EigenLayer Staking: A Potential Wealth Code or Hidden Risk?

TechFlow Selected TechFlow Selected

EigenLayer Staking: A Potential Wealth Code or Hidden Risk?

EigenLayer has demonstrated significant market potential and growth opportunities amid the restaking trend.

Author: Fishery, Core Contributor of Biteye

Editor: Crush, Core Contributor of Biteye

*Approximately 4000 words, estimated reading time: 8 minutes

Recently, EigenLayer launched the first phase of its Eigen token airdrop, generating significant market enthusiasm and positioning itself as the leading project in the restaking sector during this bull cycle.

Currently, only the staking function for Eigen is available; transfers and trading are not yet enabled. As such, whether to stake Eigen has become a highly debated topic in the market.

To help readers better understand, this article will clarify the staking mechanism of EigenLayer, potential rewards from staking, associated risks, and conclude with the author’s personal perspective on whether one should stake EIGEN.

First, it's important to note that EigenLayer’s staking mechanism differs significantly from Ethereum’s native Proof-of-Stake (PoS) system. Instead, it closely resembles the staking logic found in the Cosmos ecosystem—both in terms of user interface design and node airdrop marketing strategies. Thus, to some extent, Cosmos-based strategies can serve as useful references.

01 EigenLayer: Ethereum Restaking

Restaking refers to reusing ETH that has already been staked on the Ethereum mainnet to support the security of additional protocols. Through this method, users can earn returns not only from their original staking but also gain additional rewards by securing other applications.

Founded in 2021, EigenLayer pioneered the concept of restaking. It operates as a middleware layer between Ethereum and other decentralized applications. By deploying smart contracts on Ethereum, EigenLayer enables users to restake their ETH and liquid staking tokens (LSTs) derived from ETH.

Since its launch in June 2023, EigenLayer has experienced rapid growth, amassing over $10 billion in total value staked (TVS), making it one of the largest blockchain protocols by TVS—surpassing major DeFi platforms such as Aave, Rocket Pool, and Uniswap.

