How is liquid staking developing on Solana?

TechFlow Selected TechFlow Selected

How is liquid staking developing on Solana?

Solana liquid staking turns held tokens into liquid assets, enabling efficient utilization and higher returns through the Sanctum platform and DeFi applications.

Written by: Algo Rhythmic

Translation: Baihua Blockchain

My goal is to provide a comprehensive introduction to liquid staking on Solana. I want you not only to understand what liquid staking is and how to do it, but also why one would do it—what makes someone wake up in the morning and say, "Today I'm going to stake my SOL." Come on, join me—I'll take you into a whole new world.

I've also tried to structure this rather long article so that you can skip certain sections if you're already familiar with the topic.

Note: This article is for educational purposes only, not investment advice.

1. Staking on Solana

Before we dive into liquid staking, let’s first understand regular staking. On delegated proof-of-stake (PoS) networks like Solana, staking means delegating your tokens to a validator who must faithfully verify transactions on the network or face penalties. This creates a fundamental alignment between validators and network users; without it, double-spending, censorship, and various abuses could occur. When you stake “natively,” you choose a specific validator and delegate your tokens to them. You can do this through various wallet software or using the Solana command-line interface.

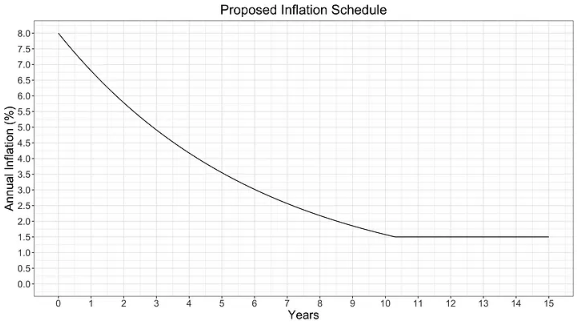

Since the launch of Solana's mainnet beta in February 2020, Solana has followed this proposed inflation schedule:

It’s now February 2024 as I write this—four years since that launch—so it's easy to see that the current inflation rate is approximately 5%. The exact inflation amount is controlled by three parameters: initial inflation rate (8%), decay rate (-15%), and long-term inflation rate (1.5%). Inflation starts at 8% and decreases annually by 15% at each epoch boundary until it stabilizes at 1.5%. This might change in the future, but it's been the observed plan since launch.

Who receives the newly minted SOL from inflation? Simply put: stakers. This means that every epoch, stakers increase their relative ownership of the total SOL supply at the expense of non-stakers. Nothing more complicated happens. If all SOL were staked, no one would gain additional value. As a result, Solana has a high staking ratio; at the time of writing, about two-thirds of all SOL is staked. However, the proportion of liquid staking remains relatively low.

For PoW blockchains, validators incur high equipment and energy costs, forcing them to sell some (or possibly all) of the tokens they earn just to break even. On PoS networks like Ethereum, these costs are very low, resulting in almost no selling pressure. On Solana, validator operating costs are slightly higher than on Ethereum because validators must execute transactions as part of consensus, which incurs costs, and validator hardware requires higher performance than Ethereum, leading to higher expenses. Thus, compared to Bitcoin, selling pressure from validators remains very low, but slightly higher than on Ethereum.

Commentary: I feel that the claim "Solana's cheap transactions are artificially subsidized by token inflation" has become a bloody slander against Solana. CT learned something about inflation from Bitcoin and now can't forget it. There is no forced buying or selling pressure.

Now let’s move on to liquid staking.

2. LSTs (Liquid Staked Tokens) and Duration Risk

There are strong incentives on Solana to stake, to avoid being diluted by other stakers. One of the few reasons not to stake is that it locks up your capital for each epoch. With liquid staking, you contribute your tokens to a staking pool that manages validator delegation and tokenize the fact that your tokens have been committed to the pool. This gives stakers a new asset representing that commitment, which users can exchange for their original staked SOL. Therefore, in many cases, it can function as a functional equivalent of SOL.

The most popular liquid staking tokens on Solana (commonly referred to as LSTs) are almost all “reward-bearing” tokens. Nearly all SOL within the pool is delegated to validators chosen by the pool operator (sometimes minus a small buffer for fast redemptions), so these delegated SOL accumulate rewards in the form of additional SOL. As a result, the quantity of LST increases over time, but each LST represents an increasing amount of SOL per epoch, causing its price relative to SOL to rise. Another method, called “rebasing,” involves distributing additional liquid tokens to holders, where each token can be redeemed 1:1 (with delay) for underlying SOL—but this approach is uncommon on Solana.

