The other side of AI tokens: Most projects focus on financial gains rather than real-world impact

TechFlow Selected TechFlow Selected

The other side of AI tokens: Most projects focus on financial gains rather than real-world impact

The naive idea of "token incentives + market trends" prevails here.

Author: Gagra

Translation: TechFlow

Executive Summary

-

This is not another optimistic VC-style article about the "AI + Web3" space. We are optimistic about the convergence of these two technologies, but this piece is a call to action—otherwise, that optimism will ultimately become unjustified.

-

Why? Because developing and running state-of-the-art AI models requires massive capital expenditures on cutting-edge, often hard-to-access hardware, plus domain-specific R&D. Simply crowdsourcing via crypto incentives—as most Web3 AI projects attempt—is insufficient to counterbalance the tens of billions invested by dominant corporations firmly in control of AI development. Given hardware constraints, this may be the first major software paradigm where brilliant and creative engineers outside incumbent organizations lack the resources to disrupt it.

-

Software’s ability to “eat the world” is accelerating rapidly and will soon grow exponentially with AI. In the current landscape, all of this value flows to tech giants, making end users—including governments, large enterprises, and consumers—increasingly dependent on their power.

Misaligned Incentives

All of this unfolds at perhaps the worst possible moment—when 90% of decentralized network participants are busy chasing easy, narrative-driven gains. Yes, developers are following investors into our industry, not the other way around. Motivations range from overt admissions to more subtle subconscious drivers, but narratives shaped around them drive much of Web3 decision-making. Participants are too immersed in reflexive bubbles to notice the outside world, except when it serves to further fuel the cycle. And AI is clearly the biggest such narrative, as it itself is undergoing a boom.

We’ve spoken with dozens of teams at the intersection of AI and crypto and can confirm many are highly capable, mission-driven, and passionate builders. But human nature being what it is, when faced with temptation, we tend to give in—and then rationalize those choices afterward.

Easy access to liquidity has long been crypto’s historical curse—one that has slowed its progress and delayed meaningful adoption by years. It even tempts the most loyal crypto believers toward “hype tokens.” The justification? More capital in token holders’ hands might give builders a better chance.

The relatively low maturity of institutional and retail capital gives builders room to make unrealistic claims while still benefiting from valuations as if those claims were already true. The result is moral hazard and capital destruction—few such strategies prove sustainable long-term. Necessity is the mother of invention, and when necessity disappears, so does invention.

The timing couldn’t be worse. While the world’s brightest tech entrepreneurs, national leaders, and businesses big and small race to secure benefits from the AI revolution, crypto founders and investors are choosing “growth at all costs.” In our view, that’s the real opportunity cost.

Web3 AI Market Overview

Given these incentives, Web3 AI projects effectively fall into three categories:

-

Legitimate (split between realists and idealists)

-

Semi-legitimate

-

Fraudsters

Fundamentally, we believe builders clearly understand what it takes to keep pace with their Web2 rivals and which verticals offer realistic competition versus those bordering on delusion—though the latter can still be pitched to VCs and unsophisticated public markets.

The goal must be to compete now. Otherwise, the pace of AI advancement may leave Web3 behind, pushing the world toward a dystopian Web4 dominated by Western corporate AI and Chinese state AI. Those who remain uncompetitive and rely on distributed tech to catch up over longer timeframes are overly optimistic to the point of unseriousness.

Obviously, this is a very rough categorization—even the “fraudster” group includes several serious teams (though perhaps more delusional ones). But this article is a call to arms, so objectivity isn’t our goal; we want readers to feel urgency.

Legitimate

Middleware for “bringing AI on-chain.” Founders behind these solutions—though few in number—recognize that decentralized training or inference for user-desired models is currently infeasible, if not impossible. Thus, connecting top-tier centralized models to on-chain environments to benefit from complex automation is seen as a sufficient first step. Currently, hardware enclaves (TEEs—“trusted execution environments”), bidirectional oracles (for indexing data both on and off-chain), and verifiable off-chain compute environments for agents appear optimal. Some co-processor architectures using zero-knowledge proofs (ZKPs) to verify snapshot state changes—not full computation—are also viable in the medium term.