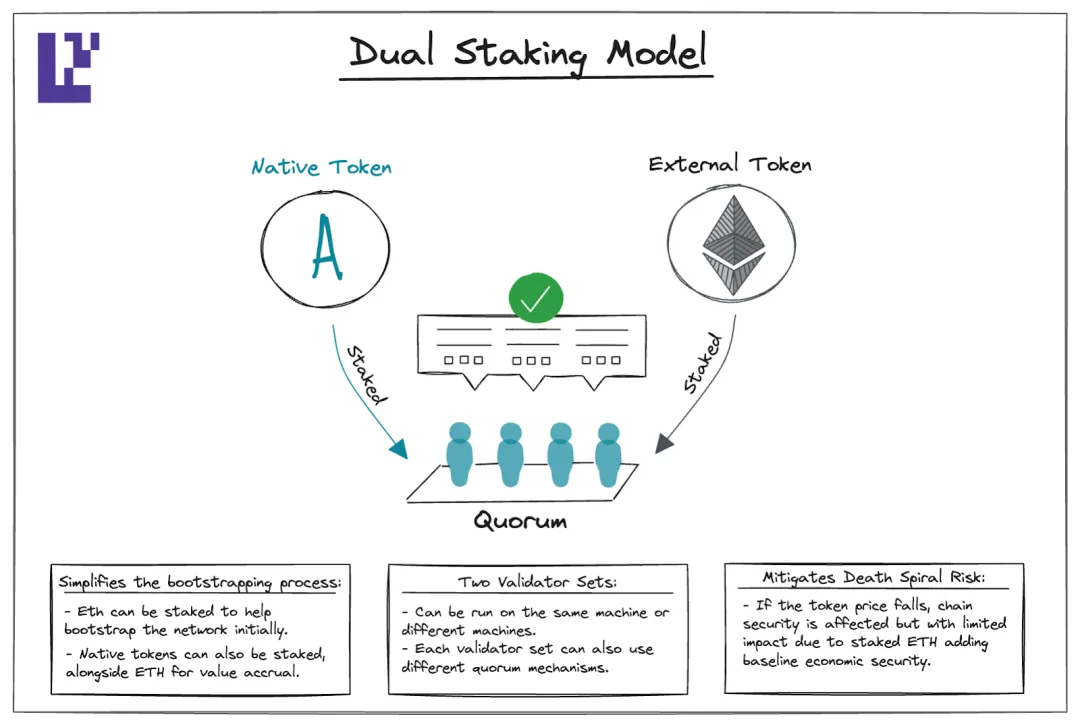

Dual Staking

With the introduction of the $EIGEN token, EigenLayer now supports not only restaking of ETH and ETH LSTs but also direct staking of $EIGEN and future native tokens issued by AVSs (Actively Validated Services).

This marks EigenLayer’s innovative "Dual Staking" model: the combination of ETH-series token restaking and Eigen-series token staking collectively secures the network.

To understand dual staking, one must first grasp the concept of Quorum.

In EigenLayer’s context, a Quorum refers to a group of assets (either restaked or directly staked) used by an AVS to leverage shared security.

Operators (nodes) can choose to join one or more token quorums based on the composition of staked assets and the design of specific AVSs.

According to official documentation, AVS teams have full control over defining the parameters and asset composition within a Quorum. These settings are dynamic and can be adjusted post-launch to adapt to changing market conditions.

The innovation of dual staking mitigates a key vulnerability in traditional PoS networks—where excessive inflation of native tokens undermines network security. By incorporating stable external assets like ETH, dual staking provides sustained economic backing, enhancing overall network security and stability.

Once network stability is achieved, projects may gradually shift the staking ratio toward greater reliance on native tokens, increasing autonomy and independence.

While dual staking enhances risk resilience and offers richer economic tooling for protocol teams, it also introduces new challenges and risks.

Firstly, this mechanism somewhat diminishes the sovereignty of project-specific tokens, potentially weakening their utility and value proposition. Additional token incentives may be required to offset these drawbacks.

Additionally, increased flexibility in staking mechanisms may lead to centralization risks—particularly if quorum modification decisions lack transparency or broad community participation.

Moreover, within the same dual staking framework, there is differential treatment between native EIGEN tokens and ETH-series tokens regarding unstaking periods.

EigenLayer’s mainnet contract imposes a 7-day withdrawal delay for LSTs and ETH restaking, whereas EIGEN tokens face a much longer 24-day withdrawal window.

The team justifies this disparity by stating that EIGEN will eventually unlock unique functionalities requiring extended lock-up periods. However, what specific features justify a threefold longer unlocking time remains unclear.

Setting such prolonged unlock times without transparent reasoning undoubtedly poses substantial risks to EIGEN stakers.

In summary, while dual staking brings notable economic advantages and high flexibility for teams, retail participants must exercise caution, carefully evaluating risks—especially around opaque protocol parameter changes and withdrawal mechanisms—with particular attention to centralization risks.

02 EigenDA

EigenDA is a data availability solution developed by EigenLabs and built atop the EigenLayer platform. It has been live on the mainnet since Q2 2024.

Given that EigenLayer’s documentation lacks detailed explanations of AVS staking parameters, EigenDA—as the first deployed AVS—offers valuable insights into how future AVSs might configure their staking rules.

The number of active operator nodes on both the mainnet and Holesky testnet is capped at 200. According to the documentation, this limit stems from the current cost of bridging EigenDA’s proof of availability back to Ethereum L1. As technology improves and costs decrease, this cap may be lifted.

There are minimum staking requirements for operators:

Operators joining the ETH quorum must stake at least 96 ETH, while those joining the EIGEN quorum need only 1 EIGEN.

Compared to newly launched PoS chains, EigenDA’s node count is relatively small—on par with Cosmos-based networks—and includes an explicit upper limit.

In contrast, other prominent PoS blockchains do not impose hard caps on node numbers, instead relying on minimum staking thresholds. For example, Solana and Avalanche each have over 1,700 nodes, while Ethereum has more than one million validators.

By imposing limits on both asset holdings and total node count, EigenDA creates a highly restrictive environment. Under such strict conditions, it's unsurprising that eligible nodes fall short of the 200-node cap—in fact, only 147 active nodes currently exist.