On Solana, each epoch lasts about 2.5 days. If a user wants to reclaim their original staked SOL, they must submit an undelegation request and wait until the end of the epoch before redemption. In traditional finance, this is known as taking duration risk. You’re betting that the reward from locking capital for 2.5 days will outweigh the risk of needing it immediately. In terms of duration, 2.5-day risk is much smaller than that of a 10-year U.S. Treasury bond. On the other hand, overall, U.S. Treasuries are less volatile than cryptocurrencies.

Therefore, when LST holders want to retrieve the underlying SOL, they can either redeem it from the staking pool controlled by the liquid staking protocol—waiting until the end of the epoch for the underlying pool to undelegate—or trade mSOL for SOL on the open market via existing liquidity pools. Here’s an example from Marinade Finance:

Marinade uses Jupiter’s decentralized exchange aggregator to trade mSOL for SOL. I ran some checks and found that undelegating 10,000 mSOL would impact the price by 0.01%, but when increasing to 100,000 mSOL, the displayed price impact jumps to 10% (in reality, I don’t have that much mSOL, but simulated). What does this mean?

It means that if you want to undelegate and get SOL immediately, you’ll receive 8.162% less SOL than if you waited for the epoch to end and then undelegated. This price impact is determined by current market conditions—specifically, available liquidity. Rechecking later may show different numbers. This highlights an important fact about LSTs. As I mentioned earlier, they can serve as functional equivalents of SOL in many contexts, but one key difference remains: you bear some degree of duration risk. If you urgently need funds and require a large amount, you’ll have to accept a lower price to obtain them.

A simple example helps illustrate this. Consider the “mSOL depeg” event on December 12, 2023. Within just 20 minutes, a single wallet address (85b5jKkgSuopF3MUA9s4zsBhRANrererBLRx689PqTPA) swapped approximately 68,536 mSOL for SOL across nine trades on the open market. This caused mSOL’s price to drop from around $78 to $66. Below is data from birdeye.so:

You can see the price quickly recovered to its previous level. Why? Because arbitrage bots and other speculators noticed the opportunity and started buying mSOL—they didn’t need the funds in the next epoch. The underlying SOL price hadn’t truly changed, so they were essentially buying discounted SOL.

This isn’t limited to mSOL—it applies to every LST (with some additional nuances we’ll explore later). Any specific LST will inevitably have lower liquidity than SOL itself. However, this mainly matters if you hold a large amount of liquid-staked SOL. Generally speaking, having more capital also means facing greater challenges.

So the lesson here is that while liquid staking tokens carry duration risks similar to regular staked SOL, these risks only become apparent when market liquidity is insufficient. The stronger the LST market liquidity, the smaller the impact of duration risk. If your position is relatively small, you may not feel this risk at all. Nonetheless, understanding token liquidity limits remains critically important.

3. LST Leaders and Their Incentive Structures

There are three LSTs on Solana with total value locked exceeding $100 million, highlighting different adoption incentive strategies: Jito (jitoSOL), Marinade (mSOL), and BlazeStake (bSOL). This could certainly change, but here are the approximate figures:

https://defillama.com/protocols/Liquid%20Staking/Solana

Currently, Jito leads, so we’ll start there.

1) Jito’s Value Proposition

The Jito protocol invites stakers to participate in MEV (Maximal Extractable Value) earning on Solana and offers rewards in the form of jitoSOL. jitoSOL is implemented through a secure SPL Stake Pool with optimized validator set and MEV distribution. The protocol supports efficient transaction processing via the Jito-Solana client and holds a significant position in Solana DeFi. Using jitoSOL allows access to points within the growing Solana ecosystem and provides competitive yields and performance, offering users a unique staking experience.

However, a real differentiator is MEV. Briefly, MEV allows traders to extract value from transaction ordering, but Solana’s design makes MEV harder to capture. Jito modifies Solana Labs’ validator software to enable validators to accept ordered transactions and charge fees, creating a more orderly and accessible MEV market. Delegating SOL to Jito’s liquid staking pool grants access to a share of these profits. Other LSTs can also benefit by delegating to validators running Jito-modified software.

2) Marinade’s Value Proposition

Marinade was the first liquid staking protocol on Solana and has pioneered best practices in the space. When staking directly, you must manually select a validator, but liquid staking pools automatically distribute your stake across multiple validators, reducing risk. Last month, Marinade proposed an initiative requiring validators to create an insurance fund to protect stakers’ interests. Additionally, they introduced “Directed Staking,” allowing stakers to support specific validators and earn extra incentives. Marinade’s governance is managed by MNDE tokens, which are separate from mSOL and allow holders to vote on protocol operations. They’re currently running a campaign where participants can earn additional MNDE tokens as rewards to encourage protocol engagement.

