocket Pool, which issued liquid staking tokens known as stETH and rETH in exchange for staked assets.

The agency stated that investors provide ETH to Lido and Rocket Pool, which then pool these ETH and stake them on the blockchain to generate returns that individual investors might not otherwise achieve.

"After receiving investors’ ETH, Lido and Rocket Pool issue a new crypto asset—stETH or rETH respectively—representing the investor’s proportional interest in the staking pool and its rewards," the SEC said. It added that Lido and Rocket Pool offer and sell investment contracts that meet the definition of securities.

The SEC also claimed that Consensys itself "facilitated transactions in crypto asset securities," listing MATIC, MANA, CHZ, SAND, and LUNA as securities—tokens previously classified as such in past enforcement actions.

Court filings state: "From their initial offering or sale onward, these crypto asset securities were offered and sold on the Consensys platform and continue to constitute investment contracts, thus qualifying as securities."

Data from DeFiLlama shows that Lido and Rocket Pool are the two largest liquid staking protocols on Ethereum, collectively holding $37.6 billion in staked TVL. After the news broke, native protocol tokens dropped sharply, with LDO plunging 12% within 30 minutes.

This is not the first time the SEC has sued a staking service provider. In February, cryptocurrency exchange Kraken settled with the SEC for $30 million and subsequently shut down its staking services for U.S. customers. Another major industry player, Coinbase, has been challenging the SEC's stance in court, arguing that staking does not constitute a securities offering.

Are the Allegations Legally Sound?

Nick Almond, CEO of Factory Labs, said the SEC’s argument that open-source crypto wallets should be forced to register as broker-dealers is flawed.

"To me, it comes down to custody—the degree to which users maintain sovereign control over their assets. If they have no custody at all, then it's not a broker-dealer," he said. Traditionally, a broker-dealer acts on behalf of others in securities transactions.

For example, according to the SEC’s official definition, a "broker-dealer is any person engaged in the business of effecting transactions in securities for the account of others." However, MetaMask’s Swap service is essentially a "bot" controlled by users who want to execute their own trades.

This view aligns with the interpretation of U.S. District Judge Katherine Failla, who on March 27 dismissed similar SEC allegations against Coinbase Wallet in this case. The judge ruled that since it is a self-custodial wallet and users retain control of their funds, neither Coinbase nor Coinbase Wallet qualifies as a broker.

Jorge Izquierdo, founder of Tuyo, noted that Consensys and MetaMask fall into the same category. He wrote on X that there is no difference between providing non-custodial smart contract support and "offering a UI for any random swap." The only distinction, he said, is that Consensys charges fees for facilitating swap services.

The same logic applies to the allegations regarding MetaMask’s staking services, which act as a so-called "intermediary" between users and decentralized protocols like Lido and Rocket Pool—though in reality, no true intermediary exists. Almond described staking services more accurately as a "UI interface."

"The idea of equating a UI frontend to a bank or something similar is kind of silly," Almond said, "because anyone can interact directly with the smart contracts, even running the frontend locally."

In other words, as long as Ethereum continues to operate, MetaMask is merely one way to access protocols that will exist indefinitely.

This year, the SEC has issued Wells notices, filed lawsuits, or reached settlements with several crypto firms focused on Ethereum and DeFi, including ShapeShift, TradeStation, and Uniswap. Bloomberg reported that the agency is also investigating the Ethereum Foundation.

In response to the new lawsuit, Consensys stated: "We firmly believe the SEC has not been granted the authority to regulate software interfaces like MetaMask, and we will continue vigorously pursuing rulings on these issues in Texas—not just because it matters for our company, but because it matters for the future success of web3."

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News