Of course, node count alone does not fully determine network security—it serves merely as a point of reference for comparison.

When the operator cap is reached, any new entrant must possess a group weight exceeding the lowest-weight current operator by at least 1.1x to displace them.

Here lies a critical challenge—one of the core problems restaking aims to solve:

Traditional PoS chains can easily verify the state of native assets within nodes and autonomously update validator sets according to protocol rules. EigenLayer, however, cannot directly access real-time data about restaked assets locked on the Ethereum mainnet.

Therefore, a secure and decentralized method is needed to prove that top-ranked nodes meet eligibility criteria.

If this verification process fails to be decentralized, malicious actors could illegitimately replace legitimate nodes and compromise EL consensus.

The difficulty lies in the impracticality of using on-chain smart contracts alone—sorting or maintaining priority queues on-chain incurs prohibitively high computational costs and complexity.

To address this, EigenLayer adopts a hybrid approach combining off-chain Churn Approvers with on-chain smart contract validation.

When the operator cap is reached and a new node wishes to join, they must request a signature from an off-chain "Churn Approver." The approver verifies whether the applicant meets financial requirements and issues a signature accordingly. This signature, along with the change request, is then submitted to the EigenDA smart contract on Ethereum.

While this off-chain signing mechanism offers operational convenience and flexibility, it introduces non-trivial centralization risks.

The off-chain approval process could be compromised due to improper operator behavior or system vulnerabilities, undermining the network’s decentralization and security guarantees.

Furthermore, the documentation does not address the risk of Churn Approvers going offline. If off-chain validators fail to respond to new node registration requests, EigenDA cannot rotate its validator set per protocol rules—meaning faulty or outdated validators remain active, posing serious security threats.

Hence, any component relying on off-chain mechanisms warrants close scrutiny from users.

03 The Missing Slash & Reward Mechanism and Staking Strategy

The slash and reward mechanism is fundamental to all PoS networks. However, due to EigenLayer’s rushed launch, these functions are not yet implemented.

Rewards are fairly straightforward—users earn APR yields plus anticipated airdrops. Penalties (slashing), however, are more complex. If an operator fails its duties—such as experiencing downtime or engaging in double-signing—the funds delegated to that node may be partially slashed, and its APR emissions may be suspended.

Note: EigenLayer has not yet published detailed specifications. The above explanation is inferred from standard practices in other PoS systems.

In the author’s view, this omission is highly problematic. Users began participating in restaking before these rules were defined, meaning most are unaware of slashing risks. Should their chosen node later misbehave or fail, users could lose funds unexpectedly.

From a capital safety standpoint, restakers should diversify across multiple operators. This way, even if slashing occurs, only a portion of funds would be affected.

However, EigenLayer’s current incentive structure favors concentration—staking with well-known nodes offering积分-based airdrop programs maximizes expected returns. Unfortunately, this behavior contradicts the principle of decentralization.

04 Conclusion

Restaking, as an emerging technology, is attracting growing attention across the blockchain industry. Notably, reports from March 15 revealed that Lido’s co-founders and Paradigm are secretly funding a new project called Symbiotic to enter the restaking space—further validating this trend.

Despite its vast potential, the technical challenges facing EigenLayer, as discussed in this article, cannot be overlooked—especially given that restaking has not yet been formally integrated into Ethereum’s EIP standards.

Currently, proposals for how Ethereum mainnet should verify EigenLayer validator exits remain unresolved, introducing uncertainty. Technical immaturity increases the risk of participation, particularly concerning potential slashing events.

At present, EigenLayer appears to prioritize economic incentives over technical robustness. If underlying technical issues are resolved, economically optimized designs are likely to yield strong returns.

Overall, EigenLayer demonstrates immense market potential and growth prospects within the restaking wave. While facing short-term technical and standardization hurdles, these are likely stepping stones rather than insurmountable barriers.

As these challenges are progressively addressed, we have reason to believe that EigenLayer will not only accelerate innovation but also achieve its long-term economic objectives.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News