A more idealistic approach aims to verify off-chain inference so it aligns with on-chain computation in terms of trust assumptions. Our view: the goal should be enabling AI to execute both on-chain and off-chain tasks within a single coherent runtime. However, many proponents of inference verifiability talk about vague objectives like “trusting model weights,” which won’t matter for years, if ever. Recently, founders in this camp have begun exploring alternative inference verification methods, though most initially rely on ZKPs. While many smart teams are working on so-called ZKML, they risk betting too heavily on cryptographic optimizations outpacing AI model complexity and computational demands. Therefore, we see them as currently unfit for competition. That said, recent advances are intriguing and shouldn’t be ignored.

Semi-legitimate

Consumer apps using wrappers for closed and open-source models (e.g., Stable Diffusion or Midjourney for image generation). Some of these teams were early movers and have real users. So, calling them all fraudulent would be unfair—but only a few are deeply thinking through how to decentralize their base models or innovate in incentive design. There are interesting variations in governance and ownership here. But most projects in this category simply add a token atop centralized wrappers like the OpenAI API to gain valuation premiums or faster liquidity for their teams.

Neither of these camps addresses the core challenge: training and inference for large models in decentralized environments. Currently, there’s no way to train foundation models within reasonable timeframes without tightly coupled hardware clusters. Given the level of competition, “reasonable time” is a critical factor.

Recently, promising research suggests methods like differential dataflow could theoretically scale across distributed computing networks, increasing future capacity as network capabilities match evolving dataflow requirements. Yet competitive model training still requires communication between localized clusters (not individual distributed devices) and cutting-edge compute power (retail GPUs are increasingly non-competitive).

Progress has also been made on research to localize inference (one of two paths to decentralization) by reducing model size, but no existing Web3 protocols leverage this yet.

The unresolved problems of decentralized training and inference logically lead us to the third and most important camp—the one that emotionally triggers us the most.

Fraudsters

Infrastructure applications focused on decentralized servers, offering bare-metal hardware or decentralized model training/hosting environments. Some software infrastructure projects promote protocols for federated learning (decentralized model training) or combine software and hardware into unified platforms where users can train and deploy decentralized models end-to-end. Most lack the sophistication needed to solve the stated problems—naive ideas like “token incentives + market trends” dominate here. Solutions we see in public and private markets cannot achieve meaningful competitiveness today. Some may evolve into viable (but niche) products, but what we need now are fresh, competitive alternatives. These can only emerge through innovative designs that overcome distributed computing bottlenecks. In training, it’s not just speed—it’s also verifiability of completed work and coordination of training workloads, which introduces bandwidth constraints.

We need a set of competitive, truly decentralized foundation models that require decentralized training and inference to function. If computers become intelligent while AI remains centralized, there will be no “world computer” to speak of—only some dystopian variant.

Training and inference are at the heart of AI innovation. As the rest of the AI world moves toward tighter integration, Web3 needs orthogonal solutions to compete—because direct competition is becoming less feasible.

Scale of the Problem

It all comes down to compute. Whether during training or inference, the more you invest, the better the results. Yes, there are tweaks and optimizations, and compute itself isn’t homogeneous—new approaches exist to bypass bottlenecks in traditional von Neumann architecture processors—but ultimately, it boils down to how many matrix multiplications you can perform on how large memory blocks and how fast.

That’s why we see so-called “hyperscalers” aggressively building data centers, each aiming to create a full-stack stack with powerful AI processors at the top and supporting hardware below: OpenAI (models) + Microsoft (compute), Anthropic (models) + AWS (compute), Google (both), and Meta (expanding data centers to play in both). There are more nuances, dynamics, and players involved, but we won’t dive deeper here. The overall picture is clear: hyperscalers are investing unprecedented tens of billions in data center expansions, creating synergies between their compute and AI offerings, expecting massive returns as AI permeates the global economy.