3) BlazeStake’s Value Proposition

BlazeStake’s key differentiator is tied to its BLZE governance token. Like MNDE, BLZE can be used to vote on incentive allocations, but it also carries independent value. BlazeStake is a relatively young project, so they’ve distributed only about 80% of the total token supply, whereas Marinade has fully distributed its tokens and must buy back MNDE to fund future incentives. Whether this is good or bad depends on your perspective and investment horizon. Jito also has a governance token, JTO, but it’s not yet used to incentivize staking with Jito. Let’s briefly compare the top three protocols’ governance tokens by TVL, including market cap, circulating supply, and growth trends:

Data as of February 16, 2024, sourced from Defillama, Coingecko, and Birdeye

BLZE performs well in terms of TVL-to-fully-diluted-market-cap ratio. However, several caveats exist. First, JTO’s FMDC is high due to low circulating supply, making FMDC potentially misleading in the short term. Second, only two-thirds of BLZE supply has been unlocked, meaning more tokens will enter the market. For unlock schedules, refer to: https://twitter.com/solblaze_org/status/1688480225255161856.

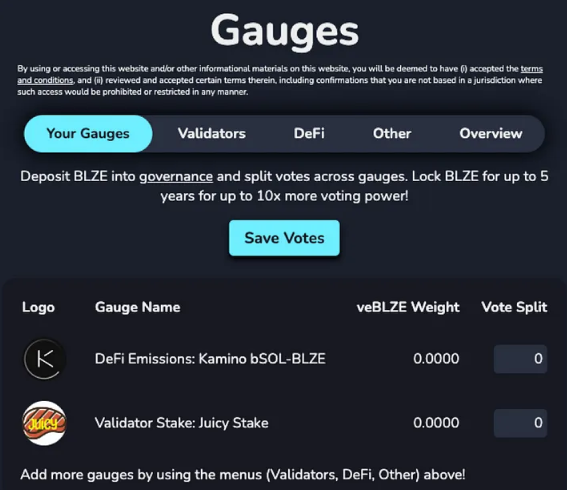

What gives BLZE value? Similar to MNDE, you can vote on governance proposals to help guide bSOL toward goals. But BlazeStake uses a mechanism called “stake gauges,” allowing finer, more continuous control. You can vote on Realms.today’s DAO to direct extra yield to specific validators or allocate more BLZE rewards to specific DeFi liquidity pools. BLZE holders can also lock their tokens for up to five years to increase voting power in the DAO. Below is a screenshot of the gauge system showing sample options after depositing into the DAO. These features are quite unique among LSTs.

Some DeFi protocols require users to claim BLZE rewards directly within their UI, with rewards airdropped biweekly. You can check your current SolBlaze score at rewards.solblaze.org. Trying to boost scores via fake wallets offers little advantage. The basic formula is: 1 bSOL in your wallet = 1 point, 1 bSOL in supported lending protocols = 1.5 points, and 1 bSOL in supported bSOL liquidity positions = 2 points. This roughly aligns with the risk taken with capital, so higher risk reasonably earns higher rewards.

Another notable feature: BlazeStake offers an option to stake your SOL with a single validator via what they call “custom liquid staking.” Unlike Marinade, 100% of the stake goes directly to that validator. Note that Marinade delegates only 20% directly to your chosen validator, with the remaining 80% distributed via their delegation strategy algorithm. Marinade documents this clearly, but it’s not immediately obvious in the UI—I find this somewhat suboptimal.

BlazeStake also offers other interesting features. They provide a real SOL faucet—if you accidentally lock all your SOL on their platform and lack enough to pay transaction fees for unlocking, you can use the faucet to get some SOL for gas. This is very convenient, eliminating the need to bring in new funds via centralized exchanges. They also offer a simple token minting UI to easily create SPL tokens, plus an RPC status page and SOL Pay SDK. All are helpful tools promoting SOL and liquid staking adoption.

If BlazeStake’s primary value comes from its governance token emissions, then BLZE’s price trajectory becomes the key driver. BLZE’s price began rising in late November 2023 and stabilized between $0.002 and $0.004, but based on the above data, there may still be significant upside. If it sustains stability like Marinade, there’s potential for nearly 2.8x growth.

