What taxes apply to mining in Nigeria? A study on cryptocurrency taxation in Nigeria

TechFlow Selected TechFlow Selected

What taxes apply to mining in Nigeria? A study on cryptocurrency taxation in Nigeria

Recently, the Nigerian government has shown a more relaxed attitude toward cryptocurrencies.

By TaxDAO

As of 2023, Nigeria is the world's second-largest user of Bitcoin, with 22 million cryptocurrency holders—10% of its total population. According to Chainalysis’ 2022 Global Cryptocurrency Adoption Index, Nigeria ranked 11th globally and 17th in peer-to-peer (P2P) exchange transaction volume.

In June 2021, the Nigerian government banned cryptocurrency mining, citing its high electricity consumption at a time when power supply in Nigeria remains constrained. Additionally, authorities expressed concerns that crypto mining might destabilize the domestic currency. However, recently the government has softened its stance, lifting the ban on crypto trading in December 2023—an action likely to benefit the development of cryptocurrency mining.

1. Cryptocurrency Mining

1.1 Conditions for Cryptocurrency Mining

Early Bitcoin mining could be done using ordinary personal computers. However, as mining difficulty increased, specialized hardware known as ASICs (Application-Specific Integrated Circuits) became the dominant choice. ASIC devices are specifically designed for Bitcoin mining and offer significantly higher efficiency than general-purpose hardware. Moreover, efficient mining operations generate substantial heat, making effective cooling systems essential for maintaining stable hardware performance. In large-scale mining facilities, beyond traditional air conditioning, advanced techniques such as liquid cooling are increasingly adopted.

Bitcoin mining is an energy-intensive process. Mining equipment operates 24/7, consuming vast amounts of electricity. Electricity cost thus becomes one of the key determinants of mining profitability. Conducting mining operations in regions with lower electricity prices can substantially reduce costs and enhance profitability.

1.2 Advantages of Cryptocurrency Mining in Nigeria

1.2.1 Abundant Natural and Energy Resources

Nigeria possesses vast natural gas reserves, which serve as the primary fuel for thermal power generation. The country ranks among the top globally in terms of natural gas reserves. This abundant fuel base makes thermal power a reliable and readily available option to meet growing domestic electricity demand. Nigeria already has well-developed thermal power infrastructure, including power plants, pipelines, and gas distribution networks. This existing infrastructure supports the continued dominance of thermal power by enabling efficient fuel supply, transmission, and distribution, making both operation and expansion of thermal power plants cost-effective.

Additionally, the country has significant renewable energy potential, including solar, wind, biomass, and small hydropower (SHP). Widespread adoption of renewables would expand Nigeria’s overall power generation capacity, helping the electricity market meet rising demand.