Let’s look at just the expected expansion levels this year from these four companies:

-

Meta expects $30–37 billion in capital expenditures for 2024, heavily weighted toward data centers.

-

Microsoft spent ~$11.5 billion in capex in 2023 and is rumored to invest $40–50 billion in 2024–2025! This is partially evident from massive announced data center investments in several countries: $3.2B in the UK, $3.5B in Australia, $2.1B in Spain, €3.2B in Germany, $1B in Georgia (USA), and $10B in Wisconsin. These are just regional investments within their network of 300 data centers across 60+ locations. Rumors suggest Microsoft may spend an additional $100B to build a supercomputer for OpenAI!

-

Amazon’s leadership forecasts a significant increase in capex in 2024, after spending $48B in 2023, primarily due to AWS infrastructure expansion for AI.

-

Google spent $11B in Q4 2023 alone expanding servers and data centers. They admit these investments aim to meet anticipated AI demand and expect infrastructure spending to accelerate significantly in 2024 due to AI.

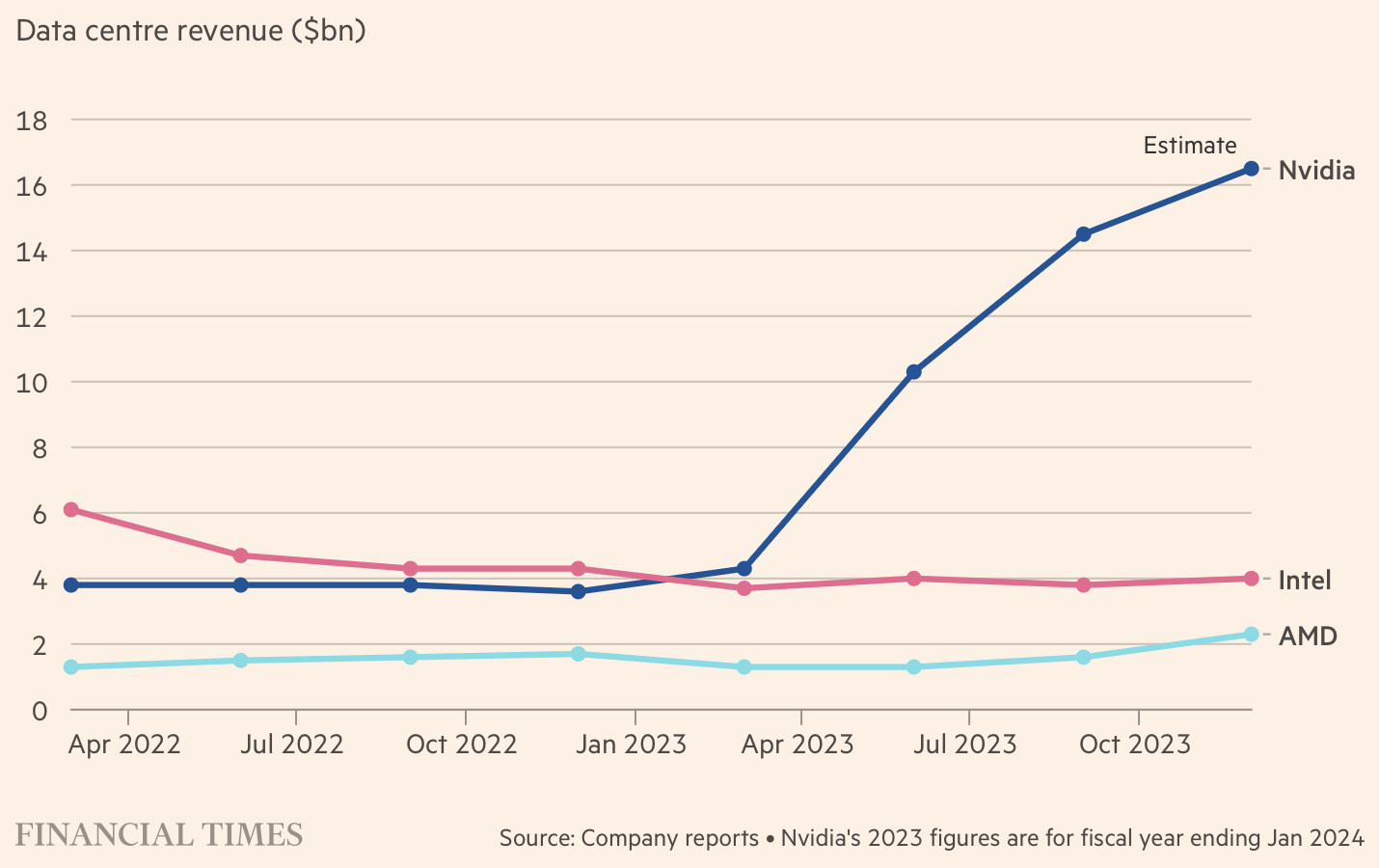

Here’s how much NVIDIA has already spent on AI hardware in 2023:

NVIDIA CEO Jensen Huang has been promoting a forecast of $1 trillion going into AI acceleration over the next few years. He recently doubled that estimate to $2 trillion, reportedly due to growing interest from sovereign actors. Analysts at Altimeter project global AI-related data center spending to reach $160B in 2024 and over $200B in 2025.

Now compare these figures with what Web3 offers independent data center operators in incentives to expand capital expenditures on the latest AI hardware:

-

The total market cap of all decentralized physical infrastructure (DePIn) projects is currently around $40B—relatively illiquid and largely speculative tokens. In essence, these networks’ market caps represent an upper-bound estimate of total capital expenditures contributors could make, incentivized by tokens. Yet current market caps are mostly irrelevant since they’re already issued.

-

Let’s assume another $80B (twice current value) in private and public DePIn token market caps enters the market over the next 3–5 years, fully dedicated to AI use cases.