In my view, BLZE’s valuation should be comparable to, or even exceed, MNDE’s. I’m unsure how to compare JTO’s valuation to the other two. I like the project—their work on MEV on Solana is fundamentally unique, and I look forward to future innovations—but nearly 90% of the token supply remains undistributed, which seems high. Still, fully diluted market cap doesn’t matter… until it does. Regardless, I believe all three projects have strong appreciation potential against the dollar, as these liquid staking protocols are creating real value. Simple argument: liquid staking is good.

To summarize this section on the three most important liquid staking protocols on Solana: they all emphasize decentralization benefits. Liquid staking pools spread stakes across a broad set of validators instead of creating winner-takes-all dynamics. They all publicly promote security. Each liquid staking protocol carries smart contract risk—the possibility of bugs in managing the staking pool—but they all demonstrate credible security awareness. These are all positive traits, but they don’t truly differentiate the three approaches, which is why I’ve focused on highlighting their unique characteristics above.

4. Sanctum and the Future of Infinite Liquid Staking

There are many other liquid staking protocols on Solana, and sanctum.so is working to dramatically increase their number through liquidity support pools. Their goal is to accept all liquid staking protocols and provide SOL swap services, making any liquid staking token highly liquid. They charge less than 0.03%, typically 0.01%, effectively absorbing duration risk for users. You can instantly exchange your liquid staking tokens for SOL, with the pool providing a buffer that spreads duration risk across a broader base.

As of now, Sanctum supports twelve different liquid staking protocols, but their aim is to solve liquidity bootstrapping for nearly all liquid staking protocols. Liquidity for liquid staking tokens currently depends on pools available on protocols like Orca and Radium, so new liquid staking protocols usually need active strategies to bootstrap liquidity and fulfill their promise. Sanctum provides a massive additional buffer, enabling new and low-market-share liquid staking protocols to achieve instant liquidity.

As of now, you can instantly exchange the following LSTs for SOL via Sanctum: bSOL, cgntSOL, daoSOL, eSOL, jitoSOL, JSOL, laineSOL, LST (Marginfi’s liquid staking token), mSOL, riskSOL, scnSOL, and stSOL.

Sanctum’s universal LST liquidity pool enables large-scale experimentation in the liquid staking space.

5. How to Perform Liquid Staking

Now that you understand some options, let’s briefly go over how to do it. Taking bSOL as an example, simply go to stake.solblaze.org, click the “Stake” tab, and the following interface appears.

Remember, like most LSTs on Solana, bSOL accrues yield, so the amount of bSOL you receive is less than the SOL you deposit. Don’t be alarmed. In the image, you can see 0.8993 bSOL = 1 SOL. This is because 0.8993 bSOL represents a claim on BlazeStake’s liquid staking pool equivalent to 1 SOL—no value is lost. As the pool’s SOL holdings grow, this number continues to decrease, meaning each bSOL will entitle you to more SOL. Currently, 1 bSOL = 1.11 SOL, and this number will continue rising over time.

Select amount, click button, approve transaction, and done.

6. LSTs and DeFi

Now that we have a solid understanding of how LSTs work, know our options, and appreciate the benefits of different approaches, let’s explore DeFi opportunities. The entire point is to turn your staked tokens into productive, usable liquidity.

Let’s start with something relatively simple: lending.

Lending

One of the simplest and lowest-risk things you can do with an LST is lend it out. Platforms like MarginFi, Solend, and Kamino allow users to deposit collateral and borrow other assets of their choice. Cryptocurrencies are highly volatile, and all these platforms only offer over-collateralized loan positions. This means borrowers must provide collateral worth more than the value of the borrowed asset. This threshold varies based on perceived collateral quality. If the collateral value drops below a certain level, it gets liquidated to repay the loan.

Liquidation rules are complex and vary across projects. If you plan to commit significant capital, make sure you understand these mechanics thoroughly.

Typically, LST lending APY is relatively low because demand isn’t very high. Since the asset is already staked, the largest, lowest-risk yield opportunities are already captured. Still, you can safely earn some extra yield by lending it out, or potentially earn protocol rewards, making it a viable option.