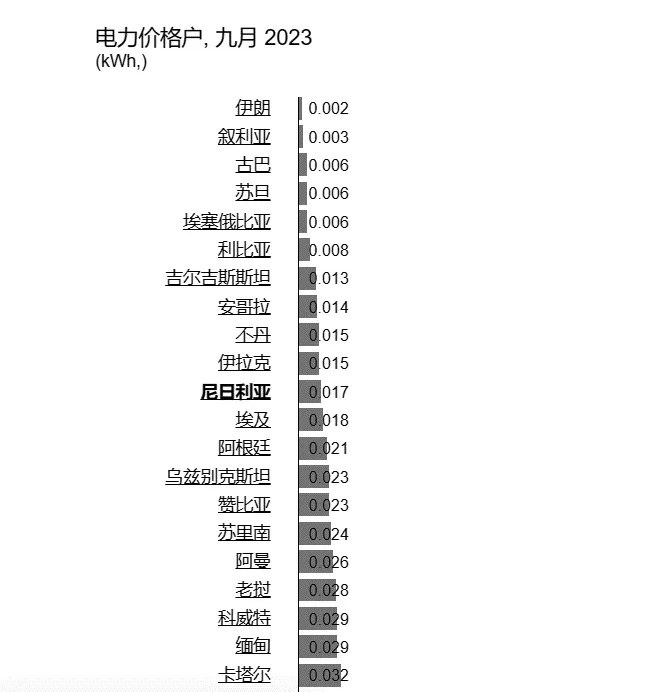

1.2.2 Relatively Low Electricity Prices

Bitcoin miners consume large quantities of electricity, with power accounting for up to 80% of operational costs. Access to cheap electricity therefore constitutes a major competitive advantage. Compared to many other countries, Nigeria offers relatively low electricity prices, as illustrated in the chart below showing electricity rates in selected countries as of September 2023.

1.2.3 Favorable Climate Conditions

Nigeria’s climate is also highly suitable for mining. The ideal temperature range for mining hardware is between 5°C and 25°C—coincidentally matching Nigeria’s average temperatures. This facilitates stable operation and efficient cooling of mining equipment.

1.2.4 Shift in Government Stance

The Central Bank of Nigeria (CBN) has recently undergone a significant shift in its position toward cryptocurrencies—from an outright ban to introducing a structured regulatory framework for virtual asset service providers. This change reflects efforts to align with global trends in blockchain and digital assets. The CBN has established strict rules for financial institutions engaging with cryptocurrency-related businesses, marking a new era in Nigeria’s digital finance landscape and a major transformation in its financial regulatory environment. As the country continues to explore this space, the CBN seeks to responsibly integrate cryptocurrencies into the financial system—a move that also benefits local cryptocurrency mining activities.

1.2.5 Potential for Mining to Alleviate Local Economic Challenges

Despite being Africa’s largest economy by GDP, Nigeria faces severe inflation issues. Foreign exchange controls limit citizens’ ability to hedge against inflation through currency conversion, prompting many to seek alternatives outside official monetary channels to preserve their wealth. The decentralized and borderless nature of cryptocurrencies meets these local needs, driving both mining activity and broader crypto adoption within the country.

2. Taxation of Cryptocurrency Mining

The tax treatment of cryptocurrency mining primarily depends on how the jurisdiction defines and classifies digital assets, as well as how mining income and expenses are recognized and measured. Depending on the country or region, different types of taxes may apply to mining revenue.

First, direct taxes—including income tax and capital gains tax on mining income. Most jurisdictions with active mining industries treat mining revenue as business or personal income, subjecting it to corporate or individual income tax. Tax rates vary based on the miner’s status (individual or entity), income level, residency, and other factors.

Second, indirect taxes—such as value-added tax (VAT) or goods and services tax (GST) on mining income. There is currently no global consensus on whether mining income should be subject to VAT/GST. In the European Union, most member states consider mining activities exempt from VAT. Israel, however, treats mining as a service under its 2017 guidance on taxing virtual currency activities and imposes a 17% VAT. Similarly, New Zealand classifies mining as a taxable service and levies a 15% GST.

Some countries also impose excise taxes on mining companies due to resource allocation considerations. For example, in March 2023, the U.S. Treasury proposed a phased excise tax based on electricity consumption from cryptocurrency mining in its “Budget Supplemental Materials.” Under this proposal, companies engaged in mining would be required to report their electricity usage and source type.

3. Nigeria’s Tax System

3.1 Overview of the Tax System

Nigeria’s tax system is built upon two main categories: direct and indirect taxes. Key direct taxes include corporate income tax, personal income tax, capital gains tax, petroleum profits tax, and various miscellaneous levies. Major indirect taxes include VAT, import duties, excise duties (also called "excise taxes"), and stamp duties.

Nigeria has a relatively comprehensive legal and administrative tax framework, aligned with its three-tier governmental structure—federal, state, and local levels—each responsible for administering specific taxes.