Even if we spread this rough estimate over three years and compare its dollar value to cash spent by hyperscalers in just 2024, it’s clear that applying token incentives to a series of “decentralized GPU networks” is insufficient.

Investors would also need tens of billions in demand to absorb these tokens, as network operators sell large quantities of mined coins to cover capital expenses. Even more billions would be needed to inflate token values and incentivize growth beyond hyperscaler capabilities.

Yet, anyone familiar with how most Web3 servers currently operate might expect much of “decentralized physical infrastructure” to actually run on hyperscalers’ cloud services. Of course, surging demand for GPUs and other AI-specialized hardware is driving increased supply, which should eventually make cloud leasing or purchasing cheaper. At least, that’s the expectation.

But consider this: NVIDIA now prioritizes latest-gen GPU allocations for select customers. Meanwhile, NVIDIA is beginning to compete directly with major cloud providers by offering AI platform services to enterprise clients already locked into hyperscale infrastructures. This may eventually push it to either build its own data centers (eroding their current high-margin profits—unlikely) or severely restrict sales of its AI hardware outside its partner cloud provider network.

Additionally, NVIDIA’s competitors are launching extra AI-specific hardware, mostly using the same chips produced by TSMC as NVIDIA. So essentially, all AI hardware firms are currently competing for TSMC’s production capacity. TSMC must prioritize certain customers. Samsung and potentially Intel (trying to re-enter advanced chip manufacturing) may absorb some excess demand, but TSMC currently produces most AI-related chips, and scaling and calibrating cutting-edge fabrication (3nm and 2nm) takes years.

Above all, nearly all cutting-edge chip manufacturing happens at TSMC in Taiwan and Samsung in Korea—near the Taiwan Strait. Before offsetting facilities under construction in the U.S. come online (and aren’t expected to produce next-gen chips for years), geopolitical conflict risks could become real.

Finally, due to U.S. restrictions on NVIDIA and TSMC, China is largely cut off from the latest AI hardware generations. China is now scrambling for remaining compute capacity—just like Web3 DePIn networks. Unlike Web3, however, Chinese firms actually have competitive models, especially large language models (LLMs) from companies like Baidu and Alibaba, which require vast amounts of previous-generation equipment to run.

Therefore, due to one or more of the above factors, there’s a non-trivial risk that hyperscale cloud providers may restrict external access to their AI hardware amid intensifying AI dominance wars. Essentially, they could reserve all AI-related cloud capacity for internal use, stop offering it to others, and hoard all the latest hardware. Once that happens, remaining compute supply will face higher demand from other major players—including sovereign nations. Meanwhile, consumer-grade GPUs grow increasingly non-competitive.

Clearly, this is an extreme scenario—but the stakes are so high for major players that they won’t back down even if hardware bottlenecks persist. In such a case, decentralized operators like secondary data centers and retail hardware owners—who make up most Web3 DePIn providers—would be excluded from competition entirely.

The Other Side of the Coin

While crypto founders remain unaware, AI giants are closely watching crypto. Government pressure and competition may force them to adopt crypto to avoid shutdowns or strict regulation.

Stability AI’s founder recently stepped down to begin “decentralizing” his company—one of the earliest public signals. He previously openly stated plans to launch a token after a successful IPO, hinting at genuine underlying motivations.

Similarly, while Sam Altman isn’t operationally involved in Worldcoin—the crypto project he co-founded—its token trades as a proxy for OpenAI. Whether there’s a path linking free internet money initiatives with AI R&D remains to be seen, but the Worldcoin team seems aware the market is testing this hypothesis.

To us, it makes sense that AI giants may explore various decentralization paths. The problem is, Web3 hasn’t proposed meaningful solutions. “Governance tokens” are largely a joke—only tokens that explicitly avoid direct links between asset holders and network development/operations, like $BTC and $ETH, are truly decentralized today.

The same misincentives slowing technical progress also hinder the evolution of different designs for managing crypto networks. Startup teams simply slap a “governance token” onto their product, hoping a solution emerges, only to get stuck allocating resources around “governance theater.”

Conclusion

The AI race is on, and everyone is taking it seriously. We don’t see cracks in Big Tech’s logic: more compute means better AI, better AI means lower costs, new revenue streams, and expanded market share. To us, this validates the current bubble—but all frauds will still be flushed out during inevitable corrections.

Centralized corporate AI dominates the field, and legitimate startups struggle to keep up. Web3 entered late but is now joining the race. Markets reward crypto AI projects too generously compared to their Web2 counterparts, shifting founders’ focus from product delivery to pushing token valuations at critical moments—rapidly closing the window to catch up. So far, no orthogonal innovations have emerged that bypass the need for scaled compute to compete.

There’s now a credible open-source movement around consumer-facing models, initially driven by some centralized players choosing to compete for market share against larger closed-source rivals (e.g., Meta, Stability AI). Now communities are catching up and pressuring leading AI firms. This pressure will continue to affect closed-source AI development but won’t be decisive unless open-source closes the gap. This presents another major opportunity for Web3—if it solves decentralized model training and inference.

Thus, despite surface-level opportunities for “classic” disruptors, reality is far from it. AI is fundamentally about compute, and unless breakthrough innovations emerge within the next 3–5 years, this won’t change—a key determinant of who controls and directs AI’s evolution.

Even if demand drives supply-side efforts, the compute market itself cannot “bloom freely,” as competition among manufacturers is constrained by structural factors like chip fabrication and economies of scale.

We remain optimistic about human ingenuity and believe enough brilliant and principled individuals exist to tackle the AI domain in ways that favor the free world over top-down corporate or government control. But the odds look grim—this is at best a speculative game, and Web3 founders are too busy chasing financial gains over real-world impact.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News