Looping

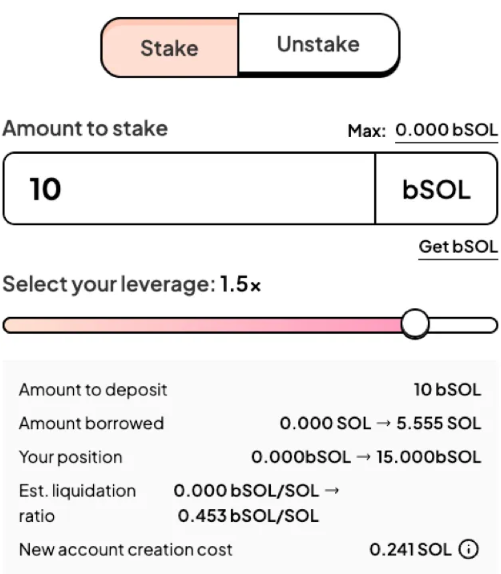

Now that we’ve discussed lending, let’s talk about what lending enables. Suppose you have 10 bSOL, currently advertising a 7.34% APY (remember, this fluctuates slightly each epoch), plus an additional 0.81% APY in BLZE emissions (dependent on BLZE price). How can you earn more? One way is to deposit those bSOL into a lending protocol, borrow more SOL, and then stake that SOL again with BlazeStake. Drift Protocol and Kamino Finance offer simple one-click products for this, with configurable leverage. You can also do this manually via protocols like Solend. A critical variable to watch is the SOL borrowing rate. The higher it is, the lower your net APY—because you must subtract it as a cost. Below is a quick example from Drift’s SuperStakeSOL UI.

In this example, you use 10 bSOL as collateral to borrow 5 SOL. You pay a 0.6% annual interest rate to borrow SOL, but then re-stake that SOL with bSOL to earn additional yield. As long as the borrowing rate is lower than the staking reward, this makes sense. Remember, you’re taking on risk here. The main risk is events like the mSOL “depeg” mentioned earlier. This can happen at any time because the mechanism linking its value to SOL has a duration component.

Providing Liquidity

Another way to boost LST yields is by providing liquidity. Decentralized exchanges rely on liquidity pools that allow token swaps. With enough such pools, you can route swaps across multiple pools to exchange any assets. Since USDC and SOL typically have the deepest liquidity, most routes pass through them—for example, swapping WIF to WHALES might involve first converting WIF to SOL, then SOL to WHALES.

Pools charge fees on swaps, which are distributed to liquidity providers (LPs). When trading is balanced—equal amounts of WIF and WHALES traded—the price stays stable, and LPs simply collect fees. These fees are justified due to impermanent loss risk. If demand shifts strongly toward WHALES, the pool’s WHALES decrease while WIF increases, eventually leaving LPs holding only depreciated WIF. This trend may reverse, hence the term “impermanent” loss, but it’s essential to keep in mind.

Which liquidity pools are attractive for LSTs? First, SOL-LST pools are popular because they support instant staking and unstaking. Second, LST1-LST2 pools are great—you hold two LSTs, both earning normal staking yields, plus a small cut of trading fees. You know their prices should stay highly correlated since both track SOL (though not pegged). Impermanent loss risk is low. Third, for higher risk and return, consider pools that let you swap LSTs for their protocol’s governance token, such as jitoSOL-JTO or bSOL-BLZE. These are often incentivized with extra governance token rewards to maintain decent liquidity.

I cannot stress enough the importance of understanding liquidity provision nuances. Different pools vary in how they allocate liquidity and how much control LPs have. Depending on how tokens trade, different approaches perform better or worse, so you need a solid mental model of how price action might unfold—and thus decide where to place liquidity for consistently good outcomes. For the first two options (SOL-LST, LST1-LST2), your mental model is basically “they’ll remain highly correlated,” making things simple. If you want to go deeper than simple options, I suggest starting small and observing how price action unfolds. Watch how pool balances shift with trading, how fees accumulate, and decide whether larger investments are worthwhile.

Some DeFi protocols, like Kamino, offer vaults with auto-managed LP strategies, so you don’t have to do much. They come with pre-built strategies for deploying funds into selected liquidity pools. Before using them, understand what they do—but this means you don’t have to manually enter pools or rebalance ranges. Of course, they charge a small fee.

These three combinations—lending, looping, and providing liquidity—don’t exhaust your LST options, but I don’t want this to become a thesis. If you haven’t tried all three, you might want to experiment carefully before diving deeper.

7. Conclusion

I hope this article has given you a solid understanding of liquid staking on Solana. The future of LSTs and DeFi on Solana looks promising, and the pace of innovation in this space is remarkable.

If you spot any errors in this article or feel I’ve misrepresented anything, I welcome feedback and am open to making corrections.

What’s amazing about Solana is that you can try nearly all of this with just $10. If you’re concerned about risks and whether you fully understand them, you can start cautiously and get a feel. Only you can assess your own risk tolerance and decide whether any given opportunity is worth pursuing.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News