3.2 Taxes Potentially Applicable to Cryptocurrency Mining Companies in Nigeria

3.2.1 Corporate Income Tax

Under the Companies Income Tax Act, all types of enterprises operating in Nigeria are liable for corporate income tax on their profits, except for exploration and production companies. Nigerian resident companies must pay tax on worldwide profits, while non-resident companies are taxed on certain Nigerian-sourced income. The federal government administers this tax. The standard corporate income tax rate for resident companies is 30%, assessed annually. Non-resident companies with annual Nigerian turnover exceeding 6 million Naira must pay a special tax of 15% of turnover. If turnover does not exceed 6 million Naira, they pay a flat amount of 900,000 Naira (15% of 6 million).

3.2.2 Value Added Tax (VAT)

Nigeria’s VAT applies to sales of goods or provision of (independent) services, as well as imported goods and services. Prior to February 1, 2020, the standard VAT rate was 5% on taxable supplies, including imports. From February 1, 2020 onward, the standard VAT rate was increased to 7.5%.

3.2.3 Customs Duties

Import tariffs in Nigeria are non-preferential and applied equally to all countries. Depending on the type of goods, either specific duties or ad valorem duties are imposed, payable in Naira. Special duties may be levied on imported goods deemed to be dumped or abnormally subsidized if they threaten existing or potential domestic industries.

3.2.4 Capital Gains Tax

Under Nigerian tax law, individuals or entities disposing of shares valued at 100 million Naira or more within any consecutive 12-month period must pay a 10% capital gains tax, unless the proceeds are reinvested in shares of another Nigerian company.

4. Tax Implications for Cryptocurrency Mining Enterprises in Nigeria

Following India, Nigeria has become the world’s second-largest adopter of cryptocurrencies. The country has lifted the central bank’s 2021 restrictions, allowing financial institutions to transact with firms offering digital currency services. Although regulation remains strict, this shift presents a rare opportunity for the crypto industry, attracting numerous cryptocurrency mining companies to establish operations in Nigeria—and inevitably bringing associated tax considerations.

Nigeria follows a combined territorial and residence-based taxation principle. Any enterprise earning income within Nigeria must pay income tax. Resident companies are taxed on global income, while non-residents pay tax on certain Nigerian-source income at specified rates. Mining companies operating in Nigeria must therefore pay corporate income tax on locally earned income according to applicable regulations.

Supplies such as electricity are considered goods or services subject to VAT. Given mining companies' heavy reliance on electricity, they may indirectly bear VAT costs passed down from power suppliers.

Mining operations require specialized hardware such as mining rigs. Due to limited local availability, mining companies often need to import such equipment, triggering customs duties. Cryptocurrency mining machines are generally classified as industrial machinery. Nigeria imposes import duties on machinery ranging from 5% to 15%, though some categories—such as agricultural machinery—are exempt.

New legislation mandates a 10% capital gains tax on cryptocurrency transactions. Former President Muhammadu Buhari signed the Finance Act 2023 into law, introducing a series of tax reforms aimed at modernizing Nigeria’s fiscal framework. The act specifies a 10% tax on gains from the disposal of digital assets, including cryptocurrencies. This comprehensive legislation aims to increase transparency, boost tax revenues, and stimulate economic growth. Taxing rapidly appreciating digital assets has thus become a necessary policy step. Through this measure, the Nigerian government seeks not only to create a level playing field for digital asset holders but also to ensure they contribute fairly to national development. This tax will similarly impact mining enterprises engaged in crypto production.

Regarding the timing of income recognition from mining, some argue that mined cryptocurrency represents internally developed intangible assets. Costs related to computing resources, electricity, and personnel are viewed as investments in developing these assets, meaning income or gain should only be recognized upon subsequent sale of the cryptocurrency. However, the Nigerian government has not issued clear guidelines on this matter.

Finally, there are currently no explicit regulations indicating special tax incentives for mining companies in Nigeria. However, mining enterprises may qualify for existing general tax relief programs. Therefore, mining firms should conduct prudent tax planning within the framework of available tax优惠政